Reports

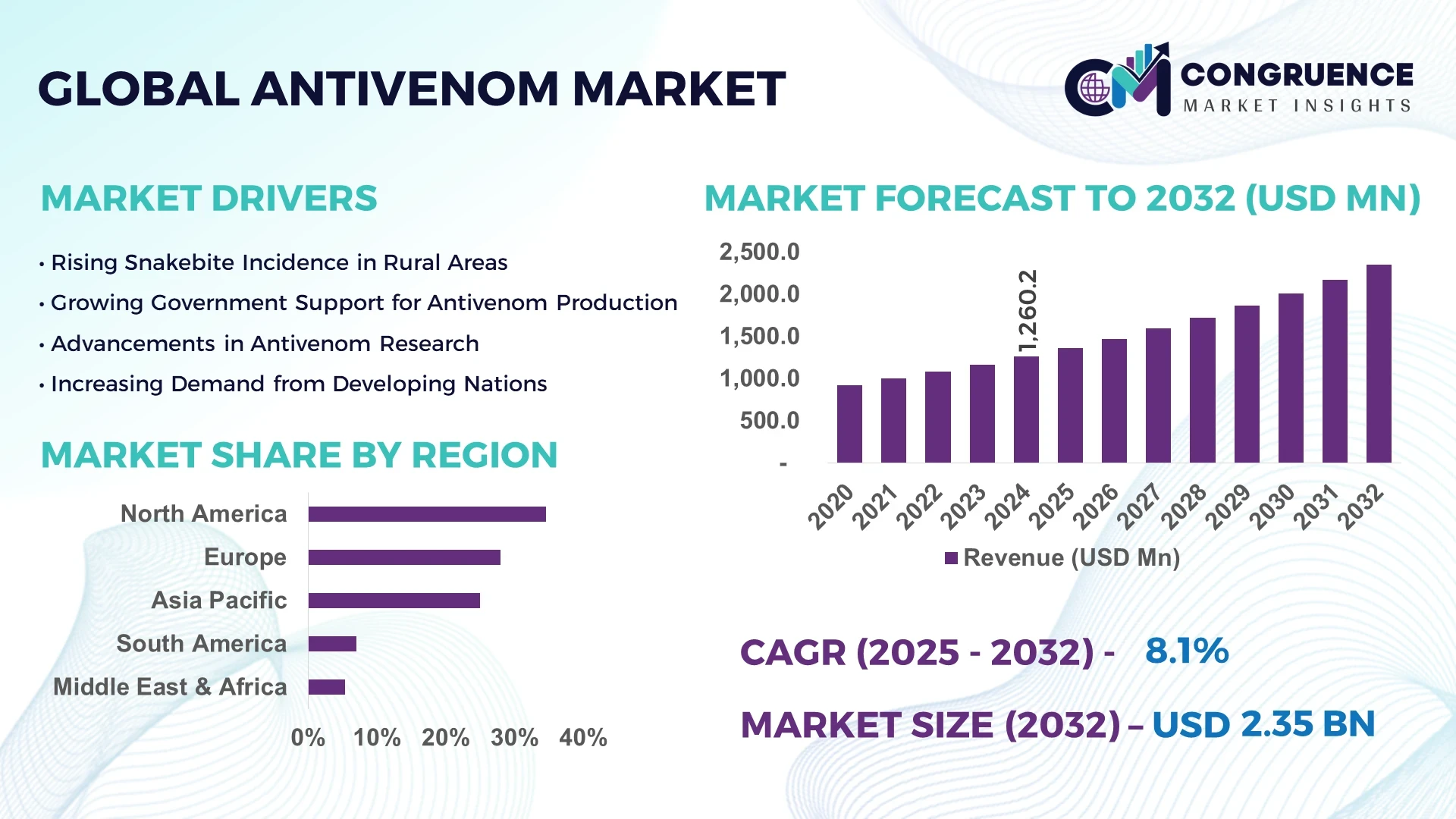

The Global Antivenom Market was valued at USD 1.26 Billion in 2024 and is anticipated to reach a value of USD 2.40 Billion by 2032, expanding at a CAGR of 8.11% between 2025 and 2032.

India stands as a dominant force in the global antivenom market, primarily due to its high incidence of snakebites, particularly from species like the Indian cobra, Russell's viper, and common krait. The country's extensive rural population, combined with agricultural activities, increases the risk of snakebite incidents. To address this, India has invested in the development and distribution of region-specific antivenoms, enhancing accessibility and treatment efficacy across diverse geographical areas.

The antivenom market is witnessing significant advancements, including the development of recombinant antivenoms that offer improved safety profiles and reduced allergic reactions. Additionally, there's a growing emphasis on rapid diagnostic kits that can quickly identify the type of venom, enabling timely and appropriate treatment. Collaborations between research institutions and pharmaceutical companies are fostering innovation, leading to more effective and affordable antivenom solutions. Furthermore, educational campaigns and community outreach programs are being implemented to raise awareness about snakebite prevention and the importance of seeking prompt medical attention.

Artificial Intelligence (AI) is revolutionizing the antivenom market by enhancing various aspects of research, production, and treatment. In research, AI algorithms analyze vast datasets to identify patterns in venom composition, facilitating the development of more targeted and effective antivenoms. This accelerates the discovery process and reduces reliance on traditional trial-and-error methods.

In manufacturing, AI-driven automation ensures precision and consistency in antivenom production, minimizing human error and improving scalability. Quality control processes benefit from AI's ability to detect anomalies in real-time, ensuring that only high-quality products reach the market. Moreover, AI aids in optimizing supply chain logistics, predicting demand patterns, and managing inventory efficiently, which is crucial for timely distribution, especially in remote areas.

From a treatment perspective, AI-powered diagnostic tools assist healthcare providers in accurately identifying the type of envenomation based on symptoms and patient data. This leads to the administration of the most appropriate antivenom, reducing the risk of complications and improving patient outcomes. Additionally, AI facilitates telemedicine services, allowing experts to guide local healthcare workers in managing snakebite cases effectively.

“In 2024, Médecins Sans Frontières (MSF) initiated a trial in South Sudan using an AI-powered application to identify venomous snakes from photographs. The app, equipped with a database of 380,000 snake images, assists medics in determining the appropriate treatment more accurately, reducing the misuse of rare and costly antivenoms. Early results indicate that the AI's identification capabilities sometimes surpass those of human experts, highlighting its potential to improve snakebite treatment outcomes.”

The increasing number of snakebite incidents, particularly in rural and agricultural regions, is a significant driver of the antivenom market. Limited access to healthcare facilities and lack of awareness exacerbate the situation, leading to higher demand for effective antivenom treatments. Efforts to improve healthcare infrastructure and education in these areas are essential to address this growing concern.

The production of antivenoms is complex and expensive, involving the maintenance of venomous animals and the extraction of antibodies. These high costs limit the availability of antivenoms, especially in low-income regions. Additionally, the short shelf-life of antivenoms poses challenges in storage and distribution, further restricting access to these life-saving treatments.

Innovations in biotechnology, such as recombinant DNA technology, offer opportunities to develop more effective and affordable antivenoms. Collaborations between research institutions and pharmaceutical companies can accelerate the development of next-generation antivenoms with improved safety profiles. These advancements have the potential to enhance treatment outcomes and expand market reach.

Stringent regulatory requirements and quality control standards pose challenges for antivenom manufacturers. Ensuring the safety and efficacy of antivenoms requires rigorous testing and compliance with international guidelines. Navigating these regulatory landscapes can be time-consuming and costly, potentially delaying the introduction of new antivenom products to the market.

Integration of AI in Antivenom Development: The adoption of AI technologies is streamlining the research and development process of antivenoms. By analyzing complex venom compositions and predicting effective antibody responses, AI accelerates the creation of targeted treatments, reducing development time and costs.

Expansion of Antivenom Production Facilities: To meet the growing demand, several countries are investing in the expansion of antivenom manufacturing facilities. This includes the establishment of regional production centers to ensure timely availability and reduce dependency on imports.

Public-Private Partnerships: Collaborations between governments, NGOs, and private pharmaceutical companies are fostering the development and distribution of antivenoms. These partnerships aim to improve access to treatments in underserved regions and support ongoing research initiatives.

Educational Campaigns and Community Engagement: Awareness programs focusing on snakebite prevention and the importance of prompt treatment are being implemented in high-risk areas. Community engagement efforts aim to educate the public, reduce stigma, and encourage timely medical intervention, thereby improving treatment outcomes.

The global antivenom market is segmented into types, applications, and end-users, offering a comprehensive understanding of the industry's structure and growth potential. This segmentation highlights the evolving nature of the market, driven by technological advancements, increasing incidence of envenomation, and the expansion of healthcare infrastructure in rural regions. Each segment plays a crucial role in shaping demand trends, with type-based segmentation covering polyvalent and monovalent antivenoms; application-based segmentation focusing on snakebites, scorpion stings, and others; and end-user segmentation including hospitals, clinics, and ambulatory surgical centers. Analyzing these segments provides clarity on where innovation and investment are intensifying, particularly in high-incidence areas across Asia-Pacific and Sub-Saharan Africa.

The antivenom market is broadly segmented into polyvalent antivenom and monovalent antivenom. Among these, polyvalent antivenom holds the largest market share and continues to dominate due to its ability to neutralize venom from multiple snake species, which is especially critical in regions where accurate identification of the snake is difficult. These antivenoms are widely used in India, Africa, and Latin America due to high snakebite diversity and prevalence.

On the other hand, monovalent antivenom, which targets venom from a single species, is witnessing significant growth, particularly in developed countries where advanced diagnostic tools can quickly identify the envenomating species. This enables precise and effective treatment, reducing the risk of allergic reactions and side effects associated with polyvalent formulations.

Polyvalent antivenoms remain the cornerstone of treatment in high-burden regions, but monovalent antivenoms are growing at a faster rate due to increased adoption in specialized care settings and improved venom detection capabilities. Investments in recombinant antivenom production are further expected to enhance the efficacy and reduce the cost of monovalent products in the future.

The primary application segments in the antivenom market include snakebite envenomation, scorpion stings, spider bites, and others (including bee or jellyfish stings). Snakebite envenomation dominates the application segment and accounts for the highest market share, driven by the staggering number of annual cases—estimated at over 5 million globally. The WHO recognizes snakebite as a neglected tropical disease, which has further catalyzed global efforts toward treatment accessibility.

Scorpion sting treatment represents the fastest growing segment, particularly in North Africa, Middle East, and parts of South America, where stings are prevalent among children and rural dwellers. The need for rapid medical intervention and the rising number of hospitalizations due to severe systemic symptoms have led to increased demand for scorpion-specific antivenoms.

Spider bite treatments remain niche, limited mostly to Australia and parts of the Americas, where venomous species like the funnel-web or brown recluse spiders exist. With increasing urbanization encroaching on habitats of venomous species, the scope of applications is gradually broadening.

The end-user segment of the antivenom market comprises hospitals, clinics, and ambulatory surgical centers. Among these, hospitals constitute the largest and leading segment, owing to their advanced facilities, higher patient intake, and ability to manage critical cases of envenomation. Government and private hospitals in rural and semi-urban areas are particularly vital in snakebite-endemic regions like India, Nigeria, and parts of Southeast Asia, where antivenom availability and immediate medical intervention can significantly reduce mortality and morbidity.

Clinics represent a smaller but essential segment, especially in suburban and semi-urban zones where initial diagnosis and stabilization of snakebite victims occur before referral to larger hospitals. They are crucial for early-stage intervention and often provide polyvalent antivenoms for emergency cases.

Ambulatory surgical centers (ASCs) are emerging as the fastest growing segment, particularly in high-income countries, where snake and insect bites can be treated in outpatient settings due to better diagnostics and milder symptoms. Their growth is driven by lower treatment costs, reduced hospitalization time, and improved patient convenience.

North America accounted for the largest market share at 34.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2025 and 2032.

North America's dominance is driven by its advanced healthcare infrastructure, strong regulatory framework, and substantial investments in research and antivenom production. In contrast, Asia-Pacific is witnessing rapid market expansion due to high incidence of snakebites in countries like India, Indonesia, and Bangladesh, coupled with increasing government efforts to enhance rural healthcare access. Moreover, ongoing developments in biotechnology and antivenom manufacturing capabilities are further propelling the region’s growth trajectory.

Technological Innovation and Wildlife Control Measures Fuel Market Demand

The North America antivenom market continues to lead globally due to the prevalence of venomous reptiles, such as rattlesnakes and coral snakes, particularly in the United States and parts of Mexico. The U.S. alone reports over 8,000 venomous snakebites annually. This demand is supported by the presence of well-established antivenom manufacturers and extensive R&D activities aimed at improving the efficacy and safety of antivenom products. Additionally, the region has seen the adoption of AI-based identification and monitoring systems for snakebite management, as well as public awareness campaigns that help reduce response time and improve survival outcomes. Government funding and support through health programs further ensure accessibility of treatment across both urban and remote regions.

Low Incidence, High Preparedness with Regional Manufacturing Hubs

Europe's antivenom market is relatively smaller in volume due to a low incidence of venomous bites, primarily from species such as the European adder. However, the region maintains high preparedness levels with localized antivenom production and advanced healthcare systems. Countries like France, Italy, and the UK have taken proactive measures by establishing dedicated antivenom stockpiles and supporting cross-border supply chains to ensure quick availability in emergencies. The market also benefits from government-funded public health initiatives focused on wildlife education and envenomation prevention. Additionally, Europe is emerging as a key exporter of antivenoms to African and Asian nations, making regional manufacturing capabilities strategically important.

High Burden of Snakebites and Expanding Healthcare Infrastructure Driving Growth

Asia-Pacific is home to more than half of the world’s snakebite-related deaths, with India alone reporting over 58,000 fatalities annually. This immense disease burden is pushing governments and private players to ramp up the production and distribution of affordable, region-specific antivenoms. The market is witnessing growth in both public procurement and NGO-driven antivenom supply chains. In addition, emerging economies like Vietnam and the Philippines are investing in healthcare outreach programs to improve access in rural and tribal areas. Technological integration, including mobile health apps and AI-powered diagnostic tools, is also gaining traction. These efforts are reshaping the treatment ecosystem and fueling rapid market expansion across the region.

Targeted Responses to Diverse Venomous Species

South America faces a diverse envenomation threat from snakes like the Bothrops (fer-de-lance), coral snakes, and bushmasters, with Brazil and Colombia accounting for the majority of cases. The region’s antivenom market is supported by a well-established network of national institutes dedicated to venom research and treatment. Brazil, in particular, has one of the largest government-operated antivenom production systems, enabling mass distribution to its Amazon and rural populations. While challenges such as distribution logistics in remote jungle regions persist, public health interventions, mobile healthcare units, and regional manufacturing hubs are playing a crucial role in bridging gaps. Countries are also actively participating in international collaborations to enhance treatment standards and venom research.

Critical Demand Across High-Burden and Under-Resourced Regions

The Middle East & Africa region represents a significant share of the global snakebite burden, with sub-Saharan Africa recording over 1 million snakebite incidents annually. Despite this high demand, access to antivenoms remains inconsistent due to supply shortages, affordability issues, and fragile healthcare systems. Countries like Nigeria and South Africa are leading efforts to improve domestic antivenom production and distribution infrastructure. Moreover, several philanthropic and government-backed initiatives are working to subsidize antivenoms and provide free access in high-risk zones. Desert and savannah regions also see a high number of scorpion stings, further increasing the demand for a broader spectrum of antivenoms. As awareness and international cooperation grow, the region is expected to become a key focus for market expansion and investment.

United States – USD 346 Million, Due to its advanced healthcare systems, established manufacturers, and high demand for snakebite treatment solutions.

India – USD 275 Million, Owing to the extremely high volume of envenomation cases and significant production of region-specific polyvalent antivenoms.

The global antivenom market is characterized by a dynamic and competitive landscape, with both established pharmaceutical giants and emerging biotech firms striving to enhance their market presence. Major players such as Pfizer Inc., CSL Limited, and Bharat Serums and Vaccines Limited have been instrumental in advancing antivenom therapies through extensive research and development initiatives. These companies focus on producing effective and safer antivenoms, catering to the diverse needs of regions affected by venomous bites.

Emerging biotechnology firms are introducing advanced solutions like monoclonal antibody-based antivenoms, intensifying competition. Strategic collaborations with governments and health organizations ensure market access in endemic regions. Manufacturers emphasize expanding distribution networks and improving affordability to enhance market presence. Regional players also play a significant role by catering to localized venom-specific needs, making the competitive landscape dynamic and innovation-driven.

Pfizer Inc.

CSL Limited

Bharat Serums and Vaccines Limited

Merck & Co., Inc.

Boehringer Ingelheim International GmbH

MicroPharm Limited

Rare Disease Therapeutics Inc.

Haffkine Bio-Pharmaceutical Corporation Limited

Vins Bioproducts Limited

Incepta Pharmaceuticals Limited

Technological advancements are playing a pivotal role in transforming the antivenom market, enhancing the efficacy, safety, and accessibility of treatments. One significant development is the shift towards lyophilized (freeze-dried) antivenom products. These formulations offer enhanced stability and longer shelf life, making them ideal for use in remote areas and regions with challenging storage conditions. Lyophilized antivenoms can be stored at room temperature for extended periods without losing potency, addressing the limitations posed by inadequate cold chain infrastructure in developing countries.

Another notable innovation is the development of monoclonal antibody-based antivenoms. These targeted therapies offer higher specificity and reduced risk of adverse reactions compared to traditional polyclonal antivenoms. By focusing on specific venom components, monoclonal antibodies can neutralize toxins more effectively, leading to improved patient outcomes.

Furthermore, advancements in recombinant DNA technology have facilitated the production of synthetic antivenoms. These recombinant antivenoms eliminate the need for animal-derived antibodies, reducing the risk of allergic reactions and ensuring a more consistent and scalable production process.

The integration of artificial intelligence (AI) and machine learning is also contributing to the antivenom market. AI-powered applications are being developed to assist in the rapid identification of venomous species, enabling healthcare providers to administer the appropriate antivenom promptly. This technological integration enhances diagnostic accuracy and treatment efficacy, particularly in regions with limited access to expert herpetologists.

Collectively, these technological innovations are reshaping the antivenom landscape, offering promising solutions to address the global burden of venomous bites and stings.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In June 2024, MicroPharm Limited, a UK-based pharmaceutical company, announced the acquisition of Sanofi Pasteur for an undisclosed amount. The acquisition aims to expand MicroPharm's portfolio of vaccine products and strengthen its capabilities in research and development. Sanofi Pasteur is a France-based global pharmaceutical company specializing in the research, development, manufacturing, and distribution of vaccines and biological products, including antivenoms.

In March 2024, Shri Apurva Chandra, the Union Health Secretary, launched the National Action Plan for the Prevention and Control of Snakebite Envenoming (NAP-SE) in India. Aiming to reduce snakebite deaths by half by 2030, the NAP-SE provides a comprehensive framework for states to develop action plans for managing, preventing, and controlling snakebites using the 'One Health' approach.

In February 2024, scientists at the Indian Institute of Science (IISc) developed a synthetic human antibody capable of neutralizing a potent neurotoxin produced by the Elapidae family of highly venomous snakes, including the cobra, king cobra, krait, and black mamba. The team from IISc's Scripps Research Institute and the Evolutionary Venomics Lab (EVL) at the Centre for Ecological Sciences (CES) employed a technique previously used to screen for antibodies against HIV and COVID-19 to create this new venom-neutralizing antibody.

The antivenom market report provides a comprehensive analysis of the global landscape, encompassing various facets of the industry. It delves into market dynamics, including drivers, restraints, opportunities, and challenges that influence market growth. The report offers detailed segmentation based on type, application, end-user, and geography, facilitating a nuanced understanding of market trends and potential areas for investment.

In terms of type, the report examines both polyvalent and monovalent antivenoms, highlighting their respective market shares and growth trajectories. Application-wise, it covers treatments for snakebites, scorpion stings, spider bites, and other envenomations. The end-user analysis focuses on hospitals, clinics, and ambulatory surgical centers, providing insights into their roles in antivenom administration.

Geographically, the report analyzes market trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, identifying key regions driving market growth. It also profiles major market players, detailing their product portfolios, strategic initiatives, and competitive positioning.

Furthermore, the report explores technological advancements shaping the antivenom market, such as lyophilized formulations, monoclonal antibody therapies, and AI integration. It also highlights recent developments, including mergers, acquisitions, partnerships, and government initiatives aimed at enhancing antivenom accessibility and efficacy.

Overall, the antivenom market report serves as a valuable resource for stakeholders, providing actionable insights to inform strategic decision-making and investment planning in the evolving antivenom landscape.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Antivenom Market |

| Market Revenue (2024) | USD 1.26 Billion |

| Market Revenue (2032) | USD 2.40 Billion |

| CAGR (2025–2032) | 8.11% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Pfizer Inc., CSL Limited, Bharat Serums and Vaccines Limited, Merck & Co., Inc., Boehringer Ingelheim International GmbH, MicroPharm Limited, Rare Disease Therapeutics Inc., Haffkine Bio-Pharmaceutical Corporation Limited, Vins Bioproducts Limited, Incepta Pharmaceuticals Limited |

| Customization & Pricing | Available on Request (10% Customization is Free) |