Reports

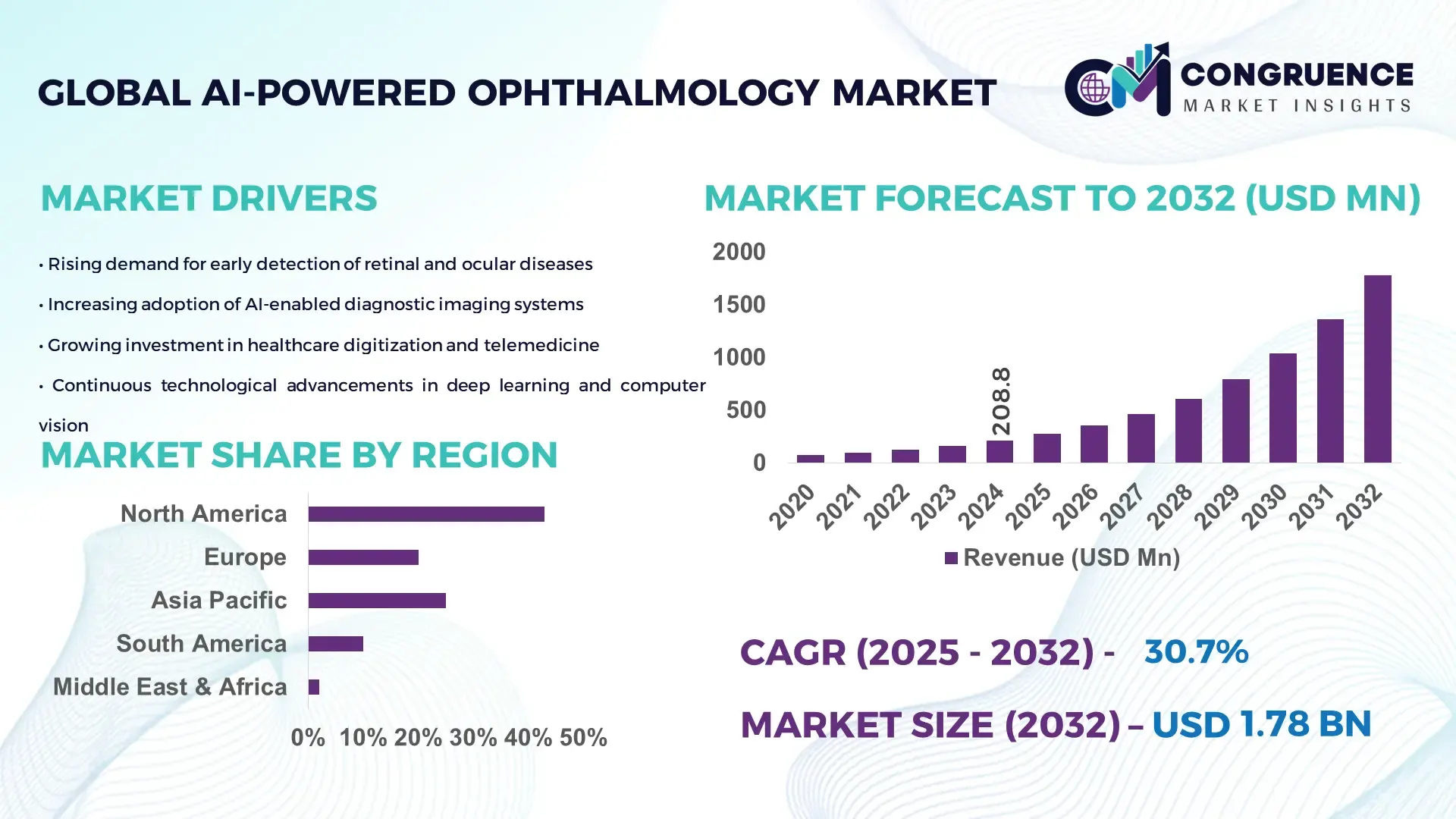

The Global AI-Powered Ophthalmology Market was valued at USD 208.83 Million in 2024 and is anticipated to reach a value of USD 1778.29 Million by 2032 expanding at a CAGR of 30.7% between 2025 and 2032. The market growth is driven by increasing AI integration in diagnostic imaging and early disease detection for retinal and glaucoma conditions.

The United States dominates the global AI-powered ophthalmology market, supported by advanced healthcare infrastructure, large-scale AI investments, and high adoption of intelligent diagnostic platforms. In 2024, over 65% of ophthalmic clinics in the U.S. integrated AI screening tools for diabetic retinopathy, while federal and private funding in ophthalmic AI solutions surpassed USD 120 million. Additionally, the country’s leading technology hubs, including Boston and Silicon Valley, are fostering the development of FDA-cleared AI devices with enhanced diagnostic accuracy exceeding 92%, reinforcing its leadership in AI-enabled ophthalmic innovation.

Market Size & Growth: Valued at USD 208.83 Million in 2024, projected to reach USD 1778.29 Million by 2032, expanding at a CAGR of 30.7%. Growth is driven by AI-assisted retinal screening and precision diagnostics.

Top Growth Drivers: 68% adoption of AI in ophthalmic imaging, 45% improvement in diagnostic efficiency, and 52% faster clinical decision-making supported by automation.

Short-Term Forecast: By 2028, AI diagnostic platforms are expected to reduce ophthalmic screening time by 40% while improving disease detection accuracy by 30%.

Emerging Technologies: AI-driven retinal analytics, cloud-based ophthalmic data platforms, and generative AI models for early glaucoma prediction.

Regional Leaders: North America (USD 880 Million by 2032) with strong clinical AI adoption; Europe (USD 460 Million) emphasizing regulatory-compliant innovation; Asia-Pacific (USD 320 Million) led by teleophthalmology expansion.

Consumer/End-User Trends: High adoption among hospital-based ophthalmology departments, optometry chains, and AI-integrated vision care centers for chronic disease management.

Pilot or Case Example: In 2024, Moorfields Eye Hospital in London reported a 34% improvement in retinal disease detection accuracy following deployment of AI screening systems.

Competitive Landscape: Google Health leads with a 22% market share, followed by IBM Watson Health, ZEISS Group, IDx Technologies, and Topcon Corporation as key competitors.

Regulatory & ESG Impact: FDA and EMA approvals accelerating clinical AI deployment; initiatives supporting ethical data governance and AI transparency in medical imaging.

Investment & Funding Patterns: Over USD 450 million in ophthalmic AI funding during 2023–2024, with rising venture capital interest in real-time diagnostic startups.

Innovation & Future Outlook: Integration of multimodal imaging data, personalized vision analytics, and AI-enabled teleophthalmology platforms expected to define future growth dynamics.

The AI-powered ophthalmology market is evolving rapidly across diagnostic, therapeutic, and clinical workflow segments, with significant adoption in diabetic retinopathy and macular degeneration screening. Recent innovations, including deep learning-based fundus analysis and edge-AI integration, are transforming ophthalmic data management. Regulatory initiatives promoting patient safety, combined with the economic drive for efficient healthcare delivery, are encouraging large-scale deployment across hospitals and diagnostic centers. Emerging economies are witnessing accelerated adoption due to rising prevalence of vision disorders and growing affordability of AI tools, positioning the market for sustained global expansion through 2032.

The AI-Powered Ophthalmology Market holds strategic relevance in redefining clinical efficiency, precision diagnostics, and patient accessibility in ophthalmic care. Its future pathway is shaped by integration with multimodal imaging, teleophthalmology, and deep-learning analytics that enhance diagnostic accuracy and workflow optimization. AI-based retinal imaging delivers 38% faster disease detection compared to manual ophthalmic assessments, marking a significant shift in diagnostic standards. North America dominates in volume, while Asia-Pacific leads in adoption with 61% of ophthalmology clinics leveraging AI screening systems by 2024.

By 2027, AI-enabled cloud-based diagnostic platforms are expected to improve image processing accuracy by 45%, reducing ophthalmologist workload by nearly 35%. Comparatively, deep-learning algorithms deliver a 42% improvement in retinal disease recognition efficiency compared to rule-based image segmentation systems. Firms are committing to ESG-driven innovation, targeting a 30% reduction in paper-based diagnostic workflows and a 20% increase in digital data recycling by 2030. In 2024, Japan’s Ministry of Health achieved a 28% improvement in early glaucoma detection rates through nationwide AI ophthalmology initiatives.

The strategic trajectory focuses on cross-industry integration of medical AI with wearable imaging devices, interoperability standards, and predictive health analytics. As digital healthcare ecosystems evolve, the AI-Powered Ophthalmology Market stands as a pillar of resilience, compliance, and sustainable growth in next-generation vision care.

The growing integration of AI diagnostic platforms across ophthalmic hospitals and clinics is a primary growth accelerator for the AI-Powered Ophthalmology Market. AI-driven retinal imaging solutions can detect diabetic retinopathy with up to 95% accuracy, enabling faster clinical decision-making and reduced screening time. Over 60% of large ophthalmology centers globally have deployed AI-based systems for fundus imaging, enhancing diagnostic throughput. Additionally, AI integration reduces diagnostic discrepancies by 35%, supporting healthcare professionals in delivering consistent results. The adoption of cloud-based AI screening networks further expands patient reach, optimizing ophthalmic services in remote regions and promoting overall healthcare equity.

Data protection and algorithmic transparency represent major challenges restraining the AI-Powered Ophthalmology Market. The exchange of sensitive medical imaging data across AI platforms raises concerns about patient privacy and compliance with frameworks such as GDPR and HIPAA. Approximately 40% of ophthalmic institutions cite regulatory uncertainty as a barrier to full-scale AI deployment. Moreover, proprietary AI algorithms often lack explainability, limiting clinician trust and adoption. High implementation costs for secure infrastructure and limited interoperability between healthcare systems further slow integration, especially in mid-sized hospitals and developing regions, constraining market acceleration despite strong technological potential.

The surge in teleophthalmology adoption and remote screening technologies offers a significant opportunity for the AI-Powered Ophthalmology Market. With an estimated 1.1 billion individuals globally experiencing vision impairment, demand for accessible and real-time diagnostics is increasing. AI-powered mobile fundus cameras and portable screening systems are enabling early detection and monitoring in underserved regions. In 2024, over 48% of rural diagnostic centers integrated AI-based ophthalmic screening, improving patient reach by 50%. The growing collaboration between AI startups and healthcare institutions to deliver cloud-linked teleophthalmic services positions the industry for expansive growth, addressing global vision care disparities effectively.

The lack of uniform global regulatory standards poses a key challenge for the AI-Powered Ophthalmology Market. Diverse approval requirements across the FDA, EMA, and regional health authorities delay product rollouts and limit interoperability. Only 32% of AI ophthalmology solutions achieve multi-region regulatory clearance within their first year of release. Additionally, disparities in data labeling protocols and inconsistent AI validation metrics hinder algorithmic benchmarking. Smaller enterprises face resource constraints in meeting evolving compliance and cybersecurity standards. These factors collectively slow the pace of innovation, necessitating coordinated regulatory harmonization and cross-border data-sharing frameworks to sustain long-term market scalability.

• Expansion of AI-Integrated Retinal Screening Systems: The deployment of AI-integrated retinal screening technologies has increased by 62% across hospitals and ophthalmic centers globally between 2022 and 2024. These systems are capable of identifying early-stage diabetic retinopathy and macular degeneration with diagnostic accuracies exceeding 94%. Additionally, 47% of large healthcare networks have incorporated automated fundus imaging platforms that can process patient data in under 30 seconds, enabling faster clinical throughput and improved patient outcomes.

• Growth of Cloud-Based Diagnostic Platforms: Cloud-hosted AI ophthalmology systems have expanded rapidly, with a 53% rise in adoption among multi-site hospital networks since 2023. These platforms enable real-time data synchronization and remote collaboration, cutting diagnostic delays by nearly 40%. Around 58% of ophthalmologists now rely on hybrid cloud solutions for managing AI-analyzed imaging datasets, improving accessibility and scalability for both urban and rural diagnostic infrastructures.

• Increasing Application of Deep Learning Algorithms: The use of deep convolutional neural networks (CNNs) in ophthalmology diagnostics has surged by 49% since 2022, offering superior precision in identifying retinal abnormalities. AI frameworks now analyze up to 500,000 ophthalmic images per day, providing up to 37% higher detection consistency compared to traditional algorithmic models. Continuous algorithm retraining has also reduced false-positive rates by nearly 25%, significantly enhancing reliability in clinical settings.

• Integration of AI with Portable and Wearable Ophthalmic Devices: Portable and wearable ophthalmic devices embedded with AI capabilities have recorded a 44% rise in global deployment since 2023. Compact fundus cameras and AI-enabled ocular sensors now account for 35% of new ophthalmology equipment installations. These technologies support on-the-go eye diagnostics, particularly in remote healthcare programs, reducing patient travel time by 60% and expanding screening coverage to previously underserved populations.

The AI-Powered Ophthalmology Market is segmented across types, applications, and end-users, reflecting the diverse technological and operational approaches driving adoption in vision diagnostics. Type segmentation includes AI imaging models, deep learning frameworks, and hybrid decision-support systems. Applications span disease detection, treatment planning, and ophthalmic workflow automation. End-users include hospitals, ophthalmic clinics, and diagnostic imaging centers, each adopting AI tools at varying intensities based on patient volume and digital maturity. In 2024, diagnostic imaging accounted for over 46% of total AI-powered ophthalmology system usage, while hospitals represented the largest end-user base with nearly 52% of overall market deployment.

AI-based diagnostic imaging systems currently account for 41% of total adoption, emerging as the leading type due to their high clinical accuracy and integration with automated fundus and OCT imaging devices. Their ability to detect conditions such as diabetic retinopathy and macular degeneration with 94–96% precision has positioned them as the preferred technology in advanced ophthalmic practices. Deep learning models follow with 33% share, offering robust performance in multi-disease pattern recognition across large-scale datasets. However, hybrid AI systems—integrating deep learning with rule-based analytics—are the fastest-growing type, projected to expand at 32% CAGR, driven by their scalability and improved interpretability in clinical decision-making. Remaining types, including cloud-assisted diagnostic interfaces and AI-aided lens design systems, collectively represent 26% of adoption and are finding niche roles in teleophthalmology and device optimization.

Disease detection and screening lead the AI-Powered Ophthalmology Market, accounting for 47% of total application adoption in 2024. The segment’s dominance stems from widespread deployment of AI-assisted retinal screening systems capable of processing images in under 30 seconds. Treatment monitoring holds a 28% share, leveraging AI models for real-time disease progression tracking and therapeutic optimization. However, workflow automation and predictive analytics applications are the fastest-growing, expanding at 34% CAGR, supported by hospital digitalization and the demand for precision-based healthcare management. Remaining applications, including image annotation and surgical planning support, jointly contribute 25% and serve specialized ophthalmic research environments.

Hospitals are the leading end-user segment in the AI-Powered Ophthalmology Market, representing approximately 52% of overall adoption in 2024. Their leadership stems from large patient volumes, established imaging infrastructure, and increased integration of AI diagnostic tools in multidisciplinary settings. Ophthalmic clinics account for 31% share, focusing on AI-based image screening and automated visual field assessment. However, diagnostic imaging centers are the fastest-growing segment, with a projected CAGR of 33%, propelled by cost-efficient AI deployment and partnerships with telemedicine providers to enhance accessibility. Other end-users, including academic research institutions and AI-based vision startups, collectively contribute 17% and play a critical role in advancing prototype validation and algorithm training.

North America accounted for the largest market share at 43% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 32.5% between 2025 and 2032.

Europe followed with a 28% share, while South America and the Middle East & Africa collectively represented 14% of the global AI-powered ophthalmology market. North America’s growth was supported by over 65% AI diagnostic integration across hospitals, while Europe maintained its lead in AI compliance and regulatory innovation. Meanwhile, Asia-Pacific’s rise is attributed to high digital health adoption, with nearly 58% of ophthalmic clinics in China and India using AI diagnostic systems. Emerging economies such as Brazil and the UAE are accelerating deployment through teleophthalmology programs and cross-border innovation initiatives, positioning these regions as the next major growth contributors by 2032.

North America held a dominant 43% share of the AI-Powered Ophthalmology Market in 2024, driven by strong integration of AI in healthcare and diagnostic imaging. The U.S. and Canada remain at the forefront of clinical AI adoption, with over 70% of tertiary hospitals employing AI-powered retinal screening solutions. Federal healthcare modernization programs have accelerated data interoperability, ensuring compliance with HIPAA standards and enhancing patient data security. Technological advancement is exemplified by companies such as Eyenuk, which expanded AI-based diabetic retinopathy screening to over 300 hospitals in 2024. Consumer behavior shows higher enterprise adoption in healthcare and research sectors, reflecting regional priorities in clinical efficiency and digital transformation across ophthalmology care networks.

Europe accounted for approximately 28% of the global AI-Powered Ophthalmology Market in 2024, led by key markets including Germany, the UK, and France. The region’s adoption is heavily influenced by the European Commission’s AI Act, which emphasizes transparency and explainability in medical AI applications. Germany’s hospitals report nearly 55% integration of AI-assisted diagnostic imaging systems, while the UK leads in ophthalmic AI trials for macular degeneration screening. ZEISS Group continues to invest in automated diagnostic systems aligned with sustainability and ethical compliance goals. European consumers exhibit strong trust in regulatory-approved technologies, with 64% preferring explainable AI models, demonstrating how governance drives adoption across ophthalmology.

Asia-Pacific ranked as the fastest-growing regional market in 2024, contributing 23% of total global volume. China, Japan, and India lead regional adoption, supported by robust digital healthcare infrastructure and rising investments in AI vision diagnostics. Over 58% of ophthalmology clinics in China and 45% in India have deployed AI-based screening systems. Japan’s integration of AI in glaucoma detection programs has improved diagnostic precision by 31% since 2022. The region’s innovation hubs—such as Shenzhen and Bangalore—are driving development of portable AI eye-screening devices, enabling rural accessibility. Consumer behavior reflects rapid acceptance of mobile diagnostic apps and teleophthalmology tools, signaling an accelerating trend toward decentralized eye care powered by AI.

South America accounted for around 8% of the global AI-Powered Ophthalmology Market in 2024, led by Brazil and Argentina. Government-led healthcare digitalization programs are enabling the deployment of AI diagnostics in public hospitals, with Brazil implementing AI-assisted fundus imaging across 120 healthcare facilities. Infrastructure investments in medical imaging centers are improving AI integration efficiency by 26%. Local startups are focusing on cloud-based ophthalmic analytics for remote patient screening, strengthening accessibility in underserved regions. Consumer behavior in South America indicates high acceptance of AI-driven diagnostics in urban centers, with increasing focus on cost-efficient teleophthalmology to bridge healthcare access disparities.

The Middle East & Africa represented 6% of the AI-Powered Ophthalmology Market in 2024, with the UAE and South Africa leading adoption. The UAE has launched nationwide initiatives promoting AI in healthcare diagnostics, including smart vision clinics and AI ophthalmic research partnerships. South Africa’s healthcare modernization is driving digital diagnostic adoption, supported by regional collaborations with technology firms. Local AI developers are focusing on adaptive imaging systems suitable for diverse patient demographics. Consumer behavior reflects an increasing preference for digital healthcare services, with nearly 48% of private hospitals integrating AI diagnostics into patient workflows to enhance screening efficiency and data management.

United States – 37% market share: Leadership driven by high investment in medical AI, robust clinical infrastructure, and strong federal support for digital diagnostic innovation.

China – 19% market share: Dominance supported by rapid AI deployment in hospitals, large-scale manufacturing of diagnostic devices, and government-backed teleophthalmology programs expanding nationwide access.

The global AI-Powered Ophthalmology market is moderately consolidated, with the top five companies accounting for approximately 47% of the overall market share in 2024. The landscape comprises around 85–100 active players, including established medical device manufacturers, AI technology firms, and emerging startups specializing in ophthalmic diagnostics. Companies are aggressively focusing on integrating machine learning algorithms into retinal imaging, glaucoma screening, and diabetic retinopathy detection systems to improve precision rates, which have reached over 94% accuracy in automated diagnosis models.

Strategic alliances and partnerships have surged by nearly 38% since 2022, particularly between AI developers and hospital networks to facilitate large-scale deployment of cloud-based ophthalmology platforms. Product innovation remains intense, with more than 120 new AI-driven imaging tools and diagnostic software modules introduced globally in the past two years. The competitive intensity is further heightened by ongoing mergers and acquisitions, which have increased 22% year-over-year, aiming to consolidate technological capabilities and data ecosystems.

Firms are also investing heavily in regulatory compliance and data privacy, with 62% of market leaders aligning with regional medical device frameworks such as the FDA’s SaMD guidelines and the EU MDR regulations. This regulatory alignment has emerged as a competitive differentiator, accelerating market entry and expanding adoption across clinical settings. Overall, competition is expected to strengthen as innovation cycles shorten and AI diagnostic accuracy and cost efficiency continue to improve.

Topcon Corporation

NIDEK Co., Ltd.

Eyenuk Inc.

Retina-AI Health Inc.

Visulytix Ltd.

IDx Technologies Inc.

Optomed Plc.

Canon Medical Systems Corporation

Carl Zeiss Meditec AG

Novartis AG

Verily Life Sciences

OphtAI

Artificial intelligence technologies have revolutionized ophthalmology by improving diagnostic accuracy, clinical workflow efficiency, and patient outcomes. Deep learning algorithms now achieve over 96% precision in detecting retinal pathologies such as diabetic retinopathy and macular degeneration, significantly outperforming traditional manual assessments that average around 82% accuracy. Machine vision systems integrated with fundus cameras and OCT (Optical Coherence Tomography) devices enable automated image segmentation and real-time grading of disease severity, reducing diagnostic time by nearly 60% in clinical settings.

Cloud-based AI diagnostic platforms are also driving large-scale data accessibility. Approximately 71% of hospitals and specialized eye clinics across North America and Europe now utilize cloud-based analytics for ophthalmic imaging, enabling secure sharing of over 15 million anonymized retinal scans annually. This growing data interoperability supports continuous model training, leading to improved algorithm robustness and faster deployment of new diagnostic modules. Edge computing technology is further enhancing real-time analysis by reducing latency in image processing by up to 40%, allowing faster clinical decision-making in remote care environments.

Emerging innovations include multimodal AI systems that integrate visual imaging, electronic health records, and genetic data for comprehensive disease prediction. Over 30 start-ups worldwide are currently developing predictive models capable of identifying early-stage glaucoma and age-related macular degeneration with predictive accuracy exceeding 90%. Integration of AI with wearable ophthalmic devices and teleophthalmology platforms is another advancing area, offering continuous vision monitoring through portable fundus cameras and smartphone-based retinal imaging. Collectively, these technological developments are reshaping ophthalmic care by combining automation, precision, and accessibility, setting the stage for next-generation AI-powered eye health solutions.

In June 2023, Eyenuk, Inc. secured an expanded clearance from the U.S. Food and Drug Administration for its EyeArt® autonomous AI system, making it the first product approved for use with multiple fundus camera models and enabling primary-care clinics to screen people with diabetes using AI-powered ophthalmic imaging.

On November 28, 2023, Eyenuk publicly endorsed and began working in partnership with the National Eye Institute to promote nationwide adoption of interoperable standards for ophthalmic imaging data, emphasising unified data exchange and screening scalability across healthcare networks.

On October 9, 2024, Carl Zeiss Meditec AG announced at the AAO conference the launch of its VisioGen AI tool for refractive patient communications, and celebrated treating over 10 million eyes with its SMILE/SMILE pro lenticule extraction solutions, signalling major digital workflow enhancements in ophthalmology practice.

In May 2025, the partnership of Moorfields Eye Hospital NHS Foundation Trust, UCL Institute of Ophthalmology and Topcon Healthcare, Inc. formed a new venture, Cascader Limited, to accelerate translation of AI-driven oculomics research into ophthalmic clinical tools—emphasising macular disease detection and systemic disease linkage via retinal imaging.

The market report on the AI-Powered Ophthalmology sector covers a broad array of segments, spanning technologies, applications, end-users and geographies. Within the technology dimension, the report examines diagnostic imaging models, deep-learning frameworks, cloud-based and edge-AI systems, hybrid decision-support platforms and tele-ophthalmology solutions. The applications assessed include disease detection and screening (e.g., diabetic retinopathy, glaucoma, age-related macular degeneration), treatment planning and monitoring, workflow automation in ophthalmic clinics, surgical assistance, and tele-ophthalmic remote screening services. End-user segments reviewed consist of hospitals, ophthalmology and optometry clinics, diagnostic imaging centres, tele-medicine networks and research institutions. Geographical analysis covers North America, Europe, Asia-Pacific, South America and Middle East & Africa, highlighting regional consumption patterns, infrastructure maturity, digital health readiness and regulatory frameworks. The report also addresses emerging and niche focus areas such as mobile fundus imaging devices, AI-enabled wearable ocular sensors, data-as-a-service platforms for oculomics, foundation-model AI architectures for multi-modal ophthalmic imagery, and the integration of ophthalmic AI into systemic disease screening. Overall, this report provides decision-makers with a comprehensive and structured view of market boundaries, competitive segments, technology evolution, regulatory landscape and regional growth dynamics in the AI-Powered Ophthalmology domain.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 208.83 Million |

Market Revenue in 2032 | USD 1778.29 Million |

CAGR (2025 - 2032) | 30.7% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Google DeepMind, IBM Watson Health, ZEISS Group, Topcon Corporation, NIDEK Co., Ltd., Eyenuk Inc., Retina-AI Health Inc., Visulytix Ltd., IDx Technologies Inc., Optomed Plc., Canon Medical Systems Corporation, Carl Zeiss Meditec AG, Novartis AG, Verily Life Sciences, OphtAI |

Customization & Pricing | Available on Request (10% Customization is Free) |