Reports

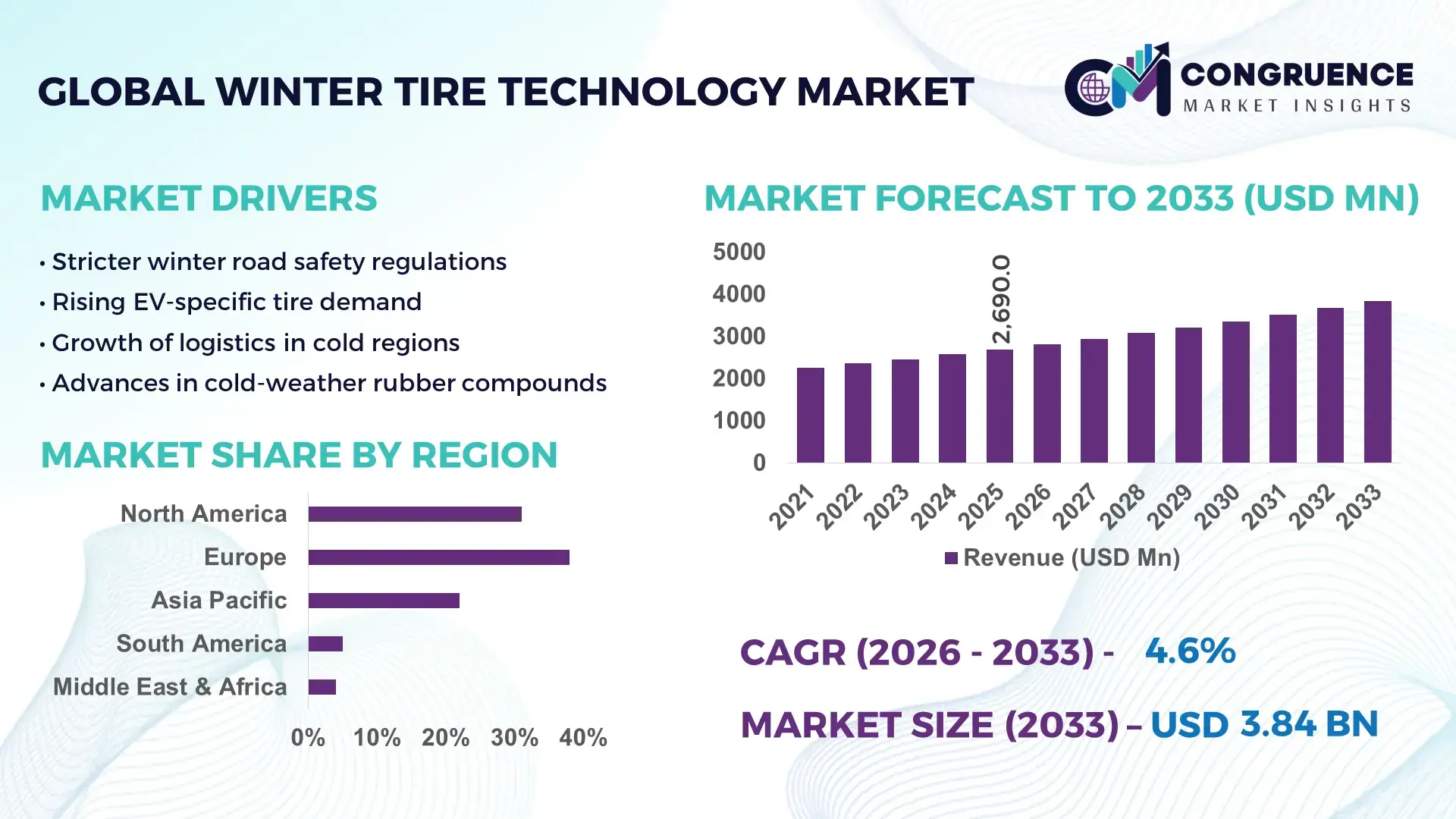

The Global Winter Tire Technology Market was valued at USD 2,690.0 Million in 2025 and is anticipated to reach a value of USD 3,840.1 Million by 2033 expanding at a CAGR of 4.55% between 2026 and 2033, according to an analysis by Congruence Market Insights. Rising adoption of advanced rubber compounding and temperature-responsive tread designs to enhance vehicle safety in cold climates is a key factor supporting market expansion.

Germany hosts one of the world’s most advanced winter tire manufacturing ecosystems, with an estimated annual production capacity exceeding 120 million tires, supported by highly automated plants in Lower Saxony, Bavaria, and North Rhine-Westphalia. German manufacturers collectively invested over USD 1.4 billion (2022–2024) in smart tire lines, cryogenic rubber testing, and AI-based tread simulation. The automotive sector—particularly premium EV and luxury ICE segments—accounts for roughly 65% of domestic demand, while commercial fleets contribute 22%. Germany operates more than 18 dedicated cold-test tracks, enabling year-round validation of ice-grip performance, and has deployed sensor-embedded winter tires in over 2.5 million vehicles for real-time traction monitoring.

Market Size & Growth: USD 2,690.0 million in 2025 to USD 3,840.1 million by 2033, driven by stricter winter safety standards and rising EV penetration.

Top Growth Drivers: 38% higher adoption in cold-climate regions; 27% improvement in ice braking via new compounds; 24% efficiency gain from automated curing.

Short-Term Forecast: By 2028, average stopping distance on ice expected to improve by 12% with next-gen siping patterns.

Emerging Technologies: Thermo-adaptive polymers, graphene-reinforced tread, and tire-embedded IoT sensors.

Regional Leaders (2033): Europe USD 1.55B (regulatory-led adoption); North America USD 1.02B (fleet demand surge); Asia-Pacific USD 0.91B (EV winter packages).

Consumer/End-User Trends: Rapid uptake among EV owners seeking low-noise winter tires and among logistics fleets prioritizing uptime.

Pilot/Case Example: In 2024, Continental’s Nordic pilot cut winter-related fleet downtime by 18% using sensorized tires.

Competitive Landscape: Michelin (~17% share); followed by Bridgestone, Continental, Goodyear, and Pirelli.

Regulatory & ESG Impact: Mandatory winter tire rules expanding across EU and Canada; rising recyclability mandates.

Investment & Funding Patterns: Over USD 620 million in recent R&D investments focused on sustainable materials and smart tires.

Innovation & Future Outlook: Integration with ADAS and predictive maintenance platforms accelerating commercialization.

Winter Tire Technology is increasingly shaped by EV-specific low-rolling-resistance designs, bio-based silica compounds, and sensor-enabled performance monitoring. Passenger vehicles account for about 58% of demand, commercial vehicles 27%, and off-road equipment 15%. Regulations in Europe and Japan mandating winter-rated tires, alongside carbon-reduction policies, are accelerating material innovation. Northern Europe and Canada show the highest per-capita usage, while China is emerging as a fast-growing manufacturing and consumption hub. Smart tires, circular recycling, and climate-adaptive compounds define the market’s future trajectory.

The Winter Tire Technology Market is strategically critical to road safety, mobility resilience, and climate-adaptive transportation systems. Governments are tightening seasonal tire mandates across Europe, Canada, and parts of the U.S., making winter tires a regulatory necessity rather than a discretionary purchase. For automakers, winter tire performance has become integral to EV certification, as battery weight amplifies braking risks on ice and snow.

From a technology benchmark perspective, graphene-reinforced tread compounds deliver ~15% better ice traction compared to conventional silica-based rubber, while reducing rolling resistance by roughly 8%, directly supporting EV range extension. Production is also becoming more digital: AI-driven curing and real-time quality analytics have cut scrap rates by 10–12% in leading plants since 2023.

Regionally, Europe dominates in volume, while North America leads in adoption with about 62% of winter-eligible vehicles using certified winter tires in high-snow states and provinces. By 2028, AI-enabled tire monitoring systems are expected to reduce winter-related fleet accidents by 20% and lower unplanned tire downtime by 14%.

On the ESG front, firms are committing to 30–40% recycled or bio-based material content by 2030, alongside 25% reductions in manufacturing emissions. In 2024, a Scandinavian logistics operator achieved a 17% fuel-saving in winter routes after deploying low-rolling-resistance winter tires with embedded sensors.

Looking ahead, the Winter Tire Technology Market will act as a pillar of safer, compliant, and climate-resilient mobility—linking advanced materials, smart data, and sustainable manufacturing into a durable growth pathway.

The Winter Tire Technology Market is shaped by evolving climate patterns, stricter safety regulations, and rapid innovation in materials science. Increasing snowfall variability has pushed automakers, fleets, and consumers toward high-performance winter tires that balance grip, durability, and energy efficiency. Electrification of vehicles has altered design priorities, as heavier batteries require stronger carcass structures and optimized tread patterns to maintain braking performance on ice.

Manufacturers are investing heavily in digital factories, automated curing, and predictive quality systems to improve consistency and reduce defects. At the same time, supply chains for natural rubber, synthetic polymers, and silica are becoming more volatile, influencing pricing and material choices. Growing public awareness of road safety, combined with government winter tire mandates in multiple regions, continues to accelerate adoption. Sustainability pressures are also reshaping product design, pushing companies toward recyclable materials, lower-carbon production, and longer-lasting tread formulations.

The rapid expansion of electric vehicles (EVs) is fundamentally reshaping the Winter Tire Technology Market. EVs are typically 20–35% heavier than comparable internal combustion vehicles due to battery packs, which increases braking distance and tire wear in icy conditions. This has forced tire manufacturers to develop reinforced winter tires with stronger sidewalls, advanced siping, and higher-density rubber compounds to maintain safety performance. Automakers are increasingly bundling winter tire packages with EV sales in cold-climate regions, accelerating demand. Many leading brands now test winter tires specifically for EV torque profiles, which can exceed 400–700 Nm, placing greater stress on tread blocks during acceleration on snow. Additionally, EV consumers prioritize low rolling resistance to preserve range, pushing innovation toward hybrid designs that balance grip with efficiency. Fleet operators deploying electric delivery vans are also adopting specialized winter tires to reduce downtime, further expanding market demand.

The Winter Tire Technology Market faces notable constraints from high replacement and maintenance costs. A full set of premium winter tires can cost 30–60% more than standard all-season tires, creating affordability barriers for price-sensitive consumers, particularly in emerging markets. Many drivers in borderline winter regions opt for all-season tires instead of investing in a dedicated winter set, limiting market penetration. Additionally, storage and seasonal tire change logistics add indirect costs, discouraging adoption among urban consumers who lack space or convenient service access. Supply chain volatility in natural rubber and specialty polymers has also increased production expenses, which manufacturers often pass on to end-users. Commercial fleets face further challenges, as frequent winter tire replacements can strain operational budgets, especially for high-mileage vehicles.

Smart tire technology represents a major growth opportunity for the Winter Tire Technology Market. Embedding sensors that monitor temperature, pressure, tread depth, and surface grip can significantly enhance winter driving safety and fleet efficiency. Pilot programs show that real-time tire analytics can reduce winter-related breakdowns by 15–20% and cut maintenance costs by 10–12%. For logistics companies, sensor-enabled winter tires allow predictive maintenance, reducing unplanned downtime and optimizing route planning in snow conditions. Insurance providers are also exploring usage-based discounts for vehicles equipped with smart winter tires, creating additional consumer incentives. As 5G and vehicle-to-everything (V2X) connectivity expand, smart tires could integrate with ADAS systems to dynamically adjust braking and traction control, further increasing adoption potential.

Volatile prices of natural rubber, synthetic elastomers, and specialty silica present a significant challenge to the Winter Tire Technology Market. Weather disruptions in major rubber-producing regions such as Southeast Asia can cause supply shortages, leading to sudden cost spikes. Over the past three years, rubber price fluctuations have exceeded 25% annually, complicating long-term manufacturing planning. Environmental regulations are also tightening chemical usage in tire production, requiring costly reformulations and compliance investments. Smaller manufacturers struggle to keep pace with these regulatory and material shifts, potentially reducing competition. Additionally, recycling infrastructure for end-of-life winter tires remains limited in many regions, creating disposal challenges and sustainability concerns that could attract stricter future regulations.

Smart sensor integration expanding rapidly: By 2025, nearly 18 million winter tires globally incorporated pressure and temperature sensors, with adoption rising 32% year-on-year in premium vehicle segments. Fleet trials show these sensors reduced roadside tire failures by 21% and cut emergency call-outs by 14% during heavy snowfall periods.

Advanced cold-adaptive rubber compounds: New cryogenic rubber blends improved ice traction by 15–18% while lowering rolling resistance by 7–9% compared with 2020-generation tires. More than 42% of new winter tire launches in 2024 used bio-silica or plant-based oils in their tread mix.

EV-optimized winter tire designs: Dedicated EV winter tires grew 28% in annual sales in 2024, featuring reinforced sidewalls that increased load capacity by 12% without adding weight. Noise reduction technologies also cut cabin tire noise by 6–10%, addressing a key EV user concern.

Circular recycling and retreading: Manufacturers expanded retread-compatible winter tires by 24% in 2023–2024, and pilot plants achieved 30% material recovery from end-of-life tires. Several European facilities now process over 1.2 million winter tires annually into recycled rubber for new tread compounds.

The Winter Tire Technology Market is segmented across type, application, and end-user, reflecting the diverse performance requirements of cold-climate mobility. By type, differentiation is driven by tread architecture, rubber chemistry, and structural reinforcement, with studded, studless, and all-weather hybrid designs serving distinct safety and regulatory needs. Application-based segmentation highlights varying performance priorities across passenger mobility, commercial logistics, and heavy-duty operations, where traction, durability, and downtime reduction are critical. End-user dynamics are shaped by regulatory mandates, fleet safety policies, and consumer behavior in snow-prone regions. Electric vehicle integration, smart tire capabilities, and sustainability considerations are increasingly influencing purchasing decisions across all segments. Overall, segmentation illustrates a market that balances safety compliance, operational efficiency, and technological innovation tailored to winter driving conditions.

Winter tires are broadly classified into studded winter tires, studless winter tires, and all-weather (winter-rated) tires, with additional niche variants such as performance winter tires and commercial-duty winter tires serving specialized needs. Studless winter tires are the leading type, accounting for ~48% of total adoption due to their ability to deliver reliable ice and snow traction without road surface damage, making them preferred in urban and highway environments where studded tires face regulatory restrictions. Their advanced silica-based compounds and multi-directional siping provide consistent grip across variable winter conditions. The fastest-growing type is studded winter tires (estimated ~6% CAGR), driven by rising use in extreme Arctic and mountainous regions, expanding mining and forestry operations, and growing adoption by rural fleets that prioritize maximum ice traction over noise or road wear concerns. All-weather winter-rated tires (approx. 32% combined share with other niche types) are gaining popularity among urban commuters who want year-round usability with moderate winter performance. Performance winter tires cater to premium vehicles and high-speed stability, while commercial-duty winter tires emphasize durability and load capacity for logistics fleets.

• In 2024, a Nordic transportation authority reported that fleets using next-generation studded tires with lightweight aluminum pins reduced winter collision incidents by 14% while cutting road wear by 9% compared with traditional steel studs.

The market serves passenger vehicles, commercial vehicles, off-road & specialty vehicles, and public transport, each requiring different winter performance attributes. Passenger vehicles dominate with ~55% share, supported by mandatory winter tire laws across much of Europe, Canada, and parts of the U.S., along with growing consumer awareness of ice-braking safety. EV-specific winter tires are becoming standard in colder regions due to higher vehicle weight and torque profiles. The fastest-growing application is commercial logistics and delivery fleets (around 7% CAGR), propelled by e-commerce expansion, 24/7 last-mile operations, and insurance incentives for sensor-equipped winter tires that reduce accidents and downtime. Off-road and specialty applications (construction, mining, forestry) collectively hold about 20% share, driven by year-round operations in cold and high-altitude environments. Public transport and municipal services account for roughly 10%, prioritizing reliability, retread compatibility, and low-noise performance. In 2025, about 41% of fleet operators in snow-prone regions reported piloting sensor-enabled winter tires for predictive maintenance. Nearly 58% of EV owners in Northern Europe indicated they would only purchase winter tires designed specifically for electric vehicles.

• In 2024, a Scandinavian city transit authority equipped 1,200 buses with low-rolling-resistance winter tires, reducing winter fuel use by 11% and improving on-time performance by 16% during heavy snowfall.

Individual consumers (retail buyers) are the leading end-user with ~50% share, reflecting strong seasonal purchasing patterns in Europe, Canada, Japan, and mountainous U.S. states. Safety regulations, insurance benefits, and dealer bundling with new vehicle sales sustain demand, particularly for EV-compatible winter tires. The fastest-growing end-user segment is commercial fleets (about 7% CAGR), fueled by logistics digitization, smart tire analytics, and rising winter delivery volumes from e-commerce. Many large fleets now require sensorized winter tires to minimize breakdowns and insurance costs. Automotive OEMs and dealerships (approx. 20% combined share) are increasingly integrating winter tire packages into vehicle sales, especially for EVs and premium cars. Government and municipal agencies (~12%) prioritize durability, retreadability, and compliance with environmental standards. Industrial users in mining, forestry, and energy (~8%) demand extreme-traction solutions for off-road winter operations. Around 39% of global logistics companies in cold regions tested smart winter tires in 2025 for real-time performance monitoring. More than 63% of Gen Z drivers in Europe prefer brands that offer eco-friendly, recyclable winter tires.

• In 2024, a German municipal fleet equipped 3,800 service vehicles with sensor-enabled winter tires, cutting winter roadside failures by 19% and lowering emergency maintenance costs by 13%.

Europe accounted for the largest market share at 38% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Europe’s dominance is supported by mandatory winter tire regulations across more than 17 countries, with winter tires fitted on over 72% of registered passenger vehicles in snow-prone areas. North America followed with a 31% share, driven by strong seasonal replacement cycles and fleet adoption in the U.S. and Canada, where over 68 million vehicles operate in certified winter zones. Asia-Pacific held a 22% share, supported by rising vehicle ownership in cold regions of China, Japan, and South Korea, while South America and Middle East & Africa collectively accounted for the remaining 9%, driven by niche alpine regions, mining activity, and cross-border trade flows. Increasing EV penetration, smart tire integration, and region-specific safety mandates continue to shape differentiated regional performance profiles.

This region accounts for approximately 31% of the global Winter Tire Technology Market, supported by high vehicle density in cold-weather states and provinces. Passenger vehicles represent nearly 57% of regional demand, while commercial fleets contribute 29%, driven by logistics, public transport, and emergency services. Regulatory frameworks in Canada mandate winter tires in provinces such as Quebec, where compliance exceeds 90% during winter months. Technological advancements include growing use of sensor-enabled winter tires, now deployed in about 34% of large logistics fleets to monitor tread wear and road grip. A leading regional manufacturer expanded EV-specific winter tire production capacity by 18% in 2024, focusing on low-noise and reinforced sidewall designs. Consumer behavior reflects higher adoption among urban drivers, with over 62% of households in northern regions owning a dedicated winter tire set.

Europe leads the global market with a 38% share, anchored by high compliance with winter tire regulations across Germany, France, Italy, Austria, and the Nordic countries. Germany alone accounts for nearly 28% of regional demand, supported by extensive automotive manufacturing and over 45 million registered vehicles. Sustainability initiatives promote low-emission and recyclable tire materials, with 41% of new winter tire models incorporating bio-based compounds. Emerging technologies such as adaptive tread patterns and AI-driven testing are widely adopted, particularly in premium vehicle segments. A major European tire producer invested in digital twin testing systems, reducing winter tire development cycles by 20%. Consumer behavior shows strong regulation-driven purchasing, with over 75% of drivers switching tires seasonally rather than relying on all-season alternatives.

Asia-Pacific holds an estimated 22% market share, ranking third globally by volume but fastest in expansion. China, Japan, and South Korea collectively contribute more than 80% of regional demand, with northern China alone accounting for over 14 million winter tire replacements annually. Manufacturing trends emphasize cost-efficient mass production and export-oriented capacity, with regional plants supplying nearly 35% of global winter tire exports. Technological innovation hubs in Japan and South Korea are advancing lightweight rubber blends and noise-reduction technologies tailored for EVs. A leading Japanese manufacturer introduced smart winter tires compatible with connected vehicle systems, now tested in over 500,000 vehicles. Consumer behavior is shifting, with 48% of new EV buyers in cold provinces opting for specialized winter tires at purchase.

South America represents approximately 5% of the global market, concentrated primarily in Argentina and Chile, where alpine and southern regions experience prolonged winter conditions. Argentina accounts for nearly 46% of regional demand, driven by passenger vehicles and mining transport fleets operating in sub-zero environments. Infrastructure projects in Patagonia and Andean corridors have increased demand for heavy-duty winter tires by 21% over three years. Trade policies supporting imports from Europe have improved access to premium winter tire technologies. A regional distributor expanded cold-weather tire distribution centers, improving seasonal availability by 30%. Consumer behavior remains selective, with winter tire usage largely limited to mountainous zones and commercial operators.

This region holds around 4% of the global Winter Tire Technology Market, largely driven by high-altitude regions, mining operations, and cross-continental logistics routes. South Africa contributes approximately 37% of regional demand, supported by mining and freight transport in colder inland areas. Turkey and parts of North Africa also generate demand through winter tourism and mountain transit corridors. Technological modernization focuses on durable tread compounds and retread-friendly designs, with 26% of commercial operators favoring heavy-duty winter tires. A regional supplier partnered with European manufacturers to introduce certified winter tires, increasing availability by 22%. Consumer behavior is predominantly commercial, with limited private adoption outside regulated zones.

Germany – 18% Market Share: Strong production capacity, strict seasonal regulations, and high passenger vehicle compliance drive sustained demand.

United States – 16% Market Share: Large vehicle parc, strong fleet adoption, and growing EV winterization requirements support market leadership.

The Winter Tire Technology Market exhibits a moderately consolidated competitive structure, with approximately 50+ active global competitors ranging from legacy tire manufacturers to specialized niche brands. The top 5 companies—Bridgestone, Michelin, Continental, Goodyear, and Nokian Tyres—collectively hold an estimated combined share of around 48–52%, underscoring significant but not overwhelming concentration in the market. Japanese multinational Bridgestone continues to assert leadership through its well-established Blizzak series and global production footprint. Michelin maintains a strong position with its X-Ice Snow and EverGrip winter tire innovations, expanded OEM contracts, and extensive R&D investments. Continental leverages its advanced engineering capabilities to integrate digital sensing and EV-compatible winter tires, with ongoing product extensions in premium SUV and passenger vehicle segments. Goodyear strengthens its competitive stance through smart tire technologies that detect rain, snow, and ice conditions to support automated braking functionality. Nokian Tyres retains a strategic edge in extreme winter climates with dedicated test facilities and a heritage of winter tire expertise.

Innovation trends in the market emphasize smart, sensor-enabled systems, adaptive compounds, and eco-centric materials, with approximately 64% of newly launched models 2023–2025 incorporating eco-silica or other performance polymers. Strategic initiatives such as OEM partnerships, digital testing platforms, and sustainability initiatives are hallmarks of high-performing competitors, guiding product differentiation and market share expansions. Overall, competitive positioning increasingly revolves around technological advancement, regional regulatory alignment, and scalable production capabilities.

Goodyear Tire & Rubber Company

Nokian Tyres plc

Hankook Tire & Technology Co. Ltd.

Sumitomo Rubber Industries, Ltd.

Pirelli & C. S.p.A

Apollo Tyres Ltd.

Toyo Tire Corporation

BFGoodrich

Yokohama Rubber Company

Kumho Tire Co., Inc.

Cooper Tire & Rubber Co.

Nexen Tire Corporation

Maxxis International GmbH

CEAT Limited

Vredestein Tyres

Emerging and current technologies are reshaping the Winter Tire Technology Market, moving beyond traditional rubber compounds and tread designs to include smart sensing, digital integration, and advanced materials engineering. A notable trend is the adoption of embedded sensor systems that provide real-time data on tire pressure, temperature, tread wear, and road surface friction. These smart technologies support predictive maintenance and integration with vehicle safety systems such as automated emergency braking (AEB), optimizing performance under real winter conditions. Sensor-enabled winter tires can detect hazardous conditions like ice and snow and communicate friction levels to the vehicle’s dynamic control systems, enhancing response accuracy even at speeds up to 80 km/h.

Advanced rubber chemistry and compound innovation play a central role in winter tire performance. New eco-friendly silica blends and bio-based polymers constitute 64% of winter tire launches between 2023 and 2025, improving grip on icy surfaces and elastic response at sub-freezing temperatures. Multiple sipe technologies and micro-structured tread blocks enhance water evacuation and traction on snow and ice, with industry development focusing on directional tread geometries for varying winter scenarios.

Electric vehicle (EV) adaptation is a significant technological vector. EV-specific winter tires are gaining traction due to the heavier mass and higher torque profiles of battery electric vehicles, demanding reinforced sidewalls and optimized low-rolling-resistance structures to maintain driving range and safety. Additionally, AI-driven tread design optimization accelerates virtual testing cycles, enabling manufacturers to simulate millions of winter driving conditions to refine traction and wear characteristics without extensive physical prototyping.

Sustainable materials and recycled components are increasingly embedded into winter tire design, with bio-based compounds and recycled steel cords reducing environmental footprints. Trends also include adaptive performance systems that could adjust stiffness and contact patch dynamics in response to temperature changes, further enhancing winter safety metrics.

Collectively, these technology advancements position tires not just as physical components but as connected, data-aware systems contributing to overall vehicle safety, energy efficiency, and regulatory compliance in cold climates.

• In January 2026, Michelin unveiled the X-Ice Snow+ winter tire designed to deliver enhanced braking performance across ice, snow, wet, and dry conditions, while offering over 26 % longer tread life and up to 34 % better fuel/EV range efficiency compared to key competitors, improving comfort with acoustic noise reduction technology ahead of the 2026 winter season. Source: www.michelinmedia.com

• In June 2025, Goodyear expanded its UltraGrip Ice 3 winter tire range with 44 new size fitments (increasing total SKUs to 106) to meet rising Nordic market demand, covering wheel sizes from 15″ to 22″ and improving handling and traction in extremely low temperatures through softer compound and Ice Handling+ features. Source: www.news.goodyear.eu

• In March 2025, Nokian Tyres commemorated 90 years of winter tire innovation, emphasizing continued safety and sustainability focus in its product development and ongoing tailored winter tire testing in Finnish Lapland environments to meet modern driver performance needs. Source: www.company.nokiantyres.com

• In March 2025, Nokian Tyres also announced the Seasonproof 2 all-season tire range, containing up to 38 % renewable and recycled materials, produced in its new zero CO₂ emission factory in Romania, marking a significant step toward the company’s goal of increasing renewable and recycled raw materials in tires to 50 % by 2030. Source: www.nokiantyres.com

The Winter Tire Technology Market Report encompasses a comprehensive landscape of product types, applications, end-users, regional markets, and technological innovations shaping the industry. It covers key winter tire types such as studded, studless, performance, and all-weather variants tailored for passenger cars, commercial vehicles, EVs, and specialty applications. The report reviews applications including urban passenger mobility, logistics fleets, public transport, and off-road operations, detailing performance needs, adoption patterns, and seasonal dynamics.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering volume-based market share insights and regional imperatives. Each region’s regulatory environment, infrastructure influences, and consumer behaviors are profiled to clarify adoption dynamics and competitive pressures. The report also delves into technological domains, such as sensor-enabled smart tires, adaptive tread design, eco-centric materials, and AI-assisted testing platforms, profiling how these innovations influence product differentiation and safety metrics under harsh winter conditions.

Emerging niche segments, such as EV-optimized winter tires and low-rolling-resistance sustainable compounds, receive dedicated analysis, including performance benchmarks in ice traction, noise reduction, and real-time monitoring capabilities. End-user insights explore adoption trends across consumer, fleet, and OEM channels, identifying usage patterns, purchase drivers, and regional variations in winter tire preferences. Overall, the scope uniquely integrates product structures, performance indicators, competitive landscapes, and future readiness metrics to support strategic decision-making for industry professionals and business leaders in the winter tire technology domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,690.0 Million |

| Market Revenue (2033) | USD 3,840.1 Million |

| CAGR (2026–2033) | 4.55% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company, Nokian Tyres plc, Hankook Tire & Technology Co. Ltd., Sumitomo Rubber Industries, Ltd., Pirelli & C. S.p.A, Apollo Tyres Ltd., Toyo Tire Corporation, BFGoodrich, Yokohama Rubber Company, Kumho Tire Co., Inc., Cooper Tire & Rubber Co., Nexen Tire Corporation, Maxxis International GmbH, CEAT Limited, Vredestein Tyres |

| Customization & Pricing | Available on Request (10% Customization Free) |