Reports

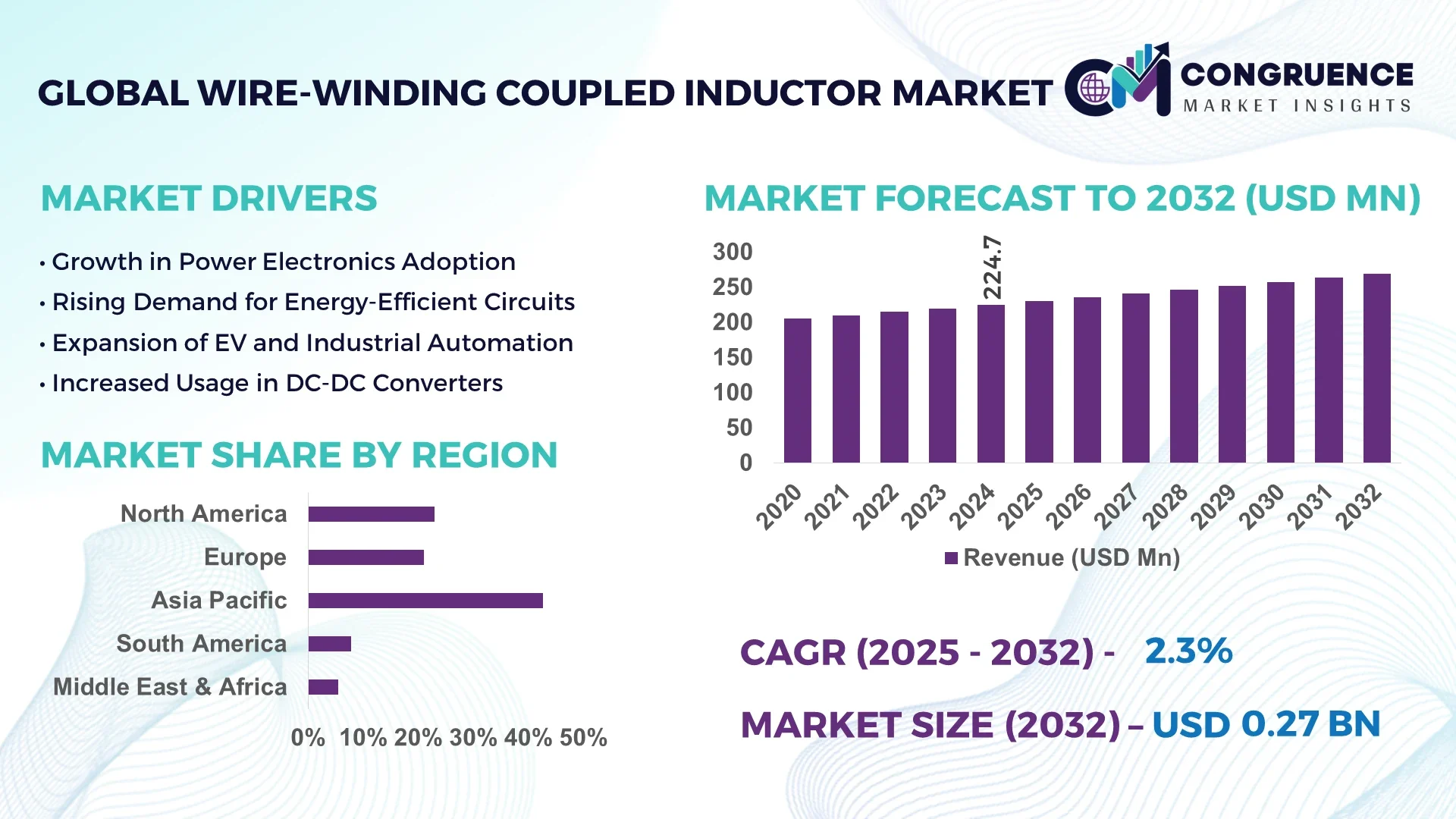

The Global Wire-winding Coupled Inductor Market was valued at USD 224.7 Million in 2024 and is anticipated to reach a value of USD 269.5 Million by 2032 expanding at a CAGR of 2.3% between 2025 and 2032.

China, a dominant player in this market, has significantly expanded its production capacity through strategic automation upgrades. With multi-million-dollar investments in advanced winding machinery, the country excels in producing high-density inductors for electric vehicle (EV) powertrains, telecom base stations, and renewable energy inverters. China’s technological progress is backed by deep R&D capabilities and strong industrial integration across its electronics manufacturing ecosystem.

The Wire-winding Coupled Inductor Market continues to evolve across critical applications such as automotive electronics, industrial power modules, smart consumer devices, and telecom infrastructure. Automotive manufacturers are increasingly integrating high-efficiency inductors into hybrid and electric drivetrains for improved DC-DC conversion. In industrial automation, wire-wound coupled inductors enable better thermal stability in power-intensive processes. Recent advancements include the adoption of high-frequency core materials, improved electromagnetic shielding, and compact multi-phase designs. Regulatory push for RoHS-compliant, energy-efficient electronics has also accelerated the adoption of innovative winding methods. Regionally, Asia-Pacific leads consumption with rapid electronics manufacturing, followed by Europe where green energy initiatives are influencing demand. Notably, future market growth is expected to benefit from the rise of miniaturized wearable electronics, solid-state power control systems, and AI-integrated energy distribution technologies.

Artificial Intelligence is profoundly transforming the Wire-winding Coupled Inductor Market by enhancing efficiency, quality control, and customized product design. AI-driven systems have been integrated into high-precision winding equipment, enabling real-time monitoring of tension, coil alignment, and thermal properties. These intelligent platforms reduce manual intervention and improve consistency in manufacturing, particularly in large-scale production environments where component precision directly impacts final product reliability.

Within the Wire-winding Coupled Inductor Market, AI also accelerates design innovation. Manufacturers now utilize AI algorithms to simulate and test multiple winding topologies, core geometries, and magnetic field interactions before physical prototyping begins. This reduces product development time while improving design optimization for specific end-use applications such as EVs, 5G infrastructure, and industrial robotics. Additionally, predictive maintenance supported by AI analytics helps identify potential equipment faults in winding machines, reducing downtime and saving operational costs.

AI’s ability to process vast sensor data during inductor production ensures stringent compliance with safety and performance standards. In quality assurance, AI-enabled machine vision systems detect micro-defects and dimensional inconsistencies with 98% accuracy, far surpassing human inspection capabilities. These advances are critical for meeting evolving demands for compact, high-power inductors used in next-generation electronic devices. As a result, AI continues to serve as a vital enabler of innovation, scalability, and cost-efficiency in the Wire-winding Coupled Inductor Market.

“In 2024, a precision electronics company in Germany implemented AI-guided winding analytics across its production line, reducing coil alignment errors by 22% and increasing throughput for high-frequency wire-wound coupled inductors used in industrial power converters.”

The increasing adoption of advanced driver-assistance systems (ADAS), electric vehicle platforms, and energy-efficient industrial automation is driving significant demand for wire-winding coupled inductors. These inductors are integral in powertrain inverters, onboard chargers, DC-DC converters, and battery management systems. For example, with global electric vehicle production surpassing 10 million units in 2024, OEMs are requiring compact magnetic components that meet both performance and size constraints. In industrial settings, wire-wound coupled inductors improve system reliability in variable frequency drives and motor control units by ensuring efficient power transfer with minimal losses. This broad application spectrum across automotive and heavy machinery is fueling consistent demand, encouraging manufacturers to scale production and innovate toward multi-phase and high-current variants.

The Wire-winding Coupled Inductor Market faces considerable pressure from volatile raw material pricing, especially for copper, ferrite cores, and high-permeability alloys. These materials are essential for maintaining inductance, efficiency, and EMI shielding. However, geopolitical uncertainties, mining restrictions, and supply chain disruptions often lead to inconsistent availability and unpredictable pricing. For instance, copper prices experienced over 18% fluctuation between Q1 and Q4 of 2024, affecting manufacturing costs for magnetic component producers. Such instability challenges procurement planning, especially for small to medium enterprises that lack long-term material sourcing contracts. Furthermore, reliance on rare earth elements for specific applications adds to supply constraints, limiting the ability of producers to scale efficiently or introduce cost-effective products.

The global transition toward decarbonized energy and grid modernization presents a major opportunity for the Wire-winding Coupled Inductor Market. Coupled inductors are key components in solar inverters, wind turbine converters, energy storage systems, and power factor correction units. As countries expand solar and wind capacity—evidenced by over 450 GW of new installations globally in 2024—efficient energy conversion becomes critical. Wire-wound coupled inductors offer high-frequency stability and energy loss reduction, making them ideal for use in high-efficiency converters and smart grid transformers. Moreover, the demand for resilient, long-life components in outdoor and high-voltage environments is driving innovation in weatherproof and thermally optimized inductor designs. This shift supports increased R&D investment and strategic partnerships aimed at enhancing performance and sustainability.

Manufacturers in the Wire-winding Coupled Inductor Market face mounting challenges due to complex international regulatory standards, including environmental mandates like RoHS, REACH, and UL certifications. Ensuring compliance often requires redesigning products, requalifying materials, and undergoing costly validation procedures. Moreover, the need for ultra-compact designs—especially in consumer electronics and EV applications—creates engineering constraints. Designers must balance inductance, current ratings, and heat dissipation within ever-smaller physical footprints. This is particularly challenging as high-frequency applications demand tighter tolerances and lower EMI emissions. Such engineering complexity increases development timelines and costs, especially for customized solutions. These limitations hinder rapid scalability and pose significant entry barriers for new or smaller market participants.

Increasing Adoption of High-Frequency Inductors in 5G Infrastructure: With the global rollout of 5G networks, the need for compact, high-frequency passive components has surged. Wire-winding coupled inductors are being integrated into RF modules and power amplifiers due to their low signal distortion and excellent magnetic coupling. In 2024 alone, over 200,000 units of compact wire-wound inductors were deployed in newly commissioned telecom towers across Asia-Pacific. Their stable inductance across wide frequency ranges makes them critical in next-gen communication systems.

Growth in Miniaturized Inductors for Wearable and IoT Devices: Consumer demand for wearable technology and ultra-compact IoT sensors is reshaping design standards. Miniaturized wire-wound coupled inductors, measuring less than 2mm in height, are gaining traction due to their space efficiency and low DC resistance. In Japan and South Korea, manufacturers have developed over 50 new miniature models optimized for smartwatches and medical wearables, enhancing battery life and system stability in portable devices.

Emergence of Multi-phase and High-current Inductors in EV Platforms: Electric vehicle architecture is demanding power components that can handle higher currents without overheating. Wire-winding coupled inductors rated above 30A are now used in multi-phase converters and charging systems. In 2024, nearly 25% of new EV powertrains utilized high-current coupled inductors with advanced ferrite cores, enabling efficient voltage transformation and reduced EMI in dense electronic assemblies.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Wire-winding Coupled Inductor market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical. As power modules for HVAC, elevators, and lighting systems in modular buildings become more integrated, wire-wound coupled inductors are increasingly tailored for compact power distribution boards.

The Wire-winding Coupled Inductor Market is segmented based on type, application, and end-user verticals, each exhibiting distinct growth dynamics and industrial relevance. By type, the market encompasses standard inductors, high-current inductors, and miniature precision types, catering to diverse design requirements. Applications span from automotive electronics and telecom equipment to renewable energy converters and industrial machinery. Among end-users, automotive manufacturers, telecom providers, industrial automation firms, and consumer electronics producers represent the key buyers. The segmentation highlights how evolving power demands, device miniaturization, and energy efficiency goals are driving adoption patterns. Regional variations also influence demand, with Asia-Pacific showing high preference for miniature types, while North America prioritizes heavy-duty inductors for EV and industrial sectors. The market’s structure is defined by a combination of mass-production efficiency, customization capabilities, and emerging niche applications such as wearable devices and grid-tied storage systems.

Wire-winding coupled inductors are classified into high-current inductors, miniature inductors, precision-wound inductors, and shielded/unshielded variants. Among these, high-current inductors lead in market volume due to their wide adoption in electric vehicle drivetrains, industrial power converters, and energy storage systems. These components are designed to handle currents above 20A without saturation, making them vital in high-efficiency applications. The fastest-growing type is the miniature wire-wound inductor, particularly used in consumer electronics and medical devices. Their compact size and high thermal performance support growing demand in smartwatches, hearing aids, and compact IoT modules. Precision-wound inductors serve niche demands in aerospace, defense, and RF applications, offering exacting tolerances and EMI control. Meanwhile, shielded inductors are gaining relevance in noise-sensitive environments such as server rooms and 5G routers. These segmentation trends show a clear shift toward application-specific optimization rather than general-purpose design, as industries prioritize tailored performance attributes.

Wire-winding coupled inductors are applied in automotive systems, consumer electronics, telecommunications infrastructure, industrial automation, and renewable energy systems. Among these, automotive systems are the leading application area, driven by the surge in electric and hybrid vehicle production. Coupled inductors are used in DC-DC converters, onboard chargers, and inverter circuits to ensure reliable voltage control and EMI mitigation. The fastest-growing application is telecommunications, fueled by the global expansion of 5G and data center infrastructure. Inductors in this sector must handle high frequencies and maintain performance stability across temperature variations, making wire-wound coupled inductors ideal for power amplifiers and signal conditioning. Consumer electronics remain a stronghold for miniature inductors, particularly in smartphones, tablets, and wearable devices. Industrial automation demands rugged inductors for use in high-load machinery and robotics, while renewable energy systems integrate them into converters and inverters, enabling optimized energy transmission from solar and wind inputs.

Key end-user segments in the Wire-winding Coupled Inductor Market include automotive manufacturers, telecommunication service providers, industrial equipment producers, and consumer electronics companies. The automotive sector remains the dominant end-user, especially with EV platforms requiring robust, high-efficiency power delivery systems. Coupled inductors ensure current regulation, battery safety, and interference-free signal management in these vehicles. The fastest-growing end-user segment is the telecommunications industry, particularly with the accelerated 5G rollout. Equipment providers are integrating advanced inductors into signal distribution systems and power conditioning units to maintain network stability in high-traffic zones. Industrial equipment producers leverage wire-wound coupled inductors in motor controllers, drives, and automation platforms. This segment values inductors with long operational life and thermal resilience. Meanwhile, consumer electronics firms continue to demand ultra-compact, high-frequency inductors to power next-gen smart devices. As IoT and connected devices proliferate, even smaller brands are investing in custom inductor designs, expanding market participation across all regions.

Asia-Pacific accounted for the largest market share at 42.7% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 3.1% between 2025 and 2032.

The Asia-Pacific region led the global demand, driven by robust consumer electronics production in China, expanding EV infrastructure in Japan, and aggressive industrial automation in South Korea. The region's manufacturing efficiency and established component supplier ecosystem further bolster its dominance. Simultaneously, North America is experiencing rapid digital transformation in automotive and aerospace sectors, increasing the demand for high-performance wire-winding coupled inductors.

The global Wire-winding Coupled Inductor Market is experiencing region-specific surges, dictated by local industrial growth and emerging technologies. In Europe, sustainability initiatives and energy-efficient power systems are reshaping the market. Latin America and the Middle East are witnessing increased adoption due to expanding grid modernization projects and manufacturing localization strategies. Across all regions, digitalization, the proliferation of connected devices, and demand for smaller, thermally resilient components are acting as primary catalysts. Market players are also aligning with regional environmental standards and industry-specific power demands, shaping future innovations in design, core materials, and magnetic coupling efficiency.

Accelerated Innovation in Power Systems and High-Frequency Applications

North America held a substantial 24.6% share of the global Wire-winding Coupled Inductor Market in 2024, supported by a strong concentration of automotive, aerospace, and data center industries. The region’s growing reliance on electric vehicles and 5G infrastructure has spurred demand for high-current inductors and RF-compatible components. The U.S. government has increased investments in domestic electronics manufacturing under CHIPS Act provisions, enhancing localized production capacities. Notably, digital design and AI-based simulation tools are being widely adopted by OEMs to optimize performance and minimize electromagnetic interference. Canada’s regulatory stance on clean energy has also promoted the use of inductors in solar inverters and storage systems.

Green Energy Transition Boosts Inductor Demand Across Core Sectors

Europe captured approximately 21.2% of the Wire-winding Coupled Inductor Market in 2024, with Germany, the UK, and France accounting for the majority of this share. Regional emphasis on sustainability has driven integration of energy-efficient components into industrial equipment and renewable energy systems. Germany’s push for Industrie 4.0 has significantly influenced automation and smart factory implementations, where wire-wound coupled inductors play a key role in motor drives and controllers. The European Commission’s RoHS compliance directives have also impacted material selection and design formats, prompting innovation in eco-friendly magnetic cores. Technological advancements in high-frequency inductors are further enabling compatibility with next-gen smart grids.

Surging Electronics Production and EV Investment Drive Market Expansion

Asia-Pacific leads the Wire-winding Coupled Inductor Market by volume, driven by strong demand from China, Japan, and India. China remains the manufacturing hub, contributing significantly to global exports of passive components including inductors. Japan’s electronics giants are heavily investing in compact, high-frequency inductors suitable for EVs and smart home devices. India is witnessing increasing adoption of industrial automation and localized electronics production under initiatives like “Make in India.” Emerging tech clusters in South Korea and Taiwan are spearheading R&D in miniaturized inductors for wearables and IoT. The region benefits from cost-effective production, strategic supply chain networks, and government-backed semiconductor incentives.

Industrial Electrification and Smart Grid Projects Propel Demand

Brazil and Argentina are leading countries in the South American Wire-winding Coupled Inductor Market, with the region accounting for approximately 5.6% of global market share in 2024. Brazil's industrial shift toward electrification and automation is a key contributor to component demand. Coupled inductors are increasingly integrated into motor drives, converters, and backup power systems across the manufacturing sector. Additionally, smart grid infrastructure projects initiated by public utilities are generating demand for energy-efficient inductive components. Favorable trade policies and regional manufacturing subsidies have enabled gradual expansion of localized component assembly. Argentina's growing renewable energy footprint is also supporting the adoption of compact inductor modules.

Power System Modernization and Electrification Programs Fuel Growth

The Middle East & Africa region is emerging in the Wire-winding Coupled Inductor Market with a regional share of 6.4% in 2024. The UAE and South Africa are at the forefront, focusing on modernizing power infrastructure and expanding industrial capacities. Coupled inductors are in demand for use in HVAC systems, solar inverters, and data center power modules. The Gulf region’s increasing investment in digital infrastructure and automation under Vision 2030 initiatives is creating fertile ground for high-frequency, thermally stable inductors. Local regulations favor energy-efficient electronic systems, accelerating the adoption of advanced inductor designs. Trade agreements with Asia-Pacific nations are also enhancing component availability.

China – 31.8% market share

Dominance is attributed to large-scale production capacity and an integrated supply chain ecosystem serving global OEMs.

United States – 18.4% market share

Strong end-user demand from electric vehicles, aerospace, and telecommunications fuels consistent component innovation and deployment.

The Wire-winding Coupled Inductor market is characterized by moderate to high competition, with over 50 active manufacturers and component suppliers operating globally. Market participants range from established electronics giants to specialized passive component producers. Competitive dynamics are shaped by innovation in magnetic core materials, miniaturization technology, and design for high-frequency, high-current applications. Several companies are focusing on product line diversification to meet the demand for inductors suited for electric vehicles, renewable energy systems, and compact IoT devices. Strategic initiatives such as cross-border joint ventures, patent filings in the high-density winding domain, and regional expansion into emerging markets are influencing the current landscape.

Key players are also investing in automation and precision manufacturing technologies to improve efficiency, consistency, and customization. Product innovation continues to be a major competitive lever, especially in segments like low-leakage inductors and thermally stable components for harsh environments. Additionally, collaboration with semiconductor and power electronics firms is becoming a trend, enhancing design integration and value-added services across multiple application verticals.

TDK Corporation

Murata Manufacturing Co., Ltd.

Bourns, Inc.

Vishay Intertechnology, Inc.

Taiyo Yuden Co., Ltd.

Würth Elektronik GmbH & Co. KG

Pulse Electronics

ICE Components, Inc.

Chilisin Electronics Corp.

Sumida Corporation

The Wire-winding Coupled Inductor Market is evolving rapidly, driven by innovation in magnetic materials and precision winding techniques. Manufacturers are increasingly using advanced core composites such as high-permeability ferrites and metal alloys, which offer superior thermal stability and magnetic efficiency. These technologies are especially suited for demanding applications in automotive power electronics, industrial drives, and renewable energy inverters. For instance, new ferrite-cored coupled inductors now operate effectively across temperature ranges of –40 °C to 125 °C with inductance values spanning from 0.5 µH to 1000 µH. In terms of structure, flat-wire and foil winding designs are gaining popularity due to their ability to minimize AC resistance and reduce eddy-current losses at high frequencies. These winding types enable higher power densities and smaller form factors, aligning with the compact design requirements of modern DC-DC converters and power supply modules.

Automated hairpin winding systems are also emerging as a key advancement, especially within automotive and industrial manufacturing sectors. These systems use pre-formed conductors to increase winding precision, reduce production time, and improve consistency. Such improvements contribute to reduced failure rates and enhanced scalability for mass production. Additionally, innovation in multi-winding coupled inductors is enabling the development of high-gain DC-DC converter architectures. These are being applied in microgrids and smart energy storage systems, where efficient voltage conversion is critical. The growing integration of these inductors into smart electronics, EV platforms, and high-efficiency power systems is expected to remain a central technological trend over the coming years.

In October 2023, TDK introduced the ERUC23 SMT flat-wire coupled inductors, featuring low-loss ferrite cores, high saturation current handling, and compact self-leaded design optimized for miniaturized electronics in automotive and telecom.

In April 2024, Central Technologies unveiled a new SMD shielded coupled inductor series designed for high-frequency performance, with enhanced EMI suppression features tailored for use in EV electronics and industrial power systems.

In December 2024, an academic consortium developed a three-winding coupled inductor-based ultra-high-voltage DC-DC converter, demonstrating a 200W prototype capable of stepping 25V input to 400V output with reduced current ripple and higher efficiency.

In June 2024, Mouser Electronics launched the IFCL line of ferrite coupled power inductors covering a range from 0.5 µH to 1000 µH, engineered for industrial, automotive, and renewable energy systems operating under wide thermal conditions.

The Wire-winding Coupled Inductor Market Report provides a comprehensive and data-driven analysis of the industry across multiple dimensions, offering strategic insights for manufacturers, investors, engineers, and decision-makers. The study evaluates a wide array of product types, including toroidal, multilayer, and SMD coupled inductors, each contributing uniquely to high-frequency, high-efficiency circuit designs used across diverse end-use verticals. This report examines key application areas such as power conversion modules, DC-DC converters, filters, inverters, and advanced energy systems. These components are becoming increasingly critical in the automotive sector, industrial automation, telecom base stations, and renewable energy infrastructure. With advancements in semiconductor miniaturization and high-efficiency power supplies, the demand for compact, thermally stable, and low-loss inductors is rising across both developed and emerging markets.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It captures distinct consumption patterns, technological adoption rates, and manufacturing trends across major countries like the U.S., China, Germany, India, and Brazil. Special attention is also given to niche markets in electric vehicles, battery storage systems, and smart grids. In terms of technology, the study includes insights into innovations in ferrite cores, flat-wire winding, high-temperature tolerance materials, automated winding systems, and integrated magnetics. The report also assesses regulatory frameworks, environmental compliance standards, and evolving design protocols influencing product development and deployment strategies. This makes the report a critical tool for understanding the full landscape and future trajectory of the wire-winding coupled inductor market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 224.7 Million |

|

Market Revenue in 2032 |

USD 269.5 Million |

|

CAGR (2025 - 2032) |

2.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Eaton Corporation, Zumtobel Group, ABB Ltd., Acuity Brands Lighting, Legrand, Signify N.V., NVC Lighting, Beghelli S.p.A, Mackwell, Daisalux |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |