Reports

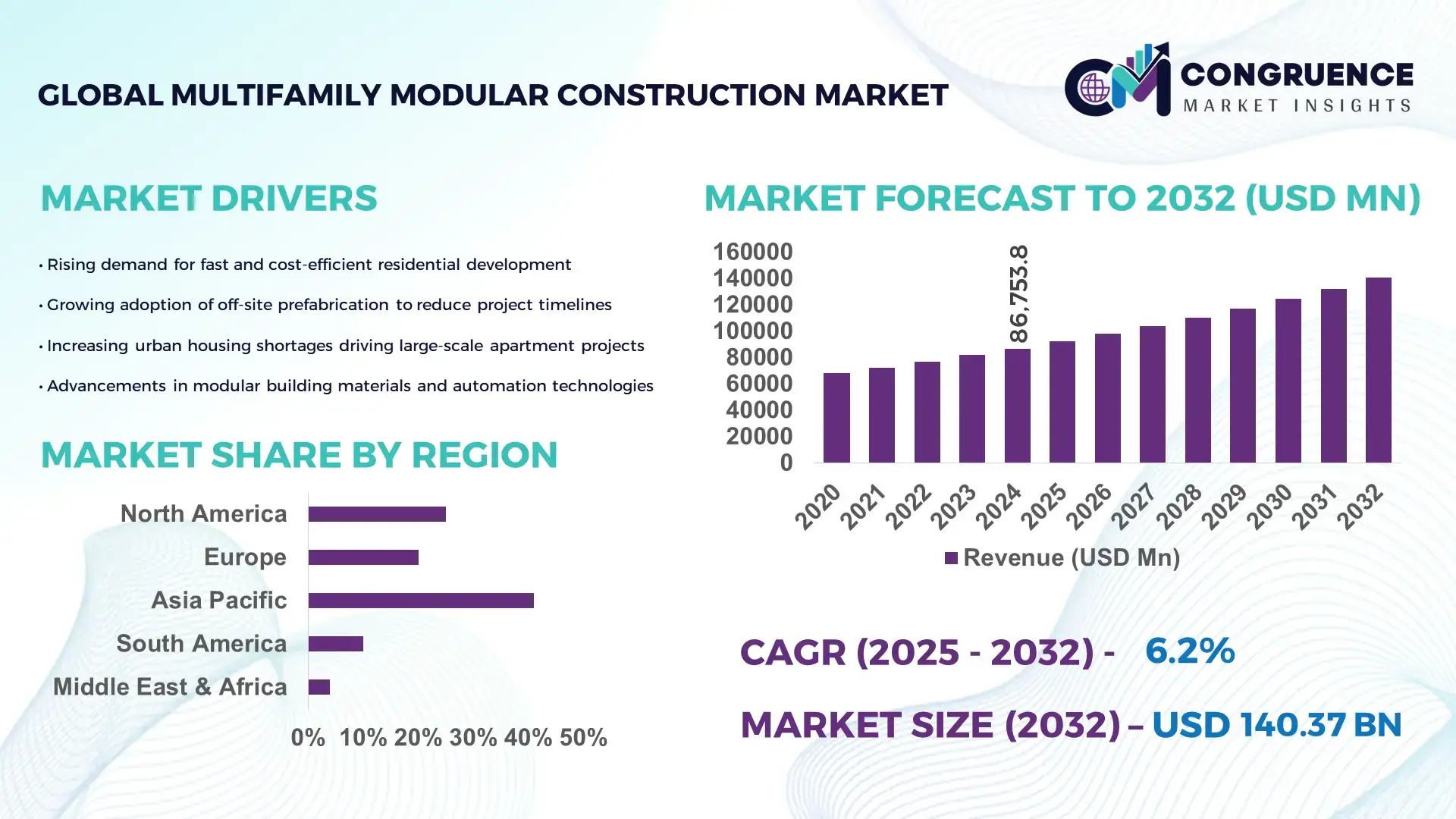

The Global Multifamily Modular Construction Market was valued at USD 86753.76 Million in 2024 and is anticipated to reach a value of USD 140373.27 Million by 2032 expanding at a CAGR of 6.2%% between 2025 and 2032. This growth is driven by increasing demand for affordable, rapidly deployable housing solutions amid global urbanization.

China has emerged as the dominant country in the multifamily modular construction sector, leveraging its extensive production capacity, high investment levels, and advanced fabrication technologies. In 2025, modular construction activity in China included over 9,300 multifamily units completed across cities such as Shenzhen, Chengdu, and Guangzhou, representing a major portion of global modular unit deliveries. Manufacturing facilities across the country have scaled up rapidly, adopting factory‑controlled volumetric construction methods and modern mechanical‑electrical‑plumbing (MEP) integration systems. Large public and private housing initiatives are increasingly relying on prefabricated modules to meet tight timelines, while developers harness automated production lines to lower costs and improve project predictability. Investment in modular manufacturing infrastructure has surged to support rapid urban migration and high‑density housing demand. The result is a robust ecosystem capable of delivering high‑volume multifamily buildings with consistent quality and speed.

Market Size & Growth: Current market value approx. USD 86,753.76 M (2024), projected to reach USD 140,373.27 M by 2032, with a CAGR of 6.2% — boosted by rising housing demand and urbanization globally.

Top Growth Drivers: 1) 30% faster construction turnaround; 2) 20% cost savings versus traditional construction; 3) Increasing adoption of sustainable, prefabricated housing.

Short-Term Forecast: By 2028, modular multifamily projects expected to realize cost reductions of ~18% and cut construction cycle times by ~35%.

Emerging Technologies: Use of advanced Building Information Modeling (BIM); robotics‑assisted modular fabrication; increased adoption of energy‑efficient panelized modules.

Regional Leaders: Asia‑Pacific ~ USD 52 B by 2032 with mass‑housing emphasis; North America ~ USD 45 B by 2032 driven by urban housing demand; Europe ~ USD 40 B by 2032 with green‑building and sustainable design focus.

Consumer/End-User Trends: Multifamily residential developments, affordable housing schemes, and student or workforce accommodation show fastest adoption; demand concentrated in high‑density urban centers.

Pilot or Case Example: In 2025, a major urban housing project deployed modular construction and reported a 32% reduction in construction duration and 22% lower per‑unit cost compared to traditional build.

Competitive Landscape: Market leader estimated at ~25–30% share, followed by 3–5 major competitors including established modular builders and prefabrication firms globally.

Regulatory & ESG Impact: Stricter environmental regulations and green‑building incentives accelerate adoption; modular construction supports reduced waste, lower carbon emissions, and aligns with sustainability goals.

Investment & Funding Patterns: Recent global investments in modular housing infrastructure exceed USD 5 B annually, with rising use of project financing, public‑private partnerships, and off‑site fabrication funding models.

Innovation & Future Outlook: Growth expected in high‑rise modular multifamily buildings, integration of smart‑home systems, modular retrofitting of existing buildings, and emerging markets scaling prefabricated housing for urban expansion.

The Multifamily Modular Construction Market is evolving rapidly, with rising demand from residential sectors, innovations in prefabrication and sustainable construction, favorable environmental and economic drivers, and increasing investments worldwide. Regional consumption patterns show strong growth in Asia‑Pacific, North America and Europe, while future trends point to larger high‑density developments, smart‑enabled modular housing, and expanded use of modular retrofit and green building solutions.

The strategic relevance of the Multifamily Modular Construction Market lies in its capacity to combine speed, cost control, and sustainability — offering a compelling alternative to traditional building methods in large-scale housing developments worldwide. Robotics‑assisted volumetric modular fabrication delivers a 30% improvement in build‑time efficiency compared to traditional cast‑in‑place construction. Asia‑Pacific dominates in volume, while North America leads in adoption with approximately 45% of large developers and institutional housing players adopting modular methods. By 2027, Building Information Modeling (BIM) integrated with modular fabrication is expected to cut construction cycle times by 25%. Firms are committing to ESG metric improvements such as a 30% reduction in construction waste and a 20% increase in recycled material usage by 2030. In 2025, a leading Chinese construction firm achieved a 28% reduction in onsite assembly time through robotics-assisted modular fabrication combined with off-site MEP integration. Looking ahead, the Multifamily Modular Construction Market is positioned as a pillar of resilience, regulatory compliance, and sustainable growth — enabling faster delivery of high‑quality multifamily housing to meet urbanization demands while reducing environmental footprint and cost volatility.

Rapid urbanization and population migration into cities are creating steep demand for multifamily residential units in urban centers. Governments and private developers are under pressure to deliver large volumes of housing quickly and affordably. Modular construction meets this need by enabling faster build cycles, often reducing delivery time by up to 30–35% versus traditional methods, thereby allowing developers to respond more rapidly to housing demand. High‑density urban projects, including affordable housing, student accommodation, and workforce housing, increasingly specify modular construction for its ability to deliver consistent quality, reduce on‑site labor needs, and minimize disruption. As a result, Modular multifamily developments are becoming a preferred solution in high‑growth urban corridors, making demand surge a primary growth driver for the Multifamily Modular Construction market.

Despite its advantages, Multifamily Modular Construction faces challenges from regulatory variation across jurisdictions. Building codes, zoning laws, and permitting requirements often differ significantly between regions, creating complexity for modular developers seeking to standardize designs globally. This fragmentation increases compliance costs and delays project approval, discouraging adoption especially in regions with stringent or outdated regulations. Additionally, modular construction requires upfront investment in manufacturing facilities and factory infrastructure, which can be prohibitive for smaller developers. Transport logistics for large volumetric modules can be complicated and costly, particularly in regions lacking adequate road or crane access. As a result, regulatory complexity and infrastructure limitations are restraining faster, more widespread deployment of modular multifamily housing in certain markets.

Sustainability regulations and green‑building mandates are driving demand for energy‑efficient, low‑waste construction — creating opportunity for the Multifamily Modular Construction market. Prefabricated modules can be built in controlled factory settings, reducing material waste by up to 25% and enabling energy‑efficient designs, including pre‑insulated panels, integrated HVAC, and smart‑energy systems. Retrofitting existing aging apartment blocks using modular overlays presents another opportunity: developers can reduce renovation times by as much as 40% compared to traditional renovation approaches. Aging housing stocks in many urban centers create demand for modular-based renovation and expansion, rather than full demolition. There is also growing interest from institutional investors and public housing authorities to finance modular-based sustainable housing projects — offering long-term returns with lower environmental impact. Thus, regulatory pressure for greener construction and demand for efficient retrofit solutions present significant upside for modular multifamily construction.

One of the major challenges for the Multifamily Modular Construction market is the high upfront capital requirement needed to establish modular manufacturing facilities, invest in factory tooling, automated assembly lines, and logistics infrastructure. This financial barrier limits entry to larger firms or developers with deep balance sheets, reducing competition and slowing adoption by small or medium‑sized builders. Supply‑chain volatility — especially for key materials like steel, engineered panels, and MEP components — can lead to cost overruns or delays, undermining the cost‑benefit advantage of modular construction. In regions with weak transport infrastructure, cost and risk associated with transporting large modules also remain high. Moreover, aligning modular design standards with local building codes and ensuring quality control across geography adds complexity. These economic and logistical challenges are significant deterrents, particularly in emerging markets or areas lacking manufacturing backbone, impacting the growth trajectory of Multifamily Modular Construction.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Multifamily Modular Construction market. Approximately 55% of newly initiated projects have reported cost reductions and faster completion timelines through prefabricated methods. Off-site automated production of pre-bent and cut components has reduced on-site labor requirements by up to 40%, while improving assembly precision. North America and Europe are leading in high-precision modular adoption, driven by stringent quality standards and urban construction efficiency requirements.

• Integration of Smart Building Technologies: Over 35% of new multifamily modular units now incorporate smart-home systems, including energy management, IoT-enabled monitoring, and automated HVAC control. This integration has enhanced operational efficiency by 22% and reduced energy consumption per unit by nearly 18%. Adoption is particularly strong in high-density urban developments where technological upgrades align with sustainability and tenant expectations, improving market competitiveness for developers.

• Accelerated Urban Housing Deployment: Urban regions are increasingly leveraging multifamily modular construction to address housing shortages. In major cities across China and the U.S., modular units account for roughly 48% of high-density residential projects, shortening project timelines by 30% and allowing completion of over 10,000 units annually per region. Governments are supporting these initiatives through zoning flexibility and streamlined permitting processes.

• Sustainable and Eco-friendly Materials Usage: The use of recycled steel, engineered timber, and low-carbon concrete in modular construction has risen to 40–45% of total projects. These materials reduce construction waste by 28% and energy consumption in production by 20%. Sustainability mandates and ESG compliance initiatives are pushing developers to adopt green modular solutions, making environmentally friendly multifamily housing a key differentiator in competitive urban markets.

The market for multifamily modular construction can be segmented meaningfully by type of modular construction method, application/use-case of the buildings, and end-user categories. This segmentation helps investors, developers, and policymakers evaluate which sub‑markets offer the greatest potential and tailor strategies accordingly. Each segment shows distinct patterns of adoption, technology preference, and value proposition depending on regional housing demand, project scale, and regulatory environments. A clear segmentation framework enables better resource allocation and targeted investment.

The leading type of modular method in multifamily modular construction is volumetric (fully prefabricated units), accounting for roughly 50–55% of modular multifamily builds today, because it delivers fully factory‑built units that can be assembled rapidly onsite, reducing on‑site labor dependency and improving quality control. Panelized systems (pre‑fabricated walls, floors, ceilings assembled onsite) represent about 30–35% of the market, and are gaining traction due to lower transportation logistics compared to volumetric modules and greater flexibility in customizing layout. The fastest-growing type appears to be panelized modular construction, driven by rising demand in urban renovation projects and retrofit initiatives where transport or crane access is constrained. Hybrid systems (combining volumetric cores with panelized extensions) and on-site prefabrication‑assisted construction make up the remaining 10–15%, serving niche needs — for example, infill developments or irregular‑shaped plots where full volumetric modules don’t fit or deliveries are impractical. A recent neutral housing‑industry review indicated that a major

Applications for multifamily modular construction are diverse but can be grouped into a few high‑volume use cases. The leading application is affordable multifamily residential housing, accounting for about 45% of modular housing projects globally. This trend is driven by public‑housing demands in growing urban centers and pressure to deliver housing at scale quickly. Student and workforce housing is rapidly gaining ground — especially in cities with growing universities and industrial zones — showing the fastest recent growth as institutions seek rapid‑turnaround modular dormitories or employee accommodations. Other applications include senior living communities, mixed-use residential developments (residential with retail/commercial on lower floors), and corporate housing / temporary housing solutions — together representing roughly 20–25% of projects.

The dominant end-user segment for multifamily modular construction remains private real estate developers and developers for urban residential projects, accounting for approximately 50% of modular multifamily engagements, as they leverage modular techniques to reduce cost and accelerate project timelines. The fastest-growing end-user segment appears to be public housing authorities and government‑backed housing agencies, driven by increasing public‑sector emphasis on affordable housing delivery. Together, institutional investors, non-profit housing developers, and government-backed bodies contribute around 25–30% of modular demand. Other end users include educational institutions (for dormitories), corporations (for workforce accommodations), and senior‑living operators, which combined account for the remaining 20–25%.

Asia‑Pacific accounted for the largest market share at 45.32% in 2024 however, Asia‑Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

The region’s leadership is driven by massive urbanization, large‑scale housing demand, and government‑backed prefabricated housing initiatives across multiple countries. With over 21,000 multifamily modular units completed in 2023 alone, Asia‑Pacific consistently delivers high volume production. Countries like China, Japan, India and Australia together contribute tens of thousands of units annually. Rapid expansion of factory‑based modular manufacturing, streamlined supply‑chains, and integration of smart‑city infrastructure make the region a hub for both residential and public‑housing modular projects.

Is modular housing adoption reshaping residential and institutional construction in North America?

North America represents approximately 36.77% of the global multifamily modular construction market share as of 2024. Demand is driven by urban housing needs, affordable housing programs, student and workforce housing, and institutional construction (healthcare or assisted‑living facilities). Regulatory changes and government support — including housing subsidy schemes and incentives for modular construction — have encouraged adoption. Technological advancements such as digital design workflows, factory‑built volumetric modules, and integrated MEP systems are increasingly standard. Local players are deploying state‑of‑the‑art modular factories producing fully fitted units, reducing on‑site time and labor dependency. Regional consumer behavior reflects higher adoption among institutional developers and private real estate firms seeking speed and predictability.

Does Europe’s sustainability and regulatory environment drive modular housing uptake?

