Reports

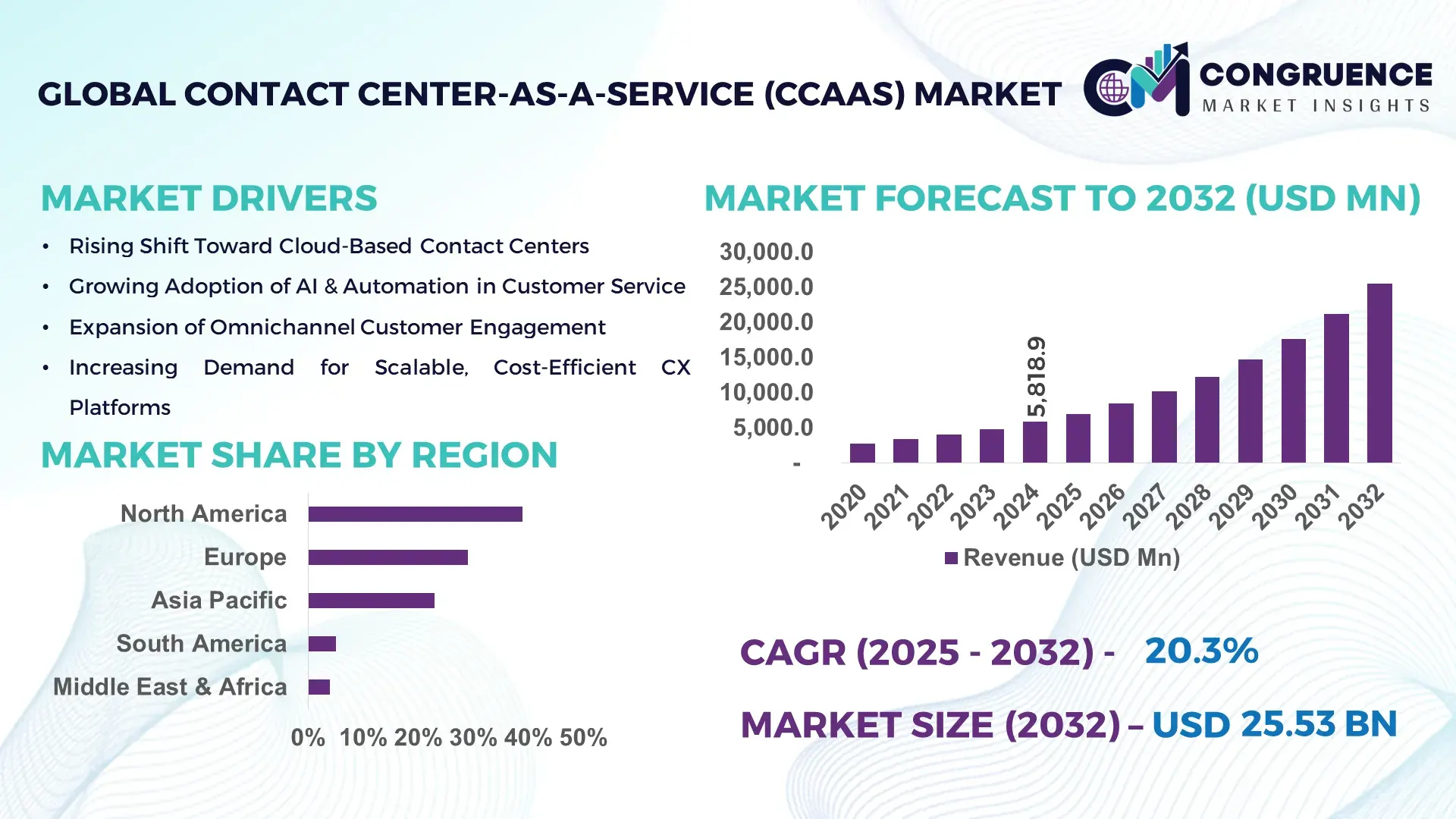

The Global Contact Center-as-a-Service (CCaaS) Market was valued at USD 5,818.9 Million in 2024 and is anticipated to reach a value of USD 25,525.0 Million by 2032 expanding at a CAGR of 20.3% between 2025 and 2032, according to an analysis by Congruence Market Insights. One key reason for this projected growth is the accelerating shift toward cloud-based customer service infrastructure as companies increasingly seek scalable, flexible, and remote-ready contact center solutions.

In the country that currently dominates the CCaaS marketplace — the United States — large-scale investment continues in cloud-native contact center infrastructure. U.S. enterprises deploy tens of thousands of CCaaS seats annually, with industry applications spanning across banking (BFSI), IT & telecom, retail, and healthcare, leveraging AI-powered analytics and omnichannel capabilities. U.S. firms report average reduction in agent onboarding time by 30–40% and support peak handling of millions of customer interactions per month, underlining both high capacity and advanced technological adoption.

Market Size & Growth: Current market value stands at USD 5.8189 billion, projected to reach USD 25.525 billion by 2032 at an expected CAGR of 20.3%, driven by growing demand for flexible, cloud-based contact center platforms.

Top Growth Drivers: ~70% enterprises migrating to cloud-native contact center solutions; ~65% improvement in operational scalability; ~60% increase in remote customer service adoption.

Short-Term Forecast (by 2028): Organizations expect a 25–30% reduction in infrastructure costs and a 20% improvement in agent productivity metrics after migrating to CCaaS.

Emerging Technologies: Integration of AI-based conversational agents, real-time analytics dashboards, and omnichannel customer engagement platforms.

Regional Leaders: North America projected at ~USD 10B by 2032 (strong enterprise adoption); Asia-Pacific ~USD 7B (rapid digital transformation in emerging economies); Europe ~USD 6.5B (steady growth in regulated markets).

Consumer/End-User Trends: Increased use of self-service chatbots, preference for omnichannel support (voice + chat + social), and demand for rapid response times across BFSI, retail, telecom, and healthcare sectors.

Pilot or Case Example: In 2025, a global telecom company implemented a CCaaS solution and reported a 22% decrease in call-handling time and 18% reduction in customer waiting time.

Competitive Landscape: Market leader holds ~30% share; major competitors include several global vendors offering cloud CCaaS solutions across sectors.

Regulatory & ESG Impact: Growing data-privacy and data-localization regulations prompting compliance-ready CCaaS deployments; increasing ESG-driven demand for energy-efficient cloud operations.

Investment & Funding Patterns: Recent venture funding rounds total over USD 500 million for CCaaS startups globally; increasing trend of long-term service contracts and subscription-based financing.

Innovation & Future Outlook: Advances in AI-powered sentiment analysis, predictive customer routing, and seamless integration with CRM/ERP systems poised to redefine customer experience and drive next-wave growth.

The market continues to evolve with rising demand across sectors, driven by digital transformation, remote work, and customer-centric service models.

In addition, the CCaaS market is seeing rapid adoption across key industries such as BFSI, IT/Telecom, retail, and healthcare, fueled by innovations like AI chatbots, omnichannel support, and real-time analytics. Economic factors like reduced operational overhead and regulatory incentives for cloud migration are encouraging regional consumption — especially in North America, Europe, and Asia-Pacific — while growing demand for personalized, scalable customer service solutions signals strong future growth potential.

The strategic relevance of the Contact Center-as-a-Service (CCaaS) Market lies in its ability to transform customer engagement infrastructure into a flexible, scalable, and cost-efficient model — essential for modern enterprises operating globally. By transitioning from on-premises systems to cloud-native CCaaS platforms, organizations can reduce upfront capital expenditure and shift to an operational-expense (OpEx) model. This transition enables quicker deployment, easier scaling during peak demand, and continuous access to software updates, resulting in measurable KPIs such as ~25–30% reduction in IT overhead and ~15–25% improvement in agent efficiency compared to legacy on-premises setups.

Emerging technologies like AI-driven conversational agents and real-time analytics deliver significant improvements. For example, AI-enabled CCaaS solutions can cut average handling time (AHT) by up to 20% compared to traditional Interactive Voice Response (IVR) systems. Regionally, North America dominates in volume due to large enterprise adoption and widespread digital infrastructure, while Asia-Pacific leads in adoption growth, with many enterprises embracing CCaaS to support rapidly expanding customer bases and multilingual support needs.

Over the next 2–3 years, AI-driven routing and predictive analytics are expected to improve first-contact resolution rates by 15–20%. In addition, because regulatory and ESG compliance is becoming critical, firms are committing to data-sovereignty and energy-efficient cloud hosting, targeting a 10–15% reduction in carbon emissions by 2030 through optimized data center utilization. In 2025, a U.S.-based multinational bank achieved a 30% reduction in customer wait times by migrating to an AI-enabled CCaaS platform — demonstrating the transformative impact of the technology.

Looking ahead, the CCaaS market stands as a pillar of resilience, compliance, and sustainable growth — offering enterprises global scalability, seamless customer engagement, and a pathway to innovation-driven operational excellence.

The Contact Center-as-a-Service (CCaaS) Market is shaped by rapid digitization, ubiquitous cloud adoption, and evolving consumer expectations for seamless, omnichannel interactions. Enterprises across sectors — including BFSI, telecom, retail, healthcare, and government — are increasingly shifting from legacy on-premises contact centers to cloud-based CCaaS platforms to benefit from flexibility, scalability, and lower maintenance overhead. The rise of remote and hybrid work models has further accelerated CCaaS uptake, enabling agents to deliver customer support from anywhere. Additionally, the proliferation of digital touchpoints (chat, social media, messaging apps) is driving demand for sophisticated CCaaS solutions capable of unifying various channels into a single platform. As a result, CCaaS is emerging as a critical enabler of customer experience, operational efficiency, and business continuity in an increasingly digital and distributed world.

Enterprises seeking scalable and cost-efficient customer service platforms are fueling the shift to CCaaS. With cloud-native CCaaS solutions, companies reduce infrastructure investment, avoid maintenance costs of on-premises systems, and gain the ability to scale agent capacity rapidly during peak demand — such as seasonal sales or product launches. This flexibility supports dynamic staffing and geographic distribution, leading to more agile operations. As digital customer interactions rise, the requirement for omnichannel support, remote agents, and real-time analytics becomes essential, making CCaaS the preferred model for modern contact centers. This growing demand across sectors is propelling market adoption globally.

A significant barrier to CCaaS adoption remains the complexity of migrating from legacy, on-premises contact center infrastructure. Many enterprises run deeply integrated CRM, ERP, and billing systems, which require careful reconfiguration, data migration, and compliance alignment when transitioning to cloud-based CCaaS. These integration challenges can delay deployment, incur additional costs, and risk service disruptions during migration. Moreover, organizations with large existing investments in traditional contact centers may prefer to delay migration due to sunk-cost concerns — particularly if ROI timelines appear long or uncertain. This inertia, combined with regulatory or data-localization constraints in some regions, slows down the pace of CCaaS adoption despite clear benefits.

The rapid growth of e-commerce, fintech, telehealth, and cloud-based SaaS services globally offers substantial opportunity for CCaaS providers. As businesses expand across geographies and serve multilingual, multicultural customer bases, demand for scalable, omnichannel, and cloud-enabled customer support rises. CCaaS platforms are well positioned to support remote contact centers, integrate AI-driven multilingual customer service, and offer analytics-driven performance optimization. Additionally, underserved markets in emerging economies present untapped potential for CCaaS adoption, especially as cloud infrastructure becomes more accessible and companies prioritize flexible service delivery over capital-intensive infrastructure.

As CCaaS platforms handle vast volumes of customer data — often including personal and sensitive information — regulatory compliance (data-localization, privacy laws, cross-border data transfer restrictions) becomes critical. Enterprises operating across multiple jurisdictions must ensure that cloud deployments comply with regional regulations like data sovereignty and GDPR-equivalent laws. These compliance requirements may necessitate localized data centers, additional security controls, and rigorous audits — increasing cost and complexity. For organizations in highly regulated sectors (e.g., healthcare, finance), these challenges can slow down CCaaS migration or limit adoption, particularly in regions with strict data-protection laws.

Rapid Migration to Cloud-Native Architectures: Over 60% of organizations are replacing legacy on-premises contact centers with cloud-native CCaaS platforms, enabling 30–40% faster deployment and improved scalability, especially for remote agent workforces.

Surge in AI-Driven Customer Engagement: Deployment of AI chatbots, real-time sentiment analysis, and automated workflows has grown by 45% in the last two years, leading to measurable improvements in response time and customer satisfaction metrics.

Omnichannel Support and Unified Communications: More than 50% of enterprises now support voice, chat, email and social media through unified CCaaS platforms, resulting in 20–25% improved first-contact resolution and streamlined customer journeys across channels.

Analytics & Workforce Optimization Adoption: Use of real-time analytics and workforce-optimization tools has increased by 35%, helping companies monitor performance across KPIs, reduce call-handling time, and increase agent utilization efficiency.

The Contact Center-as-a-Service (CCaaS) market is segmented by product type, application, and end-user, each reflecting different deployment models, use cases, and industry requirements. Type segmentation distinguishes pure cloud-native CCaaS, hybrid/cloud-plus-on-prem deployments, omnichannel AI-enabled platforms, and specialty offerings such as video-enabled or industry-vertical CCaaS. Application segmentation covers inbound customer service, outbound sales and collections, technical support, workforce optimization, and analytics/insights platforms. End-user segmentation spans BFSI, telecom, retail, healthcare, government, and third-party BPOs — each with distinct performance KPIs, compliance needs, and scalability demands. Decision-makers should evaluate segmentation through operational metrics (agent seats, AHT, FCR, concurrent sessions) and deployment constraints (data-sovereignty, latency, integration complexity). Typical adoption patterns show cloud-native and omnichannel suites concentrated in large enterprises and BPOs, while hybrid models and managed services are common among regulated and legacy IT environments. These segmentation layers drive procurement strategy, partner selection, and roadmap planning for capacity, integration, and AI investments.

Product types include cloud-native (pure SaaS) CCaaS platforms, hybrid/cloud-plus-on-prem solutions, omnichannel AI-enabled CCaaS (voice + digital + bots + analytics), video-enabled CCaaS, and industry-vertical packaged offerings. Currently, cloud-native CCaaS platforms account for approximately 42% of deployments due to their low-touch provisioning, rapid scalability, and direct subscription models. Hybrid deployments hold roughly 25%, serving organizations needing localized data control and phased migration. Omnichannel AI-enabled platforms are the fastest-growing type, with an estimated compound annual growth rate (CAGR) of ~28%, driven by investments in conversational AI, real-time analytics, and unified channel context. Remaining niche and specialty types (video-enabled, vertical packages, managed on-behalf offerings) combine for about 33% of the market, addressing specific compliance, accessibility, or vertical workflow needs.

Core applications are inbound customer service/support, outbound sales/collections, technical support & troubleshooting, proactive engagement/notifications, and analytics/workforce optimization. Inbound customer service remains the leading application, representing around 48% of use cases because it addresses the largest volume of routine customer interactions and is prioritized for CX transformation. Omnichannel engagement (integrating voice, chat, social, and bots) is rising fast and is the fastest-growing application area with an estimated CAGR of ~24%, propelled by customer preference for channel choice and the efficiency gains of AI routing and automation. Other applications (sales, back-office automation, compliance monitoring) together make up roughly 32% of deployments and are increasingly embedded within CCaaS suites as packaged workflows.

Consumer and adoption indicators include enterprise pilot activity — many organizations report piloting advanced CCaaS modules (AI routing, bot escalation) in 2023–2024 — and measurable performance improvements such as reductions in average handle time and misrouted contacts following automation rollouts.

Leading end-users include BFSI (banking, financial services & insurance), telecom & IT service providers, retail & e-commerce, healthcare, government & public sector, and third-party BPOs. BFSI currently leads with an estimated ~34% share of enterprise CCaaS seat deployments, due to high volumes of customer contacts, strict compliance needs, and sustained investment in digital channels. Healthcare is the fastest-growing end-user vertical (estimated CAGR ~27%) as telehealth, patient engagement platforms, and appointment/triage workflows push demand for secure, omnichannel contact solutions. Other sectors (retail, telecom, BPOs, public services) together represent the remaining ~36%, each contributing based on seasonal demand peaks, multilingual support needs, and outsourcing models. Adoption patterns show BPOs and large enterprises prioritizing scalability and global routing, while regulated industries emphasize data localization and secure integrations.

North America accounted for the largest market share at 39% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.7% between 2025 and 2032.

The strong 2024 dominance of North America is tied to high enterprise cloud adoption, rapid AI-based contact center integration, and early investment in omnichannel communication platforms. Europe followed with a 29% share due to strict compliance standards and sustained digital transformation initiatives, while Asia-Pacific reached 23%, supported by high-volume customer service operations across China, India, and Southeast Asia. South America and the Middle East & Africa collectively accounted for 9%, with rising cloud migration in telecom, BFSI, and retail sectors. Increasing chatbot automation rates above 60%, deployment of cloud-based IVR systems exceeding 45%, and rapid expansion of voice analytics adoption across key markets created strong demand across all regions. Additionally, global enterprise investments in customer experience (CX) technologies surpassed USD 30 billion in 2024, further strengthening CCaaS penetration worldwide.

North America held roughly 39% market share in 2024, making it the leading region for Contact Center-as-a-Service (CCaaS). The region’s market momentum is driven by high adoption among sectors such as healthcare, BFSI, retail, and government, each investing heavily in customer engagement automation and omnichannel workflows. The U.S. accounted for the majority of deployments, followed by Canada, supported by growing regulatory focus on data privacy and AI governance frameworks. Advancements like predictive call routing, sentiment analytics, NLP-powered bots, and cloud-based workforce optimization contribute to wider adoption. Local players such as Five9 continue to expand AI-driven agent assistance capabilities, strengthening competitive intensity. North American enterprises also show higher preference for digital-first service experiences, with consumer behavior shifting toward automated self-service, voice assistants, and mobile-first interactions.

Europe claimed approximately 29% of the global CCaaS market in 2024, with strong demand arising from Germany, the UK, France, and the Nordics. European companies continue to adopt CCaaS solutions driven by strict compliance requirements, including GDPR-aligned data handling and growing emphasis on sustainable IT operations. Regulatory bodies encourage transparent AI use and responsible data governance, shaping vendor deployment models. The region demonstrates increasing adoption of advanced analytics, conversational AI, and real-time monitoring tools across telecom, financial services, and public-sector applications. Local players such as Content Guru (UK) continue to expand cloud-native routing and multi-channel engagement services. Consumer behavior in Europe is heavily influenced by trust, regulatory transparency, and demand for explainable automation, prompting enterprises to invest in more secure and auditable CCaaS architectures.

Asia-Pacific represents one of the fastest-expanding CCaaS markets, accounting for 23% of global volume in 2024 and ranking as the top region in high-volume customer service outsourcing. China, India, Japan, South Korea, and Australia are the primary markets, each driving demand for cloud-native customer engagement tools. The region’s growth is supported by the expansion of e-commerce, digital payments, mobile-first communication apps, and large-scale BPO ecosystems. Infrastructure investments in data centers, 5G networks, and AI innovation hubs across India and Southeast Asia further accelerate adoption. Local companies such as Tata Communications are strengthening omnichannel platforms with AI routing and speech analytics to support enterprise CX modernization. Consumer behavior in the region favors rapid, app-based, multilingual support services, significantly boosting CCaaS platform utilization.

South America accounted for roughly 5% of the global CCaaS market in 2024, with Brazil and Argentina leading demand. The regional market is influenced by the modernization of telecom networks, strengthening retail and e-commerce sectors, and increasing investments in cloud-based customer support systems. Government digitalization incentives, data localization policies, and improved internet infrastructure support broader adoption. Energy, financial services, and media industries are emerging as key users of CCaaS solutions. Local players such as Totvs (Brazil) are enhancing AI-driven consumer service platforms, promoting regional innovation. South American users show strong preferences for localized language support, social media-based customer engagement, and rapid-response service models, making cloud-based platforms increasingly essential for enterprises.

The Middle East & Africa held approximately 4% market share in 2024, with rising adoption driven by countries such as the UAE, Saudi Arabia, South Africa, and Kenya. The region’s CCaaS growth is linked to ongoing digital economy initiatives, heavy investments in smart city programs, and rapid modernization within sectors such as oil & gas, construction, BFSI, and logistics. Cloud-based communication platforms are increasingly deployed to meet customer service modernization demands and multilingual support requirements. Local operators like Etisalat UAE are expanding AI-enabled contact center managed services to enhance enterprise communication efficiency. Consumer preferences in the region show strong demand for mobile-first support channels, personalized service experiences, and round-the-clock assistance, pushing companies toward scalable CCaaS infrastructure.

United States – 34% Market Share: Dominance supported by strong enterprise digital transformation initiatives and rapid adoption of AI-enabled cloud communication tools.

Germany – 9% Market Share: Leadership driven by high compliance-oriented adoption and strong demand from automotive, manufacturing, and BFSI sectors.

The Contact Center-as-a-Service (CCaaS) market exhibits a mix of fragmentation and emerging consolidation: there are dozens of active competitors globally (22+ prominent vendors tracked), with continuous entries from cloud, CRM, and telecom players expanding CCaaS offerings. Market positioning ranges from cloud-native pure-play CCaaS vendors to large enterprise software and cloud platform providers that bundle contact-center capabilities into broader suites. Strategic initiatives across the industry in 2023–2024 included major acquisitions, platform convergences, and deeper CRM integrations: notable moves include the close of LiveVox into a larger CX platform, converged cloud/CRM product launches, and multiple AI product rollouts and partner integrations that emphasise generative/assistive agent capabilities. Innovation trends now driving competition include memory-driven AI agent assist, unified CRM-CCaaS experiences, embedded speech and sentiment analytics, and packaged vertical workflows for regulated industries. The market is moderately fragmented but trending toward consolidation, with the combined share of the top five vendors estimated in the ~60% range, while the long tail (20–40+ smaller/platform specialists) captures remaining seat and niche vertical volumes. Vendors pursue M&A, large partner alliances, and rapid feature cadence to secure enterprise deals and seat growth.

Current and emerging technologies are reshaping CCaaS architectures and procurement criteria. First, AI & ML (including generative and memory-driven agents) are embedded into agent assist, auto-summary, real-time guidance, and customer self-service — implementations now improve average handle time and agent accuracy through real-time prompts, live summarization, and automated next-best-action suggestions. Second, deep CRM convergence is driving product roadmaps: vendors and CRMs are engineering bi-directional data flows so customer context, case histories, and predictive signals are available synchronously during interactions. Third, omniscience of channels (true omnichannel) — not just multi-channel — has become table stakes: platforms unify voice, chat, social, SMS, and app channels into a single conversation state for routing and analytics. Fourth, speech analytics, emotion/sentiment detection, and real-time quality monitoring are now standard modules; these enable near-instant compliance checks, redaction flags, and coaching triggers. Fifth, edge and regional hosting (data locality) is growing to satisfy regulatory and latency constraints; vendors increasingly offer localized data zones and hybrid deployment models to meet sovereignty and performance needs. Sixth, workforce engagement and automation — schedule optimization, AI-aided training, and robotic process automation (RPA) tie into contact flows to reduce manual wrap-up work and increase utilization. Finally, open APIs and platform extensibility are a competitive differentiator: companies favor CCaaS vendors that support low-code/no-code integrations, marketplace apps, and pre-built connectors for vertical workflows. Collectively, these technology trends are shifting procurement from purely telecom/voice considerations to platform intelligence, data governance, and extensibility — forcing vendors to prioritize continuous product delivery, partner ecosystems, and measurable operational outcomes (reduced handle time, improved FCR, agent retention gains) in RFPs.

In December 2023, NICE completed the acquisition of LiveVox, combining LiveVox’s proactive outreach and omnichannel capabilities with NICE’s CXone platform to create an interaction-centric conversational AI suite; the deal positions NICE to expand outbound automation and conversational channels. Source: www.nice.com

On June 11, 2024, NICE announced CXone Mpower, a memory-driven, CX-aware AI offering designed to enable continuous human-AI collaboration across interactions, with features for persistent context, conversation memory, and real-time agent assistance. Source: www.nice.com

On June 5, 2024, Five9 announced a deeper AI integration with Salesforce to deliver unified customer context and conversational AI enhancements across the contact center and CRM workflows, enabling synchronized customer views and AI-assisted agent experiences. Source: www.five9.com

On June 26, 2024, Talkdesk was named a Leader in the 2024 IDC MarketScape for CCaaS Applications Software, highlighting breadth of capabilities and ease-of-use for enterprise customers and reinforcing vendor momentum in AI and integrations. Source: www.talkdesk.com

This CCaaS market report covers the full lifecycle of cloud contact-center solutions and related ecosystems across product, deployment, application, vertical, and geography. Product scope includes pure SaaS CCaaS platforms, hybrid CCaaS/on-prem integrations, omnichannel offerings (voice/chat/email/social/SMS), AI/analytics modules (speech analytics, sentiment & emotion detection, real-time agent assist, automation), workforce engagement management (WEM), and complementary tools such as RPA connectors and CRM integrations. Deployment scope examines single-tenant and multi-tenant architectures, regional hosting/data-locality models, and managed-service delivery options. Application coverage spans inbound customer service, outbound outreach and campaigns, technical support, sales enablement, collections, proactive notifications, and analytics/workforce optimization. Industry verticals analysed include BFSI, healthcare, telecom & IT services, retail & e-commerce, public sector, travel & hospitality, and BPO/outsourcing providers, with distinct procurement drivers and compliance requirements described for each. Geographies include North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with regional variations in adoption patterns, data-sovereignty needs, and infrastructure maturity. The report also evaluates vendor competitive profiles, market concentration metrics, M&A and partnership activity, technology roadmaps (AI, CRM convergence, omnichannel orchestration), and buyer decision criteria such as scalability, security, extensibility, and TCO. Emerging and niche segments—such as AI-first CCaaS for multilingual/multimarket support, video-enabled customer engagement suites, and industry-packaged compliance templates—are separately discussed. Finally, the report provides pragmatic, decision-focused guidance for procurement teams: vendor shortlists by enterprise size, recommended PO/contract structures for subscription and seat pricing, migration playbooks for legacy to cloud transitions, and KPIs to measure post-deployment success (AHT, FCR, agent occupancy, and CX scores). This scope is designed to serve technology buyers, CX leaders, investors, and system integrators seeking both a strategic view and tactical execution guidance across the CCaaS landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 5,818.9 Million |

| Market Revenue (2032) | USD 25,525.0 Million |

| CAGR (2025–2032) | 20.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, End-User Behavior Analysis, Regulatory & Privacy Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Genesys, NICE, Five9, Talkdesk, Twilio, RingCentral, Cisco, 8x8, Avaya, Salesforce, Amazon Connect, Google |

| Customization & Pricing | Available on request (10% Customization Free) |