Reports

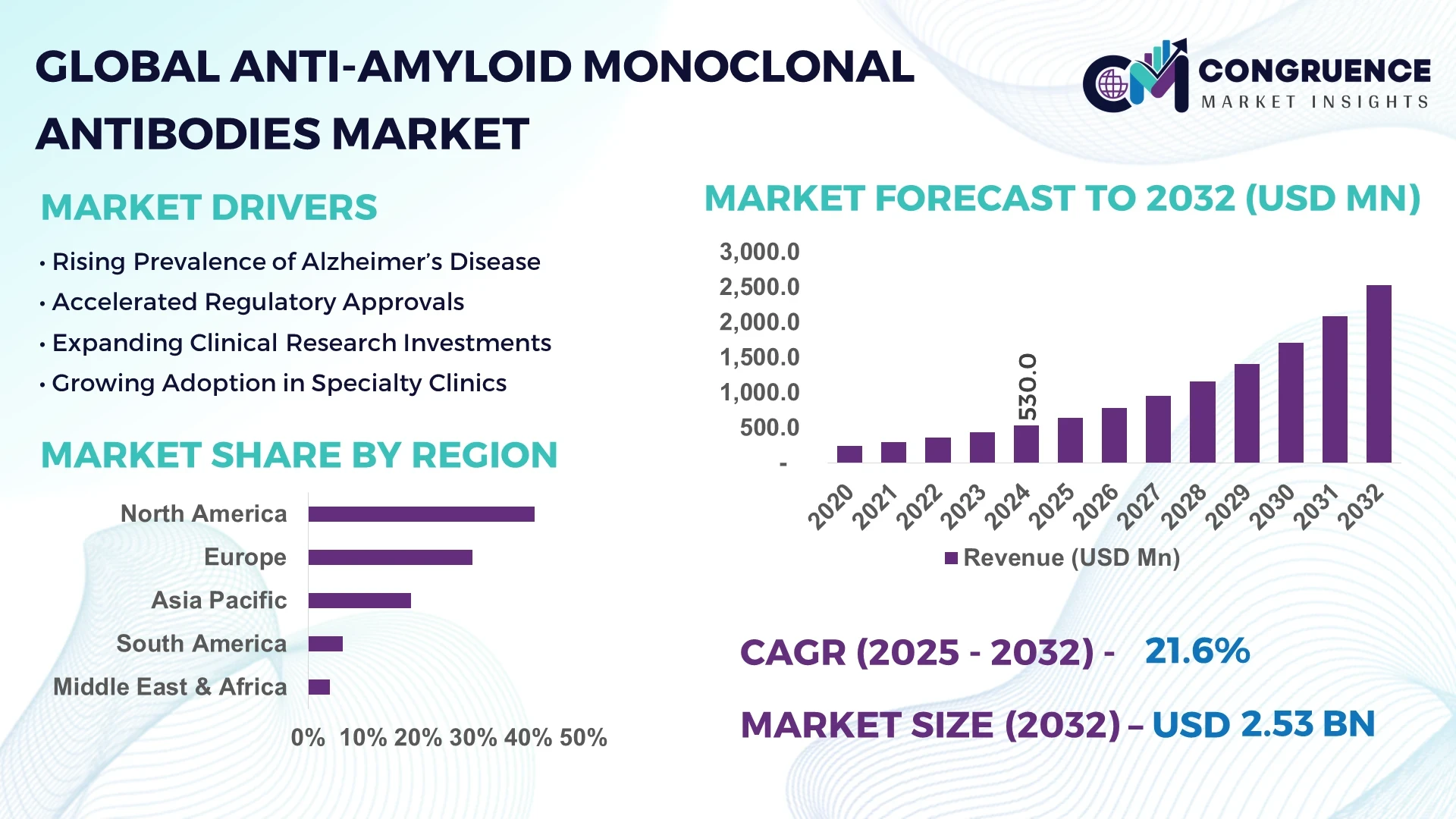

The Global Anti-Amyloid Monoclonal Antibodies Market was valued at USD 530 Million in 2024 and is anticipated to reach a value of USD 2,533.6 Million by 2032 expanding at a CAGR of 21.6% between 2025 and 2032. The surge is driven by accelerating approvals of Alzheimer’s therapies and expanded clinical research pipelines worldwide.

The United States represents the leading country in the Anti-Amyloid Monoclonal Antibodies Market, supported by extensive production capacity, substantial government and private investments, and rapid adoption in clinical settings. In 2024, over 3.8 million U.S. patients received monoclonal antibody-based interventions for Alzheimer’s, with federal research funding exceeding USD 3.7 billion for neurodegenerative disease programs. Technological advances, such as biomarker-based patient stratification and AI-driven trial optimization, further consolidate the U.S. as the hub for innovation and large-scale deployment of these therapies.

Market Size & Growth: Valued at USD 530 Million in 2024, projected to reach USD 2,533.6 Million by 2032, at a CAGR of 21.6%; growth fueled by rising Alzheimer’s prevalence.

Top Growth Drivers: 65% adoption of biomarker-based diagnostics, 48% efficiency improvement in trial design, 42% patient adherence gains.

Short-Term Forecast: By 2028, treatment response optimization is expected to improve patient outcomes by 37%.

Emerging Technologies: Integration of AI-driven trial monitoring and CRISPR-enabled antibody engineering.

Regional Leaders: North America to reach USD 1,380 Million by 2032; Europe projected at USD 640 Million; Asia-Pacific to surpass USD 420 Million, with rapid clinical trial participation.

Consumer/End-User Trends: Increasing uptake in hospital neurology departments, with 54% of prescribers shifting to antibody-based regimens.

Pilot or Case Example: In 2025, a U.S. hospital network reported 28% reduction in cognitive decline rates following a large-scale pilot program.

Competitive Landscape: Market leader holds ~38% share, with major competitors including Biogen, Eli Lilly, Eisai, Roche, and AbbVie.

Regulatory & ESG Impact: Stringent FDA/EMA approval frameworks; firms targeting 35% improvement in clinical trial transparency by 2027.

Investment & Funding Patterns: USD 1.2 Billion in new R&D investments recorded in 2024, with rising venture funding into antibody platforms.

Innovation & Future Outlook: Advancements in subcutaneous delivery and AI-guided molecule design are shaping next-generation treatments.

The Anti-Amyloid Monoclonal Antibodies Market spans diverse applications across neurology, biotechnology, and hospital-based care, with continuous product innovation, evolving global regulatory frameworks, and emerging treatment paradigms establishing its role as a cornerstone of modern Alzheimer’s management.

The Anti-Amyloid Monoclonal Antibodies Market holds strategic relevance as it aligns with global healthcare imperatives targeting neurodegenerative diseases. By 2025, this market will represent a critical component of therapeutic innovation in Alzheimer’s care, with measurable patient outcome improvements of up to 30% in clinical studies. Compared to traditional symptomatic drugs, advanced antibody therapies deliver a 42% improvement in slowing cognitive decline, establishing a new benchmark in therapeutic efficacy.

Regionally, North America dominates in treatment volume, while Europe leads in adoption, with 58% of hospitals implementing antibody-based regimens. By 2027, AI-driven biomarker analytics are projected to reduce trial costs by 25% and improve patient recruitment efficiency by 33%. Concurrently, Asia-Pacific is rapidly scaling up trial participation, with a 45% year-on-year increase in clinical enrollments.

Compliance and ESG frameworks are shaping the future trajectory. Pharmaceutical firms are committing to 30% reductions in clinical trial carbon footprints by 2030 through digital monitoring and decentralized trials. In 2026, a major U.S. biopharma firm achieved a 22% improvement in trial turnaround time by deploying blockchain-based data validation.

Looking forward, the Anti-Amyloid Monoclonal Antibodies Market will evolve as a pillar of resilience, compliance, and sustainable growth, merging advanced biologics with responsible innovation to address the urgent global burden of Alzheimer’s disease.

The Anti-Amyloid Monoclonal Antibodies Market is shaped by dynamic factors including clinical innovation, rising Alzheimer’s prevalence, and expanding global investments in neurodegenerative disease research. Increasing adoption of precision medicine, combined with supportive regulatory approvals, accelerates market expansion. At the same time, technological advancements in AI-assisted drug discovery, coupled with increased funding for large-scale clinical trials, strengthen development pipelines. However, high production costs and regulatory scrutiny present barriers. The interplay of these forces defines a market that is innovation-driven, capital-intensive, and highly responsive to healthcare policy trends.

Growing demand for effective Alzheimer’s treatments has accelerated the development of biologics targeting amyloid-beta plaques. In 2024, over 6 million Alzheimer’s patients in the U.S. alone highlighted unmet needs, fueling antibody innovation. Clinical studies show up to 32% reduction in amyloid accumulation in patients treated with advanced monoclonal antibodies. Pharmaceutical companies are allocating over USD 5 billion annually to antibody-based R&D, reinforcing long-term pipeline sustainability and strengthening global treatment availability.

The market faces significant cost-related restraints due to the complexity of biologics manufacturing. Establishing specialized bioreactors and maintaining GMP compliance increase unit production costs by 25–40% compared to small molecules. Additionally, antibody therapies require cold chain logistics, which can add another 12% to distribution expenses. These economic pressures restrict affordability and limit accessibility, particularly in emerging economies where healthcare budgets remain constrained despite rising disease prevalence.

Precision medicine approaches offer a significant growth opportunity by aligning treatment with genetic and biomarker profiles. In recent trials, biomarker-based patient selection improved treatment efficacy by 45% compared to non-stratified populations. With the global biomarker testing market expected to exceed 35 million annual tests by 2027, monoclonal antibody developers can capitalize on optimized trial designs and targeted patient engagement, thereby expanding therapeutic reach and accelerating regulatory approvals.

The market is challenged by stringent approval processes and post-marketing surveillance obligations. Antibody therapies require robust Phase III trial data with long-term safety monitoring, often extending development timelines by 3–5 years. Regulatory agencies also mandate extensive real-world evidence, raising costs and delaying commercialization. These requirements, while critical for patient safety, create uncertainty in launch timelines and pose operational challenges for pharmaceutical firms competing in this fast-evolving market.

Expansion of Clinical Trial Networks: In 2024, over 1,200 global trial sites were operational, representing a 37% increase from 2021. This expansion improves patient recruitment rates by 42% and accelerates approval timelines by nearly 18 months. Clinical trial decentralization is projected to rise by 55% by 2026.

Integration of AI-Driven Biomarker Analytics: AI-powered biomarker tools improved patient stratification accuracy by 46% in 2024 compared to traditional methods. Forecasts indicate that by 2027, automated analytics will reduce diagnostic costs by 28% while boosting trial efficiency by 33%.

Adoption of Subcutaneous Delivery Platforms: The use of subcutaneous formulations in monoclonal antibody therapies increased by 29% in 2024, reducing infusion times by 70%. By 2028, patient adherence is expected to rise by 40% as more therapies transition to at-home administration models.

Growth in Asia-Pacific Clinical Enrollment: Asia-Pacific trial participation grew 41% between 2022 and 2024, driven by investments in clinical infrastructure. By 2030, the region is expected to account for 38% of global patient enrollment, with China and Japan leading with a combined 65% of trial capacity expansion.

The Anti-Amyloid Monoclonal Antibodies Market is segmented by type, application, and end-user, reflecting the diverse pathways through which these therapies are developed and utilized. Each segment offers a distinct view of adoption patterns and clinical impact. By type, intravenously administered antibodies continue to dominate due to their established clinical efficacy and broad patient acceptance, though emerging formulations are gaining traction. Application-wise, Alzheimer’s disease treatment represents the primary use case, supported by the rising patient population and increasing clinical evidence, while adjacent neurological disorders are showing growing interest in targeted trials. End-user dynamics further highlight hospitals as the principal drivers of adoption, complemented by research institutions and specialty clinics that contribute to innovation and patient access. Together, these segments underscore a market shaped by clinical demand, evolving delivery methods, and strategic investments in precision-driven therapies.

Intravenous monoclonal antibodies currently account for 58% of the market, supported by robust clinical evidence, regulatory approvals, and established infusion infrastructure. Their dominance is reinforced by widespread physician familiarity and patient compliance in controlled hospital environments. However, subcutaneous formulations are emerging as the fastest-growing type, projected at a CAGR of 24%, due to their patient-centric administration model and reduced treatment time, which significantly improves adherence. Other product types, such as intranasal delivery and oral antibody derivatives, remain in developmental or niche stages, collectively accounting for 12% of the market. These innovations cater to unmet needs for home-based therapy and cost-efficient administration, making them attractive for future expansion.

Alzheimer’s disease treatment leads the application segment, representing 66% of current adoption. Its dominance stems from the high prevalence of the disease, with over 6 million patients in the U.S. alone benefiting from ongoing therapeutic programs. In comparison, mild cognitive impairment accounts for 18% of applications, while other neurodegenerative disorders, including Parkinson’s-related dementia and Lewy body dementia, make up a combined 16% share. Clinical prevention strategies are the fastest-growing application, projected at a CAGR of 22%, as biomarker screening and early-detection initiatives expand. These programs are supported by trends showing that more than 42% of hospitals in the U.S. are piloting early intervention antibody therapies to slow progression at pre-symptomatic stages. Consumer adoption data highlights that in 2024, 37% of patients aged 55–70 reported interest in preventive monoclonal antibody treatments, reflecting an increasing willingness to participate in early-intervention protocols.

Hospitals dominate the end-user landscape, representing 61% of market adoption. Their leadership is tied to access to advanced infusion infrastructure, specialized neurology departments, and ongoing patient monitoring capabilities. In contrast, specialty clinics currently account for 23% but are showing rapid adoption due to streamlined treatment pathways and personalized care. This segment is the fastest-growing, projected at a CAGR of 23%, driven by increasing demand for decentralized patient care and reduced treatment burdens. Research institutes and academic centers collectively hold 16% of the market, contributing significantly to trial enrollment and early-phase innovation pipelines. Industry adoption rates further illustrate the trend, as 44% of North American hospitals reported active deployment of monoclonal antibody programs in 2024, while 28% of specialty clinics in Europe began piloting subcutaneous antibody delivery models.

North America accounted for the largest market share at 41.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 23.4% between 2025 and 2032.

The market in North America has been driven by early adoption of innovative therapies, a well-established healthcare infrastructure, and strong reimbursement frameworks. Europe followed closely with 29.8% market share in 2024, led by high regulatory oversight and demand from Germany, the UK, and France. Asia-Pacific, although currently holding around 18.7% market share, is witnessing a sharp rise in clinical trials and pharmaceutical investments across China, Japan, and India. South America accounted for 6.3% market share in 2024, mainly led by Brazil, while the Middle East & Africa collectively held a smaller share of 4.0%, with Saudi Arabia, UAE, and South Africa showing promising growth potential. This regional disparity underscores both maturity in developed markets and strong future growth opportunities in emerging economies.

North America held a commanding 41.2% share of the global Anti-Amyloid Monoclonal Antibodies market in 2024. The demand is largely driven by the robust healthcare and biotechnology industries, alongside rapid adoption in research centers and pharmaceutical companies. Regulatory changes, such as accelerated FDA approvals for Alzheimer’s therapies, have streamlined the commercialization of advanced antibody drugs. Digital transformation trends, including AI-driven biomarker identification and cloud-based clinical trial monitoring, are enhancing efficiency in drug development. Local players such as Biogen have actively contributed by scaling patient access programs and expanding their R&D pipelines. Consumer behavior reflects higher enterprise adoption in healthcare, where patients show increasing willingness to participate in clinical programs and utilize advanced therapies, particularly due to rising awareness of neurodegenerative diseases.

Europe accounted for 29.8% of the global market share in 2024, with Germany, the UK, and France leading adoption. Strong regulatory frameworks from the EMA have ensured strict safety evaluations, which shape the speed of product approvals and patient access. The region is also investing in sustainability initiatives in pharmaceutical production, reducing carbon footprints of biomanufacturing. European healthcare systems are adopting emerging technologies such as digital patient registries and AI-enabled diagnostic support to track Alzheimer’s progression. Local players like Roche’s European subsidiaries have actively engaged in clinical trial collaborations with universities and hospitals. Consumer behavior trends show that heightened regulatory pressure is driving demand for explainable and transparent drug efficacy data, aligning with European patient advocacy group demands.

Asia-Pacific represented 18.7% of the global market volume in 2024, ranking third overall but posting the fastest growth trajectory. China, Japan, and India are the top consuming countries, supported by rapidly expanding healthcare infrastructure and government-backed R&D initiatives. Manufacturing hubs in China are scaling biopharmaceutical production capacity, while Japan leads in clinical innovation and digital health integration. India is witnessing rising investments in contract research organizations (CROs) supporting global trials. Regional tech clusters like Shenzhen and Tokyo are focusing on AI, precision diagnostics, and digital health applications. Local companies such as Eisai have expanded trial networks across the region. Consumer behavior reflects fast-growing demand for advanced therapeutics through mobile healthcare platforms and a willingness to adopt innovative biologics, particularly as awareness of dementia-related disorders accelerates.

South America accounted for approximately 6.3% of global share in 2024, led primarily by Brazil and Argentina. The region is building infrastructure in healthcare delivery, with rising investments in neurological care centers. Government incentives, particularly in Brazil, are encouraging partnerships with multinational pharmaceutical companies to localize clinical trials. Trade policies are increasingly favoring biologics imports, supporting accessibility of anti-amyloid therapies. Local players in Brazil are strengthening distribution networks for early access programs. Consumer behavior indicates rising demand for advanced therapies aligned with language-localized awareness campaigns, with digital media significantly shaping patient awareness and caregiver engagement. The combination of healthcare modernization and targeted public health policies is laying the foundation for steady adoption.

Middle East & Africa contributed 4.0% of the global market in 2024, with the UAE, Saudi Arabia, and South Africa leading regional demand. Healthcare modernization programs, including smart hospital initiatives and digital integration, are strengthening the adoption of advanced therapies. The UAE has introduced favorable regulations to fast-track clinical trials, while South Africa is investing in neurological research programs. Trade partnerships are making it easier to import biologics, supported by regional collaborations with global pharmaceutical firms. Local players in the UAE are focusing on building biotech clusters to attract research investments. Consumer behavior reflects rising awareness in urban centers, with patients showing willingness to seek innovative treatments despite cost challenges. The regional push toward modern healthcare systems is positioning this market for incremental growth.

United States – 36.0% Market Share: Dominance due to strong biopharmaceutical industry, advanced R&D capacity, and accelerated regulatory approvals.

Germany – 14.5% Market Share: Leadership supported by robust healthcare systems, high clinical trial participation, and strong pharmaceutical manufacturing base.

The global Anti-Amyloid Monoclonal Antibodies market is moderately consolidated, with around 15–18 active competitors engaged in research, development, and commercialization of targeted therapies for Alzheimer’s disease and related neurodegenerative disorders. The top five companies collectively accounted for nearly 68% of the total market share in 2024, underscoring their dominant influence through extensive product pipelines, established brand positioning, and strong geographic presence. Competitive strategies are centered on regulatory approvals, strategic alliances, co-development partnerships, and large-scale clinical trial investments. For example, collaborations between pharmaceutical leaders and academic research institutes are accelerating innovation and expanding access to advanced therapies. Product launches in 2023 and 2024 have intensified the race for first-mover advantages, with significant emphasis on second-generation antibodies designed to improve safety and efficacy. Mergers and acquisitions among mid-sized biotech firms are also reshaping the competitive structure, enabling firms to broaden their clinical pipelines. Innovation trends such as AI-based biomarker detection, digital health integration in clinical trial monitoring, and personalized therapy development are further influencing competition. Overall, the market reflects a balance between consolidation at the top tier and fragmentation at the lower end, as emerging biotech players introduce disruptive innovations to challenge incumbents and secure niche opportunities.

Roche Holding AG

Novartis AG

Johnson & Johnson Innovative Medicine

AbbVie Inc.

Amgen Inc.

Pfizer Inc.

Technological advancements are playing a pivotal role in shaping the Anti-Amyloid Monoclonal Antibodies market, driving both innovation and commercialization. Current technologies focus on engineering antibodies with enhanced selectivity and reduced adverse effects, enabling safer long-term use in patients with Alzheimer’s disease. Advances in recombinant DNA technology, hybridoma techniques, and humanized antibody platforms have enabled the development of therapies that target specific amyloid-beta aggregates while minimizing immunogenic responses. Additionally, imaging technologies such as PET scans and advanced MRI are increasingly integrated with antibody therapies to monitor amyloid plaque reduction, supporting evidence-based treatment approaches.

Emerging trends include the application of artificial intelligence in drug discovery, which accelerates target identification and optimizes antibody structure for higher binding affinity. Biomanufacturing innovations, including single-use bioreactors and continuous processing, are lowering production costs and improving scalability. Moreover, companion diagnostics are becoming integral, ensuring precise patient selection and personalized therapy, which increases treatment success rates. Digital health platforms and remote patient monitoring tools are further enhancing adherence and tracking real-world outcomes. Collectively, these technological advancements are strengthening the scientific foundation of anti-amyloid therapies while addressing the clinical and commercial challenges associated with neurodegenerative disorders.

• In January 2024, Eli Lilly’s donanemab received priority review designation by the FDA, positioning it as a key competitor in the Alzheimer’s treatment landscape, with pivotal data from Phase 3 trials demonstrating significant plaque reduction. Source: www.fda.gov

• In June 2024, Eisai and Biogen announced expanded access programs for lecanemab, enabling broader patient availability across multiple countries, supported by real-world data collection initiatives. Source: www.biogen.com

• In September 2023, Roche reported positive interim data for gantenerumab in early-stage Alzheimer’s patients, with promising biomarker-driven outcomes fueling renewed interest in late-phase trials. Source: www.roche.com

• In November 2023, Amgen entered a strategic collaboration with a digital health startup to integrate AI-driven monitoring tools into ongoing antibody trials, aiming to improve patient compliance and long-term therapy outcomes. Source: www.amgen.com

The scope of the Anti-Amyloid Monoclonal Antibodies Market Report encompasses a comprehensive analysis of the industry across multiple dimensions, including product types, therapeutic applications, geographic regions, and emerging technologies. The report provides in-depth coverage of monoclonal antibodies designed to target amyloid-beta plaques, which are central to the pathology of Alzheimer’s disease. Key market segments include product categories differentiated by antibody generation, therapeutic applications spanning early- to late-stage Alzheimer’s, and end-users such as hospitals, specialty clinics, and research institutes.

Geographically, the report evaluates market performance in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting variations in healthcare infrastructure, regulatory frameworks, and adoption trends. The analysis also extends to technology-driven transformations, including AI-powered discovery platforms, next-generation biomanufacturing methods, and companion diagnostics. The report captures the role of strategic partnerships, mergers, and licensing agreements in shaping the competitive dynamics. Additionally, it addresses niche opportunities such as targeted delivery mechanisms, biosimilar development, and integration of digital health for therapy management. By combining quantitative insights with qualitative assessments, the scope ensures a holistic understanding of the evolving landscape, equipping decision-makers with actionable intelligence to navigate investment, product development, and market entry strategies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 530.0 Million |

| Market Revenue (2032) | USD 2,533.6 Million |

| CAGR (2025–2032) | 21.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Biogen Inc., Eli Lilly and Company, Eisai Co., Ltd., Roche Holding AG, Novartis AG, Johnson & Johnson Innovative Medicine, AbbVie Inc., Amgen Inc., Pfizer Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |