Reports

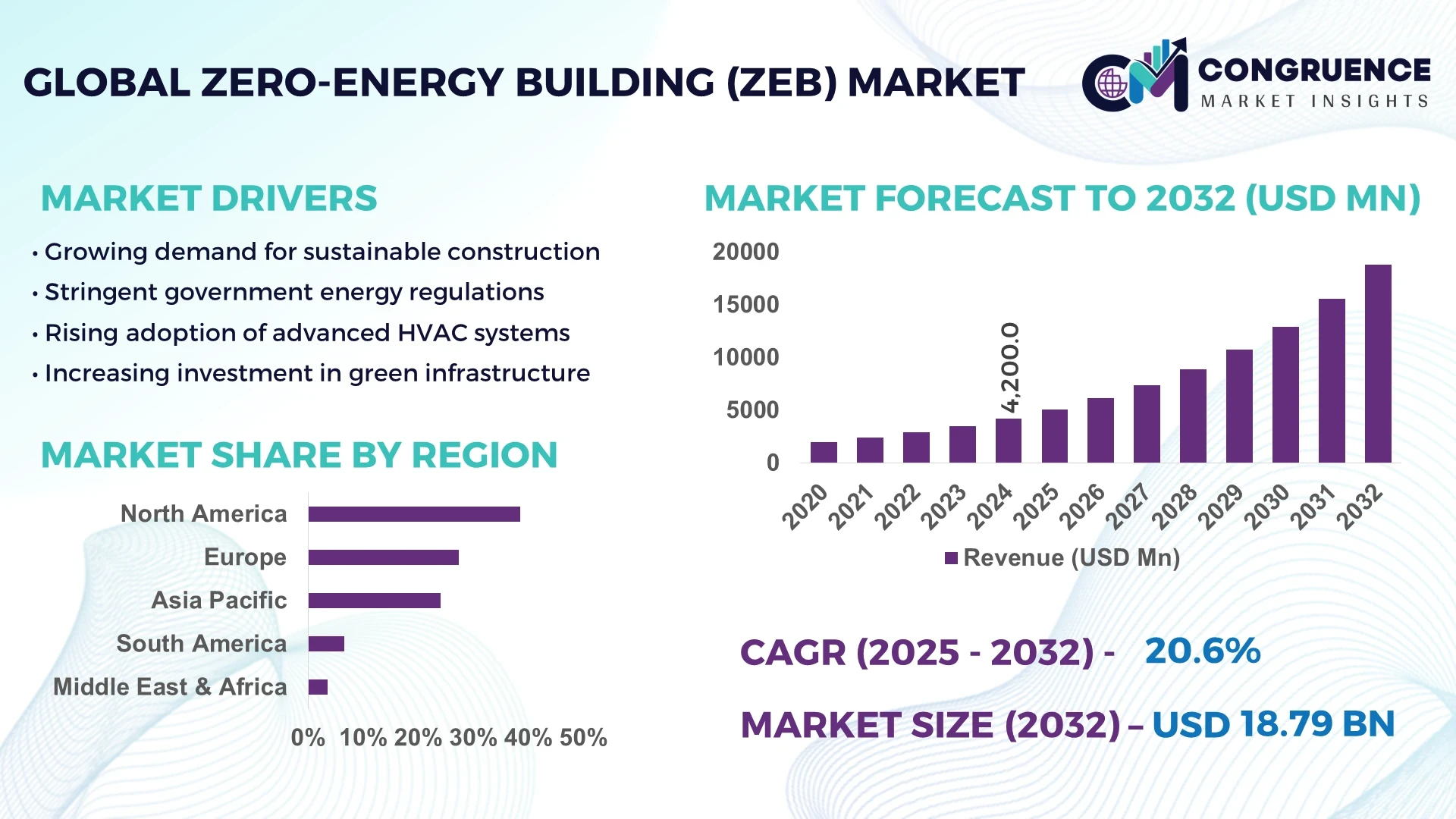

The Global Zero-Energy Building (ZEB) Market was valued at USD 4,200.0 Million in 2024 and is anticipated to reach a value of USD 18,794.4 Million by 2032 expanding at a CAGR of 20.6% between 2025 and 2032. The market growth is supported by increasing demand for sustainable construction practices and stringent global energy efficiency policies.

In the United States, Zero-Energy Building (ZEB) development has reached advanced levels due to strong federal and state-backed green building initiatives. By 2024, the country had over 180 million square feet of ZEB-certified floor area, supported by an estimated USD 15 billion in public and private investments. The application is most prominent in educational and commercial buildings, where large-scale deployment has resulted in measurable reductions of 50–70% in energy consumption compared to traditional structures. Furthermore, advancements in smart energy management, integration of solar PV systems, and AI-driven building automation have significantly strengthened production capacity and efficiency in the U.S. ZEB sector.

Market Size & Growth: Valued at USD 4,200.0 Million in 2024, projected to reach USD 18,794.4 Million by 2032, growing at a CAGR of 20.6%; driven by rising sustainability standards.

Top Growth Drivers: 40% higher adoption of solar-integrated systems, 35% efficiency improvement in HVAC, and 30% increase in energy storage integration.

Short-Term Forecast: By 2028, operational costs in ZEB projects are expected to reduce by 25% due to technology integration.

Emerging Technologies: AI-enabled energy optimization, advanced building envelopes, and next-gen solar façades are transforming the market.

Regional Leaders: North America projected at USD 7.2 billion by 2032 (driven by smart retrofitting), Europe at USD 6.1 billion (policy-driven adoption), Asia-Pacific at USD 4.9 billion (urban expansion).

Consumer/End-User Trends: Rising adoption in educational (28%) and healthcare (21%) facilities, reflecting long-term energy savings priorities.

Pilot or Case Example: In 2023, a California school district achieved 60% reduction in annual utility costs through a ZEB pilot integrating solar storage.

Competitive Landscape: Johnson Controls leads with 14% market share, followed by Schneider Electric, Siemens, Honeywell, and Skanska.

Regulatory & ESG Impact: Mandatory near-zero building codes in the EU and net-zero commitments in the U.S. are accelerating compliance-driven adoption.

Investment & Funding Patterns: Over USD 6.5 billion invested globally in 2023 across ZEB projects, with rising green bond financing.

Innovation & Future Outlook: Integration of digital twins, advanced insulation, and grid-interactive ZEB models set the stage for resilient future growth.

The Zero-Energy Building (ZEB) Market is witnessing robust adoption across commercial, residential, and institutional sectors, fueled by rapid innovations in solar PV, energy storage, and AI-based building automation. Regulatory mandates, urban expansion, and sustainability-driven financing models are expected to accelerate global adoption, positioning ZEBs as a transformative force in the future of construction.

The strategic relevance of the Zero-Energy Building (ZEB) Market lies in its role as a cornerstone of global decarbonization and sustainable urbanization strategies. Governments and corporations alike are aligning long-term infrastructure investment toward zero-energy standards, with measurable results. Comparative benchmarks indicate that advanced smart façades deliver 30% improvement in thermal efficiency compared to traditional cladding systems, directly cutting operational costs.

Regional variations are noteworthy: North America dominates in project volume, with more than 65% of large-scale ZEB projects, while Europe leads in adoption intensity, where 42% of new commercial projects comply with near-zero building standards. Short-term projections show that by 2027, AI-driven building energy management is expected to reduce HVAC energy use by 22%. Compliance commitments are also shaping adoption: the European Union mandates that all new public buildings meet near-zero standards by 2028, while the U.S. Green Building Council has pledged to cut embodied carbon by 40% by 2030.

Practical case outcomes are already visible. In 2023, Canada achieved a 28% energy intensity reduction across 120 government buildings through AI-assisted retrofitting. This showcases the micro-scenario potential for nations pursuing ZEB pathways.

Moving forward, the ZEB Market represents more than a construction trend; it is a pillar of resilience, compliance, and sustainable growth, reinforcing the transition toward climate-neutral economies while enhancing long-term asset value for investors and end-users.

The Zero-Energy Building (ZEB) Market is evolving rapidly due to converging forces of technology adoption, policy mandates, and consumer awareness. Increasing demand for low-carbon construction is fueling innovations in insulation materials, renewable integration, and AI-driven energy control systems. Policy environments in North America, Europe, and Asia-Pacific are accelerating adoption, while funding mechanisms such as green bonds and ESG-linked loans strengthen financial viability. Technological breakthroughs in prefabricated modules and smart building materials are expanding deployment opportunities, particularly in urban infrastructure projects. Collectively, these dynamics position the ZEB Market as one of the most transformative sectors within global construction and energy ecosystems.

The integration of renewable energy systems, particularly solar photovoltaic panels, is a key driver of the ZEB Market. By 2024, over 45% of ZEB projects incorporated on-site renewable generation, ensuring that buildings can meet or exceed their energy needs sustainably. The expansion of battery storage technologies further amplifies this impact, enabling uninterrupted power availability and optimizing energy use. As utility costs rise and urban electricity demand surges, renewable-backed ZEBs are emerging as cost-efficient, resilient solutions.

Despite long-term operational savings, ZEB adoption faces challenges due to elevated initial capital expenditures. Building envelopes, high-performance insulation, triple-glazed windows, and integrated energy management systems significantly increase construction budgets—by as much as 25–35% compared to conventional structures. For small and mid-sized developers, this financial barrier limits widespread adoption. Financing models and subsidies are evolving, but cost concerns remain a restraint in price-sensitive markets.

The opportunity for ZEB expansion lies strongly in retrofitting existing buildings. Globally, over 70% of current commercial buildings are energy-inefficient, creating massive potential for retrofits. By equipping old infrastructures with solar roofs, AI energy management systems, and advanced insulation, stakeholders can achieve up to 60% energy savings. With government-backed incentives and green financing, retrofitting offers a scalable pathway to accelerate ZEB adoption without waiting for new construction cycles.

The ZEB Market faces implementation challenges due to fragmented and inconsistent regulatory frameworks across regions. While the EU enforces stringent near-zero directives, regulations in Asia-Pacific and parts of Latin America remain less defined. This inconsistency complicates project financing, technology integration, and compliance timelines. Additionally, varying building codes, certification processes, and ESG reporting requirements increase operational hurdles for global developers. Aligning international standards remains a critical challenge for market acceleration.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Zero-Energy Building (ZEB) Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Expansion of Smart Building Automation: In 2024, more than 48% of ZEBs incorporated AI-driven energy automation systems, achieving an average 20% improvement in HVAC energy efficiency. Automated systems enable predictive maintenance, real-time energy optimization, and load balancing. With demand for smart energy control projected to rise by 35% by 2027, intelligent automation is becoming a central trend shaping ZEB adoption worldwide.

Growing Role of Energy Storage Systems: Battery energy storage installations in ZEB projects rose by 32% year-on-year in 2024, supporting grid resilience and optimizing renewable energy use. With lithium-ion costs dropping by 15% annually, storage integration is enabling more consistent energy supply. By 2030, projections indicate that 60% of ZEBs will feature onsite storage, strengthening their independence from conventional grids.

Integration of Next-Gen Building Materials: Innovative materials, such as vacuum-insulated panels and bio-based composites, are expanding rapidly in ZEB construction. By 2024, 28% of new ZEB projects utilized advanced insulation technologies, enabling up to 40% heat loss reduction compared to older materials. The rising use of recyclable and carbon-negative construction materials is also aligning the ZEB Market with ESG commitments and low-carbon development pathways.

The Zero-Energy Building (ZEB) Market demonstrates a diversified structure across types, applications, and end-user adoption, each influencing the pace and direction of growth. Types of ZEB solutions vary from residential to commercial and institutional models, with smart energy management systems and renewable integration defining the landscape. Applications are broad, ranging from education and healthcare to offices and residential housing, with a significant tilt toward sectors where operational cost savings and compliance drive adoption. End-users include governments, private enterprises, and real estate developers, each displaying unique priorities—whether sustainability mandates, cost-efficiency, or technological innovation. Collectively, this segmentation provides a clear picture of how ZEB adoption is shaping modern construction across geographies and industries.

Residential Zero-Energy Buildings currently account for the largest share, representing approximately 46% of the global market. This dominance is supported by widespread adoption of sustainable housing projects and rising consumer demand for energy cost savings. Commercial buildings follow at 34%, reflecting corporate investment in smart infrastructure, while institutional models, including educational and healthcare facilities, represent 20%.

Residential ZEBs maintain leadership due to large-scale integration of solar photovoltaic systems and government incentives for green housing projects. However, commercial ZEBs are the fastest-growing type, expanding at an estimated CAGR of 23%. This surge is driven by corporate commitments to ESG frameworks and increased focus on energy-efficient office complexes, particularly in North America and Europe.

The combined contribution of institutional buildings, though smaller, is significant as schools and hospitals rapidly integrate renewable systems to cut operational costs and meet compliance standards.

Educational facilities lead the application segment, holding a share of approximately 38%. Their dominance is fueled by strong government support for sustainable learning environments and rising operational cost savings, which average 50% lower than traditional buildings. Commercial offices account for 30%, while residential projects stand at 22%. Healthcare facilities and other public infrastructure collectively contribute the remaining 10%.

Commercial applications are the fastest-growing, projected to expand at a CAGR of 24%. The increase is supported by rapid corporate investments in sustainable office complexes and smart workspaces designed to reduce energy intensity. Residential applications remain critical, particularly in Asia-Pacific where urban housing demand is driving ZEB adoption.

In 2024, over 41% of universities in the U.S. reported active pilot projects for zero-energy campus buildings, reflecting institutional leadership in the sector. Additionally, consumer adoption trends show that 35% of households in Europe prioritized homes with renewable energy integration as part of their property selection criteria.

Government and public authorities dominate the end-user landscape, representing approximately 44% of ZEB adoption globally. This segment is bolstered by regulatory mandates and publicly funded infrastructure projects, particularly in education and healthcare. Private enterprises follow closely with a 33% share, reflecting corporate ESG commitments and sustainability-driven investments. Real estate developers and residential consumers together account for the remaining 23%.

Private enterprises are the fastest-growing end-user segment, expanding at a CAGR of 25%, propelled by the need to enhance corporate sustainability credentials and reduce long-term operating expenses. Real estate developers are also gaining momentum, particularly in Asia-Pacific where urbanization is accelerating demand for sustainable housing.

Adoption rates in industry show clear trends: in 2024, 52% of Fortune 500 companies disclosed investments in sustainable office spaces, while 29% of global hospitals reported integration of ZEB-compatible energy systems into their facilities.

North America accounted for the largest market share at 38.5% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22.3% between 2025 and 2032.

North America’s dominance stems from strong regulatory frameworks, higher adoption in healthcare and finance sectors, and the presence of global technology players. Europe followed with nearly 27.4% share, benefiting from strict energy-efficiency directives across Germany, the UK, and France. Asia-Pacific, though at 24.1% share in 2024, is projected to outpace other regions due to rapid urbanization in China and India, strong government subsidies, and increasing smart city developments. South America and Middle East & Africa collectively represented around 10% of the total market, reflecting early-stage adoption but rising investments in renewable energy and sustainable building codes. This regional distribution highlights a clear trend of developed economies leading adoption, while emerging markets drive future expansion.

North America held approximately 38.5% of the Zero-Energy Building (ZEB) market share in 2024, making it the leading region. The market is driven by demand from industries such as healthcare, commercial real estate, and finance, which are heavily investing in sustainable infrastructure. Regulatory initiatives like updated building codes and federal energy efficiency standards are accelerating adoption, while digital integration through IoT-enabled energy management systems supports scalability. Companies such as Rocky Mountain Institute are actively promoting ZEB pilot projects across the United States. Consumer behavior trends in this region reveal higher adoption in healthcare and financial institutions, where long-term energy cost savings and sustainability goals align with business models.

Europe captured around 27.4% of the global ZEB market share in 2024, with Germany, the UK, and France leading adoption. Strong policy frameworks under the European Green Deal and the Energy Performance of Buildings Directive have compelled construction companies to integrate ZEB solutions. Advanced technologies, including AI-driven energy optimization and high-performance insulation materials, are being increasingly deployed. Local companies like Saint-Gobain are advancing building envelope innovations that reduce energy use. Consumer adoption is shaped by strict regulatory pressure and a heightened demand for transparent and measurable sustainability outcomes. This behavior underscores Europe’s role as a policy-driven market, fostering fast-paced adoption across both residential and commercial buildings.

Asia-Pacific accounted for nearly 24.1% of the ZEB market volume in 2024, ranking as the fastest-growing region. China, India, and Japan dominate consumption, with large-scale infrastructure developments and smart city initiatives driving adoption. Manufacturing hubs in China and Japan are integrating solar PV, energy storage, and AI-enabled building management systems. Local players such as China State Construction Engineering Corporation are investing heavily in ZEB pilot projects. Consumer behavior highlights a preference for digitally connected, sustainable buildings, especially in urban residential and commercial developments. Growth is being accelerated by demand from e-commerce warehouses, IT campuses, and high-density urban centers, reflecting Asia-Pacific’s rapid transition toward energy-neutral construction.

South America accounted for nearly 6.5% of the ZEB market share in 2024, with Brazil and Argentina leading the region. Investments in urban infrastructure, renewable energy integration, and government-driven green building certifications are supporting adoption. Brazil is at the forefront with initiatives to promote net-zero energy schools and hospitals. Local construction firms are beginning to integrate smart HVAC systems and solar PV modules in commercial projects. Consumer behavior shows a growing focus on localized media, culture-driven adoption, and urban eco-housing projects. Government incentives such as tax rebates and energy-efficiency credit programs are key catalysts for broader ZEB adoption in this region.

Middle East & Africa represented about 3.5% of the global ZEB market share in 2024, with notable growth in UAE, Saudi Arabia, and South Africa. Demand is being driven by large-scale construction megaprojects such as NEOM in Saudi Arabia, coupled with energy diversification strategies that emphasize renewables. Local regulations requiring higher energy-efficiency ratings in new constructions are boosting demand. Firms like Masdar in the UAE are pioneering net-zero campuses and pilot projects to align with national sustainability targets. Consumer adoption trends reveal a growing focus on luxury green housing and energy-smart office spaces, reflecting the region’s shift toward sustainable yet high-tech building solutions.

United States – 32% Market Share: Dominance due to strong policy frameworks, high enterprise adoption, and significant private sector investment in sustainable buildings.

China – 18% Market Share: Leadership supported by large-scale infrastructure projects, rapid urbanization, and government-backed smart city initiatives driving ZEB deployment.

The competitive environment in the Zero-Energy Building (ZEB) Market is moderately fragmented, with over 50 active competitors globally offering solutions spanning renewable generation, energy-management systems, high-performance building materials, and integrated design services. The top 5 companies together hold an estimated 30-35% combined share, while the remainder of the market is made up of numerous smaller firms, specialized tech providers, and local contractors. Key players are investing in strategic initiatives such as forming partnerships with governments, launching new envelope technologies, merging with energy storage specialists, and expanding product offerings into smart building automation.

Innovations like phase change materials (PCMs), building-integrated photovoltaics (BIPV), natural ventilation systems, and predictive energy control are influencing competition heavily. Companies that integrate multiple systems—e.g., renewable generation + energy storage + intelligent controls—are gaining positioning advantages. There is also an increasing number of pilot projects in retrofits, not just new builds, so firms specializing in retrofit technologies are emerging. Product launches are focusing on envelope improvements (windows, insulation), digital twin/IoT-based energy monitoring platforms, and combinations of PV + heat-pump + storage. Furthermore, some competitors are expanding their geographic focus into high-growth regions (Asia-Pacific, Middle East) and forming alliances with local firms to meet regulatory/local content requirements. The nature of competition thus is both technological (who can deliver more efficient, integrated solutions) and strategic (who can operate across more regions and in both new construction and retrofits).

Kingspan Group

Rocky Mountain Institute

Saint-Gobain

Daikin Industries

Honeywell International Inc.

Trane Technologies

In the Zero-Energy Building (ZEB) Market, current and emerging technologies are reshaping what is feasible in both new construction and retrofits. One significant trend is the use of phase-change materials (PCMs) in walls and ceilings, which buffer thermal loads by storing and releasing heat, leading to reduced HVAC burden. Another is broader deployment of building-integrated photovoltaics (BIPV) and photovoltaic-thermal hybrids; these allow façades, roofs, or glazing to not only produce electricity but also potentially heat or cooling through dual-use surfaces.

Natural ventilation strategies coupled with smart building orientation and advanced insulation (triple glazing, high R-value walls) are becoming standard in designs aiming for zero-energy thresholds. There is also growing interest in predictive energy management systems that use sensor networks, occupancy data, weather forecasts, and machine learning to optimize building energy flows in real time.

Active renewable technologies such as efficient heat pumps (air-source, ground-source), integrating heat recovery systems, and storage (battery, thermal) are increasingly combined with passive technologies. Recent projects show that combining PCMs + BIPV + predictive controls can reduce annual delivered energy loads by 40-60% compared to otherwise similar traditional buildings. Innovation is also happening in materials: for example, optical wood with switchable solar transmittance (visible to infrared) is being explored, offering new passive thermal regulation capabilities.

All of these technologies are enabling greater modularity, adaptability, and alignment with regulatory emission and efficiency standards. Decision-makers are paying attention not just to peak performance, but to lifecycle embodied carbon, integration of smart systems, and maintainability.

In 2024, the U.S. Department of Energy awarded USD 90 million in grants to support the implementation of energy-efficient building codes under its federal high-performance buildings program, boosting adoption of zero-energy standards. Source: www.newbuildings.org

In 2023, the EnergyX DY-Building in South Korea was officially certified as a Plus Zero Energy Building with an energy self-sufficiency rate of 129.59%, achieving more energy generation than consumption via passive design, high-performance insulation, and building-integrated photovoltaics. Source: www.wikipedia.org/wiki/EnergyX_DY-Building

In 2024, innovation in photovoltaic systems with integrated cooling designs (e.g., externally finned PVs, PV with phase-change material integration) was demonstrated in cities including Barcelona, Munich, Athens, and Stockholm to improve solar panel performance on façades and roofs in ZEBs. Source: www.mdpi.com

Also in 2024, green roofs and solar chimneys regained strong focus—cities such as New York and Chicago expanded incentive programs to promote passive cooling and energy savings measures that reduce indoor temperatures by up to 30% during peak summer conditions. Source: www.theguardian.com

This report covers the full breadth of the Zero-Energy Building (ZEB) Market, spanning both new construction and retrofit projects across residential, commercial, institutional, and industrial buildings. Technologies examined include passive design elements (e.g. insulation, glazing, natural ventilation, building orientation), active systems (solar photovoltaics, BIPV/BAPV, heat pumps, energy storage, thermal systems), and digital building energy management platforms (IoT, predictive controls, occupancy sensors). Geographic regions addressed are North America, Europe, Asia-Pacific, South America, Middle East & Africa, each showing different stages of adoption and technology maturity.

Applications analyzed include housing (single-family, multi-family), offices, healthcare, education, public infrastructure, and hospitality. End-user segments include governments/public sector, private enterprises, real estate developers, and institutional users. This report also considers regulatory and ESG drivers, design trends, product innovations, pilot/case studies, and material developments (e.g., new envelope materials, optical woods, PCMs). Special attention is paid to emerging or niche realms such as Plus Zero Energy Buildings (buildings that generate more energy than they consume), hybrid renewables + cooling systems, façade-integrated PVs, and advanced thermal regulation technologies. The aim is to support decision-makers with a clear view of the competitive landscape, technology options, regional pressures, and future pathways for investment and strategic positioning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,200.0 Million |

| Market Revenue (2032) | USD 18,794.4 Million |

| CAGR (2025–2032) | 20.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Kingspan Group, Rocky Mountain Institute, Schneider Electric, Siemens, Johnson Controls, Saint-Gobain, Daikin Industries, Honeywell International Inc., Trane Technologies |

| Customization & Pricing | Available on Request (10% Customization is Free) |