Reports

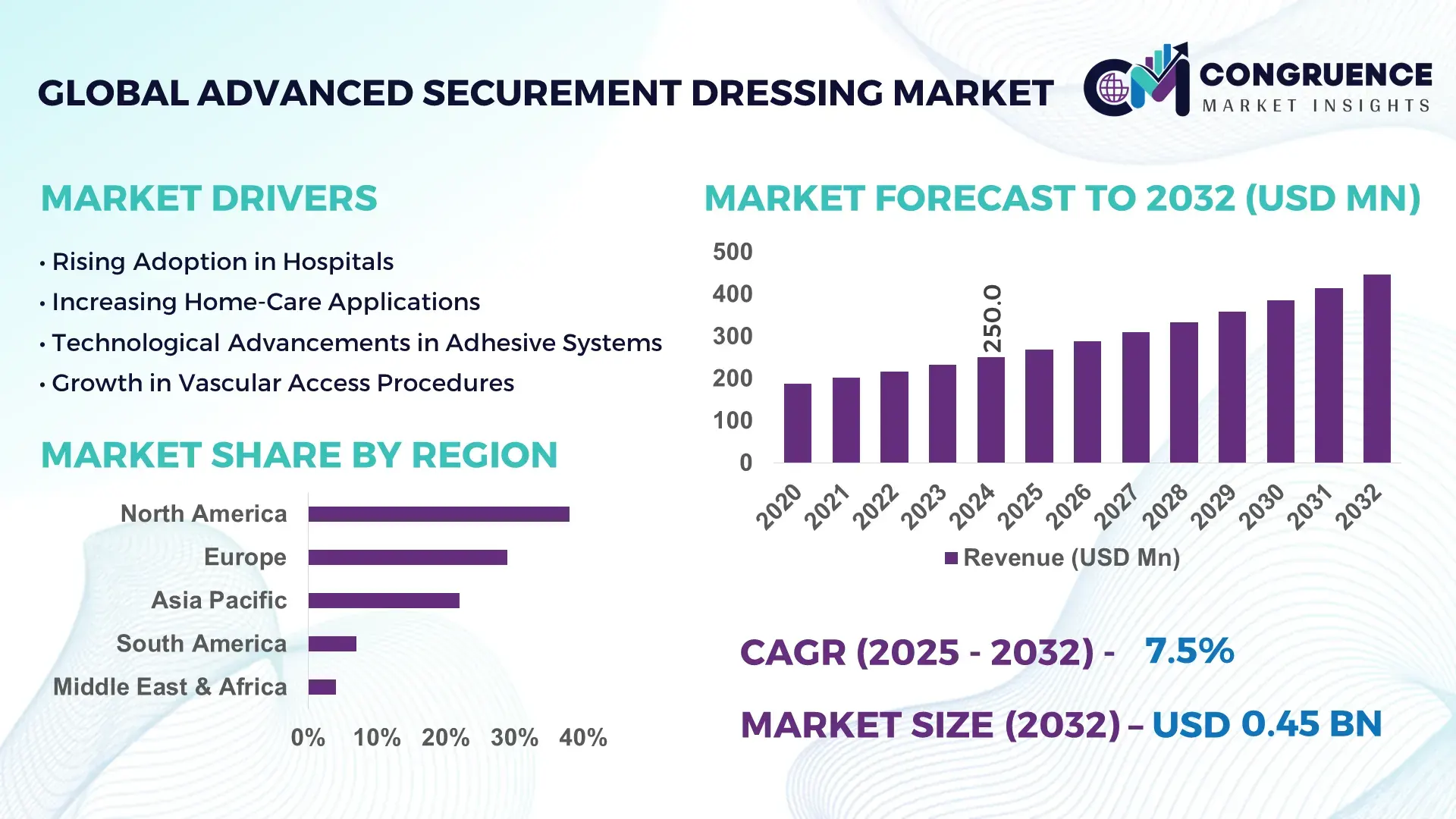

The Global Advanced Securement Dressing Market was valued at USD 250.0 Million in 2024 and is anticipated to reach a value of USD 445.9 Million by 2032 expanding at a CAGR of 7.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by rising healthcare-associated infection (HAI) prevention protocols across acute care and outpatient settings.

The United States remains the leading country in the Advanced Securement Dressing Market, supported by advanced production facilities investing over USD 120 million annually in R&D for catheter stabilization and IV securement solutions. More than 68% of hospitals in the U.S. have adopted integrated securement systems, supported by strong clinical guidelines and high utilization in vascular access, trauma, and oncology care. Furthermore, FDA-cleared antimicrobial securement technologies saw a 22% rise in procurement in 2023, reflecting strong technological adoption.

Market Size & Growth: Valued at USD 250.0 Million in 2024 and projected to reach USD 445.9 Million by 2032, expanding at 7.5% CAGR, supported by rising usage in vascular access and critical care procedures.

Top Growth Drivers: Increased catheter-related infection prevention (31%), improved device retention performance (27%), and rising clinical adoption of antimicrobial variants (22%).

Short-Term Forecast: By 2028, device failure-related complications are expected to reduce by 18% with next-generation securement innovations.

Emerging Technologies: Smart pressure-sensing dressings and advanced hydrocolloid–silicone hybrids are gaining traction as next-stage securement technologies.

Regional Leaders: North America expected to reach USD 185 Million by 2032, Europe USD 110 Million, and Asia Pacific USD 95 Million, with APAC showing rapid clinician adoption of safety-centric securement solutions.

Consumer/End-User Trends: High adoption among ICUs, oncology centers, and vascular access clinics, with 62% preferring multi-day wear securement products.

Pilot or Case Example: In 2024, a U.K. pilot program achieved 21% reduction in catheter dislodgement through antimicrobial-integrated securement dressings.

Competitive Landscape: Market leader commands ~18% share, followed by major players including 3M, BD, Smith & Nephew, Medline, and ConvaTec.

Regulatory & ESG Impact: Increasing compliance with safety mandates and low-plastic packaging directives is accelerating the shift toward sustainable securement solutions.

Investment & Funding Patterns: Over USD 95 Million invested recently in product innovation, sustainable materials, and expanded production automation.

Innovation & Future Outlook: Advancements in breathable multilayer structures, extended-wear adhesives, and infection-prevention materials will shape next-stage market evolution.

Unique Information:

Advanced securement dressings are increasingly used across vascular access, infusion therapy, and trauma care, with hospitals contributing nearly 60% of consumption. Recent innovations in antimicrobial adhesives, extended-wear silicone layers, and breathable backing films are enhancing dressing durability and patient comfort. Regulatory emphasis on infection prevention, rising surgical volumes, and improved clinical workflow efficiency continue to drive adoption across regional healthcare ecosystems.

The strategic relevance of the Advanced Securement Dressing Market lies in its growing role in clinical safety, infection prevention, and optimization of vascular access procedures. As healthcare systems push for reduced catheter-related complications, securement innovations are becoming central to improving clinical outcomes. New-generation antimicrobial securement dressings deliver a 28% improvement compared to older polyurethane-based standards, making them crucial for modern patient safety protocols. North America dominates in volume, while Europe leads in adoption with 64% of enterprises integrating advanced securement devices into standardized care pathways.

By 2028, AI-enabled material engineering is expected to improve dressing performance consistency by 20% through enhanced adhesion analytics and predictive wear-time modeling. Healthcare providers are increasingly prioritizing ESG commitments as well, with 40% of hospitals targeting a 25% reduction in non-recyclable medical consumables by 2030. In 2024, Japan achieved a 19% decrease in catheter failure rates through nationwide implementation of sensor-integrated securement systems, demonstrating measurable impact from technology-led clinical upgrades.

Looking ahead, the market will experience expanded use of hybrid silicone technologies, ergonomic stabilization designs, breathable antimicrobial films, and sustainable material innovations. With global healthcare infrastructure shifting toward safer, more efficient vascular access management, the Advanced Securement Dressing Market is poised to become a pillar of resilience, clinical compliance, and sustainable long-term growth in patient safety systems.

The Advanced Securement Dressing Market is shaped by rising demand for improved catheter stabilization, growing emphasis on hospital-acquired infection (HAI) prevention, and the shift toward advanced silicone- and hydrocolloid-based dressings. Healthcare facilities are increasingly prioritizing long-wear, skin-friendly securement products, driven by the surge in chronic disease management, infusion therapies, and critical care procedures. Trends indicate a strong move toward antimicrobial integration, breathable multilayer designs, and reduced dressing change frequency. Additionally, improvements in clinical workflow efficiency, the growth of outpatient and home infusion therapy, and enhanced clinical guidelines are influencing product design, adoption, and innovation within this market.

Increasing global focus on preventing catheter-related bloodstream infections (CRBSIs) is significantly driving the adoption of advanced securement dressings. Hospitals are implementing stringent infection control protocols, where securement dressings with antimicrobial coatings and extended-wear adhesives play a vital role. Clinical observations indicate that improved stabilization can reduce device dislodgement incidents by up to 23%, lowering associated complications. The surge in infusion therapy volumes, with over 2 billion catheter insertions annually worldwide, has increased the need for high-performance securement options. Moreover, advancements in breathable, moisture-management backing films enhance comfort and reduce skin irritation, prompting wider adoption across surgical, emergency, and intensive care units.

Despite technological advancements, skin integrity concerns remain a major restraint. Certain patient groups—such as neonates, the elderly, and individuals with fragile skin—experience higher risks of medical adhesive-related skin injuries (MARSI) when using strong adhesive securement dressings. Studies indicate that up to 21% of catheterized patients report some form of skin trauma during dressing removal, leading clinicians to hesitate in adopting certain high-strength adhesive formats. Additionally, variation in wear-time tolerance, moisture accumulation, and difficulty in removal pose challenges in sensitive care environments. These concerns create barriers for widespread adoption, especially in long-term care settings and pediatric departments.

Emerging antimicrobial technologies and digital health integrations are creating new opportunities for product differentiation. Antimicrobial agents embedded into dressings can significantly reduce pathogen growth, offering high-potential adoption in ICUs and oncology care. Furthermore, sensor-enabled dressings capable of detecting moisture buildup, adhesive failure, or early signs of infection open pathways for smart clinical monitoring. With digital health integration increasing by 34% in major hospitals, these solutions align with the growing need for remote monitoring and real-time insights. Additionally, advancements in eco-friendly materials support sustainability goals, opening new segments in markets prioritizing environmental compliance.

Increasing global regulatory standards and material compliance mandates present operational challenges for manufacturers. Requirements for biocompatibility testing, skin irritation assessments, and antimicrobial safety validations extend development timelines and raise production costs. Variations in regional regulatory frameworks make it difficult for manufacturers to standardize product formulations across international markets. Additionally, the shift toward sustainable materials introduces supply chain complexities as companies transition from traditional plastics to recyclable or bio-based compounds. These factors create delays in product launches, increase certification burdens, and elevate overall production risk.

Growth of Advanced Antimicrobial Adhesive Technologies: The market is seeing rapid adoption of antimicrobial adhesive dressings, with usage increasing by 29% in high-risk clinical units. New formulations integrating silver-ion and chlorhexidine compounds demonstrate up to 35% reduction in microbial colonization. Hospitals are increasingly prioritizing these technologies to support infection control strategies, particularly in vascular access and critical care environments.

Surge in Extended-Wear Silicone Securement Solutions: Extended-wear silicone dressings offering 5–7-day adherence have recorded a 32% rise in adoption, driven by improved patient comfort and reduced dressing change frequency. Clinical trials show skin-tear reduction of 26% compared to conventional acrylic adhesives. Demand is particularly strong in oncology, home infusion, and long-duration catheter placements.

Expansion of Eco-Efficient and Low-Waste Dressing Designs: Sustainability is shaping product development, with 41% of new product lines incorporating recyclable or reduced-plastic components. Manufacturing advances enable up to 18% reduction in material waste. Europe and Japan are leading adoption due to strict environmental regulations and hospital sustainability commitments.

Integration of Smart Monitoring Features: Sensor-enabled securement dressings capable of monitoring moisture, tension, or early infection indicators have grown by 22% in development pipelines. Pilot implementations show 17% reduction in premature dressing failures and better adherence to clinical protocols. These innovations align with the broader trend of digital health integration across hospitals.

The segmentation of the Advanced Securement Dressing Market spans three core dimensions—type, application, and end-user category—each presenting distinct adoption patterns, material preferences, and product innovation requirements. Across product types, advanced adhesive dressings, antimicrobial dressings, and hybrid silicone–hydrocolloid formats dominate usage due to their compatibility with long-wear clinical protocols. Application-wise, vascular access procedures, infusion therapy, oncology treatments, and trauma care constitute the major demand clusters, reflecting high procedural volumes in both inpatient and outpatient settings. End-users such as hospitals, specialty clinics, and home-care providers show varied adoption intensity driven by procedural frequency, patient acuity, and compliance requirements. Overall, segmentation data indicates steadily rising adoption across high-acuity medical environments, increasing preference for extended-wear solutions, and growing integration of skin-friendly adhesives and infection-prevention materials.

Advanced securement dressings are categorized into antimicrobial dressings, silicone-based securement dressings, hydrocolloid dressings, and hybrid multilayer adhesive systems. Among these, antimicrobial securement dressings currently lead the market with an estimated 38% share, supported by widespread use in infection-prone vascular access and invasive device stabilization scenarios. Silicone-based securement dressings follow with approximately 27% adoption, favored for their skin-friendly adhesive characteristics, especially in neonatal, geriatric, and long-term care environments. While these segments show strong adoption, hybrid silicone–hydrocolloid systems are the fastest-growing category, projected to expand at nearly 9.2% CAGR, driven by their extended-wear capacity, moisture management properties, and compatibility with multi-day catheter retention requirements. Other product types—such as transparent film dressings and foam-backed securement variants—collectively contribute around 35% of the remaining market, serving niche needs including high-mobility applications, moisture-heavy skin environments, and emergency care stabilization. These categories continue to see incremental product improvements focused on breathability and shear resistance. Recent authoritative data indicate accelerating adoption of silicone-based dressings in clinical settings.

Advanced securement dressings are used across vascular access stabilization, infusion therapy, central venous catheter (CVC) securement, peripherally inserted central catheter (PICC) procedures, wound management, and trauma care. Vascular access stabilization remains the leading application with an estimated 41% share, driven by the high global volume of peripheral IV insertions and the need for secure catheter retention in acute care settings. Infusion therapy accounts for approximately 26%, with increased demand stemming from oncology care, long-term medication delivery, and chronic disease management. Compared to these segments, CVC and PICC securement are expanding rapidly and represent the fastest-growing application category, projected to grow at 8.7% CAGR, supported by rising procedural complexity and stringent infection-prevention requirements. Other applications—including wound-edge stabilization and post-operative dressing securement—together contribute around 33% of the remaining share, reflecting broader usage in surgical and outpatient environments. Consumer adoption trends show that in 2024, nearly 37% of hospitals globally piloted upgraded securement solutions to reduce dressing change frequency and improve patient comfort. Additionally, more than 52% of infusion therapy centers reported transitioning toward extended-wear securement formats for multi-day treatments.

Hospitals represent the leading end-user group, accounting for approximately 48% of total adoption, driven by high patient volumes, complex care requirements, and adherence to advanced infection-prevention and catheter stabilization protocols. Specialty clinics hold around 28% share, particularly in oncology, dialysis, and vascular access specialty centers where securement performance directly influences procedural success. Meanwhile, the home-care and ambulatory care segment is the fastest-growing end-user category, expanding at 9.5% CAGR, supported by the rise in chronic care at home, increased infusion therapy outside hospital settings, and the need for long-wear, low-irritation dressings. Remaining end-users—including emergency medical services, long-term care facilities, and rehabilitation centers—collectively contribute roughly 24% of the market. Adoption among these groups correlates with growth in remote treatment programs and the demand for easy-to-apply securement systems. Trends show that in 2024, nearly 43% of outpatient centers globally adopted enhanced securement products to reduce complication rates. Additionally, surveys indicate that 58% of home infusion patients prefer silicone-based securement options due to comfort and reduced skin trauma.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2025 and 2032.

The global landscape of advanced securement dressings reflects significant regional contrasts driven by healthcare expenditure, clinical adoption patterns, regulatory emphasis, and supply-chain maturity. North America benefits from high device utilization rates, with more than 72% of hospitals standardizing advanced securement systems across critical care units. Europe follows with a 29% share, supported by stringent patient-safety regulations and increased chronic disease incidence. Asia-Pacific, holding 22% in 2024, is experiencing rapid expansion due to rising surgical volumes, growth of tertiary care facilities, and increased penetration of local manufacturers. South America and the Middle East & Africa collectively represent the remaining 11% but are showing momentum as government investments in infection control rise and procurement reforms improve access to advanced medical consumables.

North America held 38% of the global market share in 2024, supported by a mature clinical infrastructure, high procedure volumes, and strong purchasing power across hospitals and ambulatory centers. Demand is largely driven by the healthcare, home-care, and biotechnology sectors, where securement dressings are required for IV lines, catheters, and long-term infusion therapies. Regulatory agencies have tightened guidelines on infection prevention, increasing the uptake of antimicrobial and transparent securement options. Digital transformation continues to influence procurement, with more than 58% of hospitals adopting digital inventory systems to optimize consumable usage. Local players in the region have expanded portfolios of breathable, advanced adhesive technologies tailored for sensitive-skin patient groups. Consumer behavior in North America shows higher reliance on technologically enhanced medical products, with adoption rates in healthcare and finance exceeding 60% for advanced safety solutions—indicating a strong preference for innovation-driven brands.

Europe accounted for 29% of the market in 2024, with Germany, the UK, and France representing over 60% of regional consumption. These countries benefit from structured healthcare systems, standardized procurement frameworks, and strong clinician awareness related to catheter-related complication prevention. Regulatory bodies have intensified requirements on biocompatibility, sterility, and patient-safety compliance, encouraging the use of next-generation securement solutions. Sustainability initiatives—such as reducing petroleum-based consumables—have also influenced product innovation. European healthcare providers have embraced digital wound-management tools, and adoption of emerging technologies such as antimicrobial hydrogels and sensor-integrated dressings continues to increase. Local manufacturers have introduced eco-optimized securement lines with reduced plastic content to meet regulatory objectives. Consumer behavior in Europe reflects a strong preference for clinically validated and regulation-friendly solutions, further amplifying demand for standardized, explainable advanced securement products.

Asia-Pacific held 22% of the global market volume in 2024, ranking as the fastest-expanding region due to increasing surgical admissions, rapid urbanization, and growing healthcare investments. China, India, Japan, and South Korea collectively account for more than 78% of regional consumption. Expanding hospital networks, rising adoption of advanced catheter procedures, and emerging domestic manufacturing clusters have boosted availability of cost-efficient securement dressings. Major innovation hubs in China and Japan are advancing breathable, antimicrobial, and latex-free securement designs, driving regional differentiation. Local players continue to scale production capacities to meet export and domestic demand. Consumer behavior across Asia-Pacific highlights strong adoption of digital health platforms, e-commerce procurement channels, and mobile-based clinical tools—further accelerating distribution of medical consumables across the region. Growth is supported by rising clinical awareness and broader integration of infection-prevention solutions across public and private healthcare systems.

South America represented 7% of the global market share in 2024, with Brazil and Argentina accounting for more than 68% of regional demand. The region’s healthcare modernization efforts, including expanded ICU infrastructure and increased access to infusion and catheter services, contribute to growing adoption of securement dressings. Infrastructure development across public hospitals continues, particularly in Brazil, where procurement reforms have improved access to advanced consumables. Government incentives promoting domestic medical manufacturing are strengthening supply resilience. Local companies have begun introducing competitively priced sterile securement solutions tailored for humid climates. Consumer behavior in South America favors products that support media, patient-education content, and language-localized instructions—improving user compliance and boosting regional adoption. Demand trends also correlate with increasing investments in telehealth and remote-care models that require support products for home-based infusion therapy.

The Middle East & Africa region held 4% of the global share in 2024, driven by healthcare expansion across UAE, Saudi Arabia, South Africa, and Kenya. Demand is influenced by large-scale construction of hospitals, upgrading of trauma-care networks, and growth in chronic disease treatments requiring catheterization and IV therapies. Technological modernization—such as transitioning to automated inventory systems and smart hospital infrastructure—is improving adoption rates of advanced securement solutions. Regulatory bodies are increasing oversight on sterilization standards, encouraging providers to shift toward premium dressing options. Local manufacturers and distributors have expanded partnerships with global brands to improve availability. Consumer behavior in the region reflects rising expectations for durability, comfort, and heat-tolerant medical products, particularly in high-temperature climates. Trade partnerships and government healthcare funding continue to enhance market penetration across both urban and emerging centers.

United States – 34% Market Share: Dominance supported by high healthcare spending, advanced clinical standards, and strong adoption of catheter-related infection-prevention solutions.

Germany – 12% Market Share: Leadership attributed to stringent medical regulations, strong hospital networks, and high procedural volume involving vascular access and wound care.

The Advanced Securement Dressing Market is characterized by a moderately consolidated structure, with approximately 25–30 active global competitors supplying a diverse range of securement solutions across hospitals, ambulatory care centers, long-term care facilities, and home healthcare settings. The top five companies collectively command around 48–52% of the global market share, supported by strong product portfolios, extensive distribution networks, and recurring procurement contracts with major healthcare systems. Competitive dynamics are shaped by continuous product innovation, with more than 60% of leading companies launching updated catheter securement devices, antimicrobial dressings, or adhesive technologies between 2022 and 2024. Partnerships with hospitals for clinical evaluations, small-scale acquisitions of specialty dressing manufacturers, and the integration of advanced polymer science and breathable multi-layer constructions further intensify market rivalry.

The competitive landscape is also influenced by rising investments in skin-friendly silicone adhesives, extended-wear dressings, and sterile, pre-assembled securement kits, which have gained significant traction in markets with high device utilization rates. Around 40% of established vendors have expanded their presence in Asia-Pacific through localized manufacturing or distribution agreements. Technology-driven differentiation is increasing as companies integrate ergonomic designs, moisture-management layers, and enhanced tensile strength features to meet diverse clinical needs. Overall, the market competitiveness continues to rise, driven by regulatory compliance requirements, infection-prevention priorities, and growing demand from high-acuity care environments.

Derma Sciences

ConvaTec Group

Cardinal Health

3M

Medline Industries

Mölnlycke Health Care

Hollister Incorporated

Technological advancement in the Advanced Securement Dressing Market is shaped by innovations in materials science, bio-compatibility engineering, adhesive chemistry, and infection-prevention design. One of the most significant developments is the shift toward silicone-based adhesives, which reduce medical-adhesive-related skin injuries (MARSI) and improve patient comfort during prolonged device wear. Silicone dressings now represent an estimated 35–40% of technologically advanced securement products, driven by high adoption in critical care and pediatric settings.

Antimicrobial-integrated securement dressings, incorporating agents such as chlorhexidine gluconate (CHG), have become increasingly prevalent, with nearly 30% of new product introductions since 2023 including antimicrobial features to support infection control protocols. Innovations in breathable multi-layer foam structures, hydrocolloid-reinforced borders, and moisture-lock systems enhance dressing adherence while minimizing maceration risks. Additionally, manufacturers are adopting polyurethane film technologies to improve moisture vapor transmission rates (MVTR), enabling dressings to remain effective for extended periods.

Digital integration is also emerging, with early-stage developments in sensor-enabled securement dressings capable of monitoring moisture, tension, and skin condition. These prototypes are under evaluation in high-dependency care units and aim to reduce device dislodgement incidents, which are responsible for thousands of unplanned line replacements annually. Automation in manufacturing, including precision-cut adhesive layering and advanced sterilization techniques, further enhances product consistency and safety. With continuous advancements in biocompatible materials, ergonomic construction, and antimicrobial protection, technology remains a key differentiator across global vendors.

In April 2024, Smith & Nephew published new laboratory data showing that its ALLEVYN LIFE foam dressing dissipates 30–45% of mechanical energy via a novel “layer-on-layer sliding” mechanism, helping to mitigate shear forces that contribute to pressure injuries. Source: www.smith-nephew.com

In Q1 2025 (reported for 2024 activity), Smith & Nephew began the U.S. launch of a new antimicrobial Ag+ foam dressing named ALLEVYN Ag+ Surgical, featuring gentle silicone adhesion (ComfortSTAY) and flexible HighFLEX design for better wear during patient movement. Source: www.smith-nephew.com

In October 2024, Convatec announced that a second randomized controlled trial (RCT) for its InnovaMatrix® AC (a porcine placental-derived extracellular matrix device) had received Institutional Review Board (IRB) approval in the U.S., supporting its growing clinical evidence base for wound management in venous leg ulcers and diabetic foot ulcers. Source: www.convatecgroup.com

In February 2024, Convatec introduced the Esteem Body™ with Leak Defense™ ostomy system in Europe (Italy), which uses advanced adhesive technology (Durahesive®) designed to maintain a secure seal. Although this is an ostomy product, Convatec’s expertise in adhesive and securement technologies may influence their broader securement dressing portfolio. Source: www.convatecgroup.com

The Advanced Securement Dressing Market Report provides a comprehensive assessment of the global landscape, covering product types, clinical applications, end-user categories, and geographical regions. The report evaluates the full range of securement solutions, including silicone-based dressings, CHG-integrated dressings, polyurethane film dressings, foam-border dressings, and specialized catheter and tubing securement systems. It analyzes adoption trends across major clinical settings such as hospitals, surgical centers, neonatal units, emergency care, and home healthcare environments, offering quantifiable insights into usage patterns, performance requirements, and preference shifts.

Geographically, the report examines market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting variations in regulatory frameworks, healthcare infrastructure, procurement trends, and technology adoption. Segmentation analysis includes detailed coverage of device-stabilization practices, infection-prevention priorities, and skin-integrity management strategies across different regions.

The scope further extends to technological advancements such as antimicrobial integration, breathable composite structures, silicone adhesive innovations, and emerging digital-monitoring capabilities. It also considers competitive benchmarking, product portfolios, distribution networks, and strategic initiatives from leading industry players. Additionally, the report incorporates insights into supply chain structures, material availability, and manufacturing developments, providing a complete, decision-ready perspective for healthcare providers, investors, and industry stakeholders seeking to evaluate current and future market trajectories.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 250.0 Million |

| Market Revenue (2032) | USD 445.9 Million |

| CAGR (2025–2032) | 7.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Smith & Nephew, Medtronic, BD (Becton, Dickinson and Company), Derma Sciences, ConvaTec Group, Cardinal Health, 3M, Medline Industries, Mölnlycke Health Care, Hollister Incorporated |

| Customization & Pricing | Available on Request (10% Customization Free) |