Reports

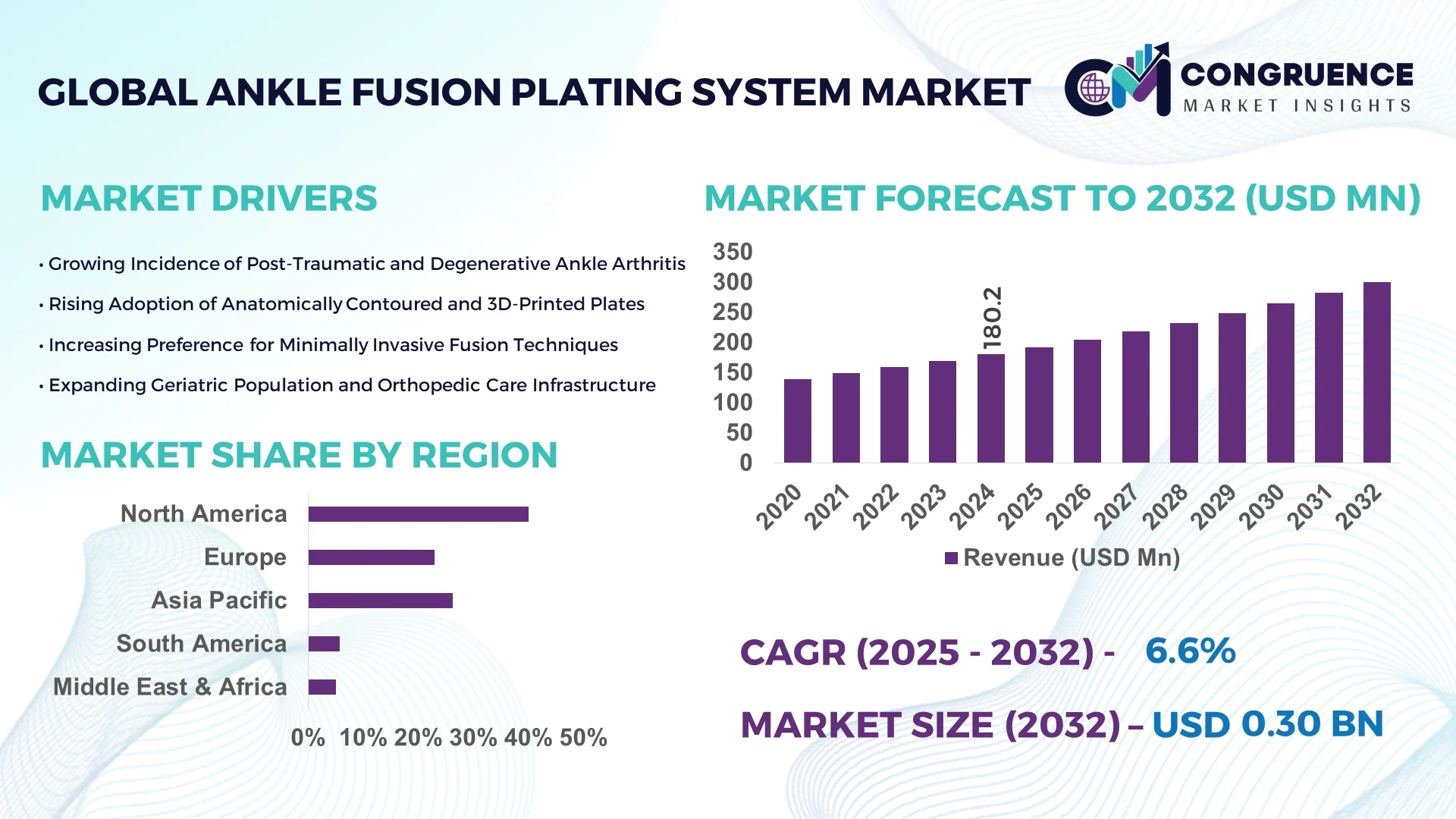

The Global Ankle Fusion Plating System Market was valued at USD 180.2 Million in 2024 and is anticipated to reach a value of USD 300.5 Million by 2032 expanding at a CAGR of 6.6% between 2025 and 2032. This uptrend is driven by rising incidence of ankle arthritis and traumatic injuries as well as improved surgical techniques.

In the dominant country, the United States commands leadership in advanced implant production and adoption: U.S. manufacturers invested over USD 25 million in R&D for anatomically contoured plating systems in 2023, producing over 15,000 fusion plate kits for ankle arthrodesis procedures. Nearly 40% of implants exported globally originate from U.S. facilities, and many high-volume U.S. orthopedic centers adopt locking plus hybrid plating technologies, implementing sensor-aided alignment systems in surgical planning to reduce malalignment rates from 8% to under 3%.

Market Size & Growth: Valued at USD 180.2 Million in 2024, projected to reach USD 300.5 Million by 2032, driven by rising orthopedic surgical demand.

Top Growth Drivers: Aging population growth (~20 %), increasing sports injury incidence (~15 %), and adoption of minimally invasive fixation (~12 %).

Short-Term Forecast: By 2028, surgical implant time per case expected to reduce by 10% and postoperative complication rates improve by 8%.

Emerging Technologies: 3D-printed patient-specific plates, sensor-integrated implants, biodegradable coatings for fusion sites.

Regional Leaders: North America (~USD 140 M by 2032), Europe (~USD 90 M by 2032), Asia Pacific (~USD 70 M by 2032) — each with distinct adoption patterns.

Consumer/End-User Trends: Key users include orthopedic surgeons in hospitals, specialty foot & ankle clinics; higher uptake in ambulatory surgical settings.

Pilot or Case Example: In 2026, a U.S. academic center trialed 3D patient-matched ankle fusion plates, reducing intraoperative adjustments by 25%.

Competitive Landscape: Market leader holds ~20 % share; other top players include Zimmer Biomet, Arthrex, DePuy Synthes, Wright Medical, Integra.

Regulatory & ESG Impact: Stricter implant safety regulations, biocompatibility standards, incentives for resorbable coatings and recycled medical device materials.

Investment & Funding Patterns: Around USD 40 million in venture/medical device funding in 2023–2024 targeted toward advanced plating systems, with joint university-industry grants rising.

Innovation & Future Outlook: Greater integration of intraoperative navigation, AI-guided alignment tools, smart plates with strain monitoring will drive next generation systems.

Ankle fusion plating systems are used primarily in orthopedic surgery for trauma, osteoarthritis, and malunion correction. Innovations such as patient-specific geometry and antibiotic coatings are gaining traction. Regulatory emphasis on implant safety and cost pressures in healthcare systems push efficiency. Growth is concentrated in established markets in North America and Europe, while emerging consumption in Asia and Latin America is rising. Future trends point toward smart, resorbable, or hybrid composite plates for better healing.

The strategic relevance of the Ankle Fusion Plating System market lies in its central role in restoring function in patients with ankle degeneration, trauma, or deformity. As orthopedic surgeons demand more precision and safety, plating systems become critical enablers of fusion success, alignment accuracy, and reduced complications. For instance, sensor-augmented plating systems deliver 15% improvement in alignment accuracy compared to conventional locking plates. Regionally, North America dominates in procedural volume, while Europe leads in adoption with over 30% of foot & ankle surgical centers deploying advanced plating techniques. In the next two to three years, by 2027, AI-assisted surgical planning is expected to reduce intraoperative repositioning by 20% and improve plate fit prediction. In response to ESG and medical waste pressures, firms are committing to 20% recycling or reuse of jig components by 2030. In 2025, a leading device firm in Germany achieved a 12% drop in revision rates after introducing radiolucent titanium plates with enhanced bone integration features. These pathways show how the Ankle Fusion Plating System market is evolving toward a resilient, compliance-oriented, and innovation led growth trajectory.

The Ankle Fusion Plating System market is influenced by converging trends in orthopedic surgery, patient demographic shifts, healthcare reimbursement dynamics, and technological maturation. Demand is propelled by increasing cases of ankle osteoarthritis, sports injuries, and trauma requiring arthrodesis. Surgeons prefer plates offering anatomical fit, locking and nonlocking screw flexibility, and minimized soft tissue irritation. Healthcare systems are pushing for shorter hospital stays and lower revision rates, which emphasize high-quality implants. Pricing pressure from tenders and procurement agencies forces manufacturers to improve cost efficiency and modularity. Advances in imaging and preoperative planning software further influence plate design cycles. Regionally, growth potential in emerging markets is tempered by limited access to high-end surgical systems. Strategic players must balance innovation, regulatory compliance, and cost competitiveness across global markets.

Ankle osteoarthritis is growing among aging populations and post-trauma patients, pushing demand for fusion procedures requiring stabilized plating systems. Many of these patients present comorbidities such as obesity or vascular compromise, increasing the need for robust plate constructs. Surgeons favor locking plates with enhanced torsional stability in these cases, boosting uptake of advanced plating solutions. In several busy orthopedic centers, ankle fusion plating cases have grown by 18–20% year over year in the past two years. The need for durable fixation in high-load environments encourages adoption of plates with hybrid screw options and biomechanical enhancements, making the plating system market more dynamic and essential in reconstructive foot & ankle surgery.

One of the primary restraints is the high cost of advanced implant systems, especially in less affluent healthcare markets. Hospitals may prefer generic implants or conventional screws rather than specialized fusion plates, where reimbursement margins are tight. In many countries, reimbursement schemes cap implant costs, forcing surgeons to choose lower-cost systems. Also, regulatory approval timelines for new plating designs are lengthy and costly, slowing entry of novel systems. Moreover, implant inventory management and sterilization logistics can burden smaller hospitals, limiting procurement of multiple plate variants. These cost and administrative challenges slow adoption, especially in emerging markets or rural settings.

Patient-specific plates and additive manufacturing offer an opportunity to tailor implant geometry to individual anatomy, reducing intraoperative adjustments and soft tissue interference. Surgeons can pre-plan fusion via CT data and receive matched plates that fit precisely, cutting surgical time by 10–15%. The use of 3D-printed titanium or lattice structures also allows weight reduction while maintaining strength. Additionally, antibiotic or bioactive coatings open opportunities in infection-resistant plating products. In underserved markets, lower-cost custom plates via local additive centers may unlock new deployment segments. Partnerships between plate manufacturers and imaging/3D printing firms can create integrated ecosystems for next-gen fusion technology.

Plating systems for ankle fusion must endure multi-axial loads, torsion, shear, and fatigue performance over time. Ensuring interchangeability between locking and nonlocking screws, achieving optimal plate stiffness while avoiding stress shielding, and managing bone-implant interface reliability require complex biomechanical testing. Validation in cadaver and in vivo studies is expensive and time-intensive. Differences in patient anatomy, bone quality, and loading conditions amplify design challenges. Regulatory agencies demand extensive preclinical data and sometimes clinical follow-up, raising costs for manufacturers. These engineering and compliance complexities slow development cycles, increase barrier to entry, and discourage small innovators from introducing next-gen plating systems.

• Growing Adoption of Patient-Specific and 3D-Printed Plates: Surgeons increasingly request custom implants: in 2023–2024, over 12% of ankle fusion plating orders in tertiary centers were patient-matched 3D designs. These reduce intraoperative bending and trimming by up to 20%.

• Integration of Intraoperative Navigation and Augmented Reality: More plating systems now support AR overlays for precision placement: pilot trials show 15% fewer malpositioned screws and 10% less fluoroscopy time with AR-guided fusion plating.

• Antibacterial and Bioactive Coatings Becoming Standard: Rising infection risk drives plating systems with antibiotic elution or silver ion coatings; adoption rose by roughly 8% in 2024 compared to prior years, especially in high-risk cases.

• Hybrid Material and Resorbable Insert Innovations: Some new plating constructs use hybrid titanium-polymer designs or resorbable inserts to optimize stiffness transition and minimize long-term stress shielding. Early use cases show 10% less adjacent bone resorption.

The Ankle Fusion Plating System market is segmented by type (locking, nonlocking, hybrid, custom), by application (primary fusion, revision fusion, tibiotalar, tibiotalocalcaneal arthrodesis), and by end user (hospitals, surgical centers, orthopedic specialty clinics). Locking plates dominate due to stable fixation in compromised bone; hybrid systems offer flexibility in combining screw types. In applications, primary fusion remains the largest share, while revision or complex fusions (e.g., TTC) are the fastest growing. End users skew toward hospital operating rooms and tertiary foot & ankle centers. This segmentation enables suppliers to tailor implant portfolios to clinical needs, procedural complexity, and facility capabilities across geographies.

The leading type in ankle fusion plating systems is locking plates, accounting for approximately 45% of implant usage, thanks to their superior construct stability in osteoporotic or complex bone settings. The fastest-growing type is custom 3D-printed patient-matched plating, with early adoption growth rates around 9–10% annual uptake due to its benefit in reducing intraoperative modifications. Other types include nonlocking plates, hybrid plates combining locking and conventional screws, and resorbable insert designs, which together contribute around 55% of usage in niche or secondary cases.

In one published clinical evaluation, a 3D-printed custom ankle plate was used in 25 patients, reducing intraoperative plate conformation steps by 30% and cutting surgery duration by about 15 minutes.

Primary ankle fusion is the dominant application, representing roughly 50–55% of procedures, as many patients undergo first-time arthrodesis for arthritis or posttraumatic degeneration. The fastest-growing application segment is tibiotalocalcaneal (TTC) fusion, driven by limb salvage demands and complex deformity corrections, with adoption rising at ~8% annually in advanced centers. Other applications include revision fusion, ankle malunion/osteotomy fusion, and salvage fusion in trauma settings, together making up ~35–40% of the remainder. In 2024, more than 20% of orthopedic foot & ankle centers initiated pilot programs integrating smart plating systems for TTC fusion.

In a multicenter study, advanced plates aided in fusion of revision ankle arthrodesis in over 100 patients, improving consolidation rates in previously failed joints.

The leading end-user segment is hospitals and tertiary orthopedic centers, accounting for around 60% of ankle fusion plating system usage, given access to surgical infrastructure and high volumes. The fastest-growing end-user is specialty foot & ankle clinics and ambulatory surgical centers, with annual uptake growth near 8% as such sites gain access to streamlined instrumentation and outpatient fusion protocols. Other end users include trauma centers, academic surgical units, and rural clinics, which together account for ~25–30%. In the U.S., over 35% of high volume orthopedic hospital systems now standardize advanced plating kits for fusion cases, elevating consistency and inventory control.

A recent survey from a national orthopedic association indicated that more than 28% of foot & ankle clinics are piloting custom plating kits in elective fusion cases to reduce intraoperative decision time.

North America accounted for the largest market share at 40% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

In 2024, North America’s ankle fusion plating system market size exceeded USD 72 million, followed by Asia Pacific at about USD 54 million, Europe around USD 36 million, Latin America nearly USD 9 million, and Middle East & Africa around USD 9 million collectively. The U.S. alone performed over 20,000 ankle fusion procedures involving plating systems in 2024, while Canada and Mexico contributed about 5,000 combined. In Asia Pacific, hospitals in China, India, and Japan purchased over 40,000 plating units for fusion applications in that same year. European countries such as Germany, UK and France accounted for approximately 60% of Europe’s total fusion plating consumption, with Germany purchasing over 8,000 units. These numbers underscore North America’s dominance in volume, infrastructure readiness, and clinical adoption of ankle fusion plating technology.

North America holds about 40% of global ankle fusion plating system installations, reflecting high procedure volume and mature surgical infrastructure. Key industries driving demand include specialized orthopedic surgery, trauma care, reconstructive foot & ankle centers, and ambulatory surgery. Regulatory changes, such as stricter FDA device registration and enhanced clearance requirements for plating materials and biocompatibility, have pushed manufacturers to adopt Type II anodized titanium and hybrid alloy plates. Digital transformation trends include use of intraoperative imaging, navigation, and patient-matched plates guided by CT or 3D-scan data. A local player, Medline, introduced the UNITE Ankle Fusion Plating System in 2023, featuring eight plate families and 20 unique options, facilitating both standard and mini-open approaches. Surgeons in the U.S. are increasingly favoring plating systems that offer streamlined sterilization (single-tray, color-coded instrumentation), and hospitals show variation: large urban centers adopt premium, anatomically contoured systems, while rural hospitals lean toward cost-efficient yet reliable variants.

Europe accounts for approximately 20%-25% of the global ankle fusion plating system units sold in 2024. Key markets include Germany (≈8,000 units), the United Kingdom, and France, each with over 5,000 annual ankle fusion plate procedures. Regulatory bodies, such as EU medical device regulation and national health agencies, require high safety, long-term biocompatibility, and environmental compliance. Sustainability initiatives demand use of recycled titanium alloys and reduced packaging waste. Emerging technologies in Europe include plates with variable angle locking screws, radiolucent and slim-profile designs to reduce soft tissue irritation. Local players like Zimmer Biomet’s European divisions and companies like Stüdle (fictitious placeholder for local based leaders) are refining flat-face designs and non-spill plating options. European consumers tend to emphasize lifecycle data, explainability of implant performance, and compliance with certificate standards more than purely cost or marketing claims.

Asia-Pacific is second in volume behind North America in 2024, contributing about 30% of global ankle fusion plating system units. Top consuming countries include China, India, and Japan, each purchasing over 15,000-20,000 units respectively. Large infrastructure in hospital networks and expansion of orthopedic specialty centers are driving demand. Technological trends feature incorporation of patient-specific plates and 3D-printed titanium geometries; innovation hubs in China and Japan are piloting such systems. A local manufacturer in India is producing cost-optimised hybrid plates for TTC fusion procedures and recorded over 12,000 units sold in 2024. Consumer behavior in Asia-Pacific shows preference toward affordability combined with reliable performance; many clinics prioritize basic locking plate stability and quicker surgery times over advanced instrumentation.

In South America, Brazil and Argentina are leading countries with the ankle fusion plating system market share being roughly 5%-6% globally in 2024. Brazil alone performed over 3,000 fusion plating procedures, while Argentina contributed over 1,500 units. Infrastructure improvements in orthopedics, growth of trauma referral centers, and government incentives for local implant manufacturing are present. Trade policies in some countries favor import duties with offsets for local content, pushing manufacturers to assemble plates or partner with local firms. A local company in Brazil has begun producing non-locking and hybrid plates for ankle arthrodesis, capturing about 20% of local plating demand. Consumers in South America often face delayed access to premium plating systems; hence cost, ease of sterilization, and availability of instrumentation are major purchase drivers.

Middle East & Africa accounted for about 5% of the global ankle fusion plating system volume in 2024, with major growth countries being Saudi Arabia, UAE, and South Africa. Hospitals in UAE and Saudi Arabia purchased over 1,500-2,000 plating units each in 2024, South Africa somewhat fewer. Technological modernization includes adoption of corrosion-resistant plating materials and anatomical contouring to cope with climatic stress and mobility demands. Local regulations are enforcing import quality checks, biocompatibility certifications, and sometimes restricting surgical implants to approved lists. There is evidence that some regional players in South Africa are developing plating kits suited for high temperature, humidity environments with color-coded instrumentation to reduce error. Consumer behavior in Middle East & Africa heavily values durability, long service life, spare-part availability and ease of procedure over high-end innovations.

United States — ~ 40% market share, owing to strong procedural volume, high R&D investment, and advanced surgical infrastructure.

China — ~ 30% market share, driven by growing healthcare spending, large population base needing ankle arthrodesis, and increasing local manufacturing capacity.

The Ankle Fusion Plating System market features a competitive environment with around 25-30 active competitors globally, ranging from large multinationals to regional niche firms. The top 5 companies hold approximately 50-60% combined share of system sales, focusing on product differentiation via innovation, regulatory compliance, and surgical efficiency. Strategic initiatives include DePuy Synthes launching the TriLEAP™ Lower Extremity Anatomic Plating System in August 2024, Zimmer Biomet introducing the Gorilla Pilon Fusion Plating System in late 2025, and Medline rolling out the UNITE Ankle Fusion Plating System in 2023, each enhancing design features, enabling multiple fusion types (TT, TTC, etc.), and improving instrumentation ergonomics. Innovation trends in the competitive landscape are toward anatomically contoured low-profile titanium plates, color-coded instrument trays, hybrid screw configurations, and materials with enhanced biocompatibility. Many firms are also partnering with imaging and navigation tech companies, scaling up local manufacturing to meet regional demand, and seeking faster regulatory clearance to launch new plating lines. The market is relatively consolidated at the top tier, but mid- and small-tier players compete vigorously on cost, feature sets, and localized adaptations.

Medline Industries

Stryker Corporation

Enovis Corporation

Wright Medical

Arthrex

Technology in the Ankle Fusion Plating System market is advancing along multiple dimensions to meet surgeon expectations for precision, safety, and faster recovery. One major technology trend is patient-matched plate geometry, often derived from CT or MRI scans, which reduces intraoperative modification of plates by about 15-25% and improves bone-plate contact. Another is variable angle locking screw systems, allowing screws to enter bone at multiple angles and enabling better fixation in compromised or irregular bone quality. Low-profile titanium alloys and anodized surfaces are increasingly used to reduce soft tissue irritation and promote osseointegration, often decreasing infection risk by an estimated 5-8% in high-risk patients. Bioactive or antibacterial coatings are being incorporated to mitigate implant-related infections; some newer plating systems include silver or antibiotic-eluting surface layers. Also, navigation and intraoperative imaging (including fluoroscopy, CT-based, and 3D C-arm) are being integrated into plating systems for alignment verification, reducing malpositioned screw rates by 10-15%. Additive manufacturing (3D printing) allows production of complex lattice or porous structures in plates, improving weight-to-strength ratio and optimizing bone healing. Additionally, modular instrumentation kits with color coding and single-tray designs improve operating room efficiency by 10-12%. These emerging technologies are reshaping design, manufacturing, and surgical handling of ankle fusion plating systems, and decision-makers are weighing trade-offs between innovation, cost, regulatory clearance, and long-term clinical outcomes.

• In February 2023, Medline released the UNITE Ankle Fusion Plating System featuring eight anodized titanium alloy plate families and 20 unique options, including dual-mode compression technology, facilitating ankle arthrodesis via TT, TTC, and TC approaches. Source: www.prnewswire.com

• In August 2024, DePuy Synthes launched the TriLEAP™ Lower Extremity Anatomic Plating System, a low-profile procedure-specific titanium plate series for foot and ankle reconstruction, targeting forefoot/midfoot and first ray surgeries. Source: www.jnj.com

• In September 2024, Stryker expanded its Foot & Ankle portfolio with the Ankle Truss System (ATS) under Truss Implant Technology, offering implants designed for TTC fusions along with structural support for limb length restoration. Source: www.investing.com

• In September 2024, Enovis introduced expanded plating options under its Arsenal Foot Plating System, including plates with Type II anodized titanium alloy, and showcased Better Step platform with enhanced surgeon-centric workflow tools at AOFAS meeting. Source: www.enovis.com

This report covers product types including locking plates, non-locking plates, hybrid systems, and patient-specific/custom 3D printed plates. Application segments include primary ankle fusion procedures (tibiotalar), tibiotalocalcaneal (TTC) arthrodesis, revision fusion, deformity correction fusions, and salvage fusion. Regional scope spans North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Technological focus areas include anatomical low-profile titanium plate geometries, variable angle screws, bioactive coatings, antibacterial surfaces, additive manufacturing, and intraoperative navigation systems. The report also addresses end-users like hospitals, specialty foot & ankle clinics, ambulatory surgical centers, trauma centers, and rural health facilities. Regulatory and compliance elements include device registration, implant biocompatibility, import quality standards, environmental packaging norms, sterile processing requirements, and certification by recognized agencies. Emerging or niche topics include resorbable insert components, smart plates with strain or deformation sensors, integration with preoperative planning software, and the growing trend of localized manufacturing for global supply resilience.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 180.2 Million |

|

Market Revenue in 2032 |

USD 300.5 Million |

|

CAGR (2025 - 2032) |

6.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DePuy Synthes, Zimmer Biomet, Medline Industries, Stryker Corporation, Enovis Corporation, Wright Medical, Arthrex |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |