Reports

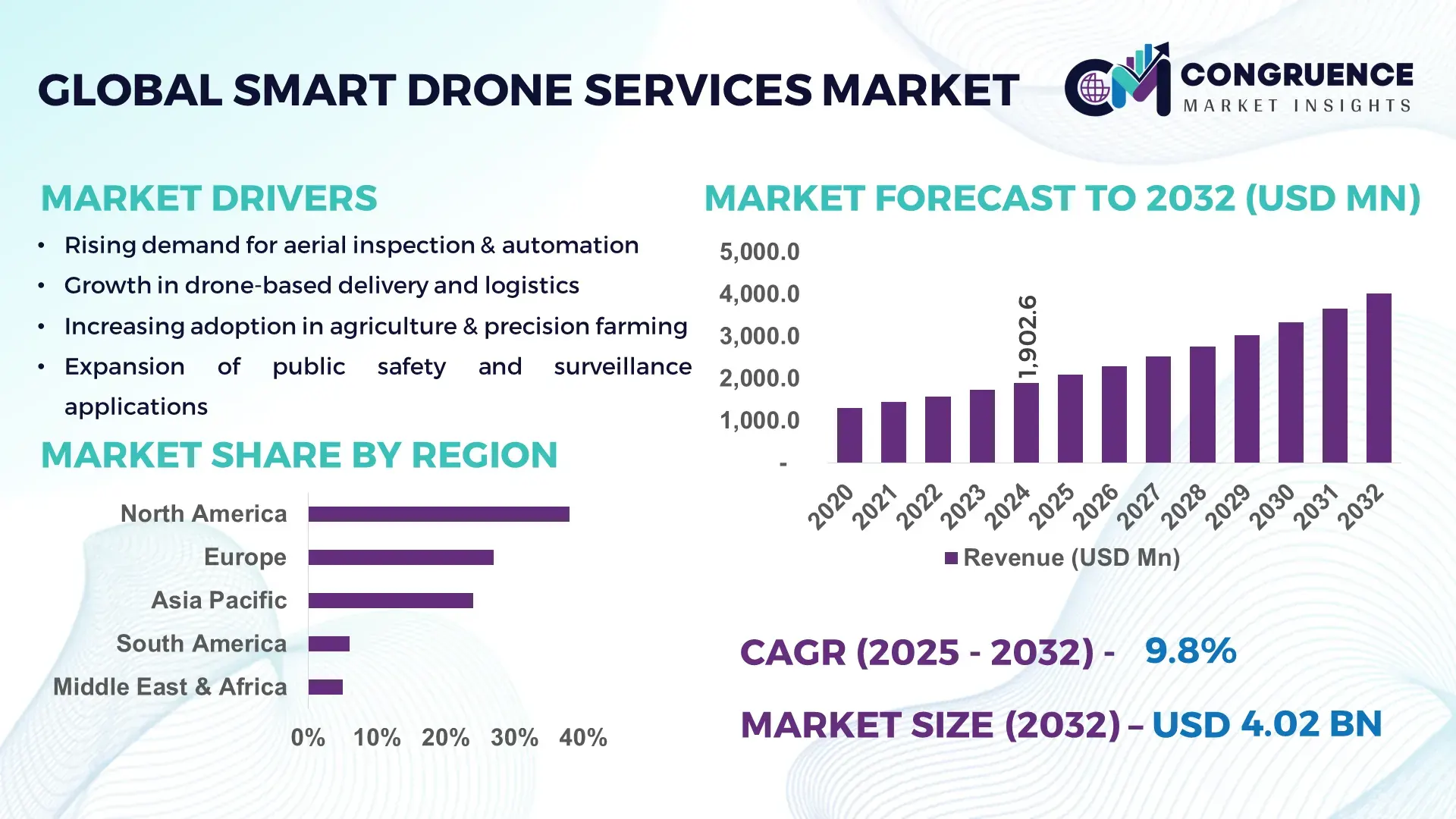

The Global Smart Drone Services Market was valued at USD 1,902.6 Million in 2024 and is anticipated to reach USD 4,019.4 Million by 2032, expanding at a CAGR of 9.8% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by accelerating enterprise-level adoption of autonomous inspection, delivery, surveillance, and mapping solutions.

The United States leads the global Smart Drone Services Market due to its extensive deployment capacity, advanced R&D investments, and strong integration of AI-driven navigation systems across defense, energy, construction, and agriculture. The country has over 22,000+ certified commercial drone operators, more than USD 3.5 billion invested in drone-related AI and autonomy technologies since 2020, and rapid uptake of BVLOS (Beyond Visual Line of Sight) applications across more than 48 states, supporting technological modernization and scalable service deployment.

Market Size & Growth: Market valued at USD 1.9 Billion in 2024 and projected to surpass USD 4.0 Billion by 2032 with a 9.8% CAGR, driven by rising autonomous operation capabilities.

Top Growth Drivers: 43% surge in infrastructure inspection adoption; 38% efficiency gains from AI-enabled flight automation; 52% increase in environmental monitoring use cases.

Short-Term Forecast: By 2028, drone-enabled industrial inspections expected to cut on-site labor requirements by 28% and enhance data accuracy by 35%.

Emerging Technologies: Expansion of 5G-enabled drone operations, AI-powered edge-processing, and autonomous swarm-coordination systems.

Regional Leaders: North America projected to reach USD 1.38 Billion by 2032 with high enterprise adoption; Europe expected to hit USD 1.12 Billion driven by regulatory modernization; Asia-Pacific forecast at USD 1.05 Billion with strong industrial digitization.

Consumer/End-User Trends: High adoption among utilities, agriculture, and construction, with growing transition to automated analytics-based workflows.

Pilot or Case Example: In 2024, a U.S. energy provider achieved 47% reduction in inspection downtime through automated thermal-imaging drone systems.

Competitive Landscape: Leading player holds ~18% market share, followed by major competitors including DJI Enterprise, Parrot Drones, Skydio, and Terra Drone.

Regulatory & ESG Impact: Governments enforcing stricter aerial safety frameworks and promoting carbon-neutral operational standards across fleet deployments.

Investment & Funding Patterns: Over USD 2.1 Billion invested globally in drone-automation platforms and BVLOS operations between 2021–2024.

Innovation & Future Outlook: Advancements in autonomous navigation, predictive analytics, and urban air-mobility integration are expected to shape next-generation drone service ecosystems.

Unique information: The Smart Drone Services Market is expanding due to convergence across energy, transportation, agriculture, and construction, each contributing rising adoption volumes. New AI-driven imaging, autonomous swarm coordination, and high-precision LiDAR upgrades are reshaping operational workflows. Evolving safety regulations, increasing environmental monitoring needs, and regional digitalization policies continue to boost usage, reinforcing a strong future outlook for industry decision-makers.

The strategic significance of the Smart Drone Services Market has increased substantially as enterprises accelerate their shift toward autonomous inspection, logistics optimization, and real-time analytics. The market’s relevance lies in its ability to reduce operational risks, strengthen asset oversight, and enhance decision-making speed through high-precision data capture. New technologies are setting performance benchmarks—AI-driven analytics deliver up to 42% improvement in inspection accuracy compared to manual surveying standards—demonstrating measurable operational impact across industries.

Regional variations further shape the market: North America dominates in volume, driven by extensive BVLOS and industrial deployment, while Europe leads in adoption with 61% of enterprises integrating drone-enabled monitoring into their operational frameworks. Short-term projections indicate strong momentum: By 2027, autonomous drone navigation systems are expected to reduce energy-sector inspection times by 32%, significantly improving safety and cost-efficiency.

ESG commitments are also reshaping drone service strategies. Firms are targeting up to 25% emission reduction in field operations by 2030, enabled by electric-powered drones and optimized flight-route planning. A measurable example includes Japan’s 2024 infrastructure modernization initiative, which achieved a 39% reduction in bridge-inspection time using AI-enhanced drone fleets.

Looking ahead, the Smart Drone Services Market will play a central role in operational resilience, compliance modernization, and sustainable industrial growth, positioning it as a critical enabler of next-generation digital infrastructure.

The Smart Drone Services Market is evolving through rapid technological upgrades, shifting regulatory frameworks, and rising enterprise digital-transformation priorities. Increasing demand for automated inspection, precision agriculture, aerial mapping, and emergency response operations continues to shape service models. Advancements in AI-based data analytics, high-resolution multispectral imaging, and autonomous navigation systems are strengthening the value proposition of drone-based solutions. Growing interest in BVLOS operations, urban air-mobility applications, and cloud-integrated drone data platforms further enhance scalability. Regional infrastructural modernization, workforce safety initiatives, and environmental monitoring requirements collectively sustain market expansion and operational adoption.

Infrastructure digitization is a major catalyst for Smart Drone Services Market expansion, driven by increasing demand for automated structural assessment, precision mapping, and high-risk asset monitoring. Organizations are leveraging drone systems to accelerate inspections of bridges, powerlines, solar facilities, and construction sites. Digital-twin integration, real-time imaging, and AI-powered defect detection are replacing traditional manual methods, boosting operational efficiency. For example, infrastructure developers report up to 40% faster site-monitoring cycles and 30% improvement in defect-identification accuracy using automated drone surveys. Rapid urbanization and rising investments in smart-city projects continue to amplify demand for drone-based data acquisition and monitoring across global infrastructure networks.

Regulatory inconsistencies remain a major barrier, particularly concerning BVLOS permissions, restricted flying zones, data-security rules, and licensing requirements. These variations create operational delays, limit service scalability, and increase compliance costs for enterprises. Many regions still maintain conservative drone-operation frameworks, resulting in extended approval timelines and limited autonomy allowances. Data privacy rules add another layer of complexity, requiring stringent protection of geospatial and industrial data. Workforces also face certification hurdles, with many countries demanding specific operator training programs. These regulations collectively slow the pace of deployment, limiting high-volume commercial applications and creating operational uncertainty for service providers.

AI-enabled automation presents substantial opportunities by enhancing predictive analytics, real-time anomaly detection, and autonomous fleet management. Industries such as energy, mining, construction, agriculture, and logistics increasingly require high-frequency data collection and large-area monitoring—tasks well suited for AI-powered drones. Automated flight-path optimization and onboard image processing significantly reduce manual intervention, enabling scalability. Studies indicate that automated drone systems can deliver up to 45% faster operational cycles and 29% lower data-processing workloads compared to traditional workflows. Expanding 5G networks and cloud-integrated analytics platforms further enable transformation across inspection, surveying, and environmental monitoring applications.

Operational risks—such as signal interference, weather sensitivity, and battery limitations—continue to challenge high-scale deployment. Harsh environments, electromagnetic disturbances, and restricted flight corridors increase the probability of system interruptions. Battery constraints limit long-range and heavy-payload missions, requiring frequent recharge or replacement cycles. Enterprises also face challenges integrating drone data with legacy infrastructure systems, creating workflow bottlenecks. Additionally, shortages of skilled drone pilots and technical specialists hinder adoption. These challenges generate additional training, maintenance, and hardware costs, slowing deployment momentum across industrial and commercial use cases.

Expansion of AI-Driven Survey Automation: AI-based automated mapping systems are rapidly transforming project workflows, enabling faster imaging cycles and enhanced terrain modeling. Adoption of automated survey solutions grew by 46% in 2024, with AI improving data-classification accuracy by 38%. Industries such as construction and mining are increasingly using AI engines that process more than 1.2 million image points per mission, strengthening data reliability and operational efficiency.

Rising Adoption of Drone-Based Environmental Monitoring: Environmental agencies and industrial operators are increasingly deploying drones for emissions tracking, biodiversity mapping, and water-quality inspection. Adoption grew by 52% in 2024, supported by sensors capable of analyzing over 20 chemical parameters in real time. Forest-monitoring programs report a 33% improvement in wildfire-risk detection due to enhanced thermal-imaging capabilities.

Growth in Industrial Asset-Inspection Robotics: Industrial sectors—especially utilities, oil & gas, and renewable energy—are integrating drone robotics to reduce manual inspections. In 2024, automated inspections contributed to 29% reduction in worker exposure to hazardous zones and 41% faster turbine-inspection cycles. Automated defect-classification tools now process up to 800 images per mission, supporting high-scale asset monitoring.

Surge in Urban Airspace Integration Technologies: Urban air-mobility planning is accelerating development of drone traffic-management (UTM) systems. In 2024, over 120 metropolitan regions adopted digital airspace coordination tools, reducing flight-path conflicts by 36%. The integration of geofencing, 5G-navigation positioning, and collision-avoidance sensors increased operational safety, supporting advanced delivery and surveillance deployments.

The Smart Drone Services Market is segmented across product types, applications, and end-user verticals, each reflecting distinct operational requirements and technology stacks. Types range from multirotor and fixed-wing platforms to hybrid VTOL, tethered systems, and ultra-small nano-drones; applications span asset inspection, mapping & surveying, delivery/logistics, agriculture, emergency response, and security; end users include utilities, oil & gas, construction, agriculture, logistics, public safety, and telecommunications. Decision-makers should note that segmentation drives procurement criteria (flight endurance, payload, sensor suite), commercial deployment models (subscription vs. project-based services), and regulatory engagement strategies. Adoption patterns show strong preference for inspection and mapping use cases in heavy industry, while delivery pilots proliferate in urban logistics. Technology advances in autonomy, onboard analytics, and connectivity are reshaping product mix and channel strategies, with differentiated value propositions emerging across service models and regions.

The market’s product-type mix is dominated by multirotor platforms, which account for approximately 52% of commercial smart-drone service deployments due to their vertical takeoff/landing flexibility, precise hover capability for inspections, and broad sensor compatibility. Fixed-wing platforms typically represent about 18%, favored for long-endurance mapping and corridor surveys; hybrid VTOL systems make up roughly 20% and are the fastest-growing segment, driven by demand for both endurance and VTOL convenience — estimated growth for hybrid VTOL stands near 12.2% CAGR over the medium term. Tethered drones and nano/micro platforms cover the remaining 10% combined, serving niche roles in persistent surveillance and close-proximity indoor inspections. Hybrid VTOL’s rapid uptake is propelled by improvements in battery energy density, modular payload integration, and regulatory pilots that permit extended-range operations. Multirotor’s leading position is reinforced by widespread operator familiarity, large certified pilot bases, and mature payload ecosystems (high-resolution RGB, multispectral, thermal, and LiDAR packages). Other types—tethered systems, nano-drones, and specialized fixed-wing variants—play niche roles with combined share of ~10%, often selected for persistent monitoring, extreme-range surveys, or indoor applications where larger platforms are unsuitable.

Inspection & monitoring remain the principal application area, accounting for roughly 36% of smart-drone service utilization, thanks to repeated, high-frequency needs in utilities, energy, and infrastructure. Mapping & surveying follow at about 22%, supporting construction, mining, and land-management projects, while delivery & logistics services now represent around 14%, showing the fastest growth supported by urban pilot programs and logistics automation initiatives — estimated growth for delivery/logistics stands near 11.5% CAGR. Agriculture, emergency response, and security/ surveillance together form the remaining 28%, with specialized sensor suites and analytics driving differentiated adoption. The leading position of inspection & monitoring is underpinned by measurable operational benefits: drone-enabled inspections reduce field crew exposure and compress inspection cycles, enabling higher-frequency condition assessments. Delivery/logistics is expanding rapidly due to investments in last-mile automation, regulatory pilots for BVLOS and UTM integration, and improved payload handling—trends that enable scalable commercialization. Mapping & surveying continues to benefit from enhanced LiDAR and photogrammetry sensor packages that increase point-cloud density and reduce post-processing time. Consumer and enterprise adoption statistics illustrate shifting behavior: in 2024, over 38% of infrastructure operators reported piloting drone-based inspection programs for predictive maintenance; and 60%+ of urban logistics pilots reported improved door-to-door transit times in trial environments.

Utilities are the single-largest end-user segment, representing roughly 30% of smart-drone service consumption, driven by needs for frequent line and substation inspection, storm-response assessment, and asset-condition monitoring. Oil & gas and renewable-energy operators collectively account for about 20%, employing drones for flare-stack inspections, turbine blade analysis, and offshore structure surveys. Construction and mining represent 18%, relying on high-precision mapping and progress-monitoring workflows. Logistics and e-commerce players compose around 12%, notably accelerating as delivery pilots scale; public safety and agriculture share the remaining 20% in combined contributions. The fastest-growing end-user category is commercial logistics and last-mile delivery, fueled by automation pilots, fleet-integration trials, and urban airspace management advancements — expected medium-term CAGR for logistics end-users is approximately 13.0%, reflecting rapid pilot-to-production transitions. Utilities’ leadership is supported by quantifiable operational outcomes: many utilities report double-digit reductions in outage-restoration times and measurable safety improvements after drone program deployment. Other end-users—construction, mining, public safety, and agriculture—collectively contribute around 40% of the market, each showing sector-specific adoption rates (e.g., construction firms report >40% adoption of drone surveys for site management in pilot-heavy markets). Adoption trends show enterprises moving from pilots to operational fleets: in 2024 more than 38% of large infrastructure firms reported transitioning from ad-hoc trials to formalized drone inspection programs, while surveys indicate over 60% of field-operations teams prefer analytics-integrated drone outputs for routine maintenance planning.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21.4% between 2025 and 2032.

North America maintained its leadership due to extensive commercial drone adoption in logistics, inspection, and defense, contributing a significant portion of the market’s estimated USD 18.7 billion global valuation in 2024. Europe followed with a 27% share, supported by strong regulatory alignment and enterprise drone usage. Asia-Pacific secured a 24% share, driven by major economies scaling their industrial drone ecosystems. South America and the Middle East & Africa captured 6% and 5%, respectively, with rising investments in agriculture, construction, and public safety. The distribution highlights a competitive landscape marked by rapid technical innovation and region-specific adoption patterns across industries such as energy, telecom, transportation, real estate, and public services.

The North America Smart Drone Services Market accounted for 38% of global share in 2024, supported by high adoption in sectors such as logistics, infrastructure inspection, oil & gas, precision agriculture, and public safety. The region benefits from strong demand across healthcare, finance, utilities, and retail, where enterprises increasingly rely on automation and real-time aerial data. Regulatory evolution—particularly streamlined FAA approval pathways for BVLOS (Beyond Visual Line of Sight) operations—has accelerated commercial drone integration. Technological upgrades in AI navigation, autonomous fleet management, and 5G-enabled drone connectivity further enhance performance. Local players such as Skydio expanded autonomous inspection deployments across utility networks, strengthening regional competitiveness. Consumer behavior trends show North American enterprises favoring high-precision, AI-driven drone intelligence, particularly in healthcare triage, financial risk monitoring, and emergency response digitalization.

Europe represented 27% of the global Smart Drone Services Market in 2024, with Germany, the UK, and France being the top contributors. Adoption is shaped by strict regulatory frameworks from bodies such as EASA, which emphasize airspace safety, sustainability, and responsible autonomy. Enterprises across manufacturing, smart cities, agriculture, and renewable energy have increased drone service utilization for emissions monitoring, asset mapping, and automated maintenance. The region’s strong sustainability initiatives—such as carbon reduction mandates and EU Green Deal digitalization programs—have boosted demand for precision-driven drone analytics. Local companies like Parrot Drones continue to advance secure enterprise-focused drone solutions. European consumer behavior shows an emphasis on regulated, explainable, and compliance-aligned aerial data intelligence, reflecting strong trust in structured governance frameworks.

Asia-Pacific held 24% of global volume in 2024, ranking as the fastest-growing regional market by 2025. China, India, and Japan lead regional consumption due to robust e-commerce ecosystems, manufacturing intensity, and advanced urban infrastructure. The region has seen rapid expansion of drone-enabled last-mile delivery, precision agriculture, and industrial surveillance. Innovation hubs in Shenzhen, Bengaluru, Seoul, and Tokyo are driving new developments in autonomous drone fleets, battery efficiency, swarm coordination, and AI mapping. Local players such as DJI expanded enterprise portfolios for construction, energy inspection, and logistics optimization. Consumer behavior across Asia-Pacific is strongly influenced by mobile-first adoption, rising e-commerce expectations, and integration of drones with real-time AI apps, fueling widespread operational use.

South America accounted for 6% of global market share in 2024, with Brazil and Argentina serving as major hubs. The region’s demand is driven by agriculture, mining, energy transmission, and environmental monitoring. Expanding renewable energy grids and infrastructure modernization programs contribute to rising deployment of smart drone inspection services. Governments have increasingly introduced incentives for digital agriculture and cross-border tech cooperation. Local players such as Speedbird Aero have piloted autonomous delivery solutions, supporting logistics expansion in remote regions. South American consumer behavior shows strong alignment with localized content, media capture, and language-specific drone applications, boosting adoption across entertainment, surveying, and commercial industries.

The Middle East & Africa region captured 5% of global market share in 2024, driven by strong uptake in oil & gas monitoring, industrial construction, security applications, and smart city programs. Countries such as the UAE, Saudi Arabia, and South Africa led implementation efforts, leveraging drones for large-scale infrastructure mapping, pipeline inspection, and urban development projects. Technological modernization initiatives—including digital transformation strategies, advanced surveillance platforms, and automated asset management—have strengthened demand. Regulatory reforms enabling controlled airspace access have supported enterprise-scale drone operations. Local firms such as Falcon Eye Drones expanded service networks for government and commercial clients. Regional behavior trends indicate strong interest in high-reliability, security-focused drone intelligence, aligned with national development agendas.

United States – 32% Market Share: Dominance driven by strong commercial demand across enterprise logistics, utilities, and defense-led innovation.

China – 19% Market Share: Leadership supported by large-scale manufacturing ecosystems and rapid integration of drones into industrial and e-commerce operations.

The Smart Drone Services Market is characterized by a dynamic mix of specialist service providers, platform OEMs, and systems integrators competing across inspection, delivery, mapping, and public-safety segments. Today there are hundreds of active competitors globally—an estimated 400+ service providers and 1,000+ OEMs/integrators supporting enterprise deployments and bespoke solutions. The market displays a moderately consolidated structure at the top with the leading vendors occupying meaningful, defendable positions while the long tail remains highly fragmented by geography and vertical. Strategic initiatives in 2023–2024 included large-scale partnerships (e.g., public-safety system integrations), targeted product launches for enterprise inspection and BVLOS-ready platforms, and M&A activity focused on software/analytics capabilities. Key facts and figures to frame competitive intensity: roughly 5 global leaders account for a ~50–55% combined share of the commercial smart-drone services revenue pool, while the remaining 45–50% is split among regional specialists and new entrants. Innovation is concentrated in autonomy (single-operator, multi-drone control), onboard AI (real-time defect detection and thermal analysis), BVLOS enabling stacks, and UTM/airspace-integration solutions. Market positioning ranges from platform-first (hardware + cloud) to software-centric players offering subscription analytics; many incumbents now pursue recurring-service contracts to improve lifetime value. For decision-makers this means procurement is shaped by vendor roadmaps for autonomy, data-ops integrations, global regulatory footprints, and demonstrated large-scale program performance.

Terra Drone

Parrot

AeroVironment

Delair

Flyability

Current and emerging technologies are rapidly reshaping capabilities and procurement criteria for smart drone services. Autonomy stacks now support single-operator control of multiple platforms, with onboard compute budgets commonly in the 5–20 TOPS range for advanced vision processing; this enables real-time object detection, classification and closed-loop navigation. LiDAR and photogrammetry sensors continue to improve point-cloud density—commercial systems now capture hundreds to over 1,000 points/m² in survey missions—delivering finer geometry for digital-twin and BIM workflows. Edge AI and onboard analytics reduce data-backhaul needs by performing pre-processing locally (e.g., anomaly flagging, thermal threshold alerts), cutting downstream data-processing loads by an estimated 20–40% in mature deployments. Communications advances—5G low-latency links (<10 ms) and hybrid SAT/mesh fallback—are enabling stable BVLOS command-and-control and live telemetry over longer ranges. Swarm coordination algorithms and cooperative flight-management are moving from lab trials to pilot deployments, enabling coordinated inspection of linear assets and large sites; typical coordinated missions now support 5–20 drones under centralized tasking in experimental production trials. Power innovations focus on higher energy-density batteries (improving flight times from typical 20–40 minutes to 60–120 minutes for long-endurance platforms) and alternative energy solutions (fuel-cell/hybrid) for heavy-payload or long-range missions. Payload miniaturization drives multi-sensor fusion—RGB, multispectral, thermal, and compact LiDAR—into single missions, increasing data richness per sortie. Software trends include standardized APIs for data ingestion into asset-management suites, federated data governance for privacy, and integrated UTM/airspace services to automate deconfliction. Cybersecurity hardening (signed firmware, secure telemetry, encrypted telemetry links) has become a procurement must for critical-infrastructure clients, and vendor roadmaps increasingly promise certified compliance with national drone-operational frameworks. Collectively, these technology advances are shifting the value proposition from single-flight capture toward recurring, analytics-driven service contracts that integrate with enterprise workflows.

In 2024, Zipline reached its one-millionth commercial autonomous drone delivery milestone and expanded U.S. service partnerships with several large retailers and health systems, underpinning scale-up in last-mile medical and consumer deliveries. Source: www.zipline.com

In July 2024, Terra Drone entered a joint R&D agreement with MODEC to develop inspection drones for FPSO (Floating Production, Storage and Offloading) systems, targeting fully unmanned internal and external inspections for offshore assets. Source: www.terra-drone.net

In mid-2024, Skydio and Axon announced a comprehensive Drone-as-First-Responder (DFR) solution, integrating autonomous Skydio platforms with Axon public-safety systems to accelerate DFR program deployment and real-time situational awareness for law-enforcement and fire agencies. Source: www.skydio.com

In 2024, Parrot reported strong 2024 operational performance with significant growth in its professional UAV business across Europe, reflecting increased enterprise adoption for photogrammetry and inspection workflows during the year. Source: www.parrot.com

This report covers the end-to-end Smart Drone Services Market landscape, from hardware platform typologies and payload integrations to software analytics, managed service models, and regulatory-enabled operational frameworks. Geographically, the scope spans all major regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—analyzing country-level demand drivers, infrastructure readiness, and regional technology hubs. Segment coverage includes product types (multirotor, fixed-wing, hybrid VTOL, tethered, micro/nano), payload categories (RGB, thermal, multispectral, LiDAR, gas sensors), service models (project-based surveys, recurring inspection subscriptions, delivery/logistics, emergency-response fleets), and end users (utilities, oil & gas, construction & mining, agriculture, logistics/e-commerce, public safety, telecom). The report also addresses enabling components such as BVLOS authorizations, UTM/UTM-to-enterprise integrations, 5G and satellite connectivity, edge-AI processing, and airspace governance models. Technology coverage extends to autonomy stacks, sensor fusion, swarm coordination, powertrain innovations (battery and hybrid systems), and cybersecurity controls essential for critical infrastructure customers. Operational scope includes procurement considerations, vendor selection criteria, deployment case studies, program-level KPIs (inspection throughput, mean time to detect anomalies, mission turnaround time), and service commercialization models (subscription, managed services, platform licensing). Additionally, niche and emerging segments—urban air mobility interfaces, drone-based environmental monitoring programs, and specialized indoor/industrial inspection services—are examined for near-term commercialization potential. The report is structured to inform commercial strategy, vendor selection, regulatory engagement, and investment decisions for executives, procurement officers, and technical program managers seeking a comprehensive, actionable view of the smart-drone services ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,902.6 Million |

| Market Revenue (2032) | USD 4,019.4 Million |

| CAGR (2025–2032) | 9.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, End-User Behavior Analysis, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | DJI Enterprise, Skydio, Zipline, Terra Drone, Parrot, AeroVironment, Delair, Flyability |

| Customization & Pricing | Available on Request (10% Customization Free) |