Reports

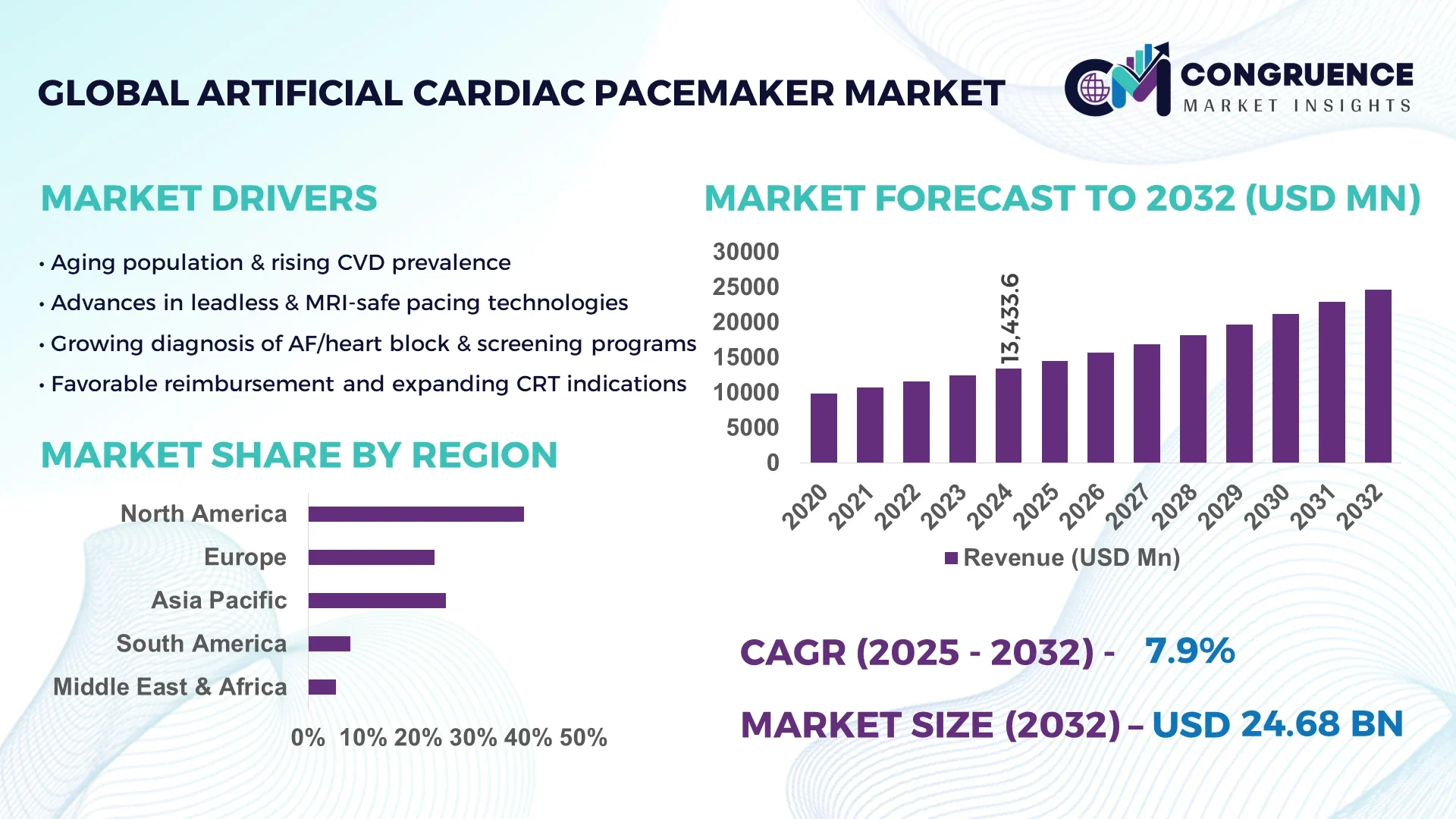

The Global Artificial Cardiac Pacemaker Market was valued at USD 13,433.55 Million in 2024 and is anticipated to reach a value of USD 24,680.97 Million by 2032 expanding at a CAGR of 7.9% between 2025 and 2032.

In the United States, advanced manufacturing capabilities, significant R&D investments, and integration of precision-engineered devices into electrophysiology labs have bolstered the domestic production of artificial cardiac pacemakers. The U.S. also leads in clinical implementation of AI-assisted pacemaker programming systems.

The artificial cardiac pacemaker market continues to gain momentum as demand surges across key sectors, including hospitals, specialty cardiac centers, and ambulatory surgical units. These sectors are increasingly adopting dual-chamber and MRI-compatible pacemakers due to growing cases of atrioventricular block and sinus node dysfunction. Technological innovation remains central to the market, with miniaturized leadless pacemakers and rechargeable battery systems gaining traction. Furthermore, the market is being reshaped by regulatory harmonization and favorable reimbursement frameworks across North America and Europe. Environmental pressures are pushing for sustainable production practices in pacemaker manufacturing, prompting firms to innovate in biocompatible materials. Regionally, Asia-Pacific is witnessing rising procedural volumes due to an aging population and lifestyle-related cardiac disorders, thereby influencing global consumption trends. Looking forward, remote monitoring technologies and AI-based pacing algorithms are expected to define future product development strategies.

AI is significantly reshaping the Artificial Cardiac Pacemaker Market by introducing intelligent systems that optimize device performance, personalize patient therapy, and enhance real-time diagnostics. AI-driven algorithms now enable predictive modeling for arrhythmia detection and automate parameter adjustments based on individual heart rhythms, minimizing the need for frequent manual reprogramming. This capability not only extends battery life but also improves the clinical effectiveness of pacemakers. Hospitals and cardiac centers are leveraging AI-integrated platforms to streamline the follow-up process, reduce complications, and detect anomalies through continuous monitoring via cloud-connected devices.

In surgical procedures, AI supports pre-operative planning through enhanced imaging analytics, allowing clinicians to determine the optimal placement and device configuration. Additionally, AI facilitates remote device management, enabling physicians to access patient data in real-time and intervene promptly, reducing hospital readmissions. The integration of machine learning models into pacemaker design is also enabling smarter data interpretation and improving diagnostic yield from device-stored cardiac events. These advancements in the Artificial Cardiac Pacemaker Market are promoting the adoption of next-generation implantable devices and fostering innovation across the supply chain, from design to post-operative care. As a result, AI is becoming an indispensable tool for manufacturers and healthcare providers focused on elevating outcomes and operational efficiency.

“In 2024, Medtronic launched an AI-based update for its Micra AV leadless pacemaker, incorporating real-time adaptive pacing algorithms that increased atrioventricular synchrony accuracy by 22% in clinical trials, improving patient responsiveness and reducing sync loss events.”

The Artificial Cardiac Pacemaker Market is undergoing dynamic transformation driven by rising incidences of cardiac arrhythmias, technological advancements, and increased adoption of minimally invasive procedures. The expanding geriatric population across developed and emerging economies is fueling demand for implantable cardiac devices that ensure efficient heart rhythm management. In parallel, the market is benefiting from favorable regulatory reforms, particularly in the U.S., Europe, and Japan, where device approvals and reimbursements are becoming more streamlined. Key market trends include the shift toward leadless pacemakers, wireless communication features, and cloud-based remote monitoring solutions. Additionally, growing awareness among patients and physicians, alongside advancements in digital health infrastructure, is driving up the implantation rates. These evolving dynamics position the Artificial Cardiac Pacemaker Market for continued innovation and growth, particularly in regions investing in digital cardiology and AI-enabled healthcare ecosystems.

Continuous advancements in pacemaker technology are significantly influencing the Artificial Cardiac Pacemaker Market by improving clinical outcomes and patient quality of life. Innovations such as leadless pacemakers, wireless telemetry, and enhanced power systems have drastically minimized complication rates associated with traditional devices. For example, newer pacemaker models now utilize multi-sensor feedback to optimize pacing based on physiological conditions in real time. Furthermore, rechargeable batteries and improved biocompatibility reduce the frequency of surgical interventions. With manufacturers incorporating adaptive pacing algorithms and Bluetooth-enabled monitoring, physicians can remotely program and monitor pacemaker performance. This not only facilitates quicker intervention but also improves treatment adherence and patient satisfaction, expanding the clinical applicability of advanced pacemakers.

Despite technological progress, the Artificial Cardiac Pacemaker Market faces significant restraints due to high device and implantation costs. In many developing economies, public health systems are underfunded and unable to absorb the high upfront costs associated with pacemaker procedures, which can exceed USD 8,000 per patient. Moreover, ongoing maintenance expenses, including battery replacements and follow-up care, add to the financial burden. Insurance coverage gaps further deter adoption in lower-income populations. These cost barriers contribute to underutilization of life-saving pacemaker therapy in regions such as Sub-Saharan Africa and parts of Southeast Asia, where healthcare infrastructure and economic resources are limited. As a result, market penetration remains uneven across geographies.

The shift toward minimally invasive cardiac procedures presents a strong opportunity in the Artificial Cardiac Pacemaker Market. Leadless pacemakers, which can be implanted via a catheter-based approach without surgical incisions, are gaining widespread acceptance due to reduced procedural risks, shorter recovery times, and lower infection rates. As patient preference for less-invasive treatment options increases, manufacturers are expanding portfolios to include smaller, smarter, and more energy-efficient devices. Additionally, emerging markets such as India, Brazil, and the UAE are investing in upgrading cardiology departments with advanced diagnostic and implant capabilities. This demand for innovation in procedural efficiency is driving global procurement of next-generation artificial pacemakers, opening new revenue streams for industry players.

A critical challenge facing the Artificial Cardiac Pacemaker Market is the shortage of trained electrophysiologists and cardiology technicians, particularly in rural and underdeveloped areas. Implanting pacemakers requires specialized expertise to avoid complications such as lead dislodgement or device malfunction. Post-operative care, including programming and troubleshooting device anomalies, demands regular follow-ups and skilled interpretation of pacemaker diagnostics. However, many healthcare systems lack standardized training programs or sufficient personnel for cardiac device management. This skill gap results in delayed diagnoses, procedural backlogs, and suboptimal patient outcomes, ultimately constraining market scalability despite rising demand for cardiac rhythm management devices.

• Surge in Demand for Leadless Pacemakers: Leadless pacemakers are gaining notable traction as they eliminate the need for leads, reducing infection risks and procedural complications. By 2024, over 100,000 leadless pacemakers were implanted globally, with the U.S. and Japan leading adoption. These devices, measuring less than 1 cc in volume, are implanted directly into the heart via catheterization, reducing hospital stay durations by up to 40%. The absence of wires improves device reliability, positioning this segment for accelerated clinical uptake.

• Integration of Remote Monitoring Capabilities: An increasing number of artificial cardiac pacemakers are now embedded with wireless telemetry and Bluetooth-enabled systems, allowing real-time remote monitoring. Over 70% of new-generation devices launched in 2023 and 2024 support data transmission to cloud-based platforms. This trend facilitates proactive patient care and enables healthcare professionals to intervene quickly in the event of abnormal rhythm patterns or device malfunctions. Remote monitoring has also reduced in-person follow-ups by 60%, enhancing clinical efficiency.

• Emphasis on MRI-Compatible Pacemakers: The development and commercial deployment of MRI-conditional pacemakers have significantly expanded patient eligibility for advanced imaging diagnostics. In 2024, nearly 65% of all newly implanted pacemakers were MRI-compatible, up from 42% in 2020. These devices ensure safe exposure to magnetic resonance imaging without compromising function or safety, improving long-term management of patients with multiple comorbidities requiring imaging procedures.

• Miniaturization and Extended Battery Life: Advancements in microelectronics and energy storage have led to smaller devices with extended operational longevity. Modern artificial cardiac pacemakers now feature batteries that last up to 14 years, compared to 7–10 years in earlier models. Additionally, manufacturers have reduced device thickness by approximately 30%, improving patient comfort and minimizing tissue disruption during implantation. These developments are enhancing both clinical and patient acceptance rates.

The Artificial Cardiac Pacemaker Market is segmented by type, application, and end-user, each contributing distinctively to the industry’s growth landscape. In terms of type, single-chamber, dual-chamber, and leadless pacemakers are dominating the product mix, with dual-chamber pacemakers holding a significant clinical share due to their capability to coordinate both atrial and ventricular pacing. On the application front, bradycardia and atrioventricular block remain the primary drivers of pacemaker implantation worldwide, while emerging applications in heart failure management are expanding the use case base. The end-user segment is broadly categorized into hospitals, ambulatory surgical centers, and specialty cardiac clinics. Hospitals remain the most prominent end-users due to their comprehensive surgical and post-operative capabilities. Meanwhile, ambulatory centers are quickly expanding their role, particularly in urban areas where outpatient procedures are becoming more common. Each segment reflects specific dynamics, shaped by clinical needs, infrastructure readiness, and patient demographics.

The artificial cardiac pacemaker market includes single-chamber, dual-chamber, biventricular, and leadless pacemakers. Dual-chamber pacemakers currently lead the market owing to their ability to simulate natural heart rhythms more accurately by pacing both the atrium and ventricle. They are particularly preferred in cases of atrioventricular block, accounting for a large portion of implantations globally. Leadless pacemakers are emerging as the fastest-growing type, driven by their minimally invasive nature, reduced infection risk, and ease of implantation, especially in elderly or high-risk patients. Their compact design and wireless features make them increasingly attractive in advanced cardiac care. Single-chamber pacemakers continue to serve specific patient profiles, particularly those requiring ventricular pacing only, while biventricular devices—used primarily in cardiac resynchronization therapy—hold a niche role in managing heart failure cases. The expanding product range and increasing physician familiarity with new models are expected to broaden device adoption across all patient categories.

Artificial cardiac pacemakers are primarily used in managing bradycardia, atrioventricular block, heart failure, and other rhythm-related disorders. Among these, bradycardia remains the leading application due to its high prevalence and immediate need for rhythm correction. It accounts for the majority of pacemaker implants globally, especially in elderly populations. Atrioventricular block follows closely, necessitating dual-chamber pacing in moderate to severe cases. Heart failure applications are the fastest-growing segment, driven by the increasing adoption of biventricular pacing and advancements in cardiac resynchronization therapy. Innovations in pacing algorithms and AI-driven synchronization methods have expanded the utility of pacemakers in managing reduced ejection fraction and improving cardiac output. Additional applications include sinus node dysfunction and post-surgical pacing, which, though smaller in volume, play a crucial role in specific surgical and recovery scenarios. The diversification of application areas is enhancing the overall value proposition of pacemaker solutions across healthcare systems.

Hospitals dominate the end-user segment of the artificial cardiac pacemaker market due to their full-spectrum infrastructure, skilled surgical teams, and post-implantation care facilities. They account for a significant volume of both primary implants and revision procedures. Their ability to handle complex cases and integrate with digital cardiac care platforms makes them the preferred venue for most pacemaker surgeries. Ambulatory surgical centers represent the fastest-growing end-user group, benefiting from lower costs, reduced wait times, and an increase in low-risk outpatient implant procedures. These centers are becoming especially popular in North America and Western Europe. Specialty cardiac clinics and electrophysiology labs contribute to diagnostic and post-operative follow-ups, playing a pivotal role in long-term device monitoring and adjustment. Additionally, home-care setups are slowly gaining importance as remote monitoring and patient-friendly technologies continue to advance. Each end-user type reflects evolving healthcare delivery models and patient expectations in cardiac rhythm management.

North America accounted for the largest market share at 39.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2025 and 2032.

The dominance of North America stems from its robust healthcare infrastructure, early adoption of technological innovations in implantable cardiac devices, and supportive reimbursement policies. Meanwhile, Asia-Pacific's accelerated growth is driven by a rising aging population, increasing healthcare investments, and growing awareness of cardiac health across nations such as China, India, and Japan. Additionally, local manufacturing and rising affordability are expanding regional access to life-saving pacemaker procedures. Europe's market performance remains stable, with regulatory harmonization and sustainability goals reshaping product design and usage patterns. Latin America and the Middle East & Africa continue to see steady progress, driven by increased healthcare outreach and public-private partnerships. As global demand for cardiovascular treatment rises, manufacturers are enhancing regional supply chains and aligning with localized patient needs to gain a competitive edge in the Artificial Cardiac Pacemaker Market.

AI Integration and Digital Monitoring Driving Implantable Device Evolution

North America held approximately 39.2% of the global artificial cardiac pacemaker market in 2024, driven by high implant volumes in the United States and Canada. Demand is led by hospitals and specialty cardiology clinics adopting advanced dual-chamber and leadless pacemakers. Key industries supporting the growth include digital health startups and medical device OEMs integrating AI into cardiac rhythm management. The U.S. FDA has fast-tracked several pacemaker models with wireless telemetry features, reflecting proactive regulatory support. Additionally, Medicare and private insurers have broadened reimbursement for remote monitoring services, enhancing clinical accessibility. The adoption of cloud-based patient tracking platforms is enabling real-time diagnostics, increasing operational efficiency across care networks and reducing in-hospital follow-ups. These developments continue to redefine how pacemaker therapy is delivered across North America.