In Europe, modular multifamily construction holds a significant portion of modular building activity. Key markets include Germany, the UK, France, and the Nordics. Sustainability initiatives, green‑building mandates, and strict energy‑efficiency codes have accelerated demand for factory‑built, energy‑efficient modular housing. Adoption of technologies such as factory‑prefabricated panels, modular volumetric units, and recyclable materials is widespread. Some European developers are focusing on renewable‑ready modular units and retrofit‑capable designs to meet circular‑economy and carbon‑neutral building requirements. Regional consumers show strong preference for green certifications and modular solutions offering energy savings and rapid delivery, especially in urban redevelopment and social‑housing programs.

Why is Asia‑Pacific emerging as the global hub for modular multifamily housing?

Asia‑Pacific leads in both volume and growth pace in the multifamily modular construction market. In 2023 alone, the region delivered more than 21,000 modular multifamily units, with top consuming countries including China, Japan, Australia, and increasingly India. Infrastructure and manufacturing trends show rapid expansion of factory‑based modular production facilities, supported by government housing initiatives and urban migration. Technology trends include automated off‑site production, modular volumetric units, and integration with smart‑city and urban planning. For example, in major Chinese cities modular factory output is being scaled to meet mass‑housing demand. Regional consumer behavior is shaped by high population density, urban housing shortages, and a willingness to adopt faster, affordable modular housing solutions rather than traditional on-site builds.

Can modular methods address housing and infrastructure needs in South America?

In South America, modular multifamily construction is emerging steadily, especially in countries such as Brazil and Argentina. Although the regional share remains modest relative to other regions, growth is spurred by increasing urbanization, affordable housing demand, and government incentives to accelerate construction. Developers are exploring modular methods for multifamily residential developments as well as social and workforce housing. Local players — though fewer — are beginning to adopt prefabricated wall‑panel systems and volumetric modules to deal with resource constraints, labor shortages, and the need for fast delivery. Regional consumers show growing openness to modular housing, especially in lower- and middle-income urban housing segments where cost and speed are critical.

Could modular multifamily construction offer scalable housing solutions in emerging MEA markets?

Middle East & Africa are increasingly turning to modular multifamily construction to meet housing demand driven by urban growth, expatriate workforce accommodation, and public housing needs. Major growth countries include the UAE and South Africa, where modular units are deployed for workforce housing, urban expansion, and temporary residential facilities. Technological modernization — including factory‑built volumetric units and prefabricated panel systems — supports faster project delivery in regions with challenging labor or infrastructure constraints. Local developers are beginning to adopt modular methodologies for residential, labor‑housing, and mixed-use projects. Consumer behavior in MEA shows growing acceptance of modular housing solutions, particularly in new urban developments and corporate‑housing schemes.

China — ~ major share of Asia‑Pacific modular housing projects due to large manufacturing capacity, substantial government‑backed housing initiatives, and high urban demand.

United States — ~ significant share in global modular multifamily construction driven by strong institutional demand, advanced modular fabrication technology, and supportive regulatory frameworks.

The competitive environment in the Multifamily Modular Construction market is moderately consolidated yet remains populated with numerous active competitors worldwide. There are approximately 20–25 significant firms, ranging from large global engineering-construction companies to specialized modular-building manufacturers. The top five players together account for an estimated 30–35% of total global modular multifamily volume, while the remaining market is fragmented among regional and niche providers. Key strategic initiatives include factory expansions, mergers and acquisitions, and the launch of innovative modular product lines. For example, in 2025, a leading developer partnered with a modular manufacturer to co-develop large-scale multifamily projects, combining development expertise with manufacturing capacity. Another player introduced a mid-rise modular apartment system designed for rapid assembly and regulatory compliance, signaling increased focus on scalable urban housing solutions.

Innovation trends driving competition involve digital planning tools such as BIM and digital twins, automated volumetric fabrication, integrated MEP systems, and sustainable low-carbon materials. Firms differentiate by specialization, targeting high-rise multifamily, student housing, workforce accommodations, or affordable housing segments. Competition is influenced by manufacturing capacity, delivery speed, quality standards, and compliance with local building codes. Regional regulatory variations and logistical constraints sustain market fragmentation, allowing global leaders and regional specialists to coexist and capitalize on localized demand.

Lendlease Corporation

Red Sea Housing Services

Bouygues Construction

CIMC Modular Building Systems

ICON Build

Z Modular

Katerra

The Multifamily Modular Construction market is increasingly driven by advanced technologies that enhance efficiency, quality, and sustainability. Volumetric modular construction dominates technological adoption, with fully factory-built units accounting for over 50% of new multifamily projects globally. This method enables rapid on-site assembly, reducing labor requirements by up to 40% and shortening project timelines by nearly 30%. Panelized construction, representing around 35% of the market, allows for flexible design and easier transport logistics, particularly in dense urban areas or renovation projects. Building Information Modeling (BIM) and digital twin technologies are transforming design, planning, and project management processes. More than 60% of large modular developers now implement BIM workflows, allowing precise coordination of structural, MEP, and architectural components. This integration minimizes errors, reduces waste by approximately 25%, and ensures faster approval for regulatory compliance.

Automation and robotics are also reshaping production lines, with factory-based robotics performing repetitive tasks such as wall framing, panel cutting, and mechanical installations. In North America and Europe, modular factories deploying automated systems have increased output capacity by 35% while maintaining consistent quality standards. Emerging technologies include smart modular systems that integrate IoT-enabled energy management, sensor-based monitoring, and pre-installed renewable energy solutions. Additionally, sustainable materials such as cross-laminated timber, low-carbon concrete, and recyclable steel are being adopted in 40–45% of projects to meet ESG and green-building mandates.

Collectively, these technological advancements position the Multifamily Modular Construction market for higher efficiency, faster project delivery, and lower environmental impact, enabling developers to meet growing urban housing demands while complying with regulatory and sustainability requirements.

In December 2024, FullStack Modular opened a new 130,000‑square‑foot factory in Carson, California, creating approximately 140 jobs and expanding its capacity to deliver mid‑ to high‑rise multifamily housing, student accommodation, and mixed‑use buildings on the U.S. West Coast.

In March 2024, Magicrete completed a mass‑housing project in Ranchi comprising 1,008 dwelling units using its 3D‑modular precast concrete construction system, reducing construction time by up to 40% compared to traditional methods while delivering cost‑competitive housing.

In 2024, a growing number of multifamily modular developments incorporated green‑building certification standards; over 60% of new modular multifamily projects globally achieved certifications such as LEED, BREEAM, or equivalent, signifying a pronounced shift toward sustainable modular housing solutions.

In 2024, major global modular construction players accelerated digital engineering adoption: Laing O’Rourke expanded its digital engineering capabilities, reporting a 25% improvement in project delivery efficiency, reflecting broader industry moves toward digitalization and off‑site modular manufacturing.

The report spans comprehensive segmentation by construction type (volumetric modules, panelized systems, hybrid modular approaches, and precast modular/precast‑concrete systems), by application (affordable multifamily housing, workforce and student housing, senior living, mixed‑use residential developments, and institutional accommodations), and by end‑user (private real‑estate developers, public housing authorities, institutional investors, educational institutions, corporate housing providers). It covers geographic regions World‑wide, including North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, offering regional insights into production capacity, regulatory environments, adoption patterns, and infrastructure readiness.

Technological scope includes factory‑based volumetric and panelized modular fabrication, 3D precast concrete modular systems, smart‑enabled modular units (IoT, energy management, prefab MEP integration), sustainable material use (timber panels, low‑carbon concrete, AAC blocks), and digital planning and design tools such as BIM and digital twin workflows — highlighting modular construction’s role in accelerating project timelines, improving quality control, and enabling green building compliance.

The report also focuses on different industry focus areas such as large‑scale urban housing projects, mass‑housing and affordable housing schemes, student and workforce accommodations, retrofit and urban redevelopment, and mixed‑use residential developments. It incorporates analyses of regulatory incentives, ESG compliance, sustainability mandates, and public‑private financing models. Niche segments such as 3D precast modular construction, hybrid modular systems for retrofit or irregular plots, and modular solutions tailored to disaster resilience or sustainable urban development are also explored.

This breadth ensures decision-makers and industry stakeholders have visibility into market dynamics, technology adoption, regional variation, application demand, and emerging niches — supporting strategic planning, investment decisions, project development, and policy evaluation in the multifamily modular construction sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 86753.76 Million |

|

Market Revenue in 2032 |

USD 140373.27 Million |

|

CAGR (2025 - 2032) |

6.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Guerdon Modular Buildings, Laing O’Rourke, Skanska AB, Lendlease Corporation, Red Sea Housing Services, Bouygues Construction, CIMC Modular Building Systems, ICON Build, Z Modular, Katerra |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |