Reports

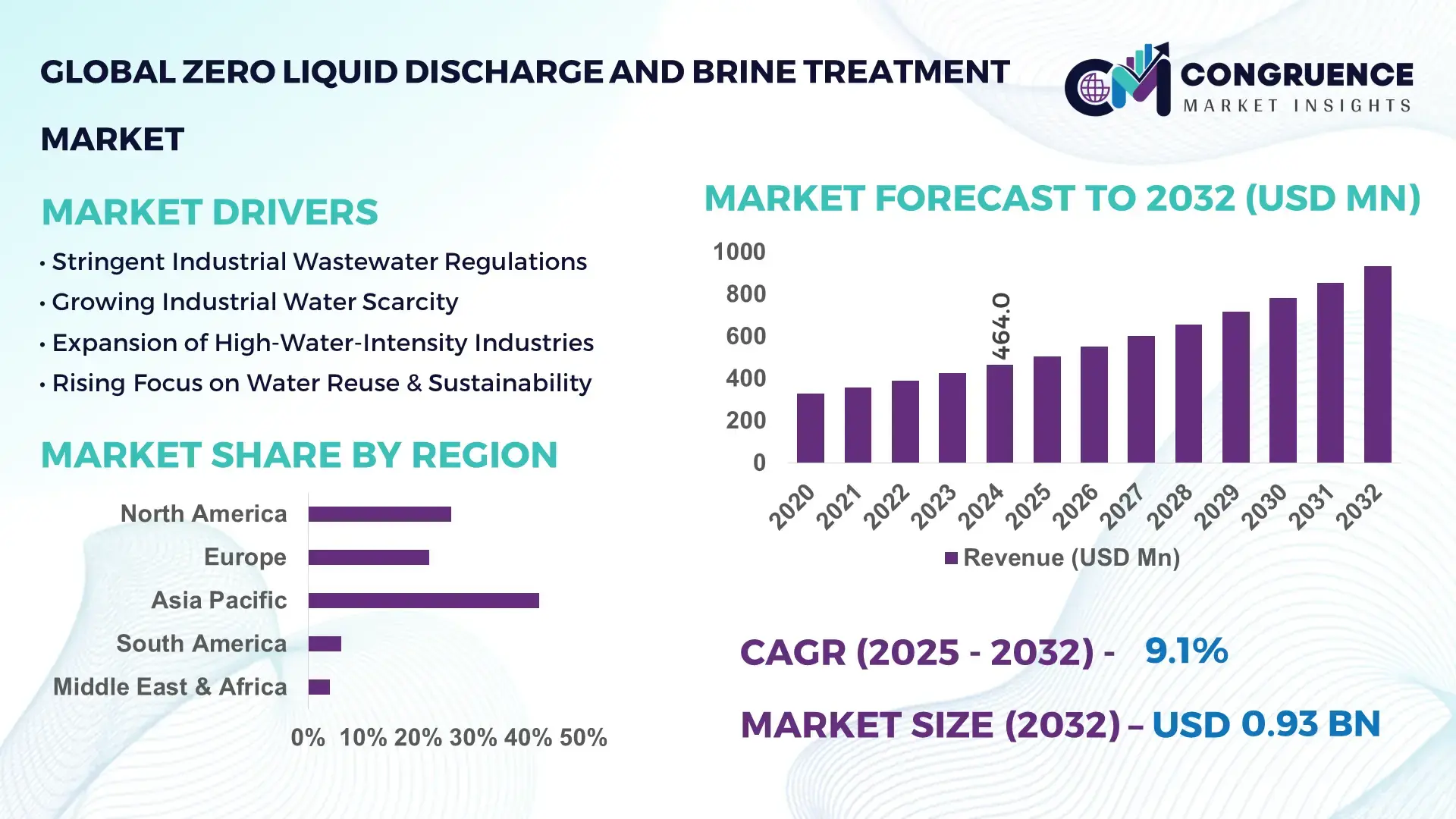

The Global Zero Liquid Discharge and Brine Treatment Market was valued at USD 464.0 Million in 2024 and is anticipated to reach a value of USD 931.4 Million by 2032, expanding at a CAGR of 9.1% between 2025 and 2032, according to an analysis by Congruence Market Insights. The market growth is primarily driven by tightening industrial wastewater discharge regulations and increasing investments in advanced water recovery and reuse infrastructure.

China dominates the Zero Liquid Discharge and Brine Treatment Market through large-scale industrial deployment and infrastructure expansion. The country operates more than 3,500 industrial ZLD facilities across power generation, coal-to-chemicals, textiles, electronics, and refining sectors. In 2024, China added over 1.2 million cubic meters per day of new high-salinity wastewater treatment capacity, supported by public and state-backed investments exceeding USD 6.5 billion. Industrial water reuse rates in regulated zones exceed 90%, while localized production of membrane systems, evaporators, and mechanical vapor recompression units has reduced dependence on imported equipment and improved deployment efficiency.

Market Size & Growth: Valued at USD 464.0 Million in 2024 and projected to reach USD 931.4 Million by 2032, growing at a CAGR of 9.1% due to stricter wastewater discharge norms and water reuse mandates.

Top Growth Drivers: Industrial wastewater reuse adoption at 68%, regulatory enforcement intensity up 42%, and water recovery efficiency improvements averaging 35%.

Short-Term Forecast: By 2028, average operational water recovery rates are expected to improve by 22% through hybrid membrane–thermal systems.

Emerging Technologies: Forward osmosis-based ZLD, membrane distillation crystallizers, and AI-enabled brine concentration optimization.

Regional Leaders: Asia Pacific projected at USD 382.0 Million by 2032, North America at USD 247.0 Million, and Europe at USD 188.4 Million, each driven by distinct regulatory and industrial adoption trends.

Consumer/End-User Trends: Power utilities and chemicals account for over 54% of installations, with mining and pharmaceuticals showing accelerating adoption.

Pilot or Case Example: A 2023 refinery ZLD pilot in India achieved a 28% reduction in freshwater intake and 31% lower brine disposal volumes.

Competitive Landscape: Veolia holds approximately 18% share, followed by SUEZ, Aquatech, Thermax, and GEA Group.

Regulatory & ESG Impact: Liquid discharge bans and ESG-linked water neutrality targets are accelerating retrofits and new installations.

Investment & Funding Patterns: Over USD 9.4 billion invested globally since 2021, with strong growth in EPC-linked performance contracts.

Innovation & Future Outlook: Digital twins, low-temperature evaporators, and resource recovery-driven ZLD designs are shaping next-generation systems.

The market serves power generation (32%), chemicals and petrochemicals (22%), mining and metals (18%), and pharmaceuticals and food processing (14%). Recent innovations focus on low-energy crystallizers and fouling-resistant membranes, while regulatory mandates, freshwater scarcity, and industrial expansion continue to influence regional demand patterns and long-term outlook.

The Zero Liquid Discharge and Brine Treatment Market has become strategically critical for industrial sustainability, regulatory compliance, and operational risk management. Rising freshwater procurement costs—up more than 40% in water-stressed regions—are positioning ZLD systems as core infrastructure. Advanced membrane crystallization delivers up to 27% efficiency improvement compared to conventional multi-effect evaporators, while hybrid systems reduce energy consumption by 18–22%.

Asia Pacific dominates in treatment volume, while North America leads in adoption, with 61% of large industrial enterprises deploying partial or full ZLD systems. By 2027, AI-based optimization is expected to cut unplanned downtime by 24% through predictive fouling and scaling control. Firms are committing to ESG water circularity goals, targeting 95% wastewater reuse and 30% freshwater withdrawal reduction by 2030. In 2024, China achieved a 21% reduction in industrial liquid waste discharge through integrated ZLD mandates. Overall, the Zero Liquid Discharge and Brine Treatment Market is emerging as a pillar of industrial resilience, regulatory compliance, and sustainable growth.

The Zero Liquid Discharge and Brine Treatment Market is shaped by regulatory enforcement, industrial water scarcity, and advances in treatment technologies. Demand is strongest in sectors producing high-salinity effluents where conventional wastewater systems are ineffective. Integrated evaporation–crystallization–membrane solutions are becoming standard, while modular designs and digital monitoring are reducing commissioning timelines. Regional policy differences continue to influence adoption speed and system configurations.

Over 70% of newly permitted industrial projects now require closed-loop water systems. Penalties for non-compliance have increased by more than 45% since 2020, making ZLD systems a strategic necessity. Industrial clusters enforcing zero-discharge mandates report wastewater reuse rates above 92%, accelerating standardized adoption.

ZLD installations typically cost USD 1.5–3.0 million per MLD of capacity, with evaporation stages accounting for nearly 38% of lifecycle costs. Smaller operators face financing barriers, long installation timelines, and skilled labor shortages, restricting broader penetration.

Recovery of salts, lithium, and industrial chemicals can offset operational costs by up to 26%. Shared ZLD infrastructure in industrial parks reduces unit treatment costs by 19%, while circular water reuse models expand adoption beyond heavy industries.

Scaling and fouling account for nearly 17% of annual downtime in poorly optimized systems. Variable influent chemistry and limited operator expertise increase operational risks, driving demand for automation and real-time analytics.

Expansion of Hybrid Thermal–Membrane Systems: Hybrid systems represent over 48% of new installations, increasing water recovery above 96% and reducing energy use by 21%.

Digitalization and AI-Based Process Control: AI platforms are deployed in 37% of new plants, reducing chemical usage by 25% and extending membrane life by 19%.

Growth of Resource Recovery-Oriented ZLD: Nearly 29% of new projects integrate mineral recovery, delivering up to 18% operational cost offset.

Rise in Modular and Prefabricated Construction: Modular ZLD units are used in 55% of new projects, cutting installation time by 34% and labor needs by 28%, particularly in Europe and North America.

The Zero Liquid Discharge and Brine Treatment Market is segmented based on type, application, and end-user, reflecting varied industrial wastewater characteristics, regulatory exposure, and operational scale. By type, the market spans thermal-based systems, membrane-based systems, and hybrid solutions, each addressing different salinity loads and recovery efficiency needs. Application-wise, demand is concentrated in power generation, chemicals, mining, oil & gas, and pharmaceuticals, where high dissolved solids and strict discharge limits prevail. From an end-user perspective, large industrial facilities dominate installations due to higher effluent volumes and regulatory scrutiny, while adoption among industrial parks and municipal utilities is steadily increasing. Segmentation trends indicate a shift toward integrated and modular configurations, driven by operational flexibility, energy optimization, and water reuse mandates. Decision-makers increasingly prioritize solutions tailored to influent chemistry, footprint constraints, and long-term compliance, making segmentation analysis critical for technology selection and investment planning.

Thermal-based ZLD systems, including evaporators and crystallizers, represent the leading product type, accounting for approximately 46% of installations due to their ability to handle extremely high total dissolved solids and variable effluent composition. Membrane-based systems, such as reverse osmosis and nanofiltration, account for nearly 31% of adoption, offering lower energy consumption and suitability for moderate salinity streams. However, hybrid ZLD systems, combining membranes with thermal processes, are the fastest-growing type, expanding at an estimated 11.8% CAGR, driven by their capability to achieve water recovery rates above 95% while reducing overall energy intensity by up to 22%. Other niche configurations, including forward osmosis and membrane distillation, collectively contribute about 23%, primarily serving specialized applications with space or energy constraints.

Power generation remains the leading application area, accounting for roughly 34% of total ZLD deployments, as thermal power plants generate large volumes of high-salinity blowdown water subject to zero-discharge mandates. The chemicals and petrochemicals segment follows at around 24%, supported by continuous-process operations and strict environmental compliance requirements. Mining and metals applications are the fastest-growing, expanding at an estimated 12.4% CAGR, driven by rising mineral processing activity and increasing restrictions on tailings water disposal. Other applications, including pharmaceuticals, food processing, and oil & gas, together contribute approximately 42%, reflecting diverse wastewater profiles and localized regulatory pressure. In 2024, over 41% of industrial facilities globally reported piloting advanced ZLD systems for process water reuse, while 39% of regulated power plants indicated plans to upgrade existing wastewater infrastructure within three years.

Large-scale industrial enterprises dominate the Zero Liquid Discharge and Brine Treatment Market, representing about 58% of total installations due to higher effluent volumes, compliance obligations, and access to capital-intensive infrastructure. Medium-sized industrial operators account for approximately 27%, increasingly adopting modular ZLD systems to meet tightening discharge standards. Industrial parks and special economic zones are the fastest-growing end-user group, expanding at an estimated 13.2% CAGR, as shared infrastructure models reduce per-unit treatment costs and accelerate adoption. Other end-users, including municipal utilities and specialized processing facilities, collectively contribute around 15% of demand. In 2024, more than 36% of industrial zones worldwide reported implementing centralized ZLD systems to support multiple tenants, while 44% of water-intensive manufacturers indicated increased reliance on reclaimed water for core operations.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 10.3% between 2025 and 2032.

Asia-Pacific’s leadership is supported by large-scale industrial water reuse mandates, high concentration of power plants, chemical clusters, and mining operations. North America’s growth momentum is driven by regulatory tightening, rising ESG-linked capital spending, and digital modernization of industrial wastewater systems. Europe follows closely with strong compliance-driven adoption, while the Middle East & Africa and South America show steady uptake tied to energy, mining, and desalination-linked brine management. Regional differences in industrial structure, water scarcity levels, and policy enforcement continue to shape deployment intensity, system design, and investment priorities across the global Zero Liquid Discharge and Brine Treatment Market.

North America represents approximately 26% of the global Zero Liquid Discharge and Brine Treatment Market, with demand concentrated in the United States and Canada. Power generation, oil & gas, chemicals, and pharmaceuticals collectively account for over 68% of regional installations. Regulatory enforcement under industrial wastewater discharge permits and water reuse mandates has increased retrofit activity, particularly in thermal power plants and refineries. More than 57% of large industrial facilities in the region have implemented advanced automation and digital monitoring within ZLD systems. Technological trends include AI-enabled scaling prediction, low-temperature evaporators, and modular crystallizers. Local engineering firms are expanding EPC-led turnkey ZLD offerings, while enterprise buyers show higher adoption in regulated sectors such as healthcare manufacturing and specialty chemicals, prioritizing reliability and compliance assurance.

Europe accounts for roughly 22% of global market activity, led by Germany, the United Kingdom, France, Italy, and the Netherlands. Industrial chemicals, food processing, pharmaceuticals, and metals dominate application demand. Environmental compliance frameworks and circular economy initiatives have driven wastewater reuse targets above 85% in multiple industrial zones. More than 49% of new ZLD deployments integrate energy-efficient evaporation or membrane distillation technologies. Regional players focus on low-carbon system designs and heat recovery integration. Consumer behavior reflects strong regulatory influence, with enterprises prioritizing explainable, auditable water treatment performance and lifecycle efficiency to meet sustainability reporting and compliance benchmarks.

Asia-Pacific is the largest and highest-volume regional market, accounting for approximately 42% of global installations. China, India, and Japan lead consumption due to extensive coal-based power generation, chemical manufacturing, textiles, and electronics production. Industrial water reuse rates exceed 90% in regulated industrial parks across major manufacturing hubs. Infrastructure expansion and localized equipment manufacturing have reduced system deployment timelines by nearly 30%. Regional innovation focuses on membrane–thermal hybridization, high-fouling tolerance designs, and centralized ZLD facilities serving multiple tenants. Industrial adoption behavior reflects scale-driven implementation, with over 60% of new projects using shared or modular systems to optimize capital efficiency.

South America contributes approximately 6% of global market demand, led by Brazil, Argentina, and Chile. Mining, metals processing, and energy sectors represent more than 70% of regional ZLD installations, driven by water scarcity and discharge controls in mineral-rich zones. Infrastructure upgrades in mining corridors have increased industrial water recycling rates above 75%. Government incentives supporting sustainable mining and industrial water reuse have accelerated pilot deployments. Regional operators emphasize cost-efficient and rugged system designs, while adoption behavior remains project-specific, closely tied to mining output cycles and energy sector investments.

The Middle East & Africa region accounts for nearly 4% of global demand, with strong uptake in the UAE, Saudi Arabia, South Africa, and Oman. Oil & gas, desalination-linked industries, and power generation dominate application demand. Industrial water reuse requirements exceed 95% in several Gulf industrial zones. Modernization trends include high-capacity crystallizers, brine concentrators, and digital monitoring platforms to manage extreme salinity. Local regulations promoting water security and industrial sustainability continue to drive investment. Consumer behavior reflects necessity-driven adoption, with enterprises prioritizing maximum recovery and operational resilience.

China – 29% Market Share: Strong dominance due to extensive industrial base, high wastewater generation volumes, and mandatory zero-discharge enforcement across multiple sectors.

United States – 21% Market Share: Leadership supported by regulatory compliance requirements, advanced industrial infrastructure, and rapid adoption of digital and modular ZLD technologies.

The Zero Liquid Discharge and Brine Treatment Market exhibits a moderately fragmented competitive environment with numerous active competitors ranging from established global firms to specialized technology providers. Approximately 15–20 major companies actively compete worldwide, offering diverse ZLD and brine treatment solutions spanning advanced membrane systems, thermal crystallization, hybrid processes, and modular skid-mounted units. Top 5 companies collectively account for around 40–50 % of the market’s technology deployments, indicating neither a highly consolidated nor a purely fragmented structure.

Market positioning varies: large multinational water technology firms dominate large industrial and municipal contracts with comprehensive portfolios, while niche players focus on high-efficiency brine concentration, resource recovery, or energy-optimizing solutions. Strategic initiatives shaping competition include partnerships (e.g., co-development deals), acquisition of specialized tech firms, modular product launches for rapid installation, and integration of digital optimization platforms. Recent activity has seen major competitors enhancing hybrid ZLD systems, deploying AI-enabled monitoring, and expanding service offerings to cover end-to-end brine valorization and water reuse.

Innovation trends also influence competitive dynamics: membrane material advancements for high-TDS tolerance, energy-minimizing thermal loops, and automated control systems are differentiators among leading vendors. The nature of competition is driven by technological breadth, project execution capability, and sustainability credentials, with companies positioning to serve water-intensive sectors such as power generation, petrochemicals, mining, and industrial wastewater treatment.

Evoqua Water Technologies

Energy Recovery Inc.

SUEZ Water Technologies & Solutions

General Electric (ZLD & filtration tech)

H2O Innovation Inc.

Pall Corporation

Lenntech B.V.

The technological landscape of the Zero Liquid Discharge and Brine Treatment Market is evolving rapidly, driven by the need for higher efficiency, lower energy consumption, and enhanced resource recovery across industries. Core technologies continue to center around membrane-based systems (including reverse osmosis and ultrafiltration), which dominate pretreatment and brine concentration stages by achieving up to 95 % contaminant removal and reducing load on subsequent units. Hybrid approaches that combine advanced RO with thermal evaporation (e.g., Mechanical Vapor Recompression or Multi-Effect Distillation) are increasingly deployed to strike a balance between operational cost and performance, cutting energy intensity in final concentration stages significantly compared to thermal alone.

Emerging tech trends include development of next-generation membranes (such as graphene oxide, ceramic, and nanocomposite materials) offering improved durability and fouling resistance, often extending membrane service life by 2–3× in hypersaline applications. Digital innovations like AI-driven process control and digital twins are enhancing real-time operational efficiency, reducing unplanned downtime due to scaling or fouling, and optimizing chemical dosing. Modular and skid-mounted ZLD systems are gaining traction for decentralized or mid-market industrial facilities, with plug-and-play designs reducing installation lead times and lowering initial capital requirements.

In brine valorization, technologies that convert concentrated brine to recoverable salts and minerals are expanding the value proposition for end-users, turning waste streams into monetizable outputs in sectors like chemicals and battery material supply chains. Alternative concentration mechanisms such as electrodialysis and forward osmosis are also being adapted to extend membrane performance while minimizing energy use. Collectively, these technological advancements shape investment decisions among industrial adopters, reinforcing the role of innovation as a competitive differentiator in the ZLD and brine treatment landscape.

Aquatech launched an advanced membrane ZLD process (AquaR2RO) designed for very high water recovery in ZLD and high-recovery plants, enabling >98 % recovery in some applications and reducing the need for larger thermal systems, optimizing CAPEX and OPEX. Source: www.aquatech.com

Aquatech has completed over 160 ZLD installations worldwide, including projects with hybrid membrane and thermal systems that maximize wastewater reclamation and allow recovery of valuable resources from brine streams. Source: www.aquatech.com

Veolia Water Technologies continues deployment of ZLD solutions across major industrial applications, with detailed case references including designing and building ZLD systems at large plants such as Shell’s Pearl GTL facility handling 45 000 m³/day using integrated ultrafiltration, RO, and evaporation/crystallization systems. Source: www.middle-east.veoliawatertechnologies.com

Veolia’s Ankleshwar ZLD common effluent treatment facility in Gujarat, India, treats concentrated wastewater from highly polluting industries and recovers ~45 % of influent water through ZLD processes, demonstrating real-world implementation of industrial ZLD solutions in emerging markets. Source: www.veolia.in

The scope of the Zero Liquid Discharge and Brine Treatment Market Report encompasses a comprehensive examination of the market’s technological, regional, application, and end-use dimensions. It covers a wide spectrum of treatment technologies, including membrane filtration, thermal evaporation, crystallization, hybrid systems, and advanced modular configurations. The report analyzes how these technologies are engineered and selected based on influent characteristics, salinity levels, and regulatory compliance requirements across industries such as power generation, petrochemicals, mining, food and beverage, and municipal wastewater management.

Geographically, the report spans major regions — North America, Europe, Asia-Pacific, South America, and Middle East & Africa — offering insight into infrastructure trends, regulatory environments, and regional consumption patterns. It assesses installation volumes, technology adoption rates, and treatment preferences by application, providing decision-makers with granular data on operational drivers and constraints. The analysis also includes forward-looking evaluations of emerging or niche market segments, such as decentralized ZLD solutions and resource recovery from brine to produce industrial salts or critical materials, creating added value streams for adopters.

The report’s industry focus areas include competitive landscapes, profiling of major vendors and innovators, and detailed segmentation by system type, process phase, and end-user category, equipping stakeholders with actionable insights for strategic planning, technology investment, and long-term operational optimization in sustainable water management.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 464.0 Million |

| Market Revenue (2032) | USD 931.4 Million |

| CAGR (2025–2032) | 9.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Veolia Environnement S.A., Aquatech International LLC, IDE Technologies, Evoqua Water Technologies, Energy Recovery Inc., SUEZ Water Technologies & Solutions, General Electric (ZLD & filtration tech), H2O Innovation Inc., Pall Corporation, Lenntech B.V. |

| Customization & Pricing | Available on Request (10% Customization Free) |