Smart Device Adoption and Regulatory Convergence Transforming Cardiac Care

Europe accounted for nearly 26.7% of the artificial cardiac pacemaker market in 2024, with leading markets including Germany, France, and the United Kingdom. Germany remains the hub for device production, while the UK and France have shown significant growth in AI-assisted pacing therapies. The European Medicines Agency (EMA) and MDR frameworks have standardized clinical evaluation, ensuring faster access to innovative devices. Sustainability goals under the EU Green Deal are prompting manufacturers to reduce e-waste and focus on recyclable, biocompatible materials. AI-powered pacemakers and MRI-conditional models are being widely adopted across urban cardiac centers, enhancing procedural precision and patient safety. Increasing awareness of cardiovascular health and improved public health initiatives are further accelerating market expansion across the continent.

Expanding Infrastructure and Domestic Innovation Fueling Device Uptake

The Asia-Pacific region ranked second globally in terms of artificial cardiac pacemaker implant volumes in 2024, reflecting fast-growing demand from countries such as China, Japan, and India. China is a major consumer due to its large elderly population and growing cardiac disease burden, while Japan remains a leader in precision device development. India is witnessing strong growth through public-private healthcare partnerships and expansion of digital cardiology services. Government-backed infrastructure investments have improved access to cardiac care in semi-urban and rural areas. Technological hubs in Singapore, South Korea, and Taiwan are accelerating AI integration in device development, driving local manufacturing and exports. The rising presence of regional medtech firms is supporting long-term market self-reliance and lowering procedural costs across the region.

Health System Expansion and Device Imports Boosting Growth Trajectory

Brazil and Argentina are the primary contributors to the South American artificial cardiac pacemaker market, with Brazil commanding the majority market share at 5.8% in 2024. Brazil’s urban health systems are rapidly adopting dual-chamber and MRI-compatible pacemakers, supported by government procurement programs and rising public awareness. Argentina follows with a growing private-sector cardiology network fueling device implantation. National regulatory bodies are simplifying approval pathways for imported medical technologies, enabling faster availability of advanced models. Infrastructure development in public hospitals and an uptick in cardiac screening programs are expanding the regional patient base. Additionally, cross-border trade agreements are improving supply chain stability, supporting broader device accessibility across emerging cities.

Digital Health Modernization and Trade Agreements Enabling Growth Surge

The Middle East & Africa artificial cardiac pacemaker market is growing steadily, with the UAE and South Africa emerging as central hubs for regional demand. In 2024, the region accounted for 4.1% of the global market. UAE’s smart hospital initiatives and heavy investment in digital health infrastructure are facilitating the adoption of connected pacemaker systems. South Africa’s expanding public health outreach is enabling wider access to cardiovascular therapies, especially in underserved communities. Local regulations now support regional device assembly and partnerships with global OEMs, improving affordability and availability. Enhanced trade agreements with Europe and Asia have improved import channels, accelerating market penetration for advanced AI-integrated pacemakers. These developments are helping transform cardiac care delivery across this diverse region.

United States – 34.8% Market Share

High production capacity, early technology adoption, and strong end-user demand from advanced healthcare systems.

China – 17.5% Market Share

Large patient base, increasing implant procedures, and expanding domestic manufacturing of AI-powered pacemakers.

The Artificial Cardiac Pacemaker market exhibits a moderately consolidated competitive environment with over 35 globally active manufacturers, ranging from legacy medtech leaders to emerging innovators. The market is driven by strategic moves such as product innovation, AI integration, and expansion into high-growth geographies. Companies are actively investing in R&D to launch next-generation leadless and MRI-compatible pacemakers equipped with wireless telemetry and remote monitoring functionalities. Strategic partnerships with healthcare systems and digital health platforms are enhancing the clinical adoption of AI-based pacemaker management tools.

Recent competitive developments include acquisitions aimed at expanding cardiac rhythm management portfolios and collaborations with software developers to embed machine learning into device programming. Key players maintain strong brand equity and distribution networks, especially in North America, Europe, and Japan. Market positioning is also influenced by regulatory agility, with faster product clearances in the U.S. and EU benefiting first-movers. Additionally, many players are diversifying their product lines to include energy-efficient devices with extended battery life and user-friendly interfaces. The continued push toward digital transformation and patient-centric cardiac care solutions is reshaping competitive dynamics across both mature and emerging economies.

Medtronic

Boston Scientific Corporation

MicroPort Scientific Corporation

Biotronik SE & Co. KG

Abbott Laboratories

LivaNova PLC

Lepu Medical Technology Co., Ltd.

OSYPKA Medical GmbH

Shree Pacetronix Ltd.

Oscor Inc.

The Artificial Cardiac Pacemaker Market is witnessing rapid technological transformation, driven by miniaturization, wireless communication, and AI-enhanced pacing systems. Leadless pacemaker technology has significantly advanced, eliminating the need for transvenous leads and reducing the risk of lead-related complications. These devices, which can be implanted via catheter directly into the right ventricle, are especially beneficial for elderly and high-risk patients. By 2024, more than 100,000 leadless pacemakers had been implanted globally, reflecting strong adoption in both developed and emerging healthcare markets.

MRI-conditional pacemakers have become standard, with nearly two-thirds of devices implanted in 2024 being safe for full-body MRI scans. This innovation ensures patients requiring advanced imaging are no longer excluded from life-saving cardiac therapies. Furthermore, AI-based pacing algorithms have enabled dynamic adjustments based on patient-specific cardiac rhythm, improving synchronization and extending battery life. These smart features are increasingly being integrated into devices connected to cloud platforms, allowing real-time remote diagnostics and predictive maintenance.

Another area of progress is energy optimization, where advanced battery technologies now support operational lifespans of 12–14 years. Additionally, flexible circuit designs and biocompatible materials are making implants less invasive and more durable. These advancements are enhancing patient outcomes while enabling clinicians to streamline long-term cardiac rhythm management with greater precision.

• In February 2024, Medtronic launched its Micra AV2 and Micra VR2 leadless pacemakers globally. These second-generation devices offer extended battery life up to 16 years and enhanced atrioventricular synchrony with improved sensing algorithms for patients with AV block.

• In July 2023, Abbott announced the CE Mark approval and European rollout of its Aveir DR dual-chamber leadless pacemaker system, which utilizes i2i™ technology to facilitate synchronized communication between the atrial and ventricular devices without the use of physical leads.

• In March 2024, Biotronik unveiled a remote update feature in its BIOMONITOR III injectable loop recorder platform, allowing physicians to upgrade device firmware remotely, enabling continuous performance improvements without requiring patient intervention or clinical visits.

• In November 2023, MicroPort secured regulatory approval in China for its SmartView™ cloud-connected pacemaker management platform, supporting real-time data transmission, automatic arrhythmia alerts, and remote reprogramming capabilities integrated with local electronic health record systems.

The Artificial Cardiac Pacemaker Market Report provides an in-depth evaluation of the global landscape for implantable cardiac rhythm devices, focusing on current trends, technological innovations, regulatory shifts, and competitive positioning. The report covers a wide range of device types, including single-chamber, dual-chamber, biventricular, and leadless pacemakers. It also explores emerging solutions such as rechargeable and MRI-conditional devices that enhance diagnostic compatibility and procedural safety.

Geographically, the market analysis spans major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, each with distinct consumption patterns, clinical infrastructures, and regulatory frameworks. Key application areas reviewed in the report include bradycardia, atrioventricular block, heart failure, and post-surgical rhythm management. The report further explores the evolving role of AI in real-time pacing optimization, remote monitoring, and predictive diagnostics.

End-user segments are categorized into hospitals, ambulatory surgical centers, specialty cardiac clinics, and remote care models, each demonstrating unique adoption trends. The report also examines niche areas such as pediatric pacemakers and adaptive pacing solutions for complex arrhythmias. Designed for decision-makers, it offers strategic insights into market segmentation, product development trends, regional opportunities, and the evolving digital transformation landscape shaping the future of cardiac rhythm therapy.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 13433.55 Million |

|

Market Revenue in 2032 |

USD 24680.97 Million |

|

CAGR (2025 - 2032) |

7.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Medtronic, Boston Scientific Corporation, MicroPort Scientific Corporation, Biotronik SE & Co. KG, Abbott Laboratories, LivaNova PLC, Lepu Medical Technology Co., Ltd., OSYPKA Medical GmbH, Shree Pacetronix Ltd., Oscor Inc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |