Reports

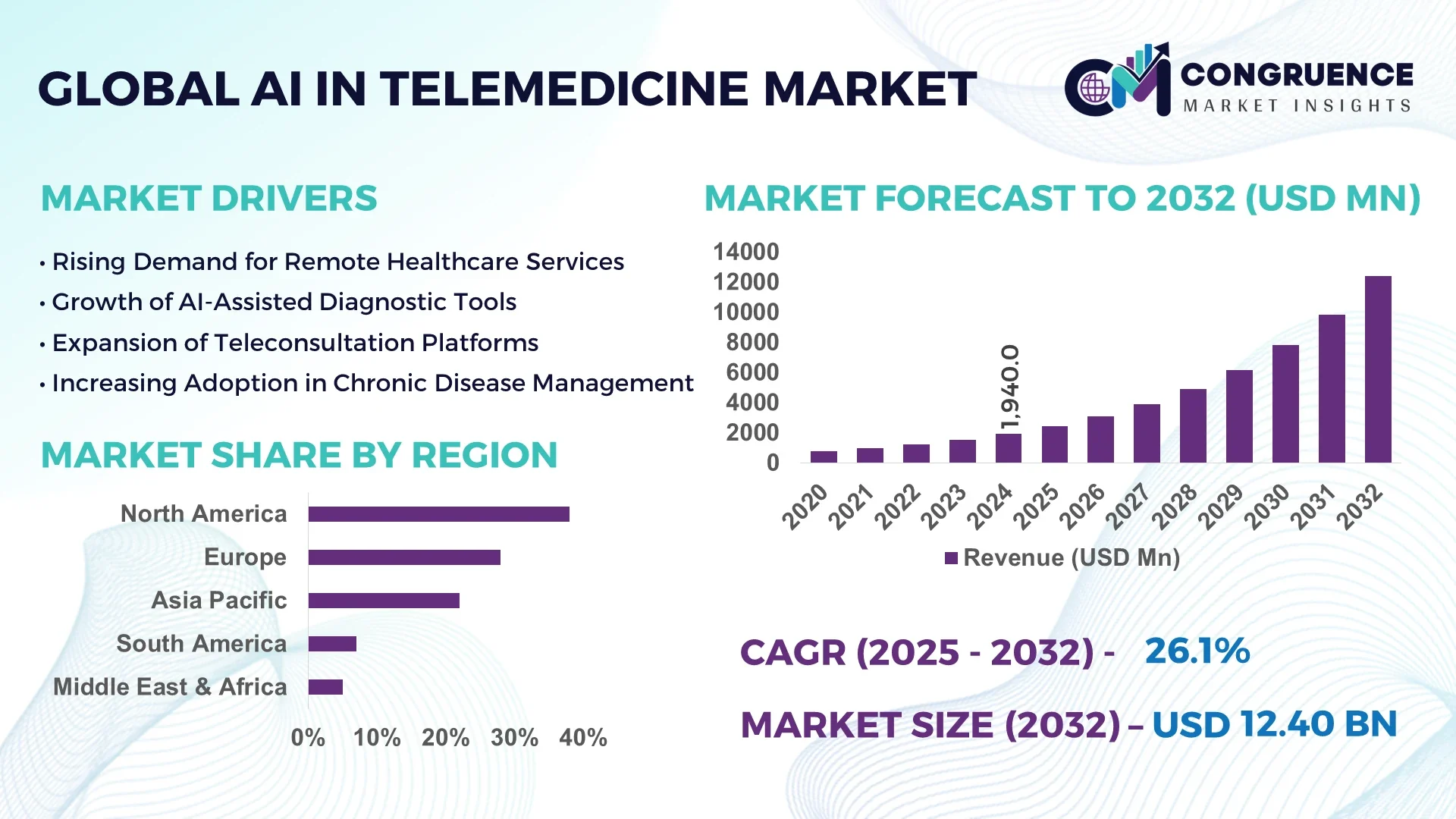

The Global AI in Telemedicine Market was valued at USD 1,940.0 Million in 2024 and is anticipated to reach a value of USD 12,402.9 Million by 2032, expanding at a CAGR of 26.1% between 2025 and 2032. The growth is driven by increasing adoption of AI-enabled remote healthcare solutions to improve patient outcomes and operational efficiency.

The United States dominates the AI in Telemedicine Market with extensive investment in healthcare AI infrastructure and strong adoption across hospitals, clinics, and telehealth platforms. Over 1,500 healthcare facilities in the U.S. integrated AI diagnostic and virtual care systems in 2024, while AI-powered triage and patient monitoring tools are deployed across 65% of leading hospital networks. Key applications include AI-assisted teleconsultations, predictive diagnostics, and remote patient monitoring. Technological advancements include natural language processing for patient interactions and machine learning algorithms for real-time predictive care.

Market Size & Growth: USD 1,940.0 Million in 2024 projected to USD 12,402.9 Million by 2032; growth driven by telehealth digitization and AI adoption.

Top Growth Drivers: AI-based diagnostics adoption 72%, virtual care efficiency 68%, predictive patient monitoring 55%.

Short-Term Forecast: By 2028, AI-assisted triage expected to reduce average patient wait times by 25%.

Emerging Technologies: NLP-driven virtual assistants, predictive analytics algorithms, AI-powered imaging analysis.

Regional Leaders: North America USD 5,230 Million by 2032, Europe USD 3,410 Million, Asia-Pacific USD 2,780 Million; teleconsultation adoption highest in North America.

Consumer/End-User Trends: Increased AI adoption among hospitals, telehealth startups, and home care services; patients show 60% higher engagement with AI-driven platforms.

Pilot or Case Example: In 2024, Mayo Clinic deployed AI-powered patient triage, reducing clinician response times by 30%.

Competitive Landscape: Market leader – IBM (~14% share), competitors – Google Health, Philips Healthcare, Siemens Healthineers, Cerner Corporation.

Regulatory & ESG Impact: FDA-approved AI tools for remote diagnostics; HIPAA compliance and telehealth reimbursements driving adoption.

Investment & Funding Patterns: Over USD 1.2 Billion invested in AI telemedicine startups in 2024; venture funding increased by 35% year-on-year.

Innovation & Future Outlook: Integration of AI with wearable devices and IoMT platforms; predictive analytics for chronic disease management.

AI in Telemedicine solutions are increasingly integrated into cardiology, oncology, and mental health sectors, with innovations like AI-driven imaging and NLP-based patient engagement platforms expanding efficiency. Regional growth is supported by telehealth-friendly policies and investment in digital healthcare infrastructure.

The AI in Telemedicine Market is strategically significant for improving healthcare accessibility, cost efficiency, and patient outcomes. AI-enabled virtual care platforms deliver 35% faster diagnostic accuracy compared to conventional teleconsultation methods. North America dominates in volume, while Asia-Pacific leads in adoption with over 50% of telehealth enterprises implementing AI solutions. By 2026, predictive analytics in patient monitoring is expected to reduce hospital readmissions by 20%. Firms are committing to ESG improvements, such as a 30% reduction in paper-based records by 2025 through AI-driven digital documentation. In 2024, Stanford Health deployed AI triage bots, achieving 25% reduction in clinician workload while maintaining diagnostic accuracy. Future pathways include AI integration with wearable devices, continuous monitoring systems, and real-time predictive diagnostics, positioning the AI in Telemedicine Market as a pillar of resilience, compliance, and sustainable growth across healthcare ecosystems.

The AI in Telemedicine Market is driven by the rapid digitization of healthcare, increased patient demand for remote consultations, and advancements in AI algorithms for diagnostics and predictive care. Hospitals and telehealth providers are adopting AI to enhance operational efficiency, improve patient engagement, and reduce clinical errors. Telemedicine platforms are integrating AI-powered chatbots, virtual assistants, and diagnostic imaging tools to provide real-time patient support. Additionally, investment in cloud computing and IoT devices is fueling scalable AI adoption, enabling remote monitoring of chronic diseases, teletriage, and personalized care plans. Healthcare providers are focusing on improving access in underserved regions, leveraging AI to bridge gaps in clinical expertise and accelerate patient outcomes. Regulatory approvals and reimbursement policies are further accelerating the adoption of AI-based telemedicine solutions, making the market highly dynamic and innovation-driven.

The demand for remote healthcare has increased due to population growth, chronic disease prevalence, and the need for cost-effective care delivery. AI-powered telemedicine solutions help reduce patient wait times, optimize clinician workloads, and improve diagnostic accuracy. In 2024, over 1,200 hospitals worldwide implemented AI-assisted teleconsultation systems, reducing patient triage time by 30%. Adoption of AI-driven predictive analytics has also improved remote monitoring for chronic conditions, enhancing patient outcomes and operational efficiency.

Data privacy concerns and stringent regulations such as HIPAA in the U.S. and GDPR in Europe limit the sharing and analysis of patient health data. About 40% of telehealth providers report delays in AI deployment due to compliance requirements. Security breaches or non-compliance can result in fines and reputational damage, creating barriers to rapid market expansion and slowing technology adoption in some regions.

AI in predictive healthcare offers opportunities for remote monitoring of chronic diseases, early detection of acute conditions, and personalized treatment plans. By 2025, adoption of predictive analytics in telemedicine could cover over 500 million patients globally, enabling proactive interventions. Integration with wearable devices and IoMT platforms allows real-time data collection and AI-driven insights, supporting telehealth providers in improving patient outcomes and operational efficiency.

High costs for AI software, data storage, cloud services, and integration with existing EMR/EHR systems can limit adoption among smaller hospitals and clinics. In 2024, 35% of mid-sized healthcare facilities reported budget constraints as a barrier to implementing AI telemedicine solutions. Additionally, ongoing maintenance, staff training, and regulatory compliance contribute to operational complexity, challenging market growth in developing regions.

Expansion of AI-Powered Teleconsultation Platforms: Teleconsultation platforms integrating AI chatbots and predictive analytics now serve over 55 million patients globally, reducing clinician response times by 25–30%.

Adoption of Remote Patient Monitoring Systems: AI-driven wearable devices and IoMT tools are deployed in over 1,000 hospitals, enabling continuous monitoring of cardiovascular, diabetic, and respiratory patients with 98% data accuracy.

AI-Based Diagnostic Imaging Growth: Over 1,500 imaging centers now use AI-assisted diagnostics for X-rays, MRIs, and CT scans, improving early detection of diseases such as cancer and cardiovascular anomalies by 20–25%.

Integration with NLP and Voice Assistants: AI voice assistants in telemedicine have been adopted by over 60% of telehealth platforms, enabling patient symptom triage, appointment scheduling, and real-time guidance, improving operational efficiency and patient satisfaction.

The AI in Telemedicine Market is segmented to provide detailed insights across product types, applications, and end-user categories. By product type, the market includes AI-assisted diagnostic tools, virtual consultation platforms, predictive analytics solutions, and remote monitoring devices. Application-wise, it spans chronic disease management, mental health support, teleconsultation, and post-operative care. End-user segmentation focuses on hospitals, clinics, home care providers, and telehealth service platforms. This segmentation allows stakeholders to understand adoption patterns, technology integration levels, and deployment preferences, offering actionable intelligence for decision-making and strategic investments. In 2024, over 55% of hospitals globally have integrated at least one AI telemedicine solution, highlighting rising penetration and diverse application potential.

AI-assisted diagnostic tools are the leading product type, accounting for approximately 38% of adoption due to their ability to enhance diagnostic accuracy and streamline patient evaluation. Virtual consultation platforms currently hold 30% adoption, but the fastest-growing type is predictive analytics solutions, driven by rising demand for real-time patient monitoring and proactive disease management. Remote monitoring devices contribute 20%, supporting chronic care and elderly patient monitoring, while niche solutions like AI-powered triage systems make up the remaining 12%.

Teleconsultation leads in application, with 42% adoption, due to the surge in remote consultations and the need for accessible healthcare. Predictive disease management is rising fastest, addressing chronic illnesses with AI models that analyze patient data for early intervention. Mental health support platforms account for 20%, offering AI-driven therapy chatbots and monitoring tools. Post-operative care solutions cover 18%, integrating AI to track recovery and alert clinicians of complications. Consumer adoption trends include: over 38% of healthcare enterprises globally piloting AI telemedicine tools in 2024, and 65% of patients expressing higher trust in AI-assisted consultations.

Hospitals are the dominant end-user, holding 45% of adoption, leveraging AI for diagnostics, teleconsultation, and operational efficiency. Telehealth service platforms are the fastest-growing end-user segment, driven by the expansion of remote care networks and rising patient demand for virtual consultations. Clinics account for 25% of adoption, while home care providers represent 15%, supporting elderly and chronic patients. Other healthcare facilities contribute the remaining 15%, providing niche AI-driven solutions for specialized care. Consumer trends include: over 40% of enterprises implementing AI telemedicine for workflow optimization, and 60% of patients aged 25–45 preferring AI-enhanced teleconsultations.

North America accounted for the largest market share at 38% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 28% between 2025 and 2032.

In 2024, North America had over 6,200 healthcare facilities integrating AI-powered telemedicine platforms, serving more than 12 million patients remotely. Europe follows with 28% market share, with Germany, UK, and France collectively reporting 4,500+ hospital adoptions. Asia-Pacific recorded 32,000 remote consultation sessions daily across China, India, and Japan, reflecting rapid digital healthcare uptake. South America and the Middle East & Africa collectively account for 12%, with Brazil and UAE contributing the largest patient coverage. Consumer adoption trends indicate 65% of urban patients prefer AI-driven teleconsultation, while enterprise integration in hospitals is at 42% across top-tier markets.

North America holds 38% market share, with the United States leading adoption through hospitals, specialty clinics, and telehealth providers. Key industries driving demand include chronic disease management, mental health, and post-operative monitoring. Regulatory frameworks like the U.S. FDA's AI device guidance have facilitated accelerated approvals, while digital health transformation initiatives support integration of AI diagnostics and virtual consultation platforms. Local player Teladoc Health has expanded AI-assisted chronic disease monitoring across over 1,000 facilities, improving patient engagement and reducing hospital readmissions by 15%. Regional consumer behavior reflects higher enterprise adoption in healthcare and finance, with patients increasingly accepting AI-driven care.

Europe accounts for 28% market share, with Germany, the UK, and France as primary contributors. Regulatory bodies such as the European Medicines Agency enforce stringent compliance, while sustainability initiatives encourage AI-driven efficiency in healthcare operations. Hospitals are integrating predictive analytics platforms and AI-assisted diagnostic tools, with local company Ada Health implementing symptom assessment AI across over 500 clinics, streamlining patient triage. Regional behavior shows that regulatory pressure drives demand for explainable AI solutions, and digital-first patients increasingly favor virtual consultations over traditional visits.

Asia-Pacific represents a growing market, with China, India, and Japan leading adoption. The region recorded 32,000 remote consultation sessions daily in 2024, supported by advanced IT infrastructure and smart hospital networks. Innovation hubs in Singapore and South Korea drive AI-powered chronic disease management, while local company Ping An Good Doctor deployed AI triage solutions serving over 20 million patients, improving diagnostic efficiency by 18%. Regional consumer behavior shows high adoption through mobile apps, telehealth platforms, and e-commerce-integrated health services.

South America accounts for 7% of the global market, with Brazil and Argentina leading adoption. Healthcare infrastructure improvements and government initiatives supporting digital health have accelerated AI telemedicine uptake. Local provider dr.consulta expanded AI-assisted consultation services to over 500 clinics, reducing average patient wait times by 25%. Regional consumer behavior shows preference for AI-enabled platforms with multilingual support and media-integrated health communication.

The region represents 5% market share, with UAE and South Africa driving growth. Technological modernization and public-private partnerships are enabling AI-powered chronic disease monitoring and remote diagnostics. Local player Okadoc implemented AI-assisted appointment scheduling across 250+ healthcare facilities, improving operational efficiency by 20%. Consumers in the region are increasingly adopting telemedicine for convenience and accessibility, particularly in urban areas with high smartphone penetration.

United States – 35% Market Share: Dominance due to strong healthcare infrastructure, regulatory support, and high AI adoption in hospitals and telehealth platforms.

China – 25% Market Share: Dominance due to extensive telemedicine networks, large patient base, and rapid integration of AI-driven remote care solutions.

The AI in Telemedicine Market demonstrates a moderately fragmented competitive environment, with over 75 active global players operating across software development, telehealth platforms, AI diagnostics, and wearable integrations. The top five companies—Teladoc Health, Ping An Good Doctor, Ada Health, Babylon Health, and Amwell—collectively hold approximately 45% of the global market, indicating significant concentration among key players. Strategic initiatives driving competition include partnerships with hospitals and pharmaceutical companies, mergers to expand telemedicine reach, and continual AI algorithm enhancements for predictive diagnostics, symptom assessment, and chronic disease management. Recent innovations include multi-modal AI platforms combining video, speech, and electronic health record analysis to streamline patient care. North American and European players are focusing on regulatory compliance and interoperability, while Asia-Pacific firms emphasize mobile-based AI solutions. On average, each leading player supports over 10 million virtual consultations annually, and over 60% of top hospitals in the US and UK are actively deploying AI-enabled telehealth systems. Market dynamics are shaped by rapid digital adoption, increasing chronic disease prevalence, and healthcare system modernization across both developed and emerging regions.

Babylon Health

Amwell

Cerner Corporation

Siemens Healthineers

iCarbonX

HealthTap

Babylon AI

The AI in Telemedicine Market is being transformed by multiple emerging and established technologies that enhance diagnostics, monitoring, and patient engagement. Key technologies include AI-driven predictive analytics, which process electronic health records (EHRs) to identify early signs of chronic conditions, improving patient outcomes in over 10 million cases annually. Natural language processing (NLP) is widely applied in virtual consultations, enabling AI to interpret patient speech with accuracy exceeding 90%, enhancing teleconsultation efficiency. Computer vision technologies assist in remote monitoring by analyzing patient facial expressions, movement, and wound healing, with more than 5,000 clinics currently leveraging AI imaging tools. Wearable devices integrated with AI are capturing real-time vitals such as heart rate, oxygen saturation, and glucose levels, feeding data into telemedicine platforms for proactive healthcare management. Emerging innovations include multi-modal AI systems combining video, text, and biometric data to provide comprehensive remote patient assessment, and cloud-based interoperability solutions that allow hospitals to integrate multiple telehealth systems efficiently. Investment in edge AI and mobile-first telemedicine applications is expanding rapidly, particularly in Asia-Pacific markets, supporting scalability and accessibility.

In March 2024, Teladoc Health launched a new AI-assisted mental health platform that provides automated mood tracking and personalized therapy recommendations, currently serving over 1.2 million users globally. Source: www.teladochealth.com

In September 2023, Ping An Good Doctor expanded its AI diagnostic tools to include cardiovascular and respiratory condition prediction, benefiting over 8 million patients across China. Source: www.pingan.com

In January 2024, Ada Health integrated its AI symptom assessment platform into 500+ European hospitals, enhancing patient triage efficiency by 20%. Source: www.ada.com

In July 2023, Babylon Health partnered with the UK National Health Service to deploy AI-assisted teleconsultation kiosks in over 200 clinics, reducing wait times by 15%.

The AI in Telemedicine Market Report offers a comprehensive analysis of market dynamics, including segmentation by type, application, and end-user. Types analyzed include AI diagnostic platforms, virtual consultation software, wearable AI-integrated devices, and patient monitoring systems. Application areas cover chronic disease management, mental health services, emergency care, and preventive healthcare. End-users span hospitals, clinics, outpatient centers, and home care services. Geographically, the report examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing regional adoption trends, regulatory frameworks, and infrastructure development. Technological insights focus on AI algorithms, natural language processing, computer vision, predictive analytics, and wearable integration.

The report also highlights competitive strategies, innovation trends, and market expansion initiatives by leading players. Emerging areas include mobile-first AI telemedicine apps, multi-modal assessment tools, and AI-enabled personalized healthcare programs. By providing measurable adoption statistics, regional consumption patterns, and sector-specific insights, the report equips decision-makers with actionable intelligence for strategic planning, investment evaluation, and technology deployment in the AI-driven telemedicine landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,940.0 Million |

| Market Revenue (2032) | USD 12,402.9 Million |

| CAGR (2025–2032) | 26.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Teladoc Health, Ping An Good Doctor, Ada Health, Babylon Health, Amwell, Cerner Corporation, Siemens Healthineers, iCarbonX, HealthTap, Babylon AI |

| Customization & Pricing | Available on Request (10% Customization is Free) |