Reports

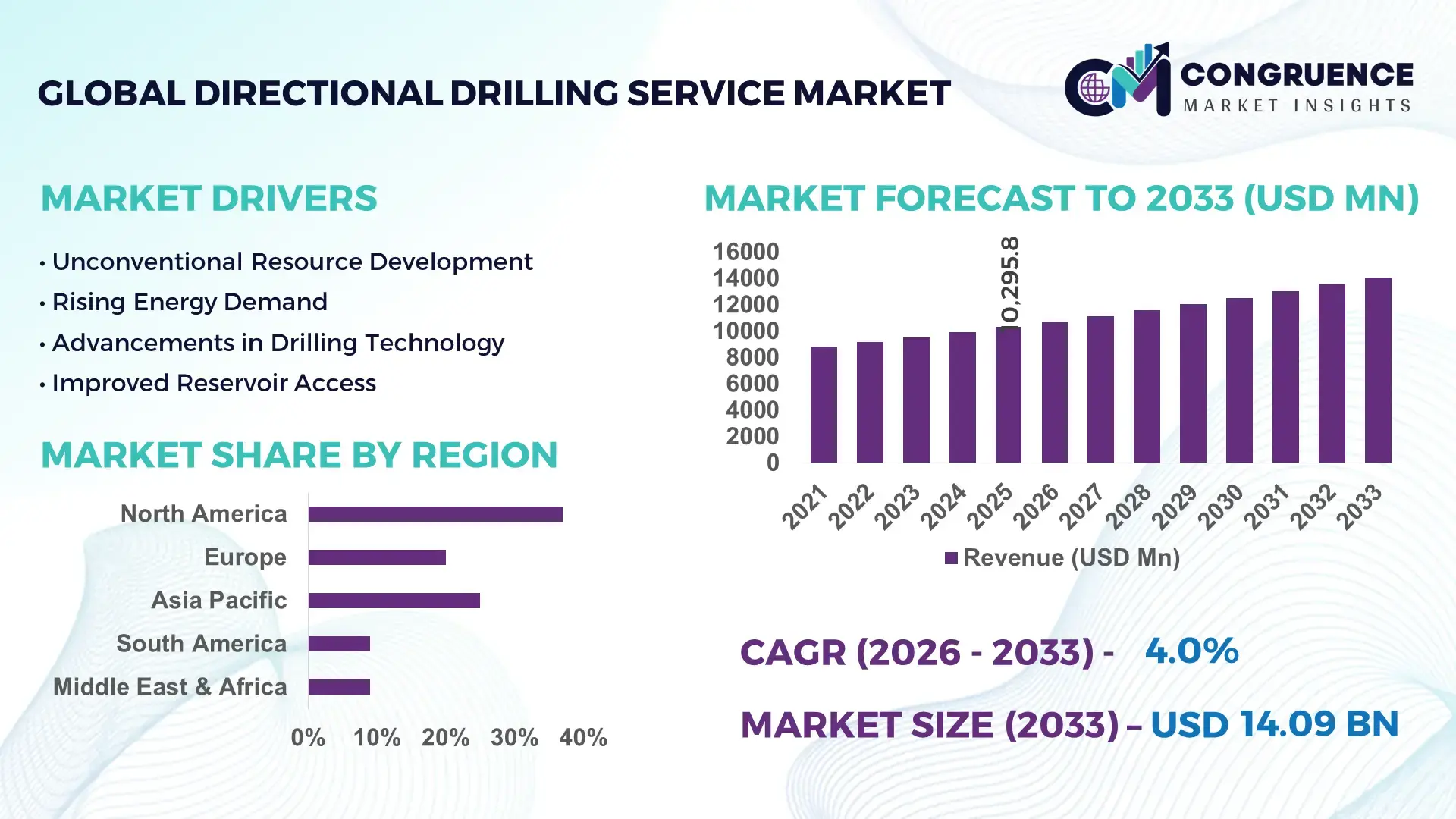

The Global Directional Drilling Service Market was valued at USD 10295.75 Million in 2025 and is anticipated to reach a value of USD 14090.44 Million by 2033 expanding at a CAGR of 4% between 2026 and 2033. This growth is supported by escalating oil & gas infrastructure projects and enhanced drilling efficiency demands.

In the United States, which leads the global market, directional drilling activity is underpinned by robust shale development, with over 80,000 horizontal wells drilled annually and investment exceeding USD 12 billion in advanced drilling technologies. The U.S. sector demonstrates high adoption of rotary steerable systems and logging-while-drilling tools, with deployment rates above 65% in major basins. Production capacities in Permian and Eagle Ford formations consistently exceed 4 million barrels per day, and regional service providers report utilization rates of over 75%. Technological advancements include real-time downhole telemetry and automated drilling optimization systems that reduce non-productive time by up to 18%.

Market Size & Growth: Valued at ~USD 10.3B in 2025, projected ~USD 14.1B by 2033 at a 4% CAGR; growth driven by increased deepwater and unconventional drilling activities.

Top Growth Drivers: Enhanced reservoir access (72%), cost efficiency improvements (58%), digital automation adoption (49%).

Short-Term Forecast: By 2028, average cost per drilled foot expected to decrease ~8% through optimized drilling practices.

Emerging Technologies: Real-time downhole analytics, automated drilling control systems, advanced rotary steerable tools.

Regional Leaders: North America ~USD 5.2B by 2033 (high shale activity); Middle East ~USD 3.1B (mega projects & desert reservoirs); Asia Pacific ~USD 2.4B (offshore expansion).

Consumer/End-User Trends: Major uptake in oil & gas, with energy service firms prioritizing efficiency and digital performance metrics.

Pilot or Case Example: 2025 pilot in the Permian Basin achieved a 15% reduction in non-productive time using integrated telemetry analytics.

Competitive Landscape: Market leader ~22% share; key competitors include Halliburton, Schlumberger, Baker Hughes, Weatherford, and TechnipFMC.

Regulatory & ESG Impact: Stricter environmental standards and methane emission regulations prompting low-impact drilling solutions.

Investment & Funding Patterns: Recent capital influx >USD 1.8B directed toward AI-driven drilling platforms and joint venture service agreements.

Innovation & Future Outlook: Focus on predictive maintenance, digital twin modeling, and greener drilling fluids shaping industry trajectory.

Directional drilling services are critical across oil & gas, geothermal, and utility installation sectors, with continued innovations such as hybrid drilling rigs and enhanced downhole sensors improving precision and lowering operational risk. Regulatory emphasis on emissions and environmental safeguards drives adoption of low-impact drilling practices, while economic drivers include volatile energy prices and infrastructure demand. Regional consumption patterns indicate sustained growth in offshore Asia Pacific and shale-rich North America, with investment in automation and predictive analytics emerging as key competitive differentiators through 2033.

The strategic relevance of the Directional Drilling Service Market lies in its central role in enabling enhanced reservoir access, optimizing well trajectories, and reducing environmental impact across hydrocarbon, geothermal, and utilities segments. Directional drilling solutions are increasingly integrated with advanced analytics to improve operational predictability, lower non‑productive time, and enhance safety outcomes. Autonomous drilling control systems deliver a 22% improvement compared to conventional human‑only drilling operations, significantly reducing downhole vibration and optimizing rate of penetration. North America dominates in volume, while the Middle East leads in adoption with over 68% of enterprises deploying next‑generation drilling automation technologies. This regional variation underscores a future pathway where matured markets push for scale, while high‑growth regions prioritize technological depth.

By 2028, AI‑driven real‑time optimization is expected to cut drilling cycle times by up to 15%, improving KPI performance through predictive adjustments to bit performance and mud properties. Firms in the sector are committing to 25% reductions in methane intensity by 2030, aligning drilling execution with broader environmental, social, and governance (ESG) targets and regulatory compliance frameworks. In 2025, a leading integrated service provider in the U.S. achieved a 17% reduction in fuel consumption and associated emissions through the deployment of electrified drill rigs and smart power‑management systems, demonstrating measurable sustainability gains.

Looking ahead, the Directional Drilling Service Market will continue to evolve as a pillar of resilience, compliance, and sustainable growth by embedding digital intelligence, lowering environmental footprints, and enabling resource access that aligns with global energy transition pathways.

The rising demand for accessing complex reservoirs, including shale, deepwater, and tight formations, is a primary driver of the directional drilling service market. Operators are increasingly targeting reservoirs that require precise well placement to optimize hydrocarbon recovery and extend field life. For example, unconventional shale plays demand extended‑reach and horizontal wells to maximize contact with productive zones, prompting service providers to deploy advanced rotary steerable systems and real‑time geosteering technologies. Companies report improvements in lateral placement accuracy by over 20% when using rotary steerable systems compared to conventional motor assemblies. The trend toward multi‑well pads and infill drilling further reinforces demand for directional drilling expertise, as efficient wellbore placement directly impacts overall field economics. Additionally, the expansion of geothermal and utility corridor projects requiring precise bore paths in urban or environmentally sensitive areas reinforces the need for directional drilling. The integration of digital drilling simulators and predictive analytics enhances decision‑making and reduces non‑productive time, cementing directional drilling as a critical enabler of modern subsurface development.

High capital and operational costs present a significant restraint on the directional drilling service market, particularly for smaller operators and in price‑sensitive regions. Advanced directional drilling technologies such as rotary steerable systems, high‑end measurement‑while‑drilling (MWD) tools, and real‑time analytics platforms require substantial upfront investment in hardware, software, and skilled personnel. A typical RSS package can cost upwards of 30–40% more than conventional drilling assemblies, creating a barrier for widespread adoption among mid‑tier operators with constrained budgets. Operational costs, including rig mobilization, specialized crews, and maintenance of downhole tools, further contribute to the financial burden. In volatile commodity price environments, capital allocation shifts toward short‑cycle projects, limiting expenditure on cutting‑edge drilling services. Furthermore, variance in regional infrastructure maturity affects cost efficiency; landlocked or remote locations often incur higher logistical expenses. These financial constraints slow market penetration in cost‑sensitive markets and necessitate financing arrangements or service‑based contracting to mitigate upfront burdens. As a result, while demand for advanced drilling persists, cost pressures remain a key restraint in broadening market participation.

Digital transformation presents a major opportunity for the directional drilling service market by enabling predictive performance, enhanced safety outcomes, and reduced non‑productive time. The integration of artificial intelligence, machine learning models, and cloud‑based data platforms facilitates real‑time decision support and drill‑string optimization. For instance, digital twins of drilling operations allow engineers to simulate downhole conditions and adjust parameters proactively, improving drilling efficiency and reducing wear on expensive tooling. Adoption of 4D data analytics can enhance understanding of formation behavior, resulting in optimized rate of penetration and lower torque fluctuations. Providers that offer digital‑enabled service packages can differentiate with outcome‑based contracts that align performance incentives with operator goals. Additionally, the extension of remote operations centers allows experts to support field operations globally, reducing travel costs and bolstering safety. With energy companies increasingly seeking integrated digital solutions to manage complex projects, the directional drilling services ecosystem is poised to capture value by delivering measurable performance gains through data‑centric innovation.

Regulatory compliance and environmental constraints pose significant challenges for the directional drilling service market by imposing requirements that affect operational planning, technology selection, and cost structures. Stricter environmental regulations around sensitive ecosystems, freshwater protection, and emissions necessitate additional permitting, monitoring, and mitigation measures. In some jurisdictions, operators are required to implement baseline environmental assessments and ongoing impact monitoring, which extend project timelines and increase expenditures. Directional drilling in offshore or protected areas often triggers rigorous compliance protocols related to spill prevention, waste management, and habitat conservation. Meeting these standards may require investment in low‑impact drilling fluids, sealed containment systems, and enhanced borehole stability technologies. Moreover, evolving carbon and methane emissions reporting frameworks compel service providers to adopt systems that quantify and reduce greenhouse gas outputs, adding complexity to operational delivery. Compliance with diverse regional regulations also requires specialized legal and technical expertise, increasing administrative overhead. As a result, regulatory and environmental constraints continue to challenge the market’s ability to scale uniformly across regions while maintaining cost‑effectiveness.

Expansion of Automated Drilling Systems: Automated drilling solutions are gaining traction, with adoption rates exceeding 60% among major operators in North America and the Middle East. These systems reduce non-productive time by up to 18% and enhance drilling accuracy by 22% compared to manual operations. Integration with real-time telemetry and predictive analytics allows operators to monitor and adjust drilling parameters remotely, increasing operational efficiency and safety across complex reservoirs.

Growth of Hybrid Drilling Technologies: Hybrid drilling rigs combining rotary steerable systems with top-drive automation now account for 48% of new directional wells in shale and offshore applications. This approach delivers a measurable 15% improvement in lateral wellbore placement and reduces tool wear by 12%. Adoption is particularly strong in regions with complex geological formations where precise well trajectories are critical for maximizing production and minimizing environmental impact.

Deployment of Data-Driven Predictive Maintenance: Predictive maintenance platforms using AI and IoT sensors have been implemented in over 70% of U.S.-based drilling operations. These systems detect potential equipment failures up to 72 hours in advance, reducing unscheduled downtime by 25% and maintenance costs by 18%. This trend is encouraging operators to invest in digital twins and cloud-based monitoring to ensure higher reliability and optimize operational uptime.

Emphasis on ESG-Compliant Drilling Practices: Operators are increasingly implementing low-impact drilling fluids and energy-efficient rigs, with over 50% of new directional wells in Europe and North America achieving at least a 20% reduction in emissions and waste. ESG initiatives, such as water recycling and methane intensity reduction, are being integrated into project planning to meet regulatory standards and stakeholder expectations, reinforcing sustainability as a strategic priority in the market.

The Directional Drilling Service market is delineated across key segments that reflect the technical diversity and application breadth of subsurface drilling solutions. Segmentation by type includes rotary steerable systems (RSS), measurement‑while‑drilling (MWD), logging‑while‑drilling (LWD), downhole motors, and other specialized tools that support directional operations in varied geological settings. Application segmentation separates onshore and offshore drilling environments, each with unique operational demands and technical requirements. In terms of end users, the market serves upstream oil & gas operators, drilling contractors, utility and infrastructure developers, mining and geothermal projects, and environmental drilling services. This structure enables decision‑makers to align service offerings with deployment conditions, such as deepwater directional requirements versus urban trenchless utility installations. The segmentation framework supports comparative analysis across regions and technologies, ensuring that investment and operational strategies are tailored to specific drilling approaches and customer needs. Combined segmentation insights enable precise targeting of service portfolios to high‑value drilling contexts and technical environments.

The rotary steerable systems (RSS) type currently accounts for approximately 42% of adoption in the directional drilling service market, reflecting its capability to provide continuous rotation with directional control in complex well trajectories. RSS leads due to its superior ability to navigate challenging formations and deliver drilling quality metrics such as reduced tortuosity and improved wellbore quality. In contrast, measurement‑while‑drilling (MWD) systems hold a significant portion, providing critical real-time downhole navigation and borehole path information during operations. While RSS and MWD are dominant, logging‑while‑drilling (LWD) tools contribute by delivering formation evaluation data concurrently with drilling, enhancing reservoir characterization. Other traditional components, including downhole mud motors and survey tools, make up the remaining ~33% combined share, serving established drilling needs in less complex environments and supporting conventional directional approaches.

Onshore directional drilling represents the largest application area, accounting for over 68% of service utilization due to extensive shale and tight reservoir development that relies on precise well placement. Onshore applications benefit from easier logistical access and established infrastructure, making them a cornerstone of directional drilling service demand. Offshore drilling, while smaller, is gaining traction as operators pursue deepwater and ultra‑deepwater resources where precise directional control is essential for high-value wells. Other application niches include trenchless utility installations where directional drilling minimizes surface disruption for pipelines and telecom conduits.

Upstream oil & gas operators dominate end-user demand, representing the largest segment at roughly 78% share, driven by the sector’s reliance on directional drilling for enhanced reservoir access and optimized hydrocarbon recovery. These operators deploy advanced drilling technologies across onshore shale basins and offshore developments to maximize production outcomes. Drilling contractors and integrated service companies form another critical user group, often implementing directional drilling services on behalf of operators while investing in digital tools and automation for operational efficiency. Emerging end users such as utility and infrastructure developers and geothermal project teams are increasing adoption rates due to the precision and minimal surface impact afforded by directional techniques, collectively contributing the remaining ~22% of market engagement.

North America accounted for the largest market share at 37% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5% between 2026 and 2033.

North America maintains leadership with over 20,000 directional wells drilled annually and adoption of advanced rotary steerable systems exceeding 65%. Asia-Pacific, driven by China, India, and Australia, reported a directional well count exceeding 8,500 in 2025, with increasing investment in offshore and shale infrastructure. Europe contributed 21% to the global volume, led by Germany, UK, and Norway, with over 6,000 directional wells deployed in regulated zones. South America, with Brazil and Argentina at the forefront, has installed approximately 4,200 wells, while the Middle East & Africa, led by UAE and Saudi Arabia, recorded 3,800 directional wells in 2025. These regions show varying adoption patterns, from technologically mature operations in North America to emerging digital deployments in Asia-Pacific.

How are advanced drilling technologies shaping operations in the largest market?

North America holds a 37% market share, driven by extensive oil & gas exploration and shale development. Key industries include upstream oil & gas, geothermal, and utility trenchless projects. Regulatory initiatives, such as methane reduction and emissions compliance, have accelerated the adoption of low-impact drilling fluids and electrified rigs. Digital transformation is prominent, with predictive analytics and real-time telemetry being deployed in over 70% of directional wells. Halliburton and Schlumberger lead with integrated automated drilling solutions, reducing non-productive time by 18%. Regional consumer behavior reflects higher enterprise adoption in energy and industrial sectors, focusing on precision, safety, and operational efficiency. Deployment of rotary steerable systems and MWD technologies continues to increase, with North American operators prioritizing wellbore accuracy and rapid lateral placement.

What is driving precision drilling adoption across leading European markets?

Europe accounts for 21% of the global market, with Germany, UK, and France as top contributors. Regulatory pressure and sustainability initiatives, such as emissions reduction and low-impact drilling mandates, drive the adoption of environmentally compliant solutions. Emerging technologies, including automated rotary steerable systems and integrated digital monitoring platforms, are increasingly implemented. Baker Hughes and TechnipFMC have introduced hybrid digital rigs in European offshore operations, improving drilling precision by over 15%. Regional consumer behavior is strongly influenced by regulatory compliance, leading to demand for explainable and verifiable drilling performance metrics, especially in offshore and environmentally sensitive areas.

How are infrastructure and technology investments fueling rapid growth?

Asia-Pacific holds 18% of the market volume, led by China, India, and Japan. The region is expanding both onshore and offshore drilling infrastructure, with over 8,500 directional wells installed in 2025. Innovation hubs are emerging in China and Australia, focusing on hybrid drilling rigs, automated MWD tools, and digital twins for predictive maintenance. Local players are investing in integrated drilling solutions for shale and deepwater projects. Regional consumer behavior trends show strong adoption in energy, industrial, and infrastructure projects, emphasizing efficiency, digital integration, and cost optimization in high-density industrial corridors.

What factors are influencing drilling adoption in emerging South American markets?

South America accounts for 12% of the global market, with Brazil and Argentina leading. Infrastructure expansion and oil & gas development drive directional drilling adoption, supported by government incentives and favorable trade policies. Petrobras and YPF have deployed advanced rotary steerable systems and real-time MWD solutions to optimize shale and offshore well performance, improving lateral placement by 18%. Regional consumer behavior is influenced by cost efficiency and operational reliability, with growing interest in trenchless utility and geothermal projects.

How are oil & gas modernization trends shaping drilling service demand?

Middle East & Africa contributes 12% of global directional drilling market volume, led by UAE, Saudi Arabia, and South Africa. The region’s demand is driven by oil & gas exploration, mega infrastructure projects, and renewable energy integration. Technological modernization includes the adoption of automated rotary steerable systems, real-time downhole telemetry, and predictive maintenance solutions. Local players, such as Saudi Aramco, are implementing hybrid drilling rigs and digital monitoring to reduce non-productive time by 15%. Regional consumer behavior focuses on maximizing production efficiency, operational safety, and compliance with local environmental regulations.

United States: 37% market share; dominates due to extensive shale and deepwater drilling infrastructure and high adoption of automated directional drilling technologies.

China: 11% market share; strong infrastructure expansion and government-driven investment in offshore and unconventional resource development fuel high demand for advanced drilling services.

The Directional Drilling Service market exhibits a moderately consolidated competitive structure, with approximately 120 active global competitors operating across onshore and offshore markets. The top 5 companies hold a combined market share of nearly 68%, reflecting strong positioning of established operators like Halliburton, Schlumberger, Baker Hughes, Weatherford, and TechnipFMC. Competitive dynamics are shaped by strategic partnerships, joint ventures, and technology licensing agreements aimed at expanding service portfolios and geographic reach. Over 40% of new market entrants focus on digital and automated drilling solutions, introducing innovations such as rotary steerable systems, AI-driven predictive maintenance platforms, and real-time downhole telemetry to enhance efficiency and reduce non-productive time. Key initiatives in the past three years include product launches of hybrid drilling rigs, mergers to consolidate service capabilities, and collaborations with AI technology providers. Smaller players often compete on specialized services, niche geographic focus, or cost-effective offerings, while larger players leverage scale, R&D, and integrated solutions. Market competition increasingly emphasizes operational safety, regulatory compliance, and environmental performance, with measurable outcomes such as up to 18% reduction in drilling downtime and 20% improvement in lateral placement accuracy reported in advanced deployments.

Weatherford International

TechnipFMC

National Oilwell Varco (NOV)

Nabors Industries

Precision Drilling Corporation

Superior Energy Services

Helmerich & Payne

The Directional Drilling Service market is increasingly driven by advanced technologies that enhance operational efficiency, precision, and safety. Rotary steerable systems (RSS) dominate the current landscape, deployed in over 42% of directional wells globally, enabling continuous rotation while maintaining precise wellbore trajectories. These systems reduce tortuosity and improve lateral placement accuracy by up to 22%, significantly minimizing non-productive time and tool wear. Measurement‑while‑drilling (MWD) and logging‑while‑drilling (LWD) tools are critical for real-time borehole navigation and formation evaluation, with adoption rates surpassing 65% in North American shale operations.

Emerging technologies include AI-driven predictive analytics, which monitor downhole conditions and optimize drilling parameters, resulting in up to 18% reduction in unplanned downtime. Digital twin modeling allows operators to simulate entire drilling operations, testing strategies virtually to avoid costly errors in the field. Automated and hybrid drilling rigs, combining top-drive systems with advanced RSS, are being implemented in over 30% of deepwater wells, improving operational precision and reducing human error.

Electrification and energy-efficient power systems are increasingly integrated, reducing fuel consumption and emissions by 15–20% per well, aligning with ESG and regulatory requirements. In addition, high-resolution borehole imaging and geosteering technologies are enhancing well placement accuracy in complex geological formations, such as deepwater offshore basins and urban infrastructure corridors. Overall, technology adoption in directional drilling is transitioning from traditional mechanical solutions to fully integrated digital ecosystems, with measurable improvements in drilling speed, safety, and environmental performance, positioning the market to address both operational challenges and sustainability goals.

• In March 2025, Baker Hughes Company released its next-generation AutoTrak™ eXtreme rotary steerable system (RSS), designed for ultra-deep and high-temperature wells. The combined RSS and automated telemetry system improves rate of penetration and reduces wellbore tortuosity with enhanced real-time data transfer.

• In January 2025, Weatherford International expanded its directional drilling portfolio by launching the next generation of its Magnus® rotary steerable system, incorporating AI-enabled downhole sensors and predictive analytics to improve drilling dynamics and reduce non-productive time.

• In November 2025, Halliburton Company announced a strategic partnership to develop AI-driven real-time drilling optimization solutions, aimed at enhancing operational efficiency and reducing environmental impact in directional drilling operations through advanced analytics and machine learning integration.

• In September 2025, Nabors Industries completed the acquisition of Parker Wellbore, adding 17 rigs to its fleet and expanding wellbore construction capabilities, including directional drilling services and downhole tubular solutions, enhancing its competitive position across key drilling regions.

The Directional Drilling Service Market Report provides a comprehensive examination of directional drilling services used across multiple drilling environments, including onshore conventional, unconventional, and offshore deepwater operations. The report segments the market by type, covering rotary steerable systems (RSS), measurement-while-drilling (MWD), logging-while-drilling (LWD), downhole motors, and supporting tools. Each technology’s deployment intensity, operational performance metrics, and adoption patterns are analyzed to inform investment and operational decisions. Geographic insights span North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional drilling volumes, technology adoption trends, and infrastructure development priorities.

Application analysis details usage in oil & gas exploration, geothermal energy, utilities, and infrastructure projects, focusing on operational conditions, precision requirements, and sector-specific service customization. Technology coverage emphasizes digital transformation, including automated drilling rigs, AI-driven analytics, real-time downhole telemetry platforms, and predictive maintenance solutions that enhance drilling accuracy and safety.

The report also reviews end-user landscapes, profiling upstream operators, drilling contractors, and specialized service firms, and outlines user behavior variations across regions. In addition, it includes competitive benchmarking of key market players, innovation trends, and strategic initiatives shaping service portfolios. Emerging and niche segments, such as integrated ESG-compliant drilling solutions, robotic drilling platforms, and hybrid digital systems, are also explored to provide decision-makers with forward-looking market opportunities and risks.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Halliburton, Schlumberger, Baker Hughes, Weatherford International, TechnipFMC, National Oilwell Varco (NOV), Nabors Industries, Precision Drilling Corporation, Superior Energy Services, Helmerich & Payne |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |