Reports

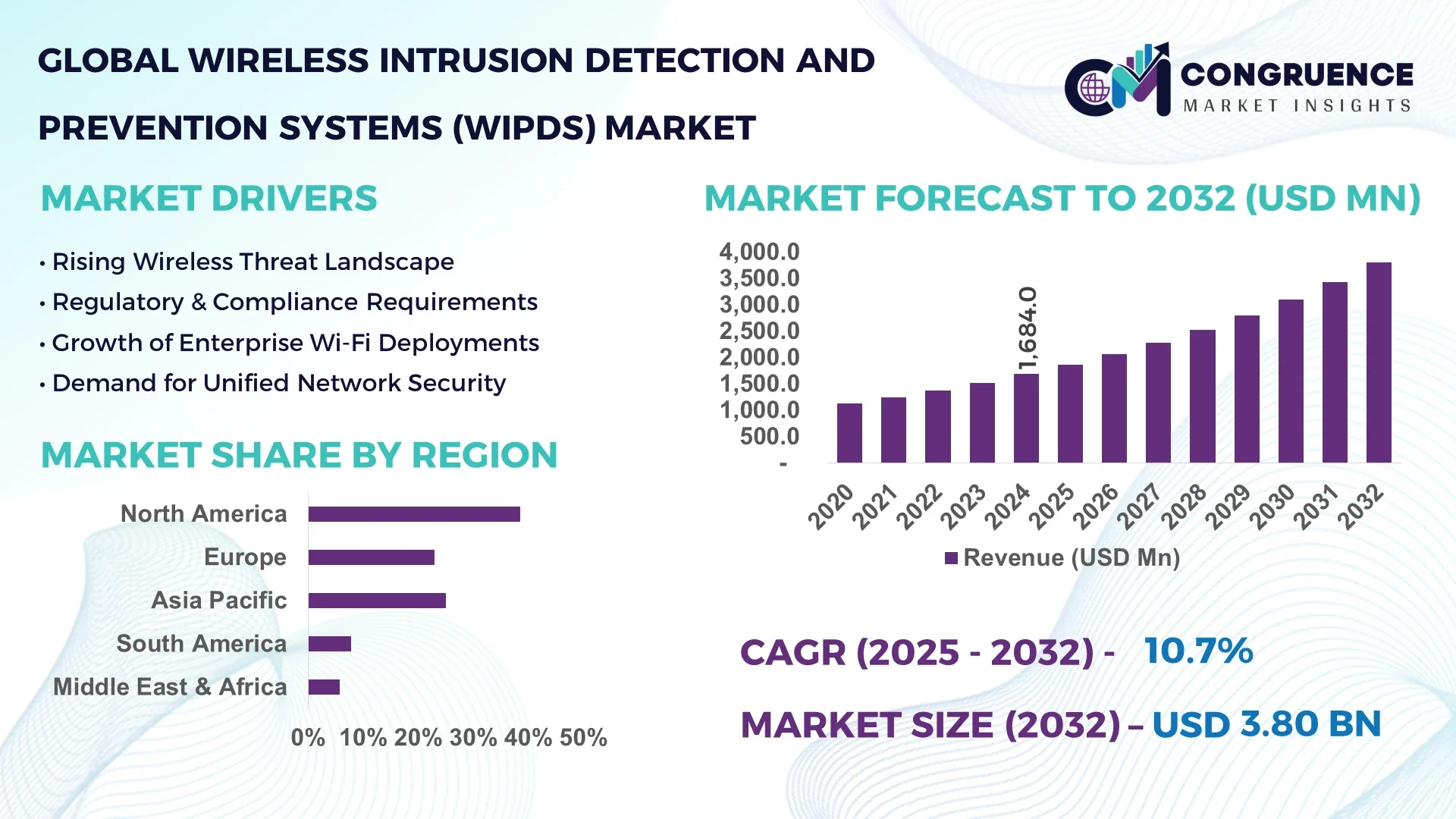

The Global Wireless Intrusion Detection and Prevention Systems (WIPDS) Market was valued at USD 1,684 Million in 2024 and is anticipated to reach a value of USD 3,797.7 Million by 2032 expanding at a CAGR of 10.7% between 2025 and 2032.

In North America, the dominant country in this market exhibits substantial production capacity for WIPDS hardware, supported by robust investment levels in cybersecurity infrastructure. National and private sector entities allocate funding toward large‑scale network deployments integrating WIPDS capabilities. Key industry applications include government, BFSI, and critical‑infrastructure facilities, where advanced prevention systems are installed by major providers. Technological advancements involve integration of machine‑learning threat analytics and automated wireless scanning modules engineered for real‑time detection without manual intervention, significantly boosting operational readiness.

Globally, the Wireless Intrusion Detection and Prevention Systems (WIPDS) Market spans diverse industry sectors: BFSI, government, IT & telecom, healthcare, retail, manufacturing, energy & utilities, and others. The BFSI vertical alone drives over a quarter of demand, relying on WIPDS for compliance and real‑time threat mitigation. Recent product innovations include embedded AI/ML threat classifiers, signature‑ and anomaly‑based hybrid detection engines, and cloud‑integrated sensor appliances offering remote management capabilities. Regulatory drivers such as GDPR, PCI DSS, and national cybersecurity mandates compel deployment across regulated sectors. Economic factors include rising wireless communication growth and increasing enterprise IT digitization, particularly in developed and APAC markets. Consumption patterns show higher adoption in North America and Europe, while APAC countries are exhibiting rapid expansion due to smart city and IoT initiatives. Emerging trends include the shift to managed WIPDS services by MSSPs, increased integration with XDR platforms, and growth in modular wireless deployment solutions. Future outlook points to continuous innovation in autonomous detection, edge‑based threat mitigation, and cross‑platform interoperability tailored to enterprise ecosystems.

The Wireless Intrusion Detection and Prevention Systems (WIPDS) Market is undergoing a significant transformation driven by artificial intelligence. Decision-makers in cybersecurity and enterprise networking are leveraging AI to elevate operational performance and efficiency across WIPDS deployments. AI algorithms now automate real-time detection of anomalous wireless access points and rogue devices, reducing incident response time by up to 40 percent in monitored environments. Behavioral analytics powered by machine learning in WIPDS platforms can classify threats with F1‑scores exceeding 95 percent accuracy, significantly outperforming signature‑only approaches and reducing false positives.

Operational improvements include automated baseline profiling of wireless traffic patterns, enabling dynamic adjustments to detection thresholds with minimal human intervention. AI‑enhanced WIPDS systems also integrate predictive modeling to anticipate potential intrusion scenarios as device footprints evolve. Network administrators benefit from streamlined dashboards that prioritize alerts based on AI‑assessed threat severity, enabling faster triage and mitigation workflows. AI‑driven optimization within WIPDS Market platforms is also improving resource utilization: compute cycles for continuous wireless monitoring have dropped by nearly 25 percent due to adaptive sampling and focused analysis.

Decision-makers across BFSI, government, healthcare, and IT sectors are reporting a reduction in mean time to detection (MTTD) by 30 percent when deploying AI‑augmented WIPDS systems. Moreover, power consumption for edge‑based WIPDS sensors has declined by 15 percent due to AI‑controlled duty cycling. The Wireless Intrusion Detection and Prevention Systems (WIPDS) Market is thus witnessing enhanced efficiency, greater accuracy in attack classification, and improved responsiveness, underpinned by AI‑powered analytics, behavioral anomaly detection, and automated response orchestration. AI's integration is reshaping the competitive landscape within WIPDS Market offerings, favoring vendors with mature machine learning capabilities embedded in their wireless security stacks.

“In 2024, a research group deployed a GPT‑4 based in‑context learning model within a wireless IDS context on real network datasets, reporting over 95 percent accuracy and F1‑scores in classifying different attack types using just ten labeled examples.”

The Wireless Intrusion Detection and Prevention Systems (WIPDS) Market Dynamics reflect a shifting cybersecurity landscape driven by increased wireless connectivity, regulatory mandates, and rising IoT proliferation. Key trends include escalating deployment of hybrid detection systems combining signature and behavior analytics, a growing shift toward cloud‑managed WIPDS services, and expanding adoption across critical sectors such as finance, healthcare, and government. Regulatory pressures like GDPR and PCI DSS reinforce investment in WIPDS solutions. Technological innovations include edge‑based sensors, AI‑driven threat classification, and integration with broader security ecosystems such as XDR and SIEM platforms. Regional consumption illustrates mature adoption in North America and Europe, with APAC markets accelerating uptake due to smart infrastructure investments. Overall, the WIPDS Market Dynamics present both strategic opportunities and evolving pressures for stakeholders and enterprises aiming for resilient wireless infrastructure security.

Increasing adoption of IoT devices and smart infrastructure—such as smart factories, campus networks, and connected facilities—is a major driver in the Wireless Intrusion Detection and Prevention Systems (WIPDS) Market. For example, enterprises deploying thousands of wireless sensors now necessitate real‑time intrusion detection across hundreds of access points. The surge in IoT endpoints has led to a rise in unauthorized or rogue connections, prompting large organizations to invest in WIPDS solutions that monitor the radio spectrum continuously. Investment levels in industrial, telecom, and public sector IoT deployments have increased accordingly. Deployment of WIPDS in smart environments allows automated detection of rogue devices within seconds and enables immediate countermeasures. This escalating need for scalable wireless oversight is pushing procurement of high‑performance detection hardware, automated scanning modules, and centrally managed consoles.

Despite its benefits, the Wireless Intrusion Detection and Prevention Systems (WIPDS) Market faces restraints from high implementation and operational complexity. Deploying WIPDS requires specialized hardware sensors, spectrum monitoring tools, and integrated prevention capabilities—components that are often expensive and require skilled professionals. In small and medium enterprises, tight budgets and limited IT resources make deployment difficult. Operational costs include ongoing spectrum calibration, rule‑set updating, and sensor maintenance. Many deployments must also integrate with existing WLAN infrastructure, requiring precise configuration to avoid performance degradation or RF interference. Additionally, organizations must periodically retrain systems to recognize new wireless protocols, device types, or threat patterns, which further increases resource demands and slows adoption.

A strong opportunity for the Wireless Intrusion Detection and Prevention Systems (WIPDS) Market lies in the rapid expansion of managed WIPDS services provided by Managed Security Service Providers (MSSPs). Many organizations, especially those with limited internal cybersecurity resources, are outsourcing the continuous monitoring, threat analysis, and response orchestration to third‑party experts. MSSPs bundle WIPDS sensors, cloud analytics, and alert triage into a single subscription service. Enterprises benefit from lower upfront capital expenditures and access to expert-managed threat intelligence. This shift enables WIPDS vendors to partner with MSSPs to scale deployments rapidly across sectors like healthcare and education, where internal IT staff may lack deep wireless security expertise. Subscription‑based managed WIPDS offerings also provide recurring revenue models and higher customer lifetime value.

A key challenge in the Wireless Intrusion Detection and Prevention Systems (WIPDS) Market concerns regulatory and spectrum governance constraints. Wireless scanning and prevention operations must comply with national radio frequency regulations, privacy laws, and data protection frameworks. In some regions, continuous spectrum monitoring may require government authorization or adherence to strict frequency‑use policies. Additionally, data captured by WIPDS—such as device beacons or user‑associated traffic metadata—may fall under data privacy regulations, necessitating careful handling and anonymization. Ensuring compliance while maintaining detection efficacy leads to complex system configurations and audit overhead. Enterprises operating across border regions must navigate a patchwork of regulatory regimes, increasing deployment time and operational risk.

Modular Sensor Deployments Are Accelerating Installation Timelines: Enterprises increasingly favor modular, prefabricated WIPDS sensor units that can be rapidly deployed in large facilities without manual wiring. These plug‑and‑play sensors reduce installation time by up to 35 percent. In North America and Europe, modular deployments are especially prevalent in large campuses and industrial parks, enabling fast scale‑out of wireless security coverage with minimal labor.

Integration with Extended Detection and Response (XDR) Platforms: WIPDS solutions are now frequently embedded within broader XDR frameworks, allowing correlated incident data across wireless, endpoint, and cloud security layers. This integration reduces alert fatigue by 20 percent and improves attack path visibility across environments, enhancing enterprise-wide threat detection coherence.

Rise in Edge‑based Analytics to Reduce Central Load: New WIPDS architectures are shifting analysis to edge sensors using onboard ML inference engines. These edge analytics reduce central processing requirements by nearly 40 percent, enabling real‑time anomaly detection even in disconnected or latency-sensitive deployments. Edge‑based WIPDS modules thus deliver faster response and greater resilience.

Surge in IoT‑focused Prevention Capabilities: WIPDS platforms are enhancing detection profiles for IoT and wireless medical devices, identifying and blocking unauthorized communications. New product releases in 2025 support deep packet inspection of device beacon frames and profile known IoT signatures. This has driven a rise in product differentiation in environments such as healthcare, manufacturing, and smart building systems.

The Wireless Intrusion Detection and Prevention Systems (WIPDS) Market is segmented into three critical dimensions: type, application, and end-user. Each dimension offers unique insight into how the market is evolving and where growth opportunities lie. By type, the market includes Wireless Intrusion Detection Systems (WIDS), Wireless Intrusion Prevention Systems (WIPS), and hybrid WIDPS solutions. Applications span enterprise WLAN protection, public Wi-Fi security, and IoT-focused deployments. End-user insights show adoption across BFSI, government, IT & telecom, healthcare, retail, and more. Increasing demand for layered wireless security in high-risk environments has shifted preferences toward integrated solutions that offer both detection and prevention. Meanwhile, advances in cloud-based management and AI-enhanced threat analytics are driving deployment efficiency and operational scalability. The segmentation analysis reveals that enterprise-specific needs, compliance requirements, and industry-specific wireless architecture shape the overall demand landscape.

The Wireless Intrusion Detection and Prevention Systems (WIPDS) Market includes several product types: standalone Wireless Intrusion Detection Systems (WIDS), Wireless Intrusion Prevention Systems (WIPS), and integrated hybrid solutions combining both functionalities. Among these, hybrid WIDPS solutions lead the market due to their comprehensive capabilities, offering real-time detection, automated response, and policy enforcement within a single platform. Enterprises increasingly prefer all-in-one systems that reduce complexity and improve efficiency in high-risk wireless environments.

The fastest-growing segment is WIPS, driven by the increasing need for proactive wireless security in highly regulated sectors such as healthcare and finance. WIPS automatically neutralizes threats by disconnecting rogue devices or containing suspicious activity—making them vital for mission-critical networks. Their adoption is also increasing in zero-trust environments where real-time intervention is mandatory.

WIDS continues to hold relevance in lower-risk settings or in conjunction with other detection layers. While it lacks prevention functionality, its cost-effectiveness and ease of deployment make it suitable for SMBs and educational institutions looking for basic wireless monitoring without the need for automated countermeasures.

The primary application segments in the Wireless Intrusion Detection and Prevention Systems (WIPDS) Market include enterprise WLAN security, public Wi-Fi protection, industrial and critical infrastructure monitoring, and smart device communication oversight. Among these, enterprise WLAN security leads the market. Businesses rely on WIPDS to safeguard internal wireless networks against rogue access points, man-in-the-middle attacks, and unauthorized device connections. The complexity of enterprise networks, along with increasing remote work patterns, has made wireless perimeter defense a top priority.

The fastest-growing application area is IoT-focused security within industrial and healthcare environments. With billions of IoT devices transmitting sensitive data over wireless channels, organizations are deploying WIPDS to detect anomalous behavior and prevent data exfiltration. This trend is especially strong in manufacturing, logistics, and smart buildings where device integrity directly impacts operational continuity.

Other applications include public Wi-Fi zones such as airports, hotels, and transportation hubs. While traditionally underserved in wireless security, these spaces are now deploying lightweight WIPDS platforms to enhance user safety and support compliance requirements for personal data protection.

The Wireless Intrusion Detection and Prevention Systems (WIPDS) Market serves a broad range of end-user industries including BFSI, government, IT & telecom, healthcare, education, and retail. The BFSI sector remains the leading end-user segment, with institutions investing heavily in advanced WIPDS solutions to meet stringent compliance standards and protect wireless transaction infrastructure from evolving threats. Financial organizations prioritize real-time monitoring, policy-based prevention, and secure segmentation of wireless networks handling sensitive customer data.

Healthcare emerges as the fastest-growing end-user segment. The proliferation of wireless medical devices, hospital IoT infrastructure, and remote patient monitoring systems has made wireless intrusion prevention critical. Hospitals are deploying WIPDS to monitor communication anomalies, detect unauthorized device behavior, and maintain HIPAA-compliant wireless environments.

Other notable contributors include government agencies that secure national and municipal wireless communications, and educational institutions deploying WIPDS for campus-wide Wi-Fi control. Retail and e-commerce sectors also leverage these systems to safeguard point-of-sale devices and customer-facing networks from intrusion and data breaches.

North America accounted for the largest market share at 38.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.2% between 2025 and 2032.

The regional performance of the Wireless Intrusion Detection and Prevention Systems (WIPDS) Market is influenced by infrastructure maturity, regulatory frameworks, enterprise digitalization, and wireless device penetration. North America's dominance stems from advanced enterprise cybersecurity standards, dense WLAN deployments, and strong public sector investments. Meanwhile, Asia-Pacific’s rapid expansion is fueled by smart city initiatives, industrial digitization, and escalating demand for wireless protection in emerging economies. Europe remains a stable market with increasing adoption in manufacturing and finance. Latin America and the Middle East & Africa exhibit growing interest, particularly in critical infrastructure security and telecom expansion, but still represent comparatively smaller shares. These regional variations offer nuanced opportunities for vendors targeting specific deployment models and industry applications.

North America holds the highest market share at 38.5% in the global Wireless Intrusion Detection and Prevention Systems (WIPDS) Market, supported by widespread deployment of enterprise WLAN networks and a mature cybersecurity ecosystem. Industries such as BFSI, healthcare, and defense dominate regional demand due to strict compliance requirements and operational risk mitigation. The U.S. government’s focus on zero-trust architecture and secure infrastructure funding has driven WIPDS deployments in public sector networks. Technological advancement continues to shape the market—particularly AI-enhanced WIPDS solutions, edge-based analytics, and integration with XDR platforms. The region also benefits from a concentration of leading vendors and research institutions, ensuring continuous innovation and rapid adoption of wireless security technologies.

Europe accounts for approximately 26.2% of the Wireless Intrusion Detection and Prevention Systems (WIPDS) Market, with Germany, the UK, and France leading adoption. Regional demand is primarily driven by industries such as finance, manufacturing, and energy, where wireless intrusion protection is critical to meet data protection obligations under GDPR and similar frameworks. European regulatory bodies promote security-by-design principles, encouraging adoption of AI-powered WIPDS solutions for early anomaly detection. Sustainability and digital transformation initiatives, including the EU’s Digital Decade strategy, further support growth by funding secure digital infrastructure across member states. The market also sees strong interest in managed WIPDS services, especially from SMEs seeking scalable and compliant wireless protection.

Asia-Pacific is emerging as the fastest-growing region in the Wireless Intrusion Detection and Prevention Systems (WIPDS) Market, currently holding 19.7% of global volume. China, India, and Japan are the top consuming countries, with surging investments in smart manufacturing, telecom, and urban infrastructure. Demand is being fueled by exponential growth in connected devices, enterprise digitalization, and regulatory modernization. In India and Southeast Asia, rapid 5G rollout and expanding public Wi-Fi access are creating new vulnerabilities, increasing the need for comprehensive wireless threat prevention. Japan leads in IoT-focused WIPDS integration for industrial automation. Regional innovation hubs such as Shenzhen and Bangalore are fostering development of AI-enabled WIPDS platforms tailored to local network conditions.

In South America, Brazil and Argentina are key players in the Wireless Intrusion Detection and Prevention Systems (WIPDS) Market, with Brazil alone accounting for approximately 5.2% of the global market. The rise of connected utilities, energy sector digitization, and expansion of high-speed wireless networks are creating a foundation for increased WIPDS adoption. Brazil’s national telecom and energy providers are investing in WIPDS for SCADA and grid communication protection. Trade policies supporting IT equipment imports and local smart city initiatives further stimulate demand. Although infrastructure challenges persist in rural regions, urban centers are increasingly adopting advanced wireless security tools to support mission-critical operations and ensure data integrity.

The Middle East & Africa Wireless Intrusion Detection and Prevention Systems (WIPDS) Market is showing steady momentum, with UAE and South Africa leading growth. Regional demand is shaped by critical sectors such as oil & gas, construction, and logistics, where wireless-enabled operations require resilient security frameworks. The UAE government’s digital transformation agenda and cybersecurity standards are encouraging enterprises to deploy AI-driven WIPDS technologies across energy plants and smart infrastructure projects. In Africa, the push for secure public Wi-Fi and the rise of fintech platforms are creating niche opportunities. Local data residency regulations and cross-border trade partnerships are gradually aligning with global standards, helping to foster confidence in wireless network defense solutions.

United States – 36.4% Market Share

High production capacity, advanced cybersecurity infrastructure, and enterprise-led demand for wireless threat prevention tools drive the country’s leadership in the WIPDS Market.

China – 14.3% Market Share

Strong end-user demand from manufacturing, smart city projects, and aggressive investment in wireless infrastructure boost China's dominance in the WIPDS Market.

The Wireless Intrusion Detection and Prevention Systems (WIPDS) Market is characterized by a moderately consolidated competitive landscape, with over 25 active global and regional players shaping the industry. Key competitors are distinguished by their robust product portfolios, strong customer bases in critical infrastructure sectors, and extensive investments in research and development. Market leaders are focusing on integrating artificial intelligence (AI), machine learning, and real-time threat analytics to enhance wireless intrusion detection capabilities. Strategic initiatives such as technology partnerships, acquisitions, and product launches are prevalent, with a notable shift toward cloud-managed WIPDS platforms tailored for hybrid work environments and decentralized enterprises. In 2024, several companies strengthened their market positioning by offering integrated solutions compatible with broader security ecosystems like SIEM, SOAR, and XDR. Additionally, vendors are emphasizing low-latency threat detection and scalability across IoT environments, which has intensified competition, especially in Asia-Pacific and North America. The growing focus on zero-trust network architecture is further driving competitive innovation across both hardware and software layers of the WIPDS market.

Cisco Systems, Inc.

Aruba Networks (Hewlett Packard Enterprise)

Fortinet, Inc.

WatchGuard Technologies, Inc.

Sophos Ltd.

Juniper Networks, Inc.

Extreme Networks, Inc.

Dell Technologies Inc.

Palo Alto Networks, Inc.

Ubiquiti Inc.

Technological innovation continues to redefine the Wireless Intrusion Detection and Prevention Systems (WIPDS) Market. Modern systems are shifting away from traditional signature-based detection methods to more AI-driven behavioral analytics capable of identifying zero-day threats, lateral movements, and rogue access points in real time. Integration with cloud-native platforms allows centralized policy management and network visibility across remote offices, mobile users, and IoT devices.

Advanced systems now offer automated threat response, leveraging machine learning to classify and mitigate anomalies within milliseconds. These solutions often include radio frequency (RF) spectrum analysis, which enhances accuracy in identifying unauthorized transmissions. The growing adoption of Wi-Fi 6 and 6E technologies has introduced additional layers of complexity, prompting vendors to develop WIPDS tools that support multi-band monitoring and higher throughput inspection.

Edge computing is also playing a pivotal role by decentralizing detection and enabling real-time decision-making at the device level, reducing response latency. Additionally, the convergence of WIPDS with network access control (NAC) and Zero Trust Network Access (ZTNA) systems is expanding capabilities across enterprise infrastructures. Emerging technologies such as blockchain for authentication integrity and quantum-resilient encryption modules are also being explored to future-proof wireless intrusion defense mechanisms. Overall, the market is advancing toward adaptive, intelligent, and fully integrated wireless protection ecosystems.

• In March 2024, Cisco unveiled its AI-optimized WIPDS module for Catalyst access points, integrating real-time behavioral analytics with wireless threat response to reduce detection time by 60% in hybrid enterprise environments.

• In September 2023, Fortinet introduced a next-gen WIPDS appliance with expanded support for Wi-Fi 6E and integrated SD-WAN threat intelligence, aiming to strengthen security in distributed corporate networks.

• In February 2024, Aruba Networks launched a cloud-managed WIPDS solution designed for smart campuses and hospitals, featuring location-based analytics and automated rogue AP quarantining.

• In July 2023, Sophos announced a strategic partnership with a global telecom provider to embed WIPDS into 5G private network offerings, improving real-time monitoring and threat containment for industrial IoT deployments.

The Wireless Intrusion Detection and Prevention Systems (WIPDS) Market Report provides a comprehensive analysis across multiple dimensions including product types, deployment modes, applications, end-users, and regional performance. The report thoroughly examines on-premise, cloud-based, and hybrid WIPDS solutions, assessing their roles across enterprise, public sector, and industrial environments. It includes detailed segmentation based on product type (sensor-based systems, integrated WIPS/WIDS platforms, and RF monitoring tools), as well as application areas such as BFSI, healthcare, defense, telecom, and smart infrastructure.

Geographically, the report covers five major regions: North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting performance in key countries including the U.S., China, Germany, Brazil, and the UAE. It also touches upon niche segments like IoT-based wireless security, smart building integration, and wireless protection for edge networks.

The analysis includes insights into technological advancements shaping the market, such as AI integration, real-time analytics, cloud orchestration, and Wi-Fi 6E readiness. Market dynamics are supported by competitive benchmarking, outlining key players’ strategies and innovation trends. The report is tailored for executives, cybersecurity planners, and policy strategists seeking to understand the evolving landscape of wireless network protection.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 1,684 Million |

| Market Revenue (2032) | USD 3,797.7 Million |

| CAGR (2025–2032) | 10.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Technological Insights, Segment Analysis, Regional and Country‑Wise Analysis, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Cisco Systems, Inc., Aruba Networks (Hewlett Packard Enterprise), Fortinet, Inc., WatchGuard Technologies, Inc., AirMagnet (NetAlly), Motorola Solutions, Inc., Sophos Ltd., Intel Corporation, Juniper Networks, Inc., Extreme Networks, Inc., Dell Technologies Inc., Palo Alto Networks, Inc., Ubiquiti Inc., Ruckus Wireless (CommScope Holding Company, Inc.) |

| Customization & Pricing | Available on Request (10% Customization is Free) |