Reports

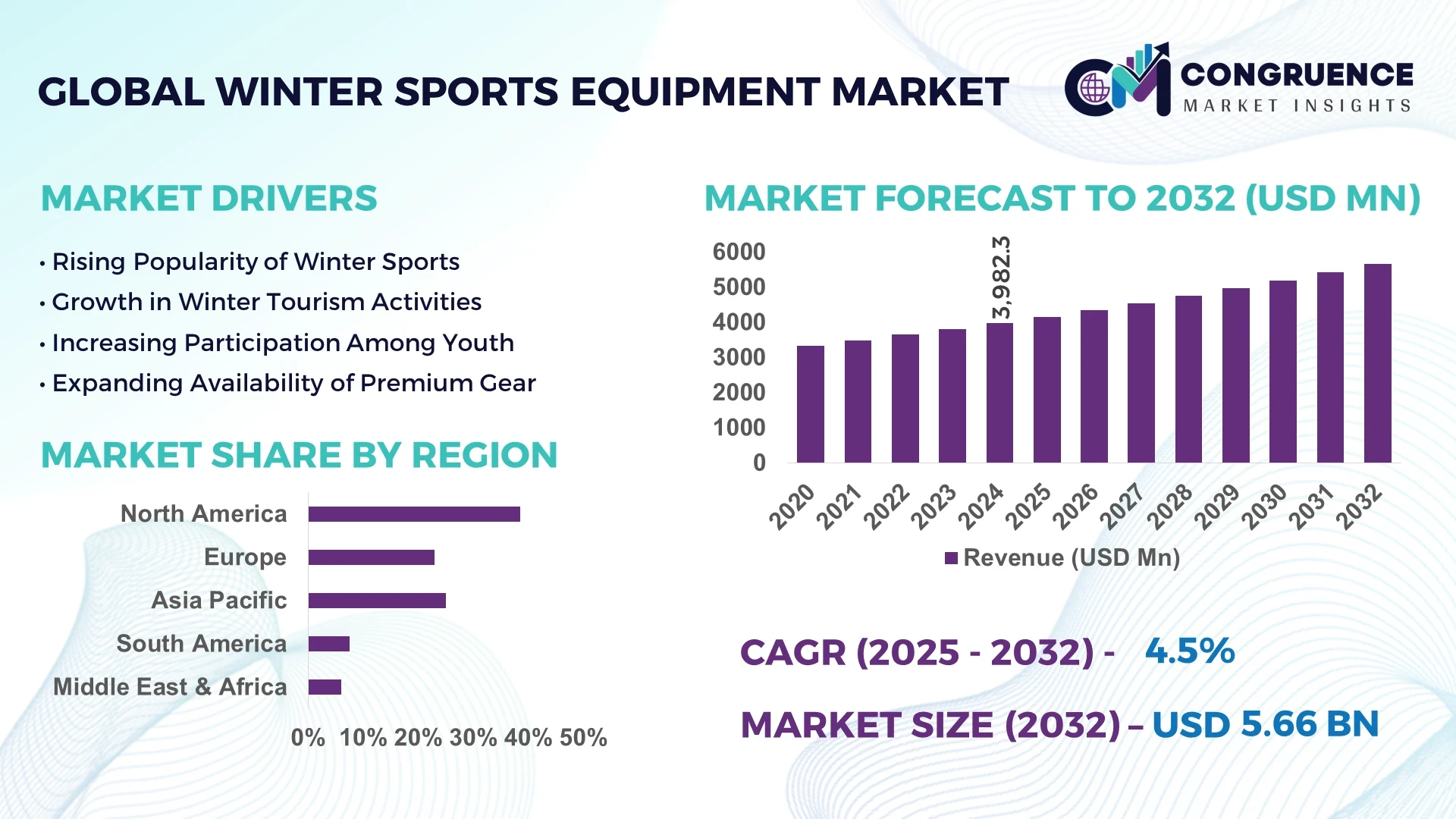

The Global Winter Sports Equipment Market was valued at USD 3,982.28 Million in 2024 and is anticipated to reach a value of USD 5,663.21 Million by 2032 expanding at a CAGR of 4.5% between 2025 and 2032.

Canada stands out as a key player in the Winter Sports Equipment market, boasting advanced manufacturing facilities specializing in high-performance skis and snowboards. The country invests significantly in research and development to enhance product durability and incorporate eco-friendly materials, while its industry benefits from strong government support for winter sports tourism and infrastructure development.

The Winter Sports Equipment market encompasses various product categories such as skis, snowboards, sledges, ice skates, and protective gear, with skiing equipment accounting for a significant share of overall sales. Recent technological advancements include lightweight composite materials and enhanced safety features, which have improved athlete performance and consumer safety. Stringent environmental regulations are prompting manufacturers to adopt sustainable production methods, aligning with global eco-conscious trends. Economically, rising disposable incomes in developed regions and expanding winter sports participation in emerging markets drive demand. Consumption patterns indicate higher sales in North America and Europe, with growing interest in Asia-Pacific markets. Emerging trends include smart wearable devices integrated with winter sports gear and increased customization options tailored to individual athletes’ needs, which collectively shape the future outlook for the Winter Sports Equipment industry.

Artificial intelligence is significantly revolutionizing the Winter Sports Equipment Market by optimizing design processes, enhancing production efficiency, and elevating user experience. AI-powered design tools enable manufacturers to simulate and test equipment performance under various conditions, reducing development time and costs while improving product reliability. For instance, machine learning algorithms analyze vast amounts of performance data to recommend optimal materials and structural modifications for skis and snowboards, resulting in lighter yet stronger equipment. Moreover, AI-driven robotics automate precision manufacturing, increasing throughput and minimizing defects in production lines.

In the retail segment of the Winter Sports Equipment Market, AI-based virtual fitting technologies provide consumers with personalized gear recommendations based on their biomechanics and skill levels, improving customer satisfaction and reducing return rates. AI also supports predictive maintenance for rental equipment, monitoring wear and tear to schedule timely servicing, thereby extending product lifespan and reducing operational downtime. Additionally, AI-enhanced data analytics offer manufacturers and retailers actionable insights into consumer behavior, inventory management, and market trends, allowing for more strategic decision-making. Collectively, these AI innovations contribute to improved operational performance, greater market responsiveness, and elevated product quality across the Winter Sports Equipment Market, fostering competitive advantage and innovation.

“In early 2024, a leading Winter Sports Equipment manufacturer integrated AI-driven materials analysis into their R&D process, resulting in a 15% reduction in prototype testing time and a 10% increase in equipment durability as measured through standardized stress tests.”

The increasing popularity of winter sports such as skiing, snowboarding, and ice skating is a significant driver in the Winter Sports Equipment Market. More individuals, especially in North America and Europe, are engaging in winter sports as leisure activities, supported by expanding infrastructure and organized events. For example, ski resorts worldwide reported a 12% increase in visitor numbers in recent years, fueling equipment sales. Additionally, government initiatives promoting winter tourism and healthy lifestyles contribute to rising demand for specialized gear, including helmets, poles, and boots. The rise in youth participation in winter sports schools and clubs also supports continuous market expansion.

A major restraint in the Winter Sports Equipment Market is the high cost associated with technologically advanced and premium-quality products. Cutting-edge equipment incorporating lightweight composites, smart sensors, or AI-enabled features typically commands premium prices, limiting accessibility for budget-conscious consumers. For instance, top-tier alpine skis can cost up to 30% more than basic models, restricting purchase decisions for casual users. Furthermore, the seasonal nature of winter sports limits year-round demand, affecting manufacturers' revenue streams. Import tariffs and fluctuating raw material prices, especially for metals and polymers, also increase production costs, posing challenges to market affordability and growth.

Emerging markets in Asia-Pacific and Latin America present significant growth opportunities for the Winter Sports Equipment Market due to rising disposable incomes and increasing interest in winter sports. Countries such as China and South Korea have invested heavily in winter sports infrastructure, especially after hosting major international events, which has driven local demand for specialized equipment. Furthermore, the market is witnessing a growing trend in customization, with manufacturers offering tailored equipment to meet individual athlete preferences and skill levels. This personalization improves customer satisfaction and brand loyalty while opening new revenue streams through premium product lines.

The Winter Sports Equipment Market faces considerable challenges due to stringent regulatory frameworks focusing on safety standards and environmental sustainability. Manufacturers must adhere to complex certification processes to ensure product safety, durability, and environmental impact compliance, often leading to extended development timelines and higher costs. For example, regulations restricting the use of certain plastics and chemicals compel producers to innovate with alternative eco-friendly materials, which can be costlier and require retooling production lines. Additionally, fluctuating environmental policies across regions complicate global supply chain management and product standardization, impacting market agility and profitability.

• Surge in Smart Winter Sports Gear Adoption: The Winter Sports Equipment market is witnessing rapid integration of smart technologies into traditional gear. Products such as AI-enabled helmets and GPS-integrated ski boots are increasingly popular among professional athletes and recreational users. Recent surveys indicate that over 35% of new winter sports gear sales in developed markets now feature embedded sensors that monitor performance and safety metrics, enhancing user experience and reducing injury risks.

• Growing Demand for Eco-Friendly and Sustainable Equipment: Sustainability has become a defining trend in the Winter Sports Equipment market. Manufacturers are adopting recycled materials and bio-based composites in producing skis, snowboards, and protective gear. Approximately 28% of winter sports products launched in the past two years incorporate eco-conscious materials, driven by stricter environmental regulations and consumer preferences for green products. This shift supports brand differentiation and long-term environmental responsibility.

• Expansion of Rental and Subscription Models: An emerging business trend is the rise of rental and subscription services for Winter Sports Equipment. These models cater to occasional users and promote accessibility by lowering upfront costs. Market data shows a 22% increase in rental service usage in ski resorts across North America, driven by millennials and urban consumers seeking flexible access to premium gear without ownership burdens.

• Advances in Lightweight Composite Materials: Technological innovation in lightweight composites is significantly impacting the Winter Sports Equipment market. New carbon fiber and fiberglass blends improve durability while reducing equipment weight by up to 15%. This development enhances athlete agility and endurance, particularly in competitive skiing and snowboarding segments, where every gram counts. Manufacturers are increasingly investing in material science to maintain a competitive edge and meet rising performance expectations.

The Winter Sports Equipment market is segmented primarily by product type, application, and end-user, each revealing distinct trends and growth drivers. Types include skis, snowboards, ice skates, sledges, and protective gear, reflecting diverse consumer preferences and sport-specific demands. Application segments range from recreational sports and professional competitions to rental services and training academies, each with unique requirements. End-users are broadly categorized into individual consumers, sports clubs, rental businesses, and professional athletes. This segmentation provides clarity on market dynamics and facilitates targeted strategies for manufacturers and distributors aiming to optimize product offerings and customer reach in a competitive environment.

Skis remain the leading product type within the Winter Sports Equipment market, commanding the largest volume due to their widespread use in both recreational and competitive skiing disciplines. High demand for alpine and cross-country skis, supported by technological enhancements like carbon fiber frames, underpins their dominance. Snowboards are the fastest-growing type, driven by increasing youth engagement and expanding snowboarding events worldwide. Their growth is further bolstered by innovations in board flexibility and safety features, appealing to beginner and advanced riders alike. Ice skates and sledges serve niche segments; ice skates are crucial in figure skating and hockey markets, while sledges cater mostly to children and leisure users. Protective gear, including helmets and padding, complements these types, emphasizing safety across all winter sports activities.

Recreational winter sports dominate the Winter Sports Equipment market, with a large consumer base engaging in skiing, snowboarding, and ice skating for leisure. The accessibility of winter resorts and outdoor sports parks supports this leading application segment. Competitive sports applications are witnessing rapid growth, fueled by increasing participation in professional and amateur winter sports events globally. This segment demands high-performance, specialized equipment tailored to athlete needs. Rental services represent another significant application area, especially in popular tourist destinations, offering cost-effective access to quality gear. Training and coaching institutions contribute steadily, driving demand for beginner-friendly and durable equipment designed for repeated use and safety in learning environments.

Individual consumers represent the largest end-user segment in the Winter Sports Equipment market, encompassing casual and avid winter sports enthusiasts purchasing personal gear for recreational or competitive use. Their demand is supported by rising participation rates and growing health-conscious lifestyles in colder regions. Rental businesses are the fastest-growing end-user group, expanding rapidly alongside the rise in winter tourism and experiential travel, particularly in North America and Europe. These services focus on providing high-quality, durable equipment to a transient user base. Sports clubs and professional athletes form a specialized end-user segment that drives demand for premium and customized equipment, often investing in the latest technological advancements to enhance performance and safety during training and competitions.

North America accounted for the largest market share at 38.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America continues to lead due to its mature winter sports infrastructure, widespread consumer engagement, and strong investment in innovative equipment manufacturing. The Asia-Pacific region is rapidly expanding, driven by increasing participation in winter sports activities, growing middle-class spending, and significant improvements in sports facilities and training centers. Europe, South America, and the Middle East & Africa also contribute notably to the market, each showing unique regional consumption patterns influenced by climate, tourism, and government initiatives supporting winter sports equipment adoption and technological innovation.

"Driving Innovation and Regulatory Support in North America"

The North America Winter Sports Equipment market holds approximately 38% of the global volume, led by strong demand from skiing, snowboarding, and ice hockey sectors. The U.S. and Canada are pivotal markets, where government programs incentivize winter sports participation and equipment safety standards have been rigorously enhanced. Digital transformation is prominent, with manufacturers leveraging AI and IoT technologies to improve product customization and safety features. Regulatory frameworks promoting sustainable production practices and reducing environmental impact further shape the market landscape. The integration of smart sensors and wearable tech in winter sports gear is also a key trend accelerating adoption among consumers focused on performance and safety.

"European Sustainability and Technology Drive Market Growth"

Europe accounts for about 27% of the Winter Sports Equipment market volume, with Germany, the UK, and France as the leading consumers. The region benefits from well-established winter sports traditions and stringent regulatory bodies enforcing environmental sustainability in manufacturing processes. The European Union’s green policies encourage manufacturers to use recycled materials and reduce carbon footprints. Technology adoption includes advanced composites and digital design tools improving product durability and user experience. European winter resorts and sports clubs are major contributors, demanding high-quality equipment to meet professional standards and recreational needs.

"Rapid Expansion and Innovation in Asia-Pacific Winter Sports"

Asia-Pacific ranks as the second-largest market region by volume, with China, Japan, and India leading consumption. Infrastructure development, including new ski resorts and indoor ice rinks, is rapidly expanding in these countries, supported by government investments in winter sports tourism. Manufacturing hubs in the region are adopting automation and advanced materials technology to boost production efficiency and product quality. Regional innovation centers are increasingly focusing on integrating AI and wearable tech into winter sports equipment, catering to a growing population of winter sports enthusiasts and competitive athletes.

"Emerging Market Potential in South America"

South America’s Winter Sports Equipment market is growing steadily, with Brazil and Argentina being key contributors, holding an estimated 5% share of the global market volume. The expansion of ski resorts in the Andes and rising interest in winter sports among the middle class are driving demand. Infrastructure improvements and energy sector investments in these countries support market growth. Government incentives aimed at boosting tourism and sports development are helping improve accessibility and affordability of winter sports equipment in the region.

"Technological Modernization Fuels Growth in Middle East & Africa"

The Middle East & Africa region holds around 3% of the global Winter Sports Equipment market, with the UAE and South Africa as major contributors. Despite the warmer climate, increasing interest in winter sports through indoor facilities and recreational complexes supports demand. Oil & gas industry growth indirectly boosts consumer spending capacity in key countries. The region is witnessing technological modernization with importers emphasizing high-tech, durable winter sports gear. Trade partnerships with Europe and Asia facilitate access to advanced products, while local regulations focus on quality standards and safety compliance.

United States: Holds approximately 25% of the Winter Sports Equipment market due to its advanced manufacturing capacity and high consumer participation in skiing and snowboarding activities.

China: Accounts for nearly 18% of the market share, driven by rapid infrastructure development and increasing popularity of winter sports among its expanding middle class.

The Winter Sports Equipment market features a highly competitive environment with over 50 active global players ranging from established multinational corporations to innovative startups. Market leaders emphasize product innovation, technological integration, and sustainability to strengthen their positioning. Key strategic initiatives include collaborations between equipment manufacturers and technology firms to develop smart gear incorporating sensors and AI for enhanced user experience. Additionally, several companies have pursued mergers and acquisitions to expand product portfolios and geographic reach, targeting emerging markets in Asia-Pacific and South America. The competitive landscape is also shaped by rapid product launches focusing on lightweight materials, durability, and eco-friendly manufacturing processes. Industry players continuously invest in R&D to introduce customizable equipment tailored to specific winter sports disciplines, enhancing performance and safety. The trend toward digital transformation, including online sales platforms and virtual fitting technologies, further intensifies competition by improving customer engagement and broadening market access globally.

Burton Snowboards

Rossignol Group

Atomic Austria GmbH

Head NV

Salomon Group

Fischer Sports GmbH

K2 Sports

Tecnica Group

Volkl Sports GmbH

Black Diamond Equipment

The Winter Sports Equipment market is undergoing significant transformation driven by cutting-edge technologies enhancing performance, safety, and user experience. Advanced materials such as carbon fiber composites and thermoplastics are increasingly used to produce lighter, more durable skis, snowboards, and protective gear. Innovations in 3D printing allow for rapid prototyping and customization, enabling manufacturers to tailor equipment to individual athlete specifications with greater precision. Sensor integration and wearable technology have become integral, providing real-time data on speed, motion, and environmental conditions that enhance training and safety for winter sports enthusiasts.

Digital technologies like augmented reality (AR) and virtual reality (VR) are revolutionizing retail and training experiences by offering virtual fittings and immersive simulation environments, reducing return rates and improving customer satisfaction. Moreover, the adoption of IoT-enabled smart helmets and goggles allows athletes to monitor vital health metrics, communicate, and navigate more efficiently in challenging winter conditions. Environmentally sustainable manufacturing processes, including recycled materials and eco-friendly coatings, are gaining traction to meet regulatory standards and consumer demand for green products. These technology advancements collectively propel innovation, operational efficiency, and competitive differentiation in the Winter Sports Equipment market.

In December 2023, Salomon launched the S/Max Carbon ski boots featuring a newly developed carbon sole that reduces weight by 15% while improving power transmission for professional alpine skiers.

In March 2024, Burton unveiled its Eco Collection snowboards made with 100% recycled base materials and bio-resin binding, reinforcing the company’s commitment to sustainability in winter sports equipment manufacturing.

In August 2023, Head introduced a new line of smart ski goggles equipped with integrated heads-up displays that provide GPS navigation, speed tracking, and weather updates, enhancing safety and performance on slopes.

In February 2024, Fischer Sports expanded its product portfolio with the launch of customized 3D-printed ski poles, allowing athletes to select ergonomic grips and optimal shaft stiffness tailored to their skiing style.

The Winter Sports Equipment Market Report offers a comprehensive analysis covering diverse product segments including skis, snowboards, ice skates, sledges, and associated protective gear. It evaluates the market’s segmentation by type, application, and end-user, providing detailed insights into product preferences and usage patterns across various winter sports disciplines. The report highlights key geographic regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering a granular view of regional demand dynamics, infrastructure development, and consumption trends.

In addition to traditional product categories, the report addresses emerging segments such as smart and connected winter sports equipment that leverage digital technologies for enhanced user experience. It examines advances in materials science and manufacturing processes impacting product innovation and sustainability. The study also explores market applications across professional sports, recreational activities, and commercial rental services, reflecting shifts in consumer behavior and industry focus.

Technological integration, including wearable devices and IoT-enabled equipment, receives particular attention to assess their role in shaping future market directions. The report further encompasses an analysis of regulatory environments, environmental considerations, and economic factors influencing production and distribution. Overall, the scope is designed to support strategic decision-making by offering a well-rounded understanding of the Winter Sports Equipment market’s current landscape and growth opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3982.28 Million |

|

Market Revenue in 2032 |

USD 5663.21 Million |

|

CAGR (2025 - 2032) |

4.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |