Reports

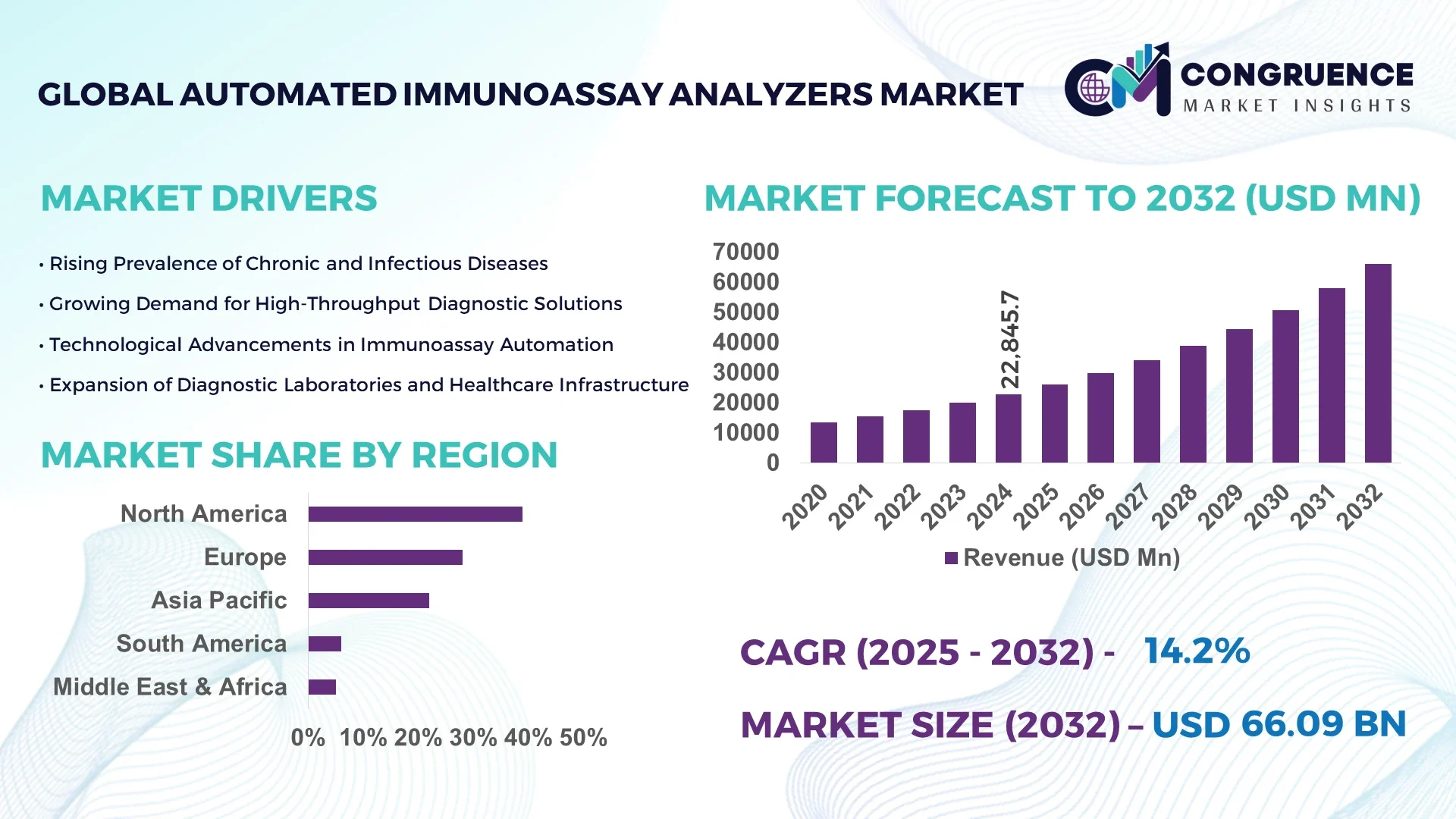

The Global Automated Immunoassay Analyzers Market was valued at USD 22,845.7 Million in 2024 and is anticipated to reach a value of USD 66,089.6 Million by 2032 expanding at a CAGR of 14.2% between 2025 and 2032.

The United States leads the Automated Immunoassay Analyzers Market with significant domestic manufacturing capacity, sustained R&D investment for high-throughput platforms, widespread adoption in clinical diagnostics, and deployment of advanced chemiluminescent and immunofluorescent modules.

The Automated Immunoassay Analyzers Market is increasingly propelled by rising prevalence of chronic and infectious diseases, encouraging widespread deployment in hospital labs, diagnostic centers, and reference facilities. Key sectors utilizing these instruments include infectious disease testing, oncology marker screening, and therapeutic drug monitoring. Innovations such as multiplex assay panels, enhanced sensitivity chemiluminescence detection (reaching below 1 pg/mL thresholds), and modular benchtop platforms are contributing to operational flexibility and performance improvements. Regulatory drivers promoting lab automation and accuracy continue to support growth, while economic investments in lab infrastructure in emerging markets are widening adoption. Emerging trends—such as predictive maintenance with sensor analytics and digital workflow integration—are redefining the future of the Automated Immunoassay Analyzers Market for healthcare decision-makers.

Artificial Intelligence is profoundly reshaping the Automated Immunoassay Analyzers Market by enhancing diagnostic precision, reducing manual intervention, and streamlining laboratory workflows. AI-powered algorithms analyze complex immunoassay signal patterns to distinguish true analyte peaks from noise, significantly lowering the incidence of false positives and accelerating result interpretation. Integration of machine learning into maintenance protocols enables analyzers to predict component wear and initiate service alerts—increasing uptime and enabling seamless throughput in high-volume labs.

Automation workflows now integrate AI-driven barcode verification, sample integrity checks, and digital protocol optimization—each step underpinned by the clarity and efficiency that AI brings to instrument operation. Labs report up to a 30% reduction in turnaround time for critical assays following AI implementation, while adoption of smart calibration routines ensures measurement consistency across extended testing cycles. Ultimately, these advances are amplifying diagnostic productivity and elevating analytical confidence in the Automated Immunoassay Analyzers Market.

“In late 2024, a global diagnostics provider deployed an AI-based readout system in its chemiluminescent immunoassay line, resulting in a 20 % reduction in test result ambiguity and a 15 % increase in throughput during clinical evaluation.”

The Automated Immunoassay Analyzers Market is evolving amid shifting healthcare demands, regulatory mandates, and technological innovation. Laboratory automation is becoming essential in managing growing test volumes and minimizing manual error. Diagnostic labs are increasing investments in walkaway systems capable of handling diverse panels, reducing staff burdens and increasing capacity. At the same time, demand for decentralized testing—at point-of-care and smaller clinics—is driving development of compact benchtop models supporting multiplex immunoassays. Regulatory and reimbursement standards that prioritize rapid, reliable diagnostics are reinforcing adoption, especially in developed economies. Environmental considerations—such as reduced reagent consumption via multiplex formats—are further influencing new platform designs. In combination, these dynamics are steering the Automated Immunoassay Analyzers Market toward smarter, more efficient solutions that align with clinical and operational demands.

Escalating rates of chronic illnesses like diabetes, cardiovascular disease, cancer, and autoimmune disorders are generating sustained demand for routine immunoassay testing. Also, frequent outbreaks of infectious diseases (e.g., influenza, SARS-CoV-2) increase reliance on high-throughput immunoassay analyzers for rapid diagnosis and mass screening. These pressures are expanding lab utilization, especially in hospital and reference lab settings, bolstering ongoing investment in automated immunoassay systems capable of delivering rapid, reliable results.

A major restraint in the Automated Immunoassay Analyzers Market is the substantial upfront investment required to purchase and install fully automated analyzer platforms. For resource-constrained healthcare facilities or smaller laboratories, the initial cost—coupled with maintenance and consumable expenses—can be prohibitive. This limits broader deployment, especially in emerging markets, or forces reliance on legacy or semi-automated systems, constraining market penetration and adoption speed.

Compact benchtop immunoassay analyzers capable of multiplex testing present a significant opportunity. These instruments enable rapid, high-throughput testing in decentralized or smaller lab settings, requiring minimal space and staffing. Multiplex assays reduce reagent needs and deliver multi-biomarker readouts simultaneously—improving cost efficiency. As a result, diagnostics in outpatient clinics and regional labs become more feasible, expanding the Automated Immunoassay Analyzers Market beyond large-scale hospitals.

A notable challenge lies in achieving seamless interoperability between automated analyzers and existing Laboratory Information Systems (LIS). Diverse communication protocols, data formats, and integration requirements complicate installation, validation, and training workflows. Delays in interface development or inadequately integrated data flow can impair turnaround time, reduce accuracy, and hamper the full potential of automation in the lab environment. Resolving these integration complexities is essential for scaling analyzer adoption effectively.

• Enhanced Chemiluminescence Detection Sensitivity: Newly launched chemiluminescent systems now detect biomarkers at sub-1 pg/mL levels, substantially increasing analytic sensitivity and enabling earlier disease detection, especially in oncology and endocrine testing.

• Multiplex Assay Platforms: Multiplex immunoassay analyzers now simultaneously detect multiple biomarkers from a single sample—boosting efficiency by up to 60% and reducing assay turnaround in high-volume settings.

• Compact Benchtop Analyzer Adoption: Smaller, automated benchtop models are being embraced by outpatient clinics and regional labs, offering high-throughput capabilities without the footprint of traditional floor-standing systems.

• AI-Driven Operational Analytics: Integration of AI-powered analytics into analyzers allows real-time error detection, reagent depletion alerts, and predictive maintenance scheduling—enhancing operational reliability.

The Automated Immunoassay Analyzers Market is segmented by product type (benchtop vs. floor-standing), detection technology (chemiluminescence, immunofluorescence, ELISA variants), applications (infectious diseases, chronic condition testing, oncology panels, therapeutic drug monitoring), and end-user categories (hospitals, diagnostic laboratories, point-of-care centers). Floor-standing systems dominate large hospital and reference labs due to higher throughput, while benchtop systems are gaining momentum in decentralized settings. Technologically, chemiluminescence remains the leading detection method for its speed and sensitivity. Applications in infectious disease and oncology drive volume, while end-user segmentation reflects hospital lab leadership, with growing adoption in ambulatory care, blood banks, and mobile testing units. These segmentation layers highlight where investments and strategic commercialization should focus.

Floor-standing high-throughput automated immunoassay analyzers continue to lead due to their capacity to serve large hospital and reference lab volumes with broad assay menus and walk-away operation. Benchtop systems are the fastest-growing type, gaining traction in decentralized and point-of-care environments due to their space efficiency, lower cost, and ability to perform multiplex testing. Hybrid modular systems offering scalability are emerging as niche segments for laboratories seeking flexible capacity expansion.

Infectious disease testing is the leading application area in the Automated Immunoassay Analyzers Market, driven by routine screening for pathogens such as influenza, HIV, and SARS-CoV-2. Oncology marker panels represent the fastest-growing application, as personalized medicine and biomarker-guided therapeutic monitoring expand. Other key applications include endocrine disorder screening and therapeutic drug monitoring, where rapid and accurate quantification is critical. This diversity in applications underlines the analyzers’ expanding clinical utility.

Hospitals account for the largest end-user segment in the Automated Immunoassay Analyzers Market, leveraging their scale and clinical testing demands. The fastest-growing end-user segment is point-of-care and decentralized diagnostic centers, adopting compact benchtop systems to deliver rapid results at or near the patient. Other contributors include diagnostic laboratories and blood banks requiring high-throughput capabilities. The evolving landscape underscores a shift toward more distributed, diagnostic-ready environments beyond traditional clinical labs.

North America accounted for the largest market share at 39% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.1% between 2025 and 2032.

North America’s dominance is driven by robust diagnostic infrastructure, higher adoption of automated analyzers, and early integration of AI technologies into laboratory workflows. Meanwhile, Asia-Pacific’s rapid growth is supported by expanding healthcare spending in China and India, strengthening hospital networks, and strong demand for decentralized diagnostic systems. Europe held a solid share of approximately 28% in 2024, with strong uptake in Germany, France, and the UK supported by regulatory focus on lab automation. Other regions such as South America and the Middle East & Africa are gaining momentum, propelled by rising healthcare investments, improving clinical laboratory capacities, and gradual digitalization of diagnostic systems. Collectively, these regional dynamics reveal a diverse but highly promising global growth outlook.

Technological Integration Driving Diagnostic Precision

North America commanded nearly 39% of the Automated Immunoassay Analyzers Market in 2024, underpinned by strong demand from hospitals, reference laboratories, and point-of-care facilities. Key industries driving this demand include oncology diagnostics, infectious disease testing, and therapeutic drug monitoring. Regulatory initiatives such as accelerated FDA approvals for diagnostic platforms and government investments in healthcare infrastructure have bolstered market penetration. Technological innovations—such as chemiluminescence analyzers with AI-based error detection and enhanced throughput—are enabling laboratories to manage higher test volumes with greater accuracy. Digital transformation trends, including integration with Laboratory Information Systems and cloud-based data management, are reshaping operational efficiencies across the region.

Rising Adoption of Multiplexed Diagnostic Platforms

Europe accounted for approximately 28% of the Automated Immunoassay Analyzers Market in 2024, with Germany, France, and the UK emerging as primary hubs of adoption. The region’s market is strongly shaped by the European Medicines Agency’s regulatory frameworks and national-level healthcare digitization programs. Sustainability initiatives—focused on reducing reagent waste and improving energy efficiency in diagnostic labs—are influencing product preferences. Adoption of emerging technologies such as multiplex immunoassay panels and compact benchtop analyzers is expanding, particularly in outpatient and decentralized care facilities. Collaborative innovation hubs across Germany and the UK are further fueling research and integration of precision diagnostic solutions.

Expanding Healthcare Infrastructure Driving Demand

Asia-Pacific held nearly 22% of the Automated Immunoassay Analyzers Market in 2024 and ranked as the fastest-growing regional segment. China, India, and Japan are the top consumers, supported by rapidly expanding healthcare infrastructure and growing investments in clinical laboratory networks. Demand is being accelerated by large-scale public health programs, increasing chronic disease burden, and growing medical tourism. Manufacturing hubs in China and South Korea are playing an instrumental role in scaling production and reducing costs. Regional technology trends such as AI-assisted diagnostics and cloud-based monitoring platforms are accelerating adoption in high-population markets, while innovation centers in Japan continue to push advancements in next-generation analyzer technologies.

Government Programs Supporting Diagnostic Expansion

South America represented close to 6% of the Automated Immunoassay Analyzers Market in 2024, led primarily by Brazil and Argentina. Growing investments in healthcare infrastructure and diagnostic laboratories are fueling market expansion. Public health initiatives to strengthen infectious disease testing and oncology diagnostics are reinforcing demand for automated systems. Regional governments are introducing tax incentives and trade policies to attract medical device manufacturers, particularly in Brazil. Infrastructure development, combined with private sector expansion of diagnostic centers, is opening new opportunities. Adoption of modular and cost-effective benchtop analyzers is particularly rising in secondary cities with underserved healthcare networks.

Healthcare Modernization Driving Analyzer Deployment

The Middle East & Africa accounted for around 5% of the Automated Immunoassay Analyzers Market in 2024, with notable demand growth in the UAE, Saudi Arabia, and South Africa. Rising demand is fueled by healthcare modernization programs, particularly in the GCC states, where public and private investments are expanding hospital and laboratory networks. Oil-driven economies are channeling resources into high-tech healthcare infrastructure, encouraging adoption of automated analyzers. Technological modernization—such as integration of smart calibration systems and IoT-enabled monitoring—supports laboratory efficiency. Local regulatory harmonization efforts and trade partnerships are improving access to diagnostic technologies across the wider region.

United States – 27% market share

Strong dominance due to advanced diagnostic infrastructure, high production capacity, and rapid integration of AI-enabled immunoassay technologies.

China – 14% market share

Leadership supported by large patient population, fast-growing healthcare spending, and rising adoption of automated diagnostic systems in both public and private laboratories.

The Automated Immunoassay Analyzers Market is highly competitive, with more than 45 global and regional players actively engaged in product development and commercialization. Market leaders maintain strong positioning through comprehensive product portfolios, advanced detection technologies, and established distribution networks across hospitals and diagnostic labs. Companies are focusing on partnerships with healthcare providers, mergers to consolidate market presence, and product launches to expand assay menus. Innovation trends, particularly AI-driven system integration and multiplex assay capabilities, are becoming decisive factors in competitive differentiation. Smaller players are targeting niche opportunities in benchtop analyzers and point-of-care settings, while established firms emphasize large-scale, fully automated systems. Competitive intensity remains high, with emphasis on both technological superiority and cost-efficient solutions.

Abbott Laboratories

Siemens Healthineers

Roche Diagnostics

bioMérieux SA

Beckman Coulter Inc.

Ortho Clinical Diagnostics

Mindray Medical International

Randox Laboratories

Tosoh Corporation

SNIBE Diagnostics

Technological evolution is central to the Automated Immunoassay Analyzers Market, with current innovations improving both analytical sensitivity and operational efficiency. Chemiluminescence detection systems dominate, offering sensitivity below 1 pg/mL, enabling earlier detection of cancer biomarkers and infectious agents. Immunofluorescence-based systems are gaining traction for their speed and suitability for point-of-care deployment. Multiplex assay platforms now allow simultaneous measurement of up to 20 biomarkers from a single sample, cutting reagent use and turnaround times by more than 40%.

Digital integration is also transforming workflows, with cloud-based monitoring platforms enabling remote system diagnostics, predictive maintenance, and real-time data analytics. Robotics-driven automation in sample loading and reagent handling reduces operator error and maximizes throughput. AI-enabled image and signal processing ensures accurate result interpretation and minimizes retesting. Compact benchtop analyzers are increasingly incorporating modular scalability, making them suitable for both small diagnostic centers and large laboratories. Future technological advancements are likely to converge around miniaturization, digital twin modeling for performance simulation, and integration with telemedicine platforms to expand diagnostic reach.

In March 2023, Roche launched a next-generation immunoassay analyzer with enhanced throughput, capable of processing over 600 tests per hour, significantly improving laboratory efficiency for large hospitals.

In August 2023, Abbott introduced a compact benchtop immunoassay system designed for decentralized laboratories, reducing space requirements while maintaining high accuracy across multiple assay types.

In February 2024, Siemens Healthineers integrated AI-driven calibration into its immunoassay analyzers, enabling predictive maintenance and a 15% increase in operational uptime during clinical evaluations.

In June 2024, bioMérieux unveiled an automated multiplex immunoassay analyzer supporting simultaneous detection of 15 biomarkers, reducing test turnaround time by nearly 45% compared to traditional single-analyte systems.

The Automated Immunoassay Analyzers Market Report provides comprehensive coverage of market segments, applications, and geographic regions influencing global adoption. Segmentation spans analyzer types (floor-standing, benchtop, and modular systems), detection technologies (chemiluminescence, immunofluorescence, ELISA derivatives, multiplex assays), and end-users (hospitals, diagnostic laboratories, point-of-care centers, and blood banks). Application areas include infectious disease testing, oncology biomarkers, therapeutic drug monitoring, and endocrine disorder screening.

Geographically, the report assesses North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional strengths, infrastructure development, and consumption patterns. The analysis also emphasizes technological advancements such as AI integration, robotics, digital connectivity, and miniaturized platforms that are reshaping the diagnostic landscape.

Beyond established domains, the report explores emerging niches such as decentralized diagnostics, personalized medicine applications, and mobile diagnostic units. It also incorporates regulatory, environmental, and economic considerations shaping market adoption globally. Designed for decision-makers, this report delivers precise, actionable insights into the breadth, depth, and evolving trajectory of the Automated Immunoassay Analyzers Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 22,845.7 Million |

|

Market Revenue in 2032 |

USD 66,089.6 Million |

|

CAGR (2025 - 2032) |

14.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Abbott Laboratories, Siemens Healthineers, Roche Diagnostics, bioMérieux SA, Beckman Coulter Inc., Ortho Clinical Diagnostics, Mindray Medical International, Randox Laboratories, Tosoh Corporation, SNIBE Diagnostics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |