Reports

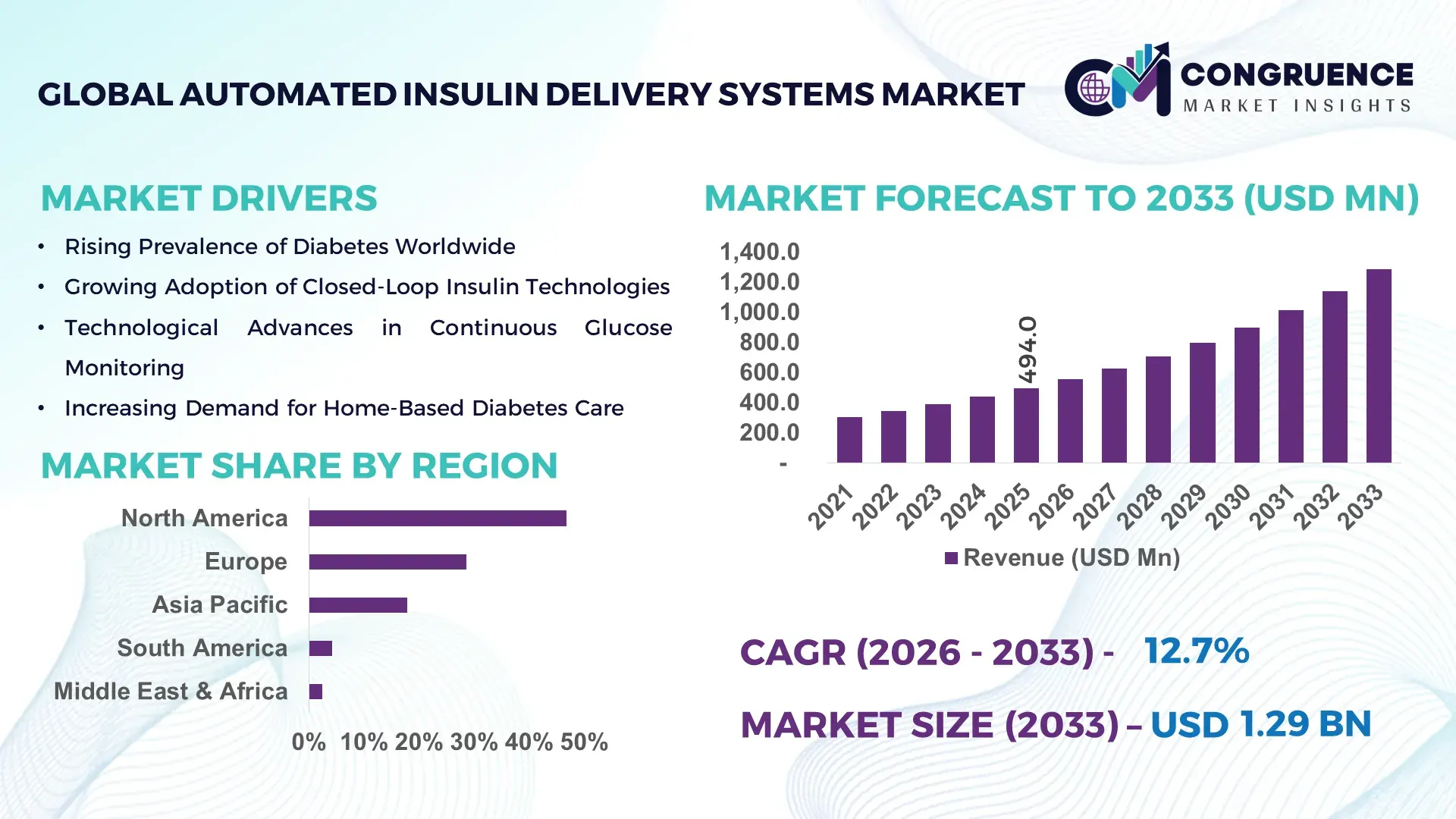

The Global Automated Insulin Delivery Systems Market was valued at USD 494.0 Million in 2025 and is anticipated to reach a value of USD 1,285.6 Million by 2033 expanding at a CAGR of 12.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily supported by rising diabetes prevalence, increasing penetration of closed-loop insulin delivery technologies, and continuous advancements in sensor-driven insulin automation.

The United States represents the dominant country within the global Automated Insulin Delivery Systems Market and serves as the primary innovation and deployment hub. The country accounts for more than 60% of global automated insulin pump production capacity, supported by large-scale manufacturing facilities operated by Medtronic, Insulet, Tandem Diabetes Care, and Abbott. Annual public and private investments in diabetes technology R&D in the U.S. exceed USD 4.5 billion, with automated insulin delivery platforms representing a major funding focus. Over 2.1 million patients in the U.S. actively use insulin pumps, and nearly 48% of pump users have transitioned to hybrid or fully automated systems. Regulatory clearance cycles are comparatively faster, with the FDA approving over 15 AID-related device upgrades between 2021 and 2024. Integration of AI-driven dosing algorithms, cloud-based glucose analytics, and smartphone-controlled insulin delivery has positioned the U.S. as the global benchmark for technological maturity and clinical deployment in this market.

Market Size & Growth: Valued at USD 494.0 Million in 2025, projected to reach USD 1,285.6 Million by 2033, driven by rising Type 1 diabetes automation adoption and improved glycemic control outcomes.

Top Growth Drivers: Automated pump adoption +34%, CGM integration +41%, reduction in hypoglycemic events +27%.

Short-Term Forecast: By 2028, automated dosing algorithms are expected to improve time-in-range glucose metrics by 18%.

Emerging Technologies: AI-based insulin algorithms, interoperable CGM-pump platforms, smartphone-controlled dosing systems.

Regional Leaders: North America USD 620 Million, Europe USD 410 Million, Asia Pacific USD 255 Million by 2033, with Europe leading pediatric adoption growth.

Consumer/End-User Trends: Adult Type 1 diabetics represent 62% of users; pediatric adoption exceeds 21% in developed markets.

Pilot or Case Example: In 2024, a U.S. hospital network reported a 22% reduction in diabetes-related inpatient complications using closed-loop systems.

Competitive Landscape: Medtronic (~34%), Insulet, Tandem Diabetes Care, Roche, Ypsomed.

Regulatory & ESG Impact: FDA interoperability standards and EU MDR compliance accelerating safer device rollouts.

Investment & Funding Patterns: Over USD 6.8 Billion invested globally since 2021 across device innovation and digital integration.

Innovation & Future Outlook: Expansion toward fully autonomous insulin delivery with AI-assisted learning models.

The Automated Insulin Delivery Systems Market is shaped by endocrinology clinics (42%), hospital diabetes programs (31%), and homecare settings (27%). Recent innovations include adaptive basal-rate algorithms, tubeless patch pumps, and extended-wear CGMs. Regulatory approvals, rising healthcare expenditure, and higher insulin-dependent diabetes diagnosis rates in North America and Europe continue to influence consumption patterns, while Asia Pacific shows accelerated future adoption.

The Automated Insulin Delivery Systems Market holds strong strategic relevance as healthcare systems increasingly prioritize outcome-based diabetes management, cost efficiency, and long-term complication reduction. Automated insulin delivery platforms reduce manual intervention and improve patient adherence, delivering measurable clinical improvements. For example, AI-based insulin dosing algorithms deliver approximately 25% better glycemic stability compared to conventional sensor-augmented pumps. North America dominates in device volume deployment, while Europe leads in structured adoption with over 44% of insulin pump users utilizing hybrid closed-loop systems.

By 2028, AI-enabled adaptive learning systems are expected to reduce severe hypoglycemic episodes by 30%, improving patient safety and lowering emergency care utilization. ESG considerations are gaining traction, with manufacturers committing to 20–25% reductions in device-related plastic waste by 2030 through recyclable cartridge systems and extended-use sensors. In 2024, Tandem Diabetes Care in the U.S. achieved a 19% improvement in patient time-in-range metrics through AI-enhanced Control-IQ algorithm upgrades.

Looking forward, integration with digital health platforms, interoperability mandates, and personalized insulin profiling will further strengthen market resilience. The Automated Insulin Delivery Systems Market is increasingly positioned as a cornerstone of sustainable, compliant, and technology-driven diabetes care worldwide.

The Automated Insulin Delivery Systems Market is driven by technological convergence between insulin pumps, continuous glucose monitoring, and artificial intelligence. Rising diabetes incidence, particularly Type 1 diabetes, and the clinical shift toward automation-based disease management continue to influence demand patterns. Healthcare providers increasingly favor closed-loop systems due to reduced clinician workload and improved patient outcomes. Regulatory frameworks in North America and Europe are evolving to support interoperable devices, while reimbursement coverage expansion plays a critical role in adoption. Meanwhile, manufacturing innovation and digital connectivity are reshaping product design and deployment models globally.

Precision diabetes management is a core growth driver for the Automated Insulin Delivery Systems Market. Automated systems enable continuous insulin adjustments based on real-time glucose data, reducing variability and improving clinical outcomes. Studies indicate that users experience up to 17% improvement in glucose time-in-range compared to manual pump therapy. Hospitals and endocrinology centers are increasingly recommending automated systems for newly diagnosed Type 1 diabetes patients, particularly in North America and Western Europe, where adoption rates exceed 45% among pump users.

High upfront device costs and recurring expenses for sensors and consumables present a significant restraint. Annual system costs can exceed USD 6,000 per patient, limiting adoption in price-sensitive regions. In emerging economies, limited insurance coverage further constrains access. Device replacement cycles and calibration requirements also increase long-term financial burden for patients and healthcare providers.

Integration with digital health platforms offers strong growth opportunities. Cloud-based analytics, telemedicine compatibility, and smartphone-controlled dosing expand patient reach and improve therapy monitoring. Remote data sharing enables clinicians to optimize insulin regimens, reducing hospital visits by up to 28%. Emerging markets adopting telehealth infrastructure are expected to accelerate system deployment.

Regulatory heterogeneity across regions complicates global commercialization. Compliance with FDA, EU MDR, and country-specific medical device standards increases development timelines. Interoperability challenges between CGMs and pumps from different manufacturers further delay adoption. Cybersecurity and data privacy concerns also require additional compliance investments.

Expansion of Fully Closed-Loop Systems: Fully automated insulin delivery systems are gaining traction, with clinical trials reporting up to 32% reduction in nocturnal hypoglycemia and improved overnight glucose control. Adoption is strongest in North America, where regulatory approvals support faster commercialization.

AI-Driven Adaptive Algorithms: Machine-learning-based insulin dosing models are improving personalization. New algorithms demonstrate 18–22% faster glucose stabilization during post-meal periods compared to rule-based systems.

Growth of Tubeless Patch Pumps: Tubeless systems now account for over 29% of new pump initiations, driven by patient preference for discreet and wearable designs. Pediatric adoption rates exceed 35% in developed markets.

Increased Pediatric and Geriatric Adoption: Automated systems are increasingly prescribed to children and elderly patients, with studies showing 24% reduction in caregiver intervention time and improved therapy adherence across age groups.

The Automated Insulin Delivery Systems Market is segmented based on type, application, and end-user, reflecting the diversity of technologies and care settings driving adoption. By type, the market spans hybrid closed-loop systems, fully closed-loop systems, and sensor-augmented pump systems, each addressing different levels of automation and clinical complexity. Applications range from Type 1 diabetes management to insulin-dependent Type 2 diabetes and hospital-based glycemic control, with varying adoption intensity depending on reimbursement structures and clinical protocols. End-user segmentation highlights hospitals and clinics, homecare settings, and specialty diabetes centers, underscoring the shift toward decentralized and patient-centric care. Increasing digital health integration, broader CGM compatibility, and clinician preference for automated dosing solutions are reshaping segmentation dynamics globally. Decision-makers increasingly evaluate systems based on interoperability, ease of use, and patient outcomes rather than standalone device performance.

The market by type is led by Hybrid Closed-Loop (HCL) Systems, which currently account for approximately 52% of overall adoption. These systems combine automated basal insulin delivery with user-initiated bolus dosing, offering a balance between automation and user control. Their leadership is supported by strong clinician familiarity, regulatory approvals across major markets, and demonstrated improvements of 15–20% in time-in-range glucose control compared to sensor-augmented pumps.

Fully Closed-Loop Systems represent the fastest-growing type, expanding at an estimated 15.4% CAGR, driven by advances in AI-driven algorithms, faster CGM response times, and reduced calibration requirements. These systems eliminate manual bolus input, appealing to pediatric and elderly populations where adherence is critical.

Sensor-Augmented Pump Systems and Other Emerging Configurations together contribute a combined 23% share, maintaining relevance in cost-sensitive markets and early-stage automation adoption scenarios, particularly where reimbursement for full automation remains limited.

In 2025, a national diabetes research program reported clinical deployment of fully closed-loop insulin delivery in public hospitals, reducing overnight hypoglycemia incidents by over 30% among trial participants.

Type 1 Diabetes Management is the leading application segment, accounting for nearly 61% of total system utilization, as automation is clinically recommended for intensive insulin therapy. High daily insulin variability and lifelong dependency make automated delivery especially valuable in this group. In comparison, insulin-dependent Type 2 diabetes applications represent about 24%, while hospital and perioperative glycemic management accounts for the remaining 15%.

The fastest-growing application is Type 2 diabetes automation, expanding at approximately 13.1% CAGR, supported by rising insulin initiation rates, aging populations, and growing evidence that automated dosing improves adherence and reduces clinician intervention.

Consumer adoption data reinforces this trend: in 2025, around 39% of insulin-dependent Type 2 patients in developed markets were enrolled in pilot automated delivery programs, while over 46% of endocrinologists reported increased prescribing of AID systems beyond Type 1 patients.

In 2024, a large-scale public health deployment introduced automated insulin delivery across more than 120 hospitals, improving inpatient glucose stability for over 1.5 million patient-days annually.

Homecare and Individual Patient Use is the dominant end-user segment, accounting for approximately 58% of total adoption, reflecting the shift toward self-managed, connected diabetes care. Patients increasingly prefer home-based systems due to reduced hospital visits, real-time monitoring, and smartphone integration. Hospitals and Clinics follow with about 27% share, driven by inpatient glycemic control protocols and post-discharge continuity programs.

The fastest-growing end-user segment is specialty diabetes centers, expanding at an estimated 14.2% CAGR, fueled by structured education programs, technology-assisted monitoring, and value-based care models. Other end-users, including long-term care facilities and research institutions, collectively represent 15% of adoption, playing a key role in pilot testing and clinical validation.

Adoption indicators show that over 42% of U.S. hospitals are actively testing or using automated insulin delivery for complex diabetes cases, while nearly 55% of digitally engaged patients report higher confidence in managing glucose levels with automated systems.

In 2025, a national healthcare system reported that specialty diabetes clinics using automated insulin delivery achieved a 21% reduction in emergency glycemic events within one year of implementation.

North America accounted for the largest market share at 46.8% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.9% between 2026 and 2033.

North America’s leadership is supported by high insulin pump penetration, where over 62% of insulin-dependent Type 1 diabetes patients use pump-based therapy, and nearly 48% of these users have adopted automated or hybrid closed-loop systems. Europe follows with a 28.6% share, driven by structured reimbursement models and national diabetes programs. Asia-Pacific currently represents 17.9% of global adoption but shows accelerating uptake due to rising diabetes prevalence, which exceeds 206 million diagnosed cases across the region, alongside expanding middle-class healthcare access. South America and the Middle East & Africa together contribute 6.7%, reflecting early-stage adoption supported by pilot programs and gradual policy alignment.

The region holds approximately 46.8% of the global Automated Insulin Delivery Systems Market, making it the largest contributor by volume and installed base. Demand is driven primarily by endocrinology clinics, hospital diabetes programs, and homecare settings, with home-based usage accounting for nearly 60% of active systems. Regulatory frameworks favor innovation, with streamlined device interoperability approvals and expanded reimbursement coverage across public and private insurers. Technological trends include AI-driven dosing algorithms, smartphone-controlled pumps, and cloud-based glucose analytics, with over 70% of new systems launched supporting mobile integration. A prominent regional player has expanded manufacturing capacity by over 20% since 2023 to meet domestic demand. Consumer behavior reflects high digital readiness, as more than 55% of insulin pump users prefer fully or semi-automated therapy to reduce daily disease management burden.

Europe accounts for around 28.6% of the global market, with Germany, the UK, and France collectively contributing over 64% of regional installations. Adoption is strongly influenced by national health systems and regulatory bodies emphasizing safety, transparency, and clinical validation. Pediatric and adolescent usage is notably high, with automated systems used by approximately 41% of insulin-dependent patients under 18 in Western Europe. Emerging technologies such as interoperable CGM-pump ecosystems and explainable dosing algorithms are gaining traction due to regulatory expectations. A regional manufacturer has focused on modular pump designs compatible with multiple CGM brands, supporting wider adoption. Consumer behavior shows that European users prioritize clinically validated, regulator-approved systems, leading to longer device retention cycles and higher adherence rates.

Asia-Pacific ranks third by current volume but leads in growth momentum, accounting for 17.9% of global adoption. China, Japan, and India represent the largest consumption bases, collectively housing over 60% of insulin-dependent diabetes patients in the region. Infrastructure expansion, domestic manufacturing of insulin pumps, and growing digital health ecosystems are key trends. Japan shows the highest penetration of automated systems in hospitals, while China leads in locally manufactured pump deployment. A regional technology firm has scaled production to supply over 150,000 units annually, targeting affordability. Consumer behavior is shaped by mobile-first healthcare delivery, with over 45% of new users engaging with app-based glucose monitoring platforms, accelerating acceptance of automation.

South America contributes approximately 4.2% of global adoption, with Brazil and Argentina accounting for nearly 68% of regional demand. Public healthcare reforms and urban diabetes clinics are expanding access to insulin technologies, particularly in metropolitan areas. Infrastructure improvements and reduced import tariffs on medical devices have lowered entry barriers. A regional distributor has partnered with public hospitals to deploy automated systems in over 120 diabetes centers. Consumer behavior varies widely, but urban patients show higher acceptance, with nearly 38% of pump users expressing interest in transitioning to automated delivery when reimbursement is available.

This region represents about 2.5% of global adoption, led by the UAE, Saudi Arabia, and South Africa. Demand is concentrated in private healthcare networks and government-backed specialty diabetes centers. Technological modernization initiatives and cross-border trade partnerships support device imports and pilot deployments. In the Gulf states, automated insulin delivery is used by nearly 29% of insulin pump users, significantly higher than the regional average. A local healthcare group has launched a diabetes digital care program integrating automated pumps with tele-endocrinology services. Consumer behavior shows strong preference for premium, digitally integrated devices among insured populations.

United States – 39.4% Market Share: High production capacity, strong reimbursement coverage, and widespread adoption across homecare and clinical settings drive leadership in the Automated Insulin Delivery Systems Market.

Germany – 11.2% Market Share: Robust public healthcare infrastructure, structured diabetes management programs, and early adoption of regulated automated insulin delivery technologies support its leading position.

The Automated Insulin Delivery Systems Market exhibits a moderately consolidated competitive environment with 20+ active competitors globally ranging from established medical device manufacturers to emerging innovators in diabetes care. The top 5 companies collectively command approximately 68–72% share of installed automated insulin delivery systems, reflecting significant concentration among leading players while allowing space for niche and technology-focused entrants. Major incumbents like Medtronic continue to dominate hybrid closed-loop and interoperable pump platforms with over 200,000 users of its MiniMed™ 780G advanced system worldwide. Insulet Corporation’s Omnipod® 5 is a key competitor with a strong 35% share of the U.S. insulin pump market, driving tubeless automated delivery adoption. Tandem Diabetes Care remains pivotal with its t:slim X2 and Control-IQ platforms and expanded indications for Type 2 diabetes use. Strategic initiatives include interoperability-focused regulatory submissions, expanded CGM integration agreements, and dual glucose-ketone sensor collaborations that enhance safety and clinical utility in AID ecosystems. Innovation trends center on cloud connectivity, AI-assisted dosing algorithms, and wearable automation designed for patient convenience and reduced clinical burden. The competitive landscape is shaped by frequent product updates, algorithmic enhancements, and strategic partnerships aimed at broadening patient access, improving regulatory alignment, and sustaining differentiation in a rapidly evolving healthcare technology sector.

Dexcom, Inc.

Abbott Laboratories

Beta Bionics

F. Hoffmann-La Roche Ltd.

Ypsomed Holding AG

Novo Nordisk A/S

Sanofi S.A.

Eli Lilly and Company

Embecta (BD)

CeQur Simplicity

Terumo Corporation

The Automated Insulin Delivery Systems Market is at the forefront of integrating advanced technologies that blend hardware innovation with sophisticated digital capabilities. Core system components now routinely combine continuous glucose monitoring (CGM) with next-generation insulin pumps and software algorithms capable of predictive insulin dosing and meal anticipation functions. Current mainstream technologies in AID platforms include hybrid closed-loop systems with automated basal adjustments informed by real-time glucose readings every five minutes and algorithms built to minimize hypo- and hyperglycemic excursions. Connectivity enhancements, such as smartphone control, cloud-based data sharing, and remote clinician access, are becoming standard, improving adherence and patient-clinician engagement.

Emerging technology trends emphasize interoperability, enabling CGMs from different manufacturers to interface seamlessly with automated pump systems, expanding patient choice and enhancing ecosystem flexibility. Innovative sensor technologies, including dual glucose-ketone sensing, are under joint development by major players to identify critical biomarkers like early ketone rises for timely intervention, broadening clinical utility. AI and machine learning are increasingly integrated into dosing algorithms to refine personalization based on individual glucose patterns, activity levels, and insulin sensitivity variations. Telehealth convergence permits remote monitoring and diabetes management support, particularly important in decentralized care models and regions with limited specialty care access. Research initiatives also explore digital twin frameworks and reinforcement learning controllers to simulate physiological responses and optimize glycemic control. These technological trajectories underscore a shift toward highly automated, user-centric solutions that reduce patient burden, improve metabolic outcomes, and support population health objectives across diverse clinical settings.

• In February 2025, Tandem Diabetes Care received expanded FDA clearance for its Control-IQ+ automated insulin delivery algorithm to be used with Tandem’s t:slim X2 and Mobi pumps in people with Type 2 diabetes, increasing access to automated delivery. Source: www.medtechdive.com

• In June 2025, Tandem Diabetes Care announced a collaboration with Abbott to integrate a future dual glucose-ketone sensor with Tandem’s automated insulin delivery systems, aimed at early detection of diabetic ketoacidosis and enhanced patient outcomes. Source: www.investor.tandemdiabetes.com

• In January 2025, Insulet launched the Omnipod® 5 Automated Insulin Delivery System in Italy, Denmark, Finland, Norway, and Sweden with compatibility for both Abbott FreeStyle Libre 2 Plus and Dexcom G6 CGM sensors, expanding European availability of tubeless AID solutions. Source: www.businesswire.com

• In April 2025, Medtronic submitted 510(k) applications to the FDA for an interoperable insulin pump and SmartGuard™ algorithm intended to integrate with Abbott’s advanced CGM platform, enhancing choice and interoperability in automated insulin delivery systems. Source: www.prnewswire.com

The Automated Insulin Delivery Systems Market Report provides a comprehensive evaluation of the current landscape and future directions of automated diabetes management technologies. It encompasses detailed segmentation across product types—such as hybrid closed-loop systems, fully autonomous systems in development, and sensor-augmented configurations—highlighting their clinical roles, adoption contexts, and technological differentiation. Geographic coverage extends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, enabling stakeholders to assess regional demand drivers, infrastructure readiness, and regulatory environments that shape deployment patterns. The report also analyzes application categories including intensive Type 1 diabetes management, insulin-dependent Type 2 therapy, and specialized inpatient protocols, with insights into usage intensity, clinician preferences, and patient behavior variations.

In addition, the document profiles major market participants and innovation ecosystems, emphasizing interoperability strategies, algorithmic advancements, and digital health integrations that enhance patient outcomes and system efficiencies. Technology insights cover next-generation sensor systems, AI-based predictive dosing, mobile connectivity, and dual biomarker detection tools poised to broaden clinical utility and safety. The scope also addresses emerging market niches, such as implantable automated insulin delivery prototypes, telehealth-enabled remote monitoring frameworks, and digital therapeutic adjuncts. Finally, the report discusses end-user segments—homecare, hospitals, specialty clinics—and offers decision-oriented analysis of competitive positioning, strategic initiatives, and industry trends critical to executives, investors, and healthcare planners assessing the future trajectory of automated insulin delivery solutions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 494.0 Million |

| Market Revenue (2033) | USD 1,285.6 Million |

| CAGR (2026–2033) | 12.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Medtronic Diabetes Solutions, Insulet Corporation, Tandem Diabetes Care, Inc., Dexcom, Inc., Abbott Laboratories, Beta Bionics, F. Hoffmann-La Roche Ltd., Ypsomed Holding AG, Novo Nordisk A/S, Sanofi S.A., Eli Lilly and Company, Embecta (BD), CeQur Simplicity, Terumo Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |