Reports

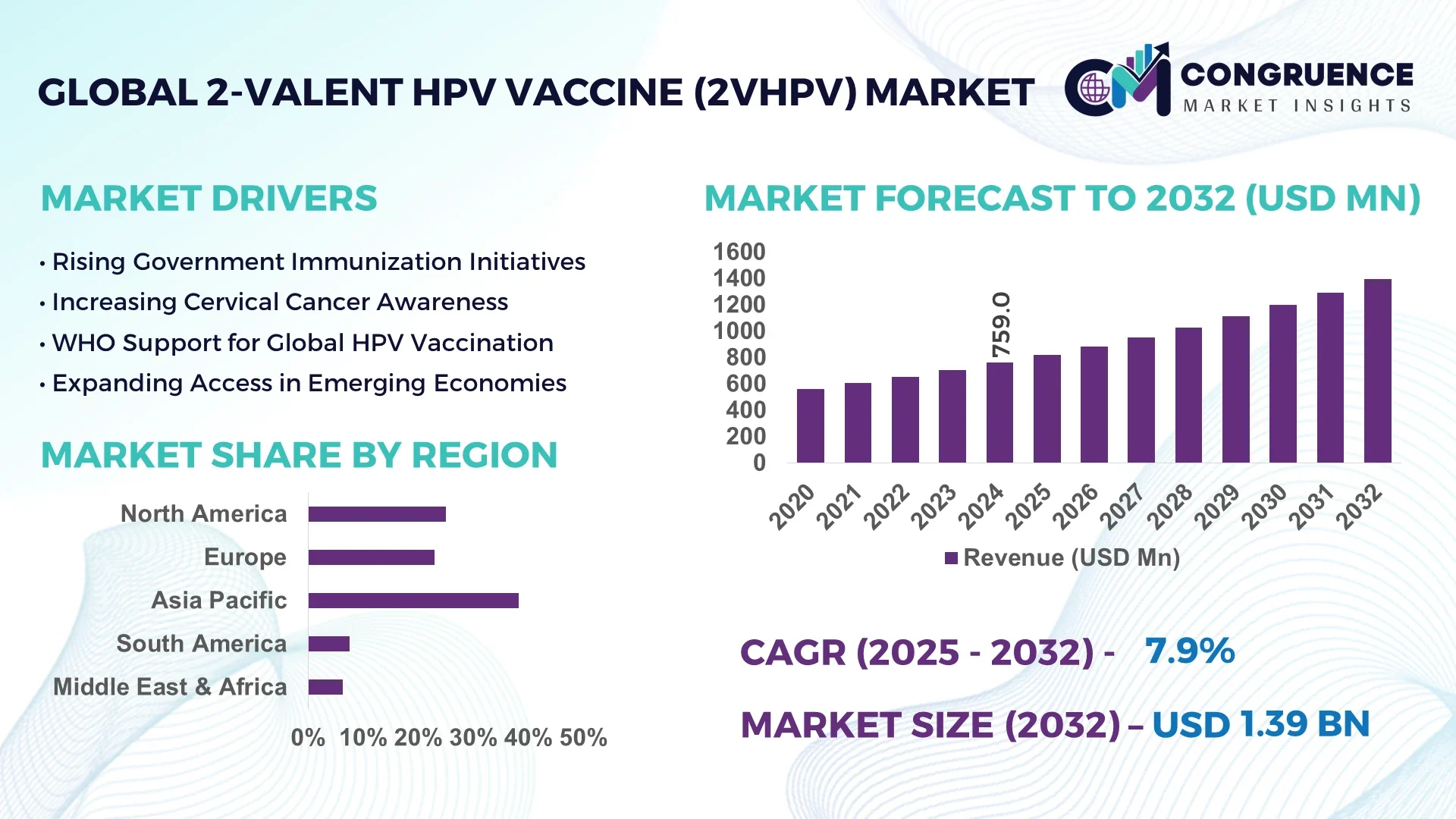

The Global 2‑valent HPV Vaccine (2vHPV) Market was valued at USD 759.0 Million in 2024 and is anticipated to reach a value of USD 1,394.5 Million by 2032 expanding at a CAGR of 7.9% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

In 2024, China dominates the 2vHPV market, accounting for nearly 35% of global sales, driven by large-scale inclusion of the vaccine in school programs for girls aged 9–14 and rising public awareness of cervical cancer prevention. National immunization policies have scaled up government-subsidized 2vHPV rollout across urban and rural provinces, leading to a significant surge in vaccine procurements and public–private partnerships focused on equitable supply distribution.

The 2vHPV vaccine market is also experiencing rapid innovation through targeted expansions in dosage formats and specialized cold-chain logistics tailored for adolescent immunization programs. Additionally, several emerging biotech firms are entering the supply chain, promoting domestic manufacturing to reduce costs and improve access in middle-income countries.

The integration of AI into the 2vHPV vaccine market is revolutionizing awareness campaigns, patient engagement, distribution networks, and clinical trial planning. AI-powered chatbots are being used to educate parents and adolescents about 2vHPV in real time, addressing vaccine hesitancy, clarifying side-effect concerns, and supporting appointment scheduling through interactive dialogue. This has led to improved vaccine literacy scores among users and increased healthcare consultations.

In logistics and supply chain, AI models now predict regional vaccine demand based on demographic trends, urbanization patterns, and prior uptake, enabling manufacturers and governments to optimize inventory distribution, minimize wastage, and ensure consistent availability in both urban centers and remote areas. These AI-driven forecasting systems also power just-in-time manufacturing responses to sudden uptake spikes, reducing storage costs and maintaining continuous supply.

Within R&D, machine learning algorithms analyze immunogenicity data from clinical trials across varied age cohorts, identifying demographic groups with exceptional immune responses to the bivalent formulation. This supports faster regulatory approvals for tailored age-specific dosing strategies and informs future iterations of the vaccine. AI has also enabled rapid meta-analysis across vaccine studies, extracting safety and efficacy signals and facilitating accelerated protocol adjustments.

AI-powered health surveillance platforms monitor social media sentiment, news trends, and misinformation spikes related specifically to 2vHPV, helping public health agencies deploy targeted outreach campaigns. These systems identify local hesitancy hotspots in near real time, prompting localized awareness drives and health professional training.

Operational efficiencies also include AI-assisted cold-chain monitoring: IoT-connected sensors at distribution hubs feed live temperature and location data into predictive maintenance systems, reducing spoilage risk and ensuring the potency of 2vHPV vaccines, especially in regions with unreliable infrastructure.

“In 2025, An AI chatbot trial in rural China among parents of girls aged 12–15 led to a 3‑fold increase in scheduled or received 2vHPV vaccination and an 8.8‑times higher likelihood of initiating vaccination compared with standard care.”

Large-scale national immunization initiatives targeting girls aged 9–14 have driven the integration of 2vHPV into public vaccination schedules. Over 50 countries now provide government funding or subsidies, which in turn boost procurement volumes and encourage vaccine uptake. Vaccine awareness campaigns funded by national health ministries and NGOs have also improved parental consent rates and community acceptance, reinforcing market expansion across multiple geographies.

Despite rising demand, limited refrigeration capacity in rural and low-income areas restricts vaccine distribution. Spoilage during transport and storage can lead to loss of up to 20% of doses in underdeveloped regions, and vaccine providers often cite unreliable electricity and lack of validated temperature monitoring systems as barriers to consistent supply.

Innovations in transportable refrigeration units, solar-powered vaccine carriers, and drone delivery platforms create chances to reach underserved adolescent populations in remote areas—potentially increasing coverage by 15–20%. Public–private partnerships aimed at deploying mobile clinics equipped with on-site 2vHPV vaccine storage are currently being piloted across Southeast Asia and sub-Saharan Africa.

While 2vHPV provides strong protection against HPV types 16 and 18, quadrivalent and nonavalent vaccines offer broader strain coverage, making them more attractive in countries with high prevalence of additional HPV strains. Varying national guidelines and differing economics for older age cohorts create pressure on producers of 2vHPV to optimize cost-effectiveness and clarify positioning in adolescent-only immunization programs.

Rise of Community-Based Education Campaigns: Health NGOs, often in collaboration with government health departments, are deploying mobile health education vans equipped with AR/VR demonstrations and AI-controlled messaging tools. These efforts have led to a 25% increase in informed consent rates among parents in peri-urban settings, driven by realistic digital simulations of vaccine benefits and potential side effects.

Integration with Adolescent Health Platforms: 2vHPV vaccination is now being offered through integrated school health programs that include digital record systems tracking adolescent health metrics. These platforms enable batch scheduling of school-based campaigns, follow-up reminders via SMS, and monitoring of side effects in real time, supporting full-course compliance within weeks of initial dose administration.

Pricing Innovations via Tiered Access Programs: Generic 2vHPV formulations from emerging manufacturers are being offered in low- and middle-income countries through tiered-pricing models aligned with per-capita income levels. These programs have reduced per-dose cost by approximately 40–60% compared to branded equivalents, enabling broader access across budget-constrained national immunization programs.

Digital Twin Modeling for Vaccination Strategy: Some public health systems are now using AI-based digital twin models of adolescent populations—integrating demographics, school enrollment rates, prior vaccine uptake, and community sentiment—to test and refine vaccination drive strategies virtually before deploying them. This trend has improved efficiency of campaign planning, leading to reduced no-show rates and optimized workforce deployment in field clinics.

The 2-valent HPV Vaccine (2vHPV) market is segmented by type, application, and end-user, each offering unique growth dynamics and market potential. The type segmentation primarily focuses on dosage formats, catering to varying immunization program needs across regions. Applications are largely driven by prevention of specific HPV-associated diseases, with cervical cancer prevention continuing to dominate the landscape. End-user segmentation provides insights into distribution channels and service models, where the public healthcare sector leads in volume deployment, while private healthcare networks demonstrate rapid growth. Each segment is shaped by local policy frameworks, healthcare infrastructure readiness, public awareness levels, and socio-economic trends that collectively influence vaccine uptake patterns.

In the 2vHPV market, key type segments include pre-filled syringes and single-dose vials. Pre-filled syringes hold the leading market share, accounting for nearly 65% of global sales in 2024. Their ease of use, reduced risk of dosing errors, and compatibility with mass immunization settings such as schools and public health campaigns make them the preferred format, particularly in high-volume programs in China, Europe, and Latin America.

Single-dose vials represent the fastest growing segment, driven by expanding demand in lower-income countries and remote regions where healthcare providers prefer more flexible and cost-effective packaging for small-scale or mobile clinics. The segment is growing notably in parts of sub-Saharan Africa and Southeast Asia, where innovative cold-chain logistics and targeted vaccination drives are being deployed. Additionally, vials offer the benefit of minimizing vaccine wastage, especially in variable-demand environments. This dual dynamic positions pre-filled syringes for sustained leadership while allowing single-dose vials to capture emerging growth opportunities.

The market is segmented by applications such as cervical cancer prevention, anal cancer prevention, oral cancer prevention, and other HPV-related disease prevention. Cervical cancer prevention is the dominant application, constituting over 75% of market demand in 2024. Strong global emphasis on reducing cervical cancer incidence through adolescent female immunization has ensured that this segment remains the core focus of national vaccination programs.

Oral cancer prevention is emerging as the fastest growing segment, driven by increasing evidence linking HPV to a rising number of oropharyngeal cancers, especially in Western countries. Public health agencies are beginning to broaden vaccine messaging and indications to include protection against non-cervical HPV-related cancers, which is fostering interest in vaccinating wider demographics, including males. As clinical guidelines evolve and awareness grows, this segment is expected to see rapid adoption over the next several years, contributing meaningfully to overall market expansion.

The market end-user segments include public health programs, private healthcare providers, and NGO-driven and other community-based initiatives. Public health programs dominate the market, accounting for nearly 70% of vaccine deployments in 2024. Government-funded immunization initiatives targeting school-aged girls and supported by organizations such as Gavi and UNICEF drive this segment’s leadership. These programs benefit from large-scale procurement capabilities and subsidized vaccine delivery models that achieve broad population coverage.

Private healthcare providers represent the fastest growing end-user segment, particularly in urban centers of high-income and emerging markets. Increasing demand from adult women seeking catch-up vaccination, as well as rising interest among male populations, is driving growth in private clinics, hospitals, and pharmacy-based immunization services. Additionally, growing consumer willingness to pay for elective vaccination outside of public programs supports sustained private sector expansion. NGO-driven initiatives also play a critical role in reaching marginalized and remote populations, though their overall market share remains smaller compared to public and private healthcare channels.

Asia-Pacific accounted for the largest market share at 38.2% in 2024; however, Latin America is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The Asia-Pacific region leads due to substantial demand from countries such as China, Japan, and India, supported by large-scale national immunization initiatives and increasing public awareness. In contrast, Latin America’s fast growth is fueled by newly launched public vaccination programs, increasing affordability through tiered-pricing agreements, and a high burden of HPV-related cancers that is driving strong public health advocacy and funding.

Rising Adult Vaccination Demand in Private Healthcare Sector

In North America, the 2vHPV market is experiencing notable growth through private healthcare channels. The United States leads with approximately 5.6 million doses administered in 2024 alone. Catch-up vaccination campaigns targeting adult women and the inclusion of males in recommended vaccination guidelines have expanded the addressable market. In Canada, provincial programs offering free 2vHPV vaccination to girls and subsidized options for boys are driving high compliance rates in adolescents, while pharmacy chains are seeing increased demand from adults seeking elective vaccination.

Expanding Gender-Neutral Vaccination Policies Across Europe

Europe is witnessing rapid policy evolution toward gender-neutral vaccination. As of 2024, 21 EU countries have adopted programs offering 2vHPV vaccines to both girls and boys. Germany, France, and Italy collectively accounted for over 3.8 million doses administered in 2024, representing the majority of the region’s volume. These shifts aim to reduce HPV transmission rates across the population and broaden protection beyond cervical cancer prevention. School-based vaccination remains the primary delivery channel, while catch-up initiatives targeting young adults are gaining momentum across Western Europe.

China Driving Regional Growth with Nationwide Adolescent Programs

Asia-Pacific leads the global market, largely due to aggressive rollout in China, which alone contributed over 35 million doses in 2024 through its school-based vaccination campaigns. Public demand is strong, with adolescent girls’ coverage exceeding 85% in major urban centers. In India, the government launched its first national HPV immunization program targeting 25 million adolescent girls annually, boosting regional growth prospects. Australia and Japan also maintain mature, high-coverage programs, positioning Asia-Pacific as both the largest and one of the most dynamic markets globally.

Public Funding Expands Access Across Low-Income Populations

In South America, Brazil and Argentina are spearheading market expansion. Brazil administered over 8 million 2vHPV doses in 2024 through its free national immunization program, which targets girls aged 9–14 and offers catch-up doses for older age groups. Argentina recently expanded vaccine eligibility to include males aged 11–26, driving significant uptake. Tiered pricing agreements and Gavi-supported funding have made vaccines more accessible, helping lower-income communities achieve coverage rates previously unattainable, and prompting neighboring countries to replicate similar public health models.

Strengthening Cold-Chain Logistics to Support Wider Access

In the Middle East & Africa, limited infrastructure historically hampered vaccine distribution, but recent investments in cold-chain capabilities are transforming market dynamics. South Africa leads with over 1.5 million doses delivered through school-based and clinic-led programs. In the Middle East, the UAE and Saudi Arabia are introducing broad public campaigns aligned with national cancer reduction strategies. Across sub-Saharan Africa, NGO partnerships are enabling innovative delivery models such as solar-powered cold-chain storage and mobile clinics, which helped distribute over 3 million doses in 2024, particularly in underserved rural regions.

China - Market Value (2024): USD 290.4 Million, driven by large-scale government-backed school immunization programs, with over 35 million doses administered and expanding coverage to both urban and rural regions.

Brazil - Market Value (2024): USD 112.7 Million, sustained by a comprehensive free national immunization program, covering adolescent girls and expanding to include boys, achieving over 8 million doses administered through public health channels.

The 2‑valent HPV Vaccine (2vHPV) market is characterized by competition among global pharmaceutical companies and emerging regional biotech firms. Market leaders such as GlaxoSmithKline and Walvax Biotech dominate through established vaccine campaigns and broad regulatory approvals. These players benefit from strong supply chains, robust cold-chain distribution, and long-standing relationships with global immunization initiatives. Meanwhile, emerging firms from China and India are rapidly expanding their footprint by securing national approvals and pursuing WHO prequalification for export markets. Though they currently hold smaller volume shares, these firms are gaining momentum by offering competitive pricing and securing government tenders. This rising competition is pushing innovation, improving access, and diversifying supply — ultimately benefiting public health outcomes in both established and underserved markets.

GlaxoSmithKline

Walvax Biotech

Xiamen Innovax Biotech

Serum Institute of India

Bharat Biotech

Zhejiang Lingyue Biopharma

Vaccine technology in the 2vHPV space is advancing in areas like antigen presentation, cold-chain optimization, and dosage efficiency. Traditional virus-like-particle (VLP) formulations remain dominant, providing strong immunogenicity against HPV types 16 and 18. Novel adjuvants and nanoparticle delivery systems are being embedded to enhance immune response while reducing dosage amounts—an innovation that supports single- or double-dose schedules. Recent developments include thermostable coatings that allow vaccines to remain effective at higher temperatures for limited periods, thus easing cold-chain constraints in remote regions. Integration of IoT temperature sensors with blockchain tracking enhances transparency and safety in vaccine logistics. Additionally, new automated fill–finish lines allow manufacturers to switch rapidly between syringe and vial presentations, improving production flexibility and responsiveness to regional demands. Biotechnology-focused firms are also exploring mRNA-based HPV vaccine candidates, which, although in early development, aim to streamline manufacturing and reduce time-to-market for updated formulations targeting emerging HPV strain variants.

In May 2025, China’s National Medical Products Administration approved Cecolin 9—the country’s first domestically developed nine-valent HPV vaccine—following earlier licensure of a domestically produced two-valent version now shipped to at least 21 countries. Trials enrolled more than 11,000 participants.

In early 2024, Canada’s National Advisory Committee on Immunization endorsed a one-dose HPV schedule for individuals aged 9–20, citing evidence that single-dose immunization provides long-lasting protection comparable to two- or three-dose regimens.

In late 2023, Serum Institute of India disclosed the successful development of “Cervavax,” a quadrivalent HPV vaccine targeting types 6, 11, 16, and 18, with immunogenicity comparable to international brands; it is now under evaluation for commercial release.

In mid-2024, China’s Walvax Biotech launched an automated mixed-format fill–finish facility designed to handle both pre-filled syringes and single-dose vials, boosting domestic output capacity by over 25%.

The 2vHPV Market Report encompasses global and regional analyses, focusing on vaccine formats, distribution channels, policy frameworks, and competitive positioning. It evaluates public and private immunization strategies, offering insights into volume and value shipped through school-based programs, pharmacy networks, and NGO partnerships. Technology trends such as thermostable formulations, adjuvant systems, and automated manufacturing are featured for their potential to reduce costs and improve scalability. Market dynamics include regulatory developments, pricing strategies, and cold-chain innovations. Strategic profiles of leading and emerging manufacturers highlight capacity expansions, WHO prequalification status, and global tender wins. The report also assesses demographic factors, coverage rates, and age-cohort performance, with targeted sections on adult catch-up programs and male vaccination policies. Geographically, it provides detailed breakdowns for North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, offering country-specific data and growth forecasts. Finally, the study outlines future opportunities and risks tied to technological disruption, policy evolution, and competitive pressures—essentia for stakeholders to plan investment, production capacity, and public health strategies.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global 2-valent HPV Vaccine (2vHPV) Market |

| Market Revenue (2024) | USD 759.0 Million |

| Market Revenue (2032) | USD 1,394.5 Million |

| CAGR (2025–2032) | 7.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | GlaxoSmithKline, Walvax Biotech, Xiamen Innovax Biotech, Serum Institute of India, Bharat Biotech, Zhejiang Lingyue Biopharma |

| Customization & Pricing | Available on Request (10% Customization is Free) |