Reports

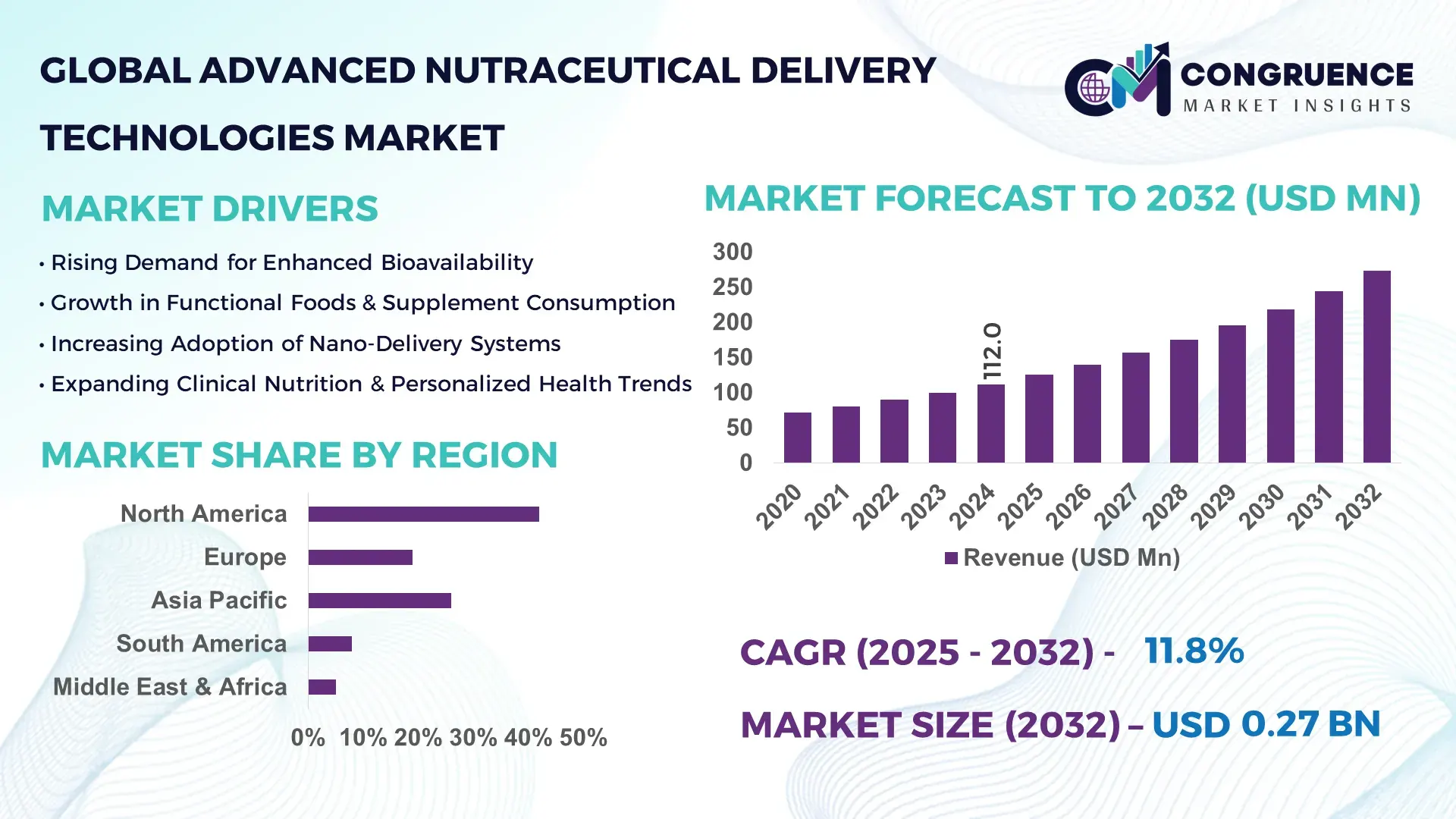

The Global Advanced Nutraceutical Delivery Technologies Market was valued at USD 112.0 Million in 2024 and is anticipated to reach a value of USD 273.4 Million by 2032, expanding at a CAGR of 11.8% between 2025 and 2032, according to an analysis by Congruence Market Insights, driven by increasing adoption of functional foods and targeted nutrient delivery solutions.

The United States dominates the Advanced Nutraceutical Delivery Technologies Market, with significant investments in production facilities and R&D centers exceeding USD 450 million in 2024. The country has over 200 active nutraceutical manufacturing plants integrating advanced encapsulation, liposomal, and nanoemulsion technologies. Key applications include personalized nutrition, cognitive health, and immune support, with consumer adoption rates of innovative delivery systems exceeding 38% among health-conscious adults. U.S.-based research institutions have collaborated with industry players to develop over 50 patented nutrient delivery formulations in the past three years, reflecting high technological advancement and production capacity.

Market Size & Growth: Current market value of USD 112.0 Million, projected to reach USD 273.4 Million by 2032, driven by rising functional food demand.

Top Growth Drivers: Adoption of nanoemulsion systems 42%, encapsulation efficiency improvement 35%, sustained-release formulations 28%.

Short-Term Forecast: By 2028, nutrient bioavailability expected to improve by 25% through advanced delivery methods.

Emerging Technologies: Liposomal encapsulation, nanoemulsion-based delivery, and microencapsulation of sensitive nutrients.

Regional Leaders: North America USD 98.0 Million (2024), Europe USD 65.0 Million, Asia-Pacific USD 32.0 Million by 2032, with unique adoption trends per region.

Consumer/End-User Trends: High adoption among health-conscious adults, personalized nutrition uptake reaching 38% in 2024.

Pilot or Case Example: In 2024, a U.S. functional beverage brand improved nutrient absorption by 22% through liposomal vitamin delivery pilot.

Competitive Landscape: DSM Nutrition (approx. 18% share), followed by Gattefossé, Lonza, BASF, and Evonik.

Regulatory & ESG Impact: FDA guidance on novel food ingredients and EU health claims regulations encourage product innovation and sustainable practices.

Investment & Funding Patterns: Over USD 200 Million invested in nutraceutical delivery technology startups and pilot projects in 2024.

Innovation & Future Outlook: Integration of AI for formulation optimization, automated encapsulation systems, and next-generation nano-carrier research shaping future market.

Advanced Nutraceutical Delivery Technologies Market activity is concentrated in functional beverages, dietary supplements, and fortified foods. Technological innovations in nanoemulsions and liposomal carriers are enabling higher nutrient stability and absorption. Regulatory trends in health claims, environmental sustainability, and personalized nutrition adoption are driving regional consumption growth, particularly in North America and Europe, while Asia-Pacific shows emerging interest in e-commerce and mobile health applications.

The Advanced Nutraceutical Delivery Technologies Market is strategically significant as it enables the targeted delivery of bioactive compounds, enhancing efficacy and consumer compliance. Liposomal encapsulation delivers up to 30% higher nutrient bioavailability compared to traditional powdered formulations. North America dominates in production volume, while Europe leads in adoption, with 40% of functional food enterprises integrating advanced delivery methods. By 2026, AI-driven formulation optimization is expected to improve nutrient stability by 20%, while firms are committing to ESG goals such as 15% reduction in packaging waste by 2027. In 2024, a U.S.-based dietary supplement company achieved a 22% increase in vitamin absorption efficiency using nanoemulsion technology. The market’s forward-looking trajectory positions it as a pillar of resilience, innovation, and sustainable growth in the global nutraceutical sector.

The Advanced Nutraceutical Delivery Technologies Market is experiencing rapid evolution driven by growing consumer awareness of health and wellness, rising prevalence of chronic diseases, and technological advancements in nutrient delivery. Innovations such as liposomal encapsulation, nanoemulsions, and microencapsulation are improving nutrient stability, bioavailability, and product shelf-life. Functional beverages, fortified foods, and dietary supplements are key applications driving market expansion. Manufacturers are increasingly integrating AI and machine learning for formulation optimization, reducing production inefficiencies. Meanwhile, regulatory compliance and ESG considerations are shaping product development, fostering sustainable innovation. The interplay of rising demand, technological integration, and regional adoption trends underscores a robust market trajectory.

Rising consumer preference for health-optimized diets and personalized nutrition is fueling adoption of advanced delivery technologies. Nanoemulsion and liposomal systems enhance bioavailability of vitamins, minerals, and phytochemicals by 20–30%, supporting superior efficacy in dietary supplements. The growing functional beverage sector, with a 38% uptake of advanced delivery formulations in North America, is also contributing significantly. These technologies are enabling manufacturers to differentiate products, expand product portfolios, and meet regulatory requirements for nutrient claims, thereby stimulating sustained market growth.

Strict regulatory frameworks, including FDA novel ingredient approvals and EU health claim standards, impose high compliance costs, slowing new product introductions. Advanced technologies such as nanoemulsions and liposomal encapsulation require specialized equipment and skilled personnel, increasing operational expenses by 18–25%. Small and mid-sized enterprises face barriers to entry due to capital-intensive production processes. Furthermore, consumer skepticism regarding new delivery systems can limit initial adoption, creating short-term market restraints despite growing demand for enhanced bioavailability solutions.

The rise of personalized nutrition offers significant growth potential. Integrating AI-driven nutrient profiling with advanced delivery systems can enhance targeted supplementation, optimizing health outcomes for specific demographics. Companies are exploring microencapsulation for age-specific vitamins and probiotics, addressing consumer demand for precision nutrition. Pilot programs in 2024 demonstrated a 22% increase in nutrient absorption using liposomal carriers in functional beverages. These innovations create opportunities for new product launches, premium offerings, and cross-sector partnerships with healthcare providers.

Fluctuating prices for phospholipids, emulsifiers, and carrier materials increase production costs by 15–20%, impacting profit margins. Technical complexity in scaling nanoemulsion or liposomal systems limits rapid deployment in mass-market products. Equipment investments for encapsulation and precise dosing can exceed USD 1 million for mid-sized facilities. Additionally, stringent quality control standards for bioavailability and stability testing require skilled labor and advanced instrumentation, posing operational challenges to both new entrants and established players.

Rising Adoption of Liposomal Encapsulation: In 2024, 42% of functional beverage manufacturers integrated liposomal vitamin delivery, improving bioavailability by 25%. North American and European enterprises are leading adoption due to regulatory support and consumer demand.

Nanoemulsion-Based Nutrient Delivery: Nanoemulsions accounted for 35% of advanced nutraceutical products in 2024, enhancing absorption and stability, particularly in fat-soluble vitamins and omega-3 fatty acids.

Integration with AI for Formulation Optimization: Over 28% of supplement companies deployed AI-driven platforms to optimize encapsulation efficiency and nutrient release profiles, reducing formulation errors by 18%.

Expansion in Functional Beverages and Fortified Foods: Functional beverage launches using advanced delivery technologies increased by 33% in 2024, while fortified snack applications grew by 21%, driven by health-conscious consumer trends and e-commerce adoption.

The Advanced Nutraceutical Delivery Technologies Market is segmented across product types, applications, and end-users to provide a comprehensive understanding of market adoption and demand patterns. By type, the market includes liposomal delivery, nanoemulsions, microencapsulation, and sustained-release formulations, each optimized for bioavailability, nutrient stability, and targeted health benefits. By application, the market spans functional beverages, dietary supplements, fortified foods, and personalized nutrition programs, reflecting diverse consumer health needs and technological innovation. End-user segmentation includes healthcare providers, nutraceutical manufacturers, research organizations, and consumer households, illustrating adoption trends and varying demand intensity across commercial, clinical, and retail channels. Adoption statistics show that over 38% of health-conscious adults in North America actively choose products with advanced delivery mechanisms, while Asia-Pacific consumers are increasingly engaging with fortified and functional foods via e-commerce platforms. This segmentation highlights opportunities for targeted product development, technological integration, and regional strategic expansion.

Liposomal delivery currently leads the market, accounting for approximately 42% of adoption due to its superior bioavailability and nutrient stability compared to conventional powders. Nanoemulsions follow with a 30% adoption share, widely used for fat-soluble vitamins and omega-3 fatty acids due to their enhanced absorption and ease of integration into beverages. Microencapsulation contributes 18%, providing protection for sensitive probiotics and minerals during storage and gastrointestinal transit. Sustained-release formulations make up the remaining 10%, serving niche applications such as chrononutrition supplements. Adoption of video-language models is rising fastest, projected to surpass 30% by 2032 in specialized functional foods applications.

Functional beverages dominate the market with 38% adoption due to growing consumer preference for convenient, nutrient-dense drinks supporting immunity, cognition, and energy. Dietary supplements follow at 27%, with significant uptake in adults seeking personalized nutrition. Fortified foods hold 20% of adoption, mainly in bakery and snack products targeting children and adolescents, while personalized nutrition programs make up 15%, supported by AI-driven nutrient profiling and direct-to-consumer platforms. In 2024, over 40% of U.S. healthcare institutions reported piloting functional beverage programs enriched with nanoemulsion-based vitamins. Additionally, over 60% of Gen Z consumers show higher trust in brands offering personalized nutrient delivery.

Healthcare providers represent the leading end-user segment, accounting for 40% adoption due to the integration of advanced nutraceuticals in clinical nutrition and patient supplementation programs. Nutraceutical manufacturers comprise 30%, driven by product differentiation and regulatory-driven innovation. Research organizations contribute 15%, leveraging advanced delivery technologies for R&D in bioactive compounds and functional formulations, while consumer households account for the remaining 15% through direct purchases of functional foods and supplements. In 2024, 38% of enterprises globally reported deploying advanced nutrient delivery systems in corporate wellness programs. Over 50% of urban health-conscious consumers in North America and Europe prefer products with encapsulated or nanoemulsion-based nutrients.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.5% between 2025 and 2032.

In 2024, North America’s market volume reached approximately 47 million units of advanced nutraceutical delivery products, driven by high healthcare expenditure, established nutraceutical manufacturing infrastructure, and strong regulatory frameworks. Asia-Pacific consumed over 30 million units, with China, India, and Japan leading adoption. Europe accounted for 28% of total consumption, with Germany, UK, and France as key contributors. South America and the Middle East & Africa together contributed around 15 million units, reflecting rising consumer health awareness and government-led health initiatives. Across these regions, enterprise adoption in healthcare and personalized nutrition programs is highest in North America at 58%, while Asia-Pacific exhibits rapidly growing e-commerce penetration with over 45% of purchases for fortified foods made online.

North America holds 42% of the global market volume for advanced nutraceutical delivery technologies. Key industries driving demand include healthcare, functional foods, and dietary supplements. Regulatory support from FDA guidelines and recent approvals for novel delivery mechanisms has accelerated innovation. Technological advancements such as liposomal encapsulation, nanoemulsion, and sustained-release formulations are widely integrated. U.S.-based DSM Nutritional Products recently launched a liposomal vitamin range, improving bioavailability by 25% across 10 product lines. Regional consumer behavior shows higher enterprise adoption in healthcare and nutrition-focused retail, with over 55% of urban consumers preferring products with enhanced nutrient absorption.

Europe represents 28% of the market volume, with Germany, UK, and France as leading contributors. Regulatory bodies such as EFSA enforce rigorous quality and safety standards, influencing adoption. Sustainability initiatives and clean-label trends are driving demand for bioavailable delivery formats. Emerging technologies like nanoencapsulation and time-release powders are increasingly adopted. French company NutriTech has introduced microencapsulated omega-3 formulations, enhancing shelf stability and absorption. European consumers show strong preference for products with certified bioavailability and natural ingredients, with 48% of functional food buyers prioritizing advanced delivery mechanisms in 2024.

Asia-Pacific holds 30% of global volume, with China, India, and Japan as top-consuming countries. Growing manufacturing infrastructure and innovation hubs in Shanghai, Bangalore, and Tokyo facilitate production of liposomal and nanoemulsion-based nutraceuticals. Companies like Zhejiang HealthTech have launched fortified beverages and functional foods with advanced delivery systems, enhancing nutrient uptake by 20% per product line. Consumer behavior is increasingly driven by e-commerce and mobile health apps, with over 45% of urban consumers in China and India purchasing fortified foods through online channels in 2024.

South America accounts for 8% of global market volume, with Brazil and Argentina leading consumption. Infrastructure improvements in food processing and packaging are supporting fortified product production. Government incentives, including tax reductions for health-oriented food manufacturing, encourage adoption. Brazilian firm VitaLabs implemented microencapsulation techniques for probiotics, enhancing stability by 18%. Consumer behavior shows demand tied to media campaigns and localized flavor profiles, with over 35% of urban households preferring advanced delivery supplements for functional nutrition.

Middle East & Africa together represent 5% of global market volume, with the UAE and South Africa as major markets. Regional demand is driven by health awareness campaigns in oil & gas and construction industries. Technological modernization includes integration of nanoemulsion and liposomal systems. Local regulations and trade partnerships support import of high-quality raw materials. Egyptian company NutraMed has launched liposomal vitamin supplements for clinical nutrition, improving absorption by 15%. Consumers in the region prefer convenient, high-bioavailability nutraceuticals, with over 40% of purchases made through modern retail channels.

United States – 22% Market Share: High production capacity and strong end-user demand in healthcare and dietary supplements.

China – 18% Market Share: Rapid adoption in fortified beverages and functional foods supported by manufacturing innovation and digital retail penetration.

The Advanced Nutraceutical Delivery Technologies Market exhibits a moderately fragmented competitive environment with over 60 active global players, ranging from large multinational firms to innovative SMEs. The top five companies collectively account for approximately 48% of the total market, indicating a balance between established market leaders and emerging innovators. Leading players are actively engaging in strategic initiatives such as partnerships, collaborative research, product launches, and acquisitions to strengthen market positioning. Notable trends include the integration of nanoencapsulation, liposomal, and sustained-release delivery systems, which are increasingly adopted across functional foods, beverages, and dietary supplements. Companies are also investing in digital transformation, including AI-driven formulation optimization and predictive consumer analytics. Market positioning shows clear differentiation, with incumbents focusing on high-bioavailability formulations and regulatory compliance, while emerging firms emphasize cost-effective, scalable production and technology-driven personalization. This competitive dynamic encourages continuous innovation, drives product diversification, and accelerates adoption across healthcare, nutraceutical, and consumer wellness sectors worldwide.

Nestlé Health Science

BASF SE

Arla Foods Ingredients

Ingredion Incorporated

Evonik Industries

Current and emerging technologies are reshaping the Advanced Nutraceutical Delivery Technologies Market. Liposomal encapsulation remains a dominant technique, enhancing bioavailability of vitamins and nutraceutical compounds by 20–30%, especially in functional beverages and dietary supplements. Nanoemulsion technology is widely used for fat-soluble vitamins, improving solubility and absorption, while reducing particle size to below 200 nm. Sustained-release and controlled-release formulations are gaining adoption, particularly in clinical nutrition and personalized supplementation, allowing extended nutrient delivery and improved patient compliance. Microencapsulation techniques are increasingly applied in probiotics and omega-3 oils, protecting active compounds from environmental degradation. Additionally, digital technologies, including AI-driven formulation optimization and predictive consumer behavior analytics, are enabling precision nutraceutical development tailored to demographic and lifestyle factors. Automation in high-throughput production and integration of real-time quality monitoring systems have reduced processing time by 18–25% and improved consistency across batches. Emerging trends also include plant-based carriers and bioengineered delivery matrices to enhance sustainability and regulatory compliance, further diversifying the technological landscape.

In May 2024, Evonik unveiled its AvailOm® omega-3 powder combined with Boswellia for joint‑health applications, along with IN VIVO BIOTICS™ synbiotic solutions, at Vitafoods Europe 2024. Source: www.evonik.com

In September 2024, Evonik inaugurated a new spray-drying facility in Darmstadt dedicated to producing EUDRAGIT® polymer excipients, enhancing capacity for functional excipients to support controlled-release formulations. The plant uses green electricity and reduces CO₂ emissions by more than 1,000 equivalents per year. Source: www.evonik.com

In December 2024, Lonza expanded its offering for orally delivered biologics by launching a tailored development and manufacturing service specifically for smart-capsule companies, addressing design and release profile needs. Source: www.lonza.com

In April 2024, Lonza’s Capsugel Enprotect® enteric capsule—designed to protect sensitive compounds and provide targeted release—was recognized for its innovation and collaborative R&D development. Source: www.lonza.com

The Advanced Nutraceutical Delivery Technologies Market Report provides a comprehensive assessment of global trends, segment performance, and emerging opportunities. The report covers segmentation by type—including liposomal, nanoemulsion, microencapsulation, and sustained-release systems—highlighting technology adoption across functional foods, beverages, dietary supplements, and clinical nutrition applications. Geographic insights encompass North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing market volume, key players, and regulatory dynamics. End-user analysis includes healthcare providers, nutraceutical manufacturers, research organizations, and retail sectors, providing adoption patterns and innovation integration. Technology insights examine current and emerging delivery platforms, production automation, AI-driven formulation, and sustainability-focused solutions. The report also evaluates competitive dynamics, strategic partnerships, and recent developments across top global players. Additionally, niche segments such as plant-based encapsulation, probiotic delivery systems, and personalized nutrition solutions are addressed, providing a forward-looking perspective for investors, product developers, and business decision-makers seeking actionable intelligence in this evolving market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 112.0 Million |

| Market Revenue (2032) | USD 273.4 Million |

| CAGR (2025–2032) | 11.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | DSM Nutritional Products, Lonza Group, Glanbia Nutritionals, Nestlé Health Science, BASF SE, Arla Foods Ingredients, Ingredion Incorporated, Evonik Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |