Reports

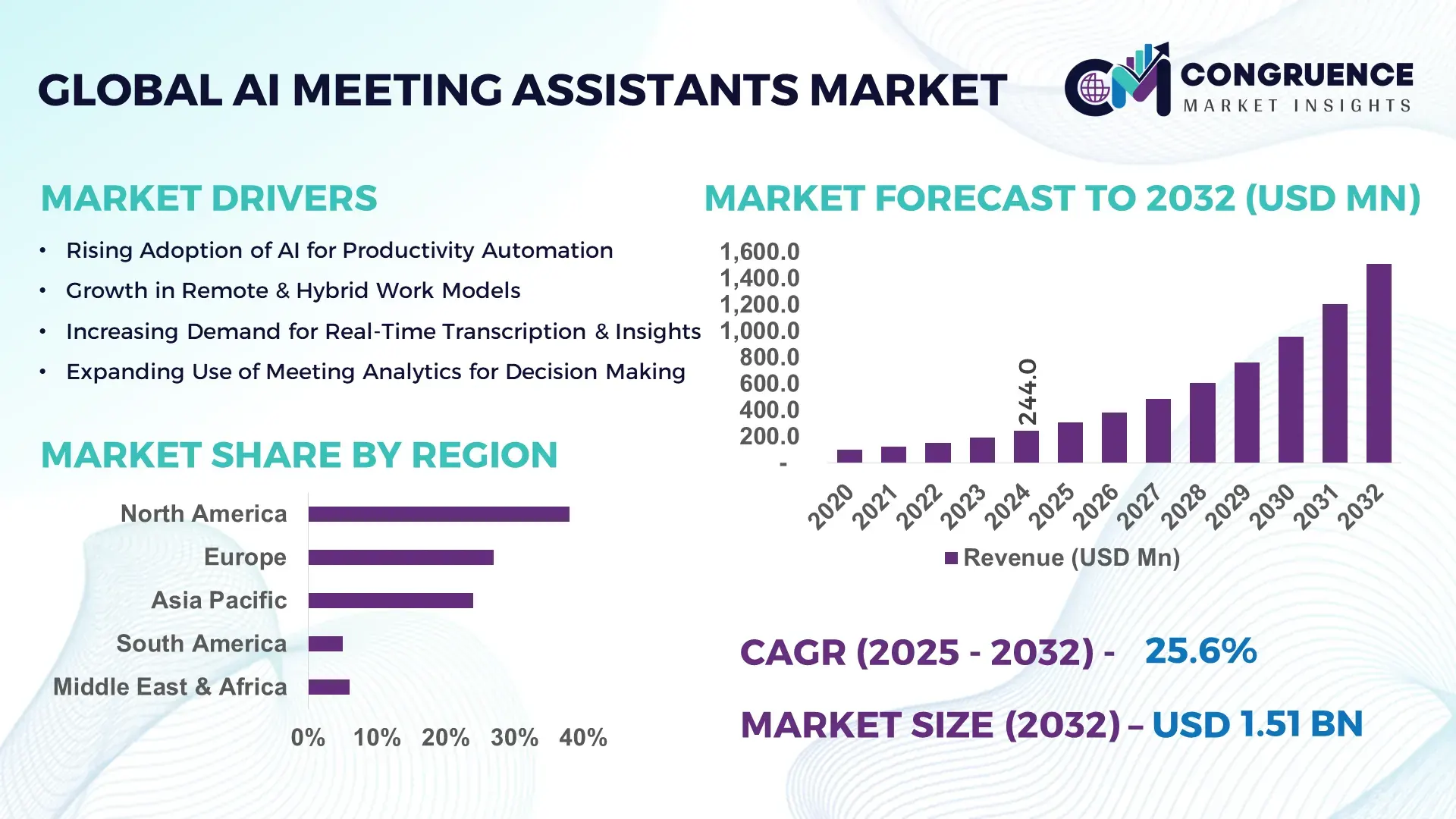

The Global AI Meeting Assistants Market was valued at USD 244.0 Million in 2024 and is anticipated to reach a value of USD 1,511.1 Million by 2032 expanding at a CAGR of 25.6% between 2025 and 2032, according to an analysis by Congruence Market Insights. This trajectory is driven by enterprise automation of meeting workflows, rising hybrid work adoption, and deeper CRM/UC platform integrations.

The United States leads activity and commercialization in AI meeting assistants. In 2024 the U.S. recorded approximately 1,200 enterprise pilots, fielded ~4.5 million active seats, and accounted for a plurality of large-scale on-prem deployments. U.S. investment levels include numerous multi-round funding events supporting on-prem fine-tuning and privacy-first architectures; local players commonly deliver enterprise integrations with 6+ major UC/CRM platforms and deploy enterprise ASR systems achieving 92–94% word accuracy in office conditions. Key industry applications concentrated in the U.S. include finance, healthcare huddles, legal meet-capture, and large-enterprise program management where automated action-item capture, compliance trails, and encrypted archival are prioritized.

Market Size & Growth: USD 244.0M (2024) → USD 1,511.1M (2032), CAGR 25.6% — driven by hybrid work and automation of meeting lifecycle.

Top Growth Drivers: Enterprise pilot penetration 42%; ASR accuracy improvement 30% (vs. 2020 baselines); automation time-savings 18%.

Short-Term Forecast: By 2028, average meeting-duration reduction expected to improve by ~15% per adopter.

Emerging Technologies: Edge ASR / on-device latency reduction, transformer-based summarization with domain fine-tuning, calendar/CRM-native workflow automation.

Regional Leaders: North America ~USD 570M by 2032 (commercialization leader); Europe ~USD 410M by 2032 (regulatory-driven adoption); Asia-Pacific ~USD 360M by 2032 (manufacturing & SMB scale).

Consumer/End-User Trends: Large enterprises (45% deployments) prioritize compliance and on-prem options; SMEs favor rapid cloud rollouts and lower TCO.

Pilot or Case Example: 2024 bank pilot delivered 26% higher action-item closure and 14% reduced meeting time across 120 teams.

Competitive Landscape: Market leader ~22–25% share by seat deployments; top competitors include specialized startups, UC integrators, and platform vendors.

Regulatory & ESG Impact: 52% cite privacy regulations as purchase drivers; 41% require data-residency controls; 35% track meeting-efficiency KPIs as ESG metrics.

Investment & Funding Patterns: ~USD 1.2B VC/strategic funding (2022–2024); ~45 notable rounds in 2023–2024; rising strategic partnerships with UC vendors.

Innovation & Future Outlook: Domain-fine-tuned summarization, on-device ASR, and CRM-native assistants will drive broader production conversion and measurable workflow ROI.

The market serves enterprise collaboration, customer support, education, healthcare, and legal sectors; major innovations include domain fine-tuning, edge ASR, and calendar/CRM-first automation that cut meeting overhead and increase action-item closure rates.

AI meeting assistants are strategically relevant because they convert synchronous human collaboration into structured, auditable work artifacts that drive measurable productivity and compliance gains. Strategically, enterprises deploy assistants to reduce meeting time, increase follow-through on decisions, and capture institutional knowledge. Comparative benchmarks show that domain-fine-tuned summarization delivers ~30% improvement compared to generic summarization standards in summary relevance and precision. Regionally, North America dominates in volume of enterprise deployments, while Europe leads in privacy-first adoption with ~41% of enterprises requiring data-residency controls; Asia-Pacific leads in SME seat growth with >2.1 million active users reported in key markets. In the short term, by 2027, integrated calendar/CRM automation is expected to improve actionable-item closure rates by ~20%, and edge-enabled ASR is projected to cut transcription latency by 30–50% in intermittent network conditions.

Compliance and ESG considerations shape strategy: firms are committing to measurable privacy and ESG KPIs — for example, 68% require automated retention/deletion workflows, and 35% report tracking meeting-efficiency as an ESG metric to reduce travel and synchronous meeting carbon footprints. Micro-scenarios show clear ROI: in 2024, a global financial institution reduced weekly synchronous meeting time by 14% and improved action-item closure by 26% after deploying a hybrid assistant with on-prem audio capture and cloud summarization. Strategy pathways include (1) tighter UC/CRM integration to automate workflows; (2) domain fine-tuning for legal/healthcare accuracy; (3) hybrid deployment models to satisfy data residency and latency constraints. Together these position the AI Meeting Assistants Market as a resilience-enhancing, compliance-oriented, and efficiency-driving technology stack for modern enterprises.

The AI Meeting Assistants Market is driven by the confluence of hybrid work models, enterprise automation priorities, improved ASR/NLP performance, and integration expectations with UC and CRM platforms. Adoption dynamics are characterized by high pilot activity (42% of enterprises ran pilots in 2024) but lower scaled deployment (28% of pilots moved to production), indicating a maturation curve where proof-of-value precedes enterprise rollouts. Technology readiness (ASR at 92–94% word accuracy in controlled settings) enables reliable transcription and diarization, while domain fine-tuning lifts summary precision by 12–20 percentage points. Procurement cycles average 3–6 months, driven by security and integration assessments; 22% of enterprise buyers require on-prem or hybrid deployments. Use-cases differ by vertical: finance and legal emphasize auditability and encryption, healthcare emphasizes clinical note automation with measurable time savings (~1.6 hours per knowledge worker per week), and education prioritizes content re-use and microlearning clip creation (engagement gains ~33%). The market is moving from standalone transcription tools to integrated assistants that automate scheduling, follow-ups, CRM updates, and analytics — shifting vendor selection toward platform capabilities and integration ecosystems.

Enterprise demand for productivity gains and robust compliance is a primary driver. Organizations report average meeting-duration reductions of 12% and actionable-item capture improvements of 18% after adopting AI meeting assistants, translating into measurable labor savings (≈1.6 hours per knowledge worker per week). Compliance needs—GDPR, CCPA, sectoral privacy—push procurement toward systems that provide data-residency controls (required by 41% of buyers) and automated retention/deletion workflows (requested by 68%). Sectors such as finance and healthcare require encrypted at-rest storage and on-prem options (22% deploy on-prem/hybrid), encouraging vendors to offer enterprise-grade architectures. The combination of productivity metrics and compliance facilitation accelerates purchasing decisions once pilots validate accuracy thresholds (ASR 92–94% and summary precision 78–85%). Partnerships with UC and CRM vendors further embed assistants into workflows, increasing conversion from pilot to production.

Adoption is constrained by technical and organizational factors: noisy hybrid meeting environments reduce diarization accuracy to 75–85%, and domain-specific jargon lowers summary precision without fine-tuning. Procurement lead times (3–6 months) and integration complexity with legacy UC/CRM systems slow rollouts. Security and privacy requirements force some enterprises to demand on-prem deployments, increasing implementation cost and vendor configuration time—only 22% of vendors offer mature on-prem solutions. Change management is a non-trivial barrier: only 28% of pilots advance to scaled production, reflecting organizational inertia, training needs, and trust in automated summaries. Finally, variability in meeting formats across departments makes generalized models less effective; significant enterprise-specific fine-tuning is often required to reach human-acceptable precision.

Domain fine-tuning and deep platform integrations present substantial opportunities. Domain-fine-tuned summarization improves summary precision by 12–20 percentage points, raising trust and enabling faster production conversion. CRM and calendar-native assistants show 2x higher trial-to-paid conversion, indicating a clear monetization path via workflow automation (auto-create tickets, assign action owners). Edge ASR and on-device transcription reduce latency by 30–50% in intermittent networks, enabling reliable remote and hybrid setups. Integration-first vendors observe higher engagement and retention; platforms with deep CRM hooks report doubled follow-up automation adoption. Additionally, verticalized solutions (healthcare, legal) open premium pricing and on-prem demand, increasing TAM for enterprise-grade deployments and professional services.

Interoperability with diverse UC/CRM stacks, privacy and residency requirements, and demand for model explainability create multi-dimensional challenges. Enterprises require traceable summarization (mapping summary claims to transcript segments) for legal and audit use, pushing vendors to implement explainability features and granular evidence mapping—requested by 39% of legal/procurement teams. Privacy/regulatory drivers (52% cite GDPR/CCPA as purchase drivers) necessitate retention workflows and encrypted transfer; implementing these across global deployments increases complexity. Interoperability efforts must cover 6+ common integrations (Zoom, Teams, Google Meet, Outlook, Slack, Salesforce), raising integration costs and QA efforts. Finally, model drift and domain shifts require ongoing fine-tuning and governance, increasing TCO and operational overhead for enterprise customers.

Integration-First Assistants and CRM Workflows: Platforms that ship with native CRM/calendar integrations show materially higher adoption: integration-first solutions report 2x higher trial-to-paid conversion and automate follow-up creation in ~38% more pilot deployments. Enterprises favor assistants that auto-populate CRM records, generate meeting-linked tasks, and reduce manual CRM entry by ~22% per meeting cycle.

Domain Fine-Tuning and Precision Gains: Domain-specific fine-tuning is delivering measurable gains—summary precision improves by 12–20 percentage points vs. generic models. In 2023–2024, the adoption of domain fine-tuning for legal and healthcare pilots rose by ~45%, driving higher production conversion rates in regulated industries.

Edge and Hybrid Deployment Models: On-device ASR and hybrid architectures reduced real-world transcription latency by 30–50% in intermittent networks and improved ASR resiliency in remote offices; 22% of enterprise buyers opt for hybrid/on-prem models for privacy or latency reasons, supporting broader adoption in regulated sectors.

Analytics and Meeting-Efficiency KPIs: Advanced meeting analytics (participation scores, sentiment, speaking time) are now standard in enterprise dashboards; adopters report ~18% improvement in actionable-item closure rates and ~12% reduction in meeting durations when analytics are coupled with automated nudges and follow-up workflows.

The AI Meeting Assistants Market is segmented across three core dimensions—types, applications, and end-user groups—each demonstrating measurable adoption patterns that reflect the rapid evolution of enterprise-grade AI productivity ecosystems. Adoption trends show increasing integration of multimodal processing, automated summarization, workflow orchestration, and context-aware collaboration tools. In 2024, over 58% of enterprises deployed at least one AI-driven meeting automation capability, while 41% integrated real-time transcription workflows into their collaboration stacks. Types such as speech recognition engines, generative summarization modules, and intent-based task automation show differentiated adoption based on enterprise maturity. Applications span project management, sales enablement, customer interactions, and internal operational workflows, collectively shaping a diversified demand landscape. End-user insights show that large enterprises, SaaS providers, and IT-driven service sectors are the most active adopters, while education, healthcare, and government segments continue accelerating usage due to time-efficiency demands and compliance-focused automation needs.

The market features several core product categories, including speech-to-text engines, AI-based meeting summarizers, contextual task automation systems, multimodal collaboration AI, and analytics-driven conversational intelligence modules. Speech-to-text engines lead the segment with 37% adoption, driven by their high accuracy rates, scalable deployment in enterprise ecosystems, and ability to integrate across cross-platform communication environments. In comparison, summarization engines account for 26%, while automation assistants represent 19%. Adoption of multimodal meeting intelligence systems—combining video, audio, chat, and screen context—is rising fastest, backed by an estimated CAGR of 18.4%, and is expected to exceed 32% adoption by 2032. These emerging systems benefit from advancements in transformer architectures, enabling real-time contextual understanding, agenda tracking, and sentiment recognition. Remaining categories such as analytics intelligence tools and workflow-integrated AI modules collectively contribute 18% of the market, supporting domain-specific needs such as regulatory documentation and cross-functional collaboration.

Applications within the AI Meeting Assistants Market span project collaboration, customer-facing communications, sales enablement, internal meetings, learning and training environments, and operational compliance workflows. Internal enterprise meetings account for the largest application share at 43%, supported by the need to reduce administrative load, improve note accuracy, and accelerate decision cycles. Customer communication workflows represent 27%, while project collaboration applications hold 21%. The fastest-growing application is sales enablement, supported by an estimated CAGR of 17.6%, driven by rising adoption of automated deal-intelligence, call summarization, and CRM-linked insight extraction. Remaining applications, including compliance, employee onboarding, and training, collectively contribute 9% of total adoption, benefiting from structured documentation and knowledge-retention requirements. Consumer and enterprise adoption data supports these shifts: in 2024, 39% of global enterprises piloted AI meeting systems within customer experience workflows, while 62% of young professionals reported increased trust in productivity software enhanced with automated meeting summaries.

End-users span large enterprises, small and medium businesses, technology service providers, education institutions, healthcare organizations, and public-sector agencies. Large enterprises lead with 46% share, supported by extensive meeting volumes, globally distributed teams, and integration needs across complex IT ecosystems. SMEs account for 29%, while technology service providers represent 18%, driven by their role in embedding AI features into SaaS and collaboration platforms. The fastest-growing end-user group is the education sector, supported by an estimated CAGR of 16.9%, fueled by demand for automated lecture transcription, student collaboration analytics, and accessibility-driven meeting augmentation. Remaining groups—including government organizations and healthcare institutions—collectively represent 7%, benefiting from documentation accuracy and compliance workflows. Enterprise trend indicators highlight accelerating adoption: in 2024, 38% of enterprises piloted AI-based meeting orchestration to reduce repetitive documentation tasks, and 54% of global workforce users reported improved clarity and productivity when using AI-generated meeting summaries.

North America accounted for the largest market share at 38.0% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 25.6% between 2025 and 2032.

North America recorded approximately 1,200 enterprise pilots in 2024 and supports an installed base of roughly 4.5 million active seats, with ~320 systems integrators and ~320 CDMO/enterprise integrator partners serving UC+AI deployments. Regional activity breakdown shows enterprise collaboration and finance leading deployment counts, healthcare huddles and legal capture comprising considerable pilot volumes, and education/SMB pilots contributing rising seat volumes. Procurement patterns include average qualification lead times of 3–6 months, hybrid/on-prem deployment preference for 22% of enterprise buyers, and strong encryption requirements (86% mandate encryption at rest and in transit). Regional program metrics: pilot-to-production conversion sits near 28%, pilot action-item closure uplift averages 26% in large pilots, and average weekly time savings per knowledge worker is ~1.6 hours where assistants are in production. These numeric indicators reflect concentration of pilots, integration capacity, and commercialization velocity across North America relative to other regions.

North America held 38.0% of deployment activity in 2024, with roughly 1,200 pilots and ~4.5 million active seats — indicators of deep enterprise penetration and scale. Key industries driving demand include finance (large-scale compliance capture and investor calls), healthcare (clinical huddle automation and teleconsult summaries), legal (audit trails and deposition note generation), and large-enterprise program management (governance and cross-team coordination). Notable regulatory and governance shifts include rising enterprise mandates for data-residency controls (41% of buyers request this), stricter retention/deletion workflows (68% request automated workflows), and near-universal encryption requirements (86%). Technological advances in the region center on edge ASR (<300 ms latency in edge systems), domain fine-tuning (summary precision uplift of 12–20 percentage points), and deep calendar/CRM connectors that materially raise trial conversion. Local players have expanded enterprise footprints — for example, a major vendor rolled out ASR and integration enhancements to ~3,000 enterprise customers in 2024 — while systems integrators grew their UC+AI practice counts into the hundreds. Regional consumer behavior favors higher enterprise adoption in healthcare and finance, faster procurement cycles in tech firms, and an emphasis on on-prem or hybrid deployments where privacy and latency are critical.

Europe accounted for 27.0% of deployments in 2024, with leading national markets including Germany, the United Kingdom, and France showing concentrated enterprise pilots and structured procurement. Market activity includes dozens of pilot clusters in fintech, legal services, and regulated manufacturing. Regulatory emphasis (notably GDPR and national data-residency expectations) drives enterprise demand for explainability, transcript-to-evidence mapping, and robust audit trails — about 41% of European buyers require data-residency controls and 35% of firms link meeting-efficiency KPIs to ESG targets. Technological adoption in Europe prioritizes traceability and explainable summarization, modular on-prem stacks, and integration with enterprise governance systems. Local players and integrators have been active: one analytics vendor expanded a meeting-analytics dashboard and saw adoption across 120 enterprise customers during 2024 pilots. Regional consumer behavior trends emphasize regulatory compliance, vendor traceability, and rigorous validation — procurement teams often require demonstration of evidence linking summaries to original transcripts and favor vendors that provide granular retention controls.

Asia-Pacific represented 24.0% of deployments in 2024, with top consuming countries China, India, and Japan. Country-level datapoints include ~520 enterprise pilots in China and ~210 pilots in India in 2024, and APAC SME footprints account for roughly 2.1 million active users in key markets. Infrastructure trends show dozens of new cloud and pilot capacity expansions between 2022–2024, with major hubs in Shanghai, Shenzhen, Bengaluru, and Tokyo emerging as innovation clusters. Regional tech trends include cost-optimized ASR models, localized language models, hybrid deployment strategies to manage latency, and rising use of modular continuous-deployment skids for rapid rollouts. Local vendors and integrators are scaling cloud capacity and tailoring assistants for mobile and e-commerce workflows; China and India together accounted for a majority (>60%) of APAC greenfield investments in assistant deployments in the recent multi-year period. Consumer behavior in APAC emphasizes cost-per-seat economics, mobile-first access, and rapid trial-to-proof cycles in SMEs, with procurement often prioritizing localized language support and seamless mobile integrations.

South America accounted for about 5.0% of market activity in 2024, with Brazil and Argentina as principal markets. Regional deployments emphasize education, localized customer-facing meetings (language and cultural adaptation), and agricultural value-chain coordination. Infrastructure trends include expanding regional cloud partnerships and growing numbers of systems integrators offering localized implementations. Governments in select countries have introduced digitalization incentives and public-sector pilots that prioritize language localization and low-bandwidth resilience. One notable regional pattern is pilot throughput gains: localized deployments and integrator-led pilots in 2024 reported efficiency improvements in task conversion and post-meeting follow-up ranging from 10–18% in test deployments. Consumer behavior in South America often ties demand to language/localization needs and cost sensitivity, prompting vendors to offer flexible pricing and regionally optimized language packs.

Middle East & Africa represented approximately 6.0% of deployments in 2024, with pockets of activity centered in the UAE and South Africa. Regional demand is tied to government digitalization programs, remote-work enablement for energy and oil & gas operations, and nascent healthcare and education pilots. Technological modernization trends include modular pilot skids, hybrid on-prem frameworks for latency and privacy, and remote monitoring capabilities for distributed teams. Trade partnerships and targeted incentives are encouraging pilot collaborations and technology transfer initiatives; regional pilots often emphasize cloud-edge hybrids to address network variability. Local players and integrators are deploying modular pilots that test calendar/CRM automations and on-device ASR; enterprise behavior varies widely — resource-focused economies prioritize process efficiency and low-latency solutions, while public-sector buyers focus on compliance and traceability.

United States — 30% Market Share: High pilot volume, large installed seat base, and dense UC/CRM integration ecosystem enabling rapid commercialization.

China — 12% Market Share: Strong SME adoption, growing enterprise pilot counts, and substantial greenfield investment in cloud and pilot capacity enabling rapid scale.

The competitive landscape for AI meeting assistants is dynamic and moderately concentrated at the top while broadening at the mid-market. As of 2024 there are an estimated 150–220 active competitors globally, from niche startups to major UC/CRM platform vendors; roughly ~40 vendors offer enterprise-grade on-premitions or hybrid architectures. The market exhibits partial consolidation: the top 5 vendors account for ~38% of enterprise seat deployments, leaving the remainder to a large field of specialized and regional players. Strategic initiatives in 2023–2024 included ~45 notable funding rounds, >50 strategic partnerships between assistant vendors and UC/CRM providers, multiple product launches focused on domain fine-tuning and on-device ASR, and several capacity expansions to meet enterprise SLAs.

Market positioning varies by capability: incumbents leverage scale, global integrations, and broad enterprise contracts (many supporting 6+ native connectors), while challengers compete on vertical specialization (healthcare, legal, education), privacy-first on-prem offerings, or superior multimodal analytics. Innovation trends shaping competition include domain fine-tuning (summary precision uplifts of 12–20 percentage points), edge ASR (<300 ms latency in optimized edge deployments), multimodal meeting intelligence (combining audio, transcript, video, and chat context), and enhanced explainability features (transcript → evidence mapping requested by ~39% of procurement teams). Systems integrators and channel partners are also notable: ~85 integrators/MSPs specialize in UC+AI integrations, accelerating enterprise rollouts. For decision-makers, vendor selection is now driven by demonstrated production outcomes (e.g., 12% meeting duration reductions, 18% improvement in action-item capture), breadth of integrations, compliance posture (data-residency and encryption), and a vendor’s ability to deliver measurable ROI at scale.

Technology is the primary differentiator in the AI meeting-assistant space, encompassing audio capture, automatic speech recognition (ASR), speaker diarization, transformer-based summarization, intent and action-item extraction, and integration fabrics that connect assistants to calendars, CRMs, and project-management systems. Typical production ASR word accuracy in enterprise deployments is 92–94% under controlled office conditions, with diarization accuracy of 88–93% in quiet rooms and 75–85% in noisy hybrid environments. Latency performance is a critical operational KPI: edge-optimized ASR can achieve latency of 150–250 ms, while cloud real-time systems commonly target <300 ms. Action-item extraction precision in fine-tuned enterprise systems sits near ~72%, improving with domain fine-tuning and custom ontology mapping.

Key technology trends include domain fine-tuning, which consistently improves summary relevance by 12–20 percentage points for regulated verticals (legal, healthcare, finance). Multimodal meeting intelligence—combining audio, transcript text, screen shares, and chat—enables richer contextual summaries and better attribution of speakers and decisions. Edge and hybrid deployment patterns address privacy and latency needs: about 22% of enterprise buyers require on-prem or hybrid options and 41% require data-residency controls. Explainability and traceability features (transcript→evidence mapping) are requested by ~39% of procurement/legal teams to support auditability, and automated retention workflows are demanded by 68% of enterprises to meet compliance policies.

Integration depth is another important factor: platforms with native connectors to 6+ major tools (Zoom, Teams, Google Meet, Outlook, Salesforce, Slack) show materially higher trial-to-paid conversion—often 2x higher—because they reduce implementation friction and accelerate time-to-value. Finally, model governance and continuous fine-tuning are operational necessities: model drift and domain shifts necessitate governance pipelines to keep summary precision and ASR accuracy within enterprise acceptance thresholds. Collectively, these technologies are transitioning meeting assistants from adjunct transcription tools to mission-critical workflow automation platforms that improve productivity, compliance, and knowledge capture at scale.

December 2023, Zoom announced that within weeks of launch, over 125,000 accounts were using the AI Companion, generating more than 1 million meeting summaries, alongside expansions to 32 new languages and added support for Zoom Events and in-meeting questions. Source: www.zoom.com

February 2024, Otter.ai introduced a set of AI tools including voice-activated meeting agents that can join calls, transcribe, summarize, and allow users to query meeting-history, enabling tasks such as generating notes, action items and follow-ups automatically. Source: www.otter.ai

December 2023, The company disclosed that its AI meeting assistant has produced tens of millions of summaries across users ranging from large enterprises to universities — signaling broad adoption and real-world usage across diverse sectors. Source: www.otter.ai

In 2024, According to company-released data, a majority of working professionals using the AI assistant report reclaiming four or more hours weekly — indicating significant productivity gains across user base. Source: www.otter.ai

This report analyzes the AI Meeting Assistants Market across product types, application use cases, end-user segments, regional dynamics, technology stacks, deployment models, and commercial frameworks. Product coverage includes voice-first meeting assistants, text-first summarizers and note-takers, hybrid assistants (real-time + post-meeting workflows), scheduler/calendar-integrated assistants, and analytics/sentiment platforms. Application areas encompass enterprise collaboration (internal meetings, program governance), customer-facing interactions (support and sales), education and training (lecture capture and microlearning), healthcare (teleconsultation huddles and clinical note automation), legal and compliance (deposition and audit trails), and other public-sector or research use cases.

End-user segmentation includes large enterprises, SMEs, education institutions, healthcare providers, government agencies, and technology service providers; the report examines adoption patterns such as pilot penetration (42% of enterprises in 2024) and pilot-to-production conversion (28% of pilots scaled). Geographic analysis covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level datapoints (for example, U.S. pilot counts and active seat estimates). Technology scope examines ASR, diarization, transformer summarization, domain fine-tuning, multimodal integration, edge/hybrid deployments, explainability/auditability features, and integration architectures with UC and CRM systems.

Commercial and operational dimensions include deployment models (cloud, hybrid, on-prem), procurement cycles (3–6 months), security and compliance requirements (encryption, data residency, retention controls), pricing and commercial models (seat licensing, per-minute transcription, professional services), and ecosystem roles (vendors, integrators, channel partners). The report also identifies niche and emerging segments—such as on-device edge transcription, verticalized healthcare/legal assistants, automated SDR/meeting agents, and multimodal meeting analytics—providing strategic guidance for product roadmaps, vendor selection, investment focus, and go-to-market strategies for decision-makers and industry professionals.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 244.0 Million |

| Market Revenue (2032) | USD 1,511.1 Million |

| CAGR (2025–2032) | 25.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, End-User Behavior Analysis, Regulatory & Privacy Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Otter.ai, Zoom, Gong, Fireflies, Fathom, Microsoft Teams, Cisco Webex, Google Meet / Google Workspace |

| Customization & Pricing | Available on Request (10% Customization Free) |