Reports

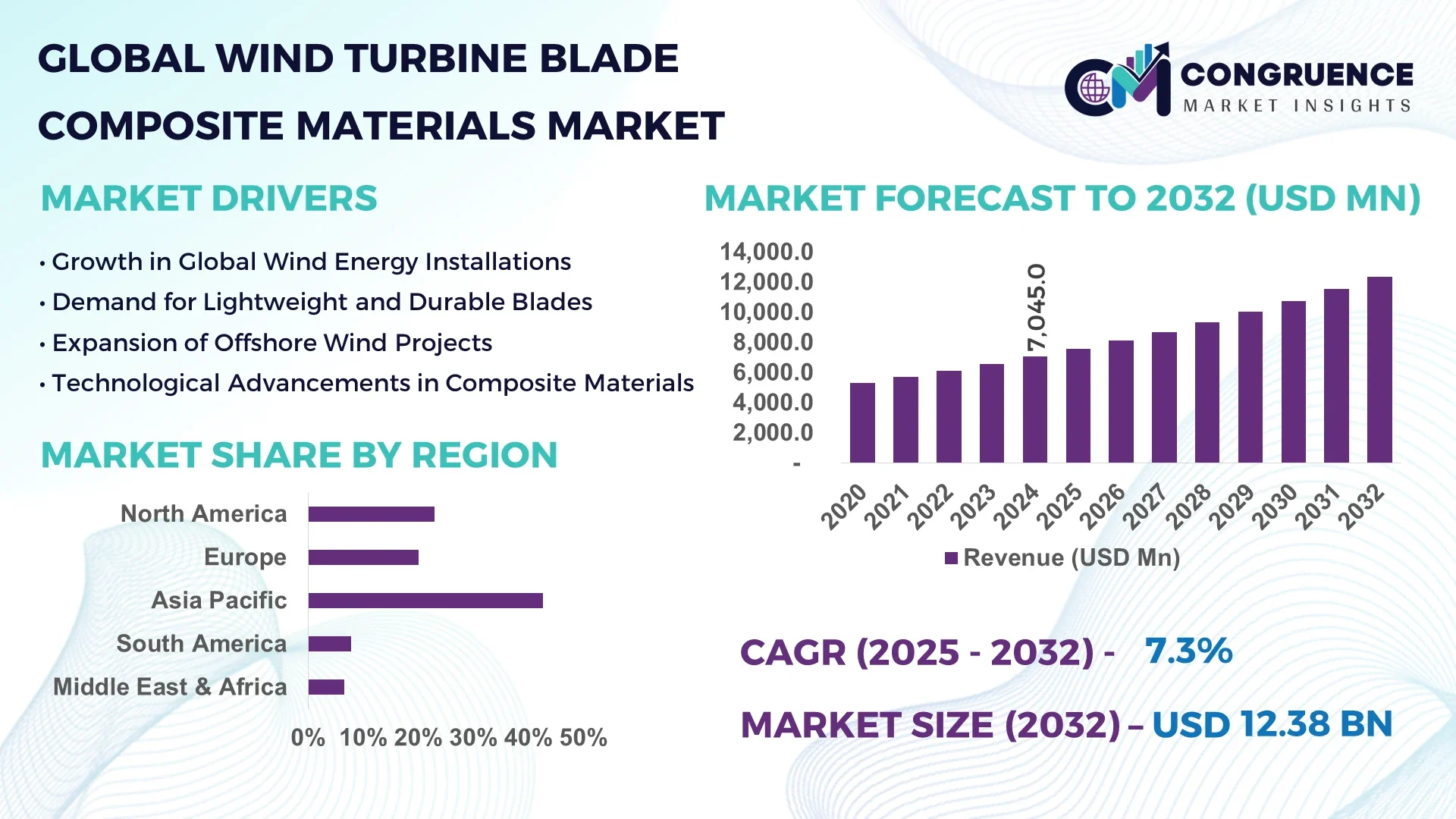

The Global Wind Turbine Blade Composite Materials Market was valued at USD 7,045 Million in 2024 and is anticipated to reach a value of USD 12,378.8 Million by 2032 expanding at a CAGR of 7.3% between 2025 and 2032.

China leads the Wind Turbine Blade Composite Materials Market, with an annual composite blade production capacity exceeding 35 GW, supported by record investment of over USD 18 billion in 2024. The country hosts multiple manufacturing hubs and R&D centers focusing on high-modulus carbon-fiber blades and advanced resin infusion technologies, which supply both domestic and global offshore wind projects.

The Wind Turbine Blade Composite Materials Market is characterized by strong engagement across utility-scale and offshore wind sectors. Glass-fiber composites dominate, though carbon-fiber blades are increasingly used for larger rotor diameters. Recent innovations include automated fiber placement and resin transfer molding, reducing cycle times by 15–20%, while hybrid thermoplastic prepregs are enhancing recyclability. Regulations in Europe and North America are steering the market toward eco-friendly composites and automated manufacturing. Regional demand varies—Asia Pacific focuses on cost-efficient mass production, Europe emphasizes high-performance offshore blades, and North America is expanding domestic supply chains. Growing trends include sensor-embedded blades for real-time health monitoring and development of thermoplastic recycling programs. The future outlook includes rising demand for recyclable blade composites, digitalized manufacturing with Industry 4.0 systems, and expanded regional manufacturing footprints to support larger blade sizes and offshore capacity build-out.

Artificial intelligence is increasingly embedded in manufacturing, quality assurance, and performance optimization processes across the Wind Turbine Blade Composite Materials Market. AI-driven layup planning tools now analyze blade geometry and fiber orientation to create optimal plies, improving material utilization by up to 12%. In production, computer vision and machine learning inspect fiber alignment, resin saturation, and microcracks in real time, reducing defect rates by approximately 30%. Additionally, digital twins of composite curing ovens use predictive algorithms to control temperature and pressure profiles, ensuring consistent resin polymerization and reducing cycle variations across batches. These AI systems also analyze vibration and structural sensor data from installed blades to forecast fatigue damage and trigger targeted maintenance, thus extending blade lifespan by an estimated 8%.

Overall, the Wind Turbine Blade Composite Materials Market is benefiting from AI systems that integrate across the value chain—design, manufacturing, inspection, and in-field monitoring—enhancing efficiency, reliability, and cost control. Manufacturers report reduced waste from overuse of resin and fibers, and procurement teams use AI forecasting to align material purchases with project timelines, minimizing inventory costs. Industrial IoT platforms, powered by machine learning, optimize layup schedules and mold turnaround times, boosting throughput without additional floor-space investments. Decision-makers in this market are increasingly prioritizing AI as a core enabler for accelerated, scalable, and data-driven production of composite blade components.

“In mid‑2024, Siemens Gamesa implemented an ML‑based resin monitoring system in its Aalborg blade plant, enabling detection of resin voids during curing and cutting scrap rates by 22% per batch.”

The Wind Turbine Blade Composite Materials Market is shaped by escalating global wind installations, evolving regulatory expectations, and advancing composite technologies. Eliminating fossil fuels and meeting renewable mandates are pushing turbine sizes upward, necessitating higher-performance composite solutions. At the same time, sustainability regulations mandate recyclable or bio‑resins, prompting material innovation. Supply chain localization—such as onshore production in North America under domestic-content incentives—is intensifying competition and investment. Meanwhile, labor shortages and inflationary cost dynamics are accelerating automation in composite layup and inspection. Cost-parity pressures drive consolidation among composite suppliers and blade OEMs. Sectors under strain include offshore wind, where materials must resist extreme marine conditions, and utility-scale onshore farms where modular logistics impact composite design. Overall, the market is evolving toward digitalized, sustainable, and geographically diversified production.

Rapid expansion of large-scale wind projects is heavily impacting the Wind Turbine Blade Composite Materials Market. In 2024, offshore turbine blade lengths surpassed 90 meters, requiring high-modulus composites and precision molding techniques capable of supporting increased aerodynamic loading. Manufacturing data shows that composites for offshore blades must meet 25% higher fatigue load resistance than onshore counterparts. As a result, demand for epoxy-carbon composite laminates has surged, while suppliers ramp production lines and automated layup stations. This shift is enabling economies of scale and pushing manufacturers to invest in large-format molds and high-capacity prepreg systems.

The Wind Turbine Blade Composite Materials Market faces notable challenges due to rising capital expenditures and material reliance on global suppliers. Establishing a single automated blade layup line can cost upwards of USD 15 million, while specialized molds for long-span blades exceed USD 5 million each. Additionally, composite raw materials—especially carbon fiber and high-grade resins—depend on a geographically limited supply base, leading to lead times of 20–30 weeks. In 2024, shipments of epoxy resins experienced a 40% surge in spot prices due to disruptions in Asia. These factors pressure margins and discourage new entrants, impeding the market’s ability to rapidly scale with demand.

Emerging recyclable composites represent a strategic opportunity within the Wind Turbine Blade Composite Materials Market. In 2024, three global OEMs conducted pilot blade production using thermoplastic fiber reinforcements with reversed thermal debonding. These blades demonstrated a 70% reduction in end-of-life composite waste, and trial installations reported an identical stiffness coefficient to traditional composites. As regulators increase blade disposal mandates in Europe and North America, suppliers with certified recyclable composites expect new contracts and long-term procurement agreements. The market is seeing growing interest in bio-based epoxy resins and thermoplastic recycling infrastructure, positioning these innovations as competitive differentiators.

The Wind Turbine Blade Composite Materials Market is contending with evolving regulatory standards and prolonged certification timelines. In Europe, updated composite flame-retardancy rules mandated stricter smoke-toxicity limits beginning in 2024. Suppliers were required to revise resin formulations to comply, costing several million dollars and extending certification timelines by nine to twelve months. These delays directly affect project schedules and procurement cycles. Additionally, structural certifications for new composite blends now require expanded fatigue testing—typically doubling test duration. Consequently, OEMs face certification bottlenecks when introducing next-gen composite technologies, slowing down market adoption and limiting product roll-out windows.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Wind Turbine Blade Composite Materials Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Growth of Embedded Sensor Technology: Blade OEMs are increasingly integrating fiber-optic strain gauges and piezoelectric sensors directly into composite layers. In 2024, approximately 18% of newly delivered blades included embedded monitoring systems, enabling predictive fatigue analysis and reducing unplanned maintenance events by 14%.

Automation in Layup Stations: Robotic fiber placement and automated resin dispensing are now installed in over 60% of European blade facilities. This shift has cut manual layup time by 35% and improved dimensional accuracy by +/- 0.5 mm, enabling consistent composite quality across large blade segments.

Thermoplastic Prepreg Adoption for Recyclability: Thermoplastic prepreg materials comprised 12% of new blade composites in 2024, up from 5% in 2023. These materials allow heat-based separation of fiber and resin during end-of-life recycling, offering a 50% lower carbon footprint compared to conventional thermoset composites and aligning with sustainability regulations.

The Wind Turbine Blade Composite Materials Market is segmented into three critical categories: type, application, and end-user. This structure allows for detailed insights into material innovations, sectoral adoption patterns, and industry-specific demands. By type, the market includes various fiber and resin-based composites such as glass fiber, carbon fiber, and hybrid materials. Application-wise, the focus lies in onshore and offshore wind deployments, each with differing technical and environmental requirements. End-user segmentation reveals the demand concentrations from utility providers, independent power producers (IPPs), and EPC (engineering, procurement, and construction) contractors. The segmentation analysis provides stakeholders with essential knowledge to align production strategies, sourcing, and investment planning in response to the market's evolving technological and structural demands.

Glass fiber composites continue to dominate the Wind Turbine Blade Composite Materials Market due to their cost-effectiveness, robust mechanical properties, and ease of processing. These materials are widely adopted for both onshore and medium-sized offshore blades, often using epoxy resins for durability and load-bearing performance. Carbon fiber composites, although more expensive, are the fastest-growing segment. Their use is driven by the increasing size of offshore turbines, where higher strength-to-weight ratios and fatigue resistance are critical. Carbon fiber blades help reduce nacelle loads and allow for larger rotor diameters, contributing to improved energy capture. Hybrid composites—blending glass and carbon fibers—serve a niche but important role in enhancing performance while controlling material costs. Thermoplastic composites, though still emerging, are gaining attention for their recyclability and potential to reduce end-of-life blade waste. Each material type aligns with different design strategies, regional standards, and turbine sizes, making material selection a core strategic decision for blade manufacturers.

Onshore wind applications lead the market, largely due to the sheer number of installations and the ongoing expansion of wind farms in land-rich countries. These applications favor glass fiber composites due to their cost-efficiency and proven reliability in standard climate conditions. Offshore wind is the fastest-growing application segment, driven by government-backed offshore wind initiatives in Europe, China, and the U.S. Offshore installations demand superior blade materials with higher resistance to saline corrosion, humidity, and extreme wind loading. Consequently, carbon fiber and high-modulus epoxy systems are seeing increased deployment in offshore applications. Other application areas include small-scale distributed wind turbines and research prototypes, which serve educational, R&D, or localized power needs. These smaller-scale applications typically use simplified composite systems and manual manufacturing techniques. The growing trend toward offshore megaprojects, coupled with rising demand for larger and more efficient turbines, is shaping the application mix and setting new material performance benchmarks across regions.

Utility companies represent the leading end-user segment in the Wind Turbine Blade Composite Materials Market, benefiting from vertically integrated operations that allow them to influence blade design, performance parameters, and sourcing decisions. These organizations prioritize material reliability, blade lifespan, and aerodynamic performance to maximize energy generation over project lifecycles. Independent Power Producers (IPPs) are the fastest-growing end-user group, driven by a surge in private renewable energy investments and public-private partnership models. IPPs often seek advanced materials that reduce maintenance frequency and optimize return on investment, particularly in offshore projects. EPC contractors also form a significant end-user segment, especially in markets where turnkey wind farm projects are common. Their role includes selecting blade suppliers based on project-specific criteria such as environmental exposure, transport constraints, and compliance with local content regulations. Collectively, these end-users shape procurement strategies, influence technological adoption, and determine the operational priorities of the composite material supply chain.

Asia-Pacific accounted for the largest market share at 42.7% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

The Wind Turbine Blade Composite Materials Market is seeing a sharp regional shift as installation capacity, regulatory frameworks, and investment in clean energy continue to evolve. Asia-Pacific leads due to strong demand in China and India, backed by large-scale turbine production hubs and export-oriented manufacturing. North America’s accelerated growth is being driven by policy incentives, domestic production expansion, and rising offshore wind investments. Europe holds a significant share, bolstered by offshore wind infrastructure and strict sustainability mandates. Meanwhile, emerging markets across Latin America, the Middle East, and Africa are scaling up investment in renewable energy infrastructure, contributing to expanding demand for advanced composite materials in turbine blades.

North America held approximately 23.6% of the global Wind Turbine Blade Composite Materials Market in 2024, with the U.S. leading regional demand due to its expanding offshore wind projects in states like New York and Massachusetts. Key industries driving this demand include utility-scale renewable energy providers and offshore wind developers partnering with global OEMs. The Biden administration’s goal to deploy 30 GW of offshore wind by 2030 has prompted federal and state-level incentives for blade production and port-side manufacturing. Digital transformation is accelerating, with U.S.-based facilities integrating AI-enabled defect detection and robotic fiber placement systems. Additionally, the enforcement of the Inflation Reduction Act has spurred capital investment into domestic composite supply chains and infrastructure upgrades, further strengthening the region’s capacity for long-span, high-performance blade production.

Europe captured around 28.3% of the global Wind Turbine Blade Composite Materials Market in 2024. Germany, the UK, and France remain the dominant markets, largely due to their leadership in offshore wind energy and green technology adoption. The European Commission's Fit for 55 initiative and local sustainability policies are enforcing the use of recyclable and low-emission composite materials. France has expanded its offshore wind zones, while Germany’s northern coastline has become a manufacturing hub for turbine blades and nacelle assemblies. Across the region, AI-driven process optimization and the adoption of thermoplastic composites are being prioritized for recyclability and structural efficiency. Europe's regulatory environment fosters innovation in carbon-fiber reinforced systems, particularly in floating wind applications, where lighter, stronger blades are essential.

Asia-Pacific led the Wind Turbine Blade Composite Materials Market by volume in 2024, accounting for approximately 42.7% of global demand. China dominates regional consumption, followed by India and Japan. China’s high-output composite blade manufacturing facilities supply both domestic installations and export markets. India’s Make-in-India initiative has attracted investments in turbine component production, especially for onshore projects across Gujarat and Tamil Nadu. Technological advancements include infusion molding with bio-resins and smart blade systems using embedded sensors for predictive maintenance. Innovation hubs in China and South Korea are pushing R&D in recyclable materials and hybrid fiber technologies. With extensive infrastructure and lower labor costs, Asia-Pacific continues to be the global production engine for composite wind blades.

South America represented 3.9% of the Wind Turbine Blade Composite Materials Market in 2024, with Brazil leading regional demand. The country’s wind-rich northeastern states have witnessed rapid onshore project approvals, fueling domestic blade manufacturing. Argentina is following suit with state-supported energy transition programs. Infrastructure development in coastal zones is boosting interest in localized blade production, while hybrid energy parks combining wind and solar are creating new market opportunities. Brazil’s recent tax exemptions on renewable energy components have attracted international OEMs and composite suppliers. While currently focused on glass fiber composites, the region is showing interest in scalable thermoset-to-thermoplastic transitions to align with global recycling initiatives.

The Middle East & Africa region contributed 1.5% to the global Wind Turbine Blade Composite Materials Market in 2024. UAE and South Africa are at the forefront of renewable diversification efforts. UAE’s investment in green hydrogen and wind capacity is prompting demand for lightweight, high-durability blade materials. South Africa’s Renewable Energy IPP Procurement Programme (REIPPPP) is catalyzing regional manufacturing partnerships. Oil-rich nations such as Saudi Arabia are launching clean energy projects under Vision 2030, indirectly boosting demand for advanced composite components. Technological modernization across the region includes smart turbine deployments and digital twin simulation systems. Local trade agreements and free zones are helping global composite suppliers establish low-cost manufacturing bases to serve African and Middle Eastern markets.

China – 38.2% Market Share

High production capacity and large-scale blade export infrastructure support its leading position in the Wind Turbine Blade Composite Materials Market.

Germany – 12.4% Market Share

Advanced engineering capabilities and robust offshore wind expansion fuel its dominance in blade composite adoption and innovation.

The Wind Turbine Blade Composite Materials Market is characterized by a moderately consolidated competitive landscape with over 50 actively operating global and regional manufacturers. These players range from large-scale composite producers to specialized material innovators focusing on epoxy systems, fiber reinforcements, and automation solutions. Market leaders are strategically positioned based on production scale, proximity to major turbine OEMs, and proprietary technology portfolios. Mergers and acquisitions have intensified since 2023, particularly in Europe and Asia, with companies aiming to vertically integrate resin formulation, fiber processing, and blade fabrication capabilities.

Strategic initiatives such as joint ventures between composite manufacturers and turbine OEMs have become more common, with recent partnerships centered on recyclable thermoplastic blade programs and automation in fiber layup. Product innovation is a key differentiator, with competitors investing in materials that reduce blade weight by up to 20% without sacrificing strength. Additionally, digital transformation—through AI-powered defect detection and digital twin modeling—is influencing market entry and reshaping operational benchmarks. The drive to localize manufacturing and reduce lead times in the wake of global supply chain disruptions is further shaping competitive dynamics, especially in North America and Asia-Pacific.

TPI Composites Inc.

LM Wind Power (a GE Renewable Energy business)

Sinoma Wind Power Blade Co., Ltd.

Gurit Holding AG

Hexcel Corporation

Toray Industries, Inc.

Mitsubishi Chemical Group

Teijin Limited

Nordex SE

Siemens Gamesa Renewable Energy S.A.

Vestas Wind Systems A/S

Zhongfu Lianzhong Composites Co., Ltd.

BFG International

Technological advancements are playing a pivotal role in shaping the Wind Turbine Blade Composite Materials Market. A major focus is on high-modulus carbon fiber, which provides superior strength-to-weight ratios, enabling the design of longer and lighter blades suitable for offshore wind environments. In 2024, manufacturers reported a 15% increase in production of carbon fiber-based blades for turbines exceeding 12 MW in capacity.

Thermoplastic composite systems are emerging as a sustainable alternative to traditional thermosets. These materials allow for heat-based reshaping and recycling, significantly reducing waste from end-of-life blades. Pilot programs in Europe and North America have successfully tested thermoplastic resins in full-scale blade segments, offering faster curing times and lower embodied carbon.

AI-powered process automation is now widely integrated into blade manufacturing, including automated fiber placement (AFP), machine vision-based quality control, and digital twin simulation. These technologies have improved production efficiency by 20–25% while reducing material scrap rates by up to 18%.

Other innovations include resin infusion techniques using bio-based epoxies, structural health monitoring sensors embedded into blade laminates, and robotic trimming and sanding. Collectively, these technologies are improving composite reliability, enabling customization at scale, and aligning with evolving environmental compliance standards across global regions.

• In February 2024, TPI Composites launched a next-generation modular blade platform in India, integrating AI-based resin infusion monitoring and cutting material waste by 16% compared to traditional processes.

• In August 2023, Vestas introduced a recyclable blade prototype using thermoplastic resin developed in partnership with a European materials lab. The blade passed fatigue testing standards for 11 MW turbines.

• In May 2024, Gurit opened a new 60,000 sq. ft. prepreg facility in the U.S. Midwest to supply North American blade OEMs, with an annual output capacity of 4,500 metric tons of composite materials.

• In October 2023, LM Wind Power completed a full-scale field trial of a smart blade embedded with fiber-optic sensors that monitor real-time wind load distribution, improving turbine efficiency in fluctuating wind conditions.

The Wind Turbine Blade Composite Materials Market Report offers a comprehensive analysis of the global landscape across multiple critical dimensions. It covers composite types such as glass fiber, carbon fiber, hybrid fibers, thermoset and thermoplastic resins, and advanced structural core materials. The report segments the market based on application areas, including onshore wind, offshore wind, and small-scale distributed turbines.

Geographically, the report analyzes trends and demand dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with specific insights into key countries such as China, Germany, the U.S., India, and Brazil. Additionally, it explores end-user categories like utility providers, independent power producers, and EPC contractors.

A focus is placed on technology adoption, such as automated layup, bio-based resins, embedded sensors, AI-driven manufacturing systems, and recyclability initiatives. The report also highlights sustainability trends, regional regulations, and energy infrastructure developments influencing the market's evolution. Furthermore, niche areas such as recyclable blade innovation and floating wind-specific composite requirements are explored, offering decision-makers actionable insights into current and future opportunities across this dynamic sector.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 7,045.0 Million |

| Market Revenue (2032) | USD 12,378.8 Million |

| CAGR (2025–2032) | 7.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | TPI Composites Inc., LM Wind Power (a GE Renewable Energy business), Sinoma Wind Power Blade Co., Ltd., Gurit Holding AG, Hexcel Corporation, Toray Industries, Inc., Mitsubishi Chemical Group, Teijin Limited, Nordex SE, Siemens Gamesa Renewable Energy S.A., Vestas Wind Systems A/S, Zhongfu Lianzhong Composites Co., Ltd., BFG International |

| Customization & Pricing | Available on Request (10% Customization is Free) |