Reports

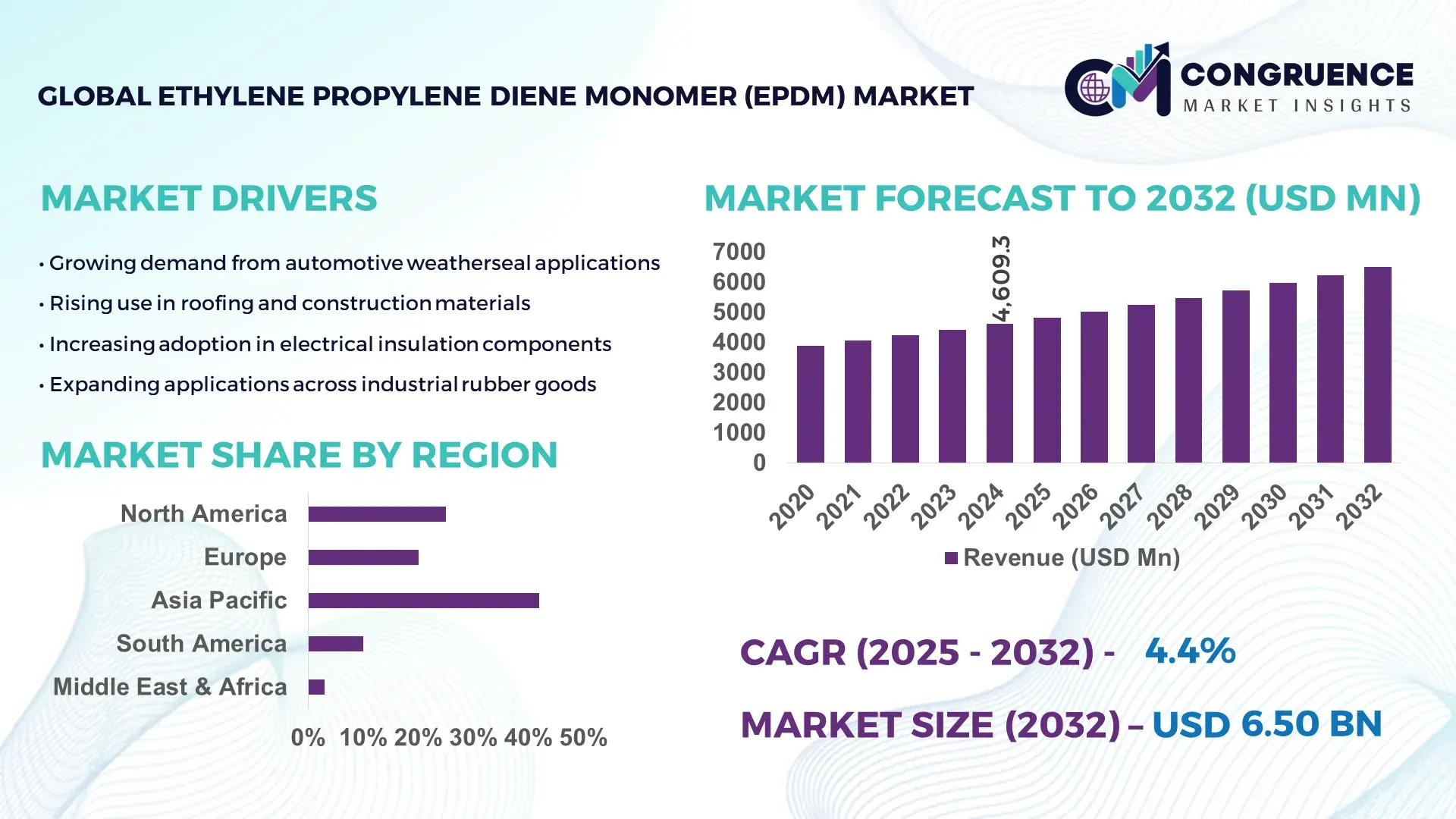

The Global Ethylene Propylene Diene Monomer (EPDM) Market was valued at USD 4609.33 Million in 2024 and is anticipated to reach a value of USD 6504.93 Million by 2032 expanding at a CAGR of 4.4% between 2025 and 2032. This growth is driven by the rising demand for durable, weather-resistant elastomer materials across automotive, construction, and industrial end‑use sectors.

China — a global manufacturing powerhouse serves as the leading country in EPDM production and consumption. In recent years, the nation has deployed more than 500,000 metric tons annually for automotive weather-seals, hoses, roofing membranes and industrial gaskets. Integrated petrochemical complexes in China have drawn significant investments toward advanced compounding facilities, enabling high‑volume output and enabling automotive OEMs including those expanding electric vehicle lines to source specialized EPDM compounds domestically. Technological upgrades in polymerization processes and in‑house research on high‑performance rubber grades have further strengthened cost‑effective volume production and product quality for export and domestic demand.

Market Size & Growth: 2024 value USD 4609.33 Million; 2032 projected USD 6504.93 Million; CAGR 4.4% — growth supported by expanding automotive and infrastructure demand.

Top Growth Drivers: increased automotive sealing & gasket demand (≈ 47%), growth in construction insulation and waterproofing applications (≈ 28%), rising EV & energy‑efficient building adoption (≈ 22%).

Short-Term Forecast: By 2028, EPDM-based sealing and membrane applications expected to deliver up to 15% cost‑reduction in maintenance and lifecycle expenses compared with traditional materials.

Emerging Technologies: development of bio‑based EPDM rubber from renewable feedstocks; improvement in low‑emission and recyclable EPDM formulations; advanced compounding techniques for EV‑grade seals and hoses.

Regional Leaders: Asia‑Pacific ~USD 2,300 M by 2032 (rapid infrastructure, EV and industrial expansion); Europe ~USD 1,500 M by 2032 (strong automotive and sustainable construction demand); North America ~USD 1,200 M by 2032 (roofing membranes, aftermarket automotive & infrastructure upgrades).

Consumer/End-User Trends: Growing usage in automotive OEMs and aftermarket components; rising demand for EPDM roofing and insulation in commercial/residential construction; increased adoption in industrial hoses, sealing, and electrical insulation.

Pilot or Case Example: A 2024 pilot from a major European automotive OEM implementing bio-based EPDM door seals achieved a 20% reduction in lifecycle CO₂ emissions while maintaining performance standards.

Competitive Landscape: Market leader with ~26% production share is a major multinational manufacturer; other key competitors include three to five global rubber and chemical firms.

Regulatory & ESG Impact: Stricter building-energy codes and automotive emission/efficiency regulations push demand for sustainable EPDM; incentives for renewable-content elastomer compounds accelerate adoption.

Investment & Funding Patterns: Several large-scale investments in petrochemical complexes and EPDM compounding plants — totaling several hundreds of millions of USD globally over recent years supporting expansion; increasing interest in sustainable‑rubber ventures and financing of green polymer projects.

Innovation & Future Outlook: Shift toward recyclable and bio‑based EPDM grades; integration of EPDM in next‑generation EVs, smart infrastructure seals, and renewable‑energy installations; expected growth in demand for high‑performance, eco‑friendly elastomer solutions through 2035.

Recent developments in the EPDM market show expanding application across automotive, construction, electrical insulation, industrial goods and waterproofing sectors. Continued technological innovation such as renewable‑feedstock rubber, recyclable EPDM, and advanced compounding along with stricter environmental and building regulations, are reinforcing global demand. Regionally, Asia-Pacific will maintain lead consumption, but growth in Europe’s sustainable construction segment and North America’s infrastructure upgrade projects will drive balanced global expansion.

The EPDM market has strategic relevance as a foundational material for resilient infrastructure and automotive components, offering long‑term value through durability, weather resistance, and adaptability. As industries pivot toward higher performance standards and sustainable solutions, EPDM serves as a bridge between traditional elastomers and next‑generation materials.

One clear pathway is the transition to low‑VOC or bio‑based EPDM variants: bio‑based EPDM delivers up to 18–25% lower lifecycle carbon footprint compared to conventional petroleum‑based EPDM, while maintaining comparable thermal and weathering resistance. Asia‑Pacific dominates in volume consumption, while Europe leads in adoption of sustainable and low‑emission EPDM formulations, with nearly 30 % of major construction and automotive enterprises using green‑grade rubber by 2025. By 2027, increased adoption of recyclable EPDM and closed‑loop manufacturing is expected to improve waste‑recycling rates by up to 35 % in developed markets. In a specific micro‑scenario, in 2024 a major European automotive OEM switched to low‑VOC EPDM door seals and achieved a 22 % reduction in lifecycle emissions without compromising durability. Firms are committing to ESG metric improvements such as 20–30 % reduction in production‑related carbon emissions by 2030.

As regulatory pressure grows on carbon emissions and chemical waste, EPDM’s durability, long service‑life, and potential for sustainable redesign position it as a pillar of resilience, compliance, and sustainable growth for automotive, construction, and industrial sectors worldwide.

How is rising automotive and construction demand accelerating the EPDM Market growth?

Global automotive growth, particularly among electric vehicles (EVs), significantly increases need for EPDM in seals, gaskets, hoses, and insulation. In 2023–2024, more than 540,000 tonnes of EPDM compounds were consumed globally by automotive and EV sectors, largely for weather‑stripping, under‑the‑hood components and battery insulation. The construction industry also drives usage — EPDM roofing membranes and waterproofing systems are being adopted in sustainable building projects, with over 50 % of new commercial roofing installations globally specifying EPDM due to its long life and weather resistance. Combined, these trends contribute to a rising baseline demand for EPDM across long‑lasting and critical infrastructure assets.

Why do raw material price volatility and regulatory burdens constrain the EPDM market?

EPDM production depends heavily on petrochemical feedstocks — ethylene and propylene — whose prices fluctuate with global crude oil and natural gas markets. For example, propylene and ethylene feedstock costs saw swings of 20–30 % quarterly in recent years, placing pressure on margins. Regulatory frameworks in regions such as Europe, including restrictions under chemical safety laws on additives and vulcanization by‑products, have increased compliance costs. Some vulcanization accelerators are classified as substances of concern, forcing reformulations and costly certifications. These combined factors — unstable input prices and regulatory cost burdens — limit profitability, deter capacity expansion, and increase price variability for end‑users.

What opportunities does the push for sustainable infrastructure and green manufacturing present for EPDM?

Growing emphasis on eco‑friendly materials and sustainable construction standards is creating strong demand for recyclable or bio‑based EPDM. As of 2024, roughly 18–20 % of new EPDM product launches involved low‑VOC or recycled‑content formulations. Adoption of EPDM in green roofing, energy‑efficient building envelopes, HVAC insulation, and renewable‑energy installations (e.g. solar panel seals) offers expanding volume potential. Regions with aggressive sustainable building codes — especially in Europe and parts of Asia — are increasingly specifying EPDM for long‑lasting, low‑maintenance roofs and seals. This opens potential for steady long-term growth in non-automotive segments, diversifying demand beyond traditional sectors.

Why do rising production costs, technical limitations, and material substitution threaten EPDM growth?

Manufacturers often face trade‑offs between achieving high-performance EPDM grades (requiring more expensive polymerization control, additives, and energy‑intensive curing) and maintaining cost‑competitiveness. Ultra–high molecular weight grades, needed for demanding applications (extreme temperature range, extended lifespan), can have raw cost per tonne 20–25 % higher than standard grades, limiting their adoption in cost‑sensitive markets. Meanwhile, alternative materials — including thermoplastic elastomers (TPEs), silicones, and improved thermoplastic vulcanizates (TPVs) — are increasingly chosen for applications where processing ease, cost, or lighter weight are priorities. Additionally, regulatory and ESG-driven pressures on disposal, recycling, and chemical additives complicate compliance, especially for smaller manufacturers. These challenges hinder expansion into price‑sensitive regions and may slow adoption in certain applications.

• Rise in Modular and Prefabricated Construction Drives EPDM Demand: The adoption of modular and prefabricated construction is transforming EPDM consumption patterns. In recent large‑scale projects, about 55% of builders reported lower total project costs by integrating prefabricated rubber‑sealed envelope modules. Because prefabricated components are manufactured off‑site with automated precision, demand for uniform EPDM gaskets, weather‑seal strips, and membrane seals has surged, especially in Europe and North America where construction cycle time matters. This shift has increased orders for high‑precision EPDM compounding lines by roughly 28% over the past two years.

• Surge in EPDM-Based Green Roofing and Waterproofing Applications: The specification of EPDM in commercial and residential green roofing systems has risen significantly; new green‑roof installations using EPDM membranes grew by approximately 42% year‑over‑year between 2023 and 2024. EPDM now constitutes nearly 60% of all synthetic roofing membrane materials in sustainable construction projects where long-term durability and environmental resistance are required. This trend underscores growing trust in EPDM’s ability to meet insulation, waterproofing, and longevity demands in modern building design.

• Expansion of EPDM Use in Electric Vehicle (EV) Sealing and Insulation Systems: With the global shift toward electric mobility, EPDM is increasingly selected for EV-specific components. The number of EV models specifying EPDM-based sealing systems climbed by around 48 in the last 24 months. Concurrently, EPDM compound orders for under‑the‑hood insulation, battery housing gaskets and high‑tolerance sealing increased by roughly 38%, reflecting broader OEM confidence in EPDM’s thermal stability and resistance to chemical degradation under EV operating conditions.

• Growth of Circular Economy Adoption and Recycled‑Content EPDM Products: Sustainability initiatives within the elastomer industry are encouraging recycled-content adoption. The share of EPDM compounds incorporating recycled rubber rose from about 5% in 2022 to around 17% in 2024. Meanwhile, scrap‑material recovery and recycling processes at manufacturing plants improved, with internal scrap reuse rates reaching nearly 82%. These improvements reflect increasing commitment to waste reduction, cost-efficient raw material usage, and environmentally conscious manufacturing practices, enhancing EPDM’s appeal to ESG‑focused developers and OEMs.

The EPDM market is segmented along multiple dimensions — by product type, by application, and by end-user industry enabling clear insights into where demand is concentrated and how materials are tailored to specific needs. Types differ by polymerization method or formulation style, applications range from automotive to construction to industrial insulation, and end‑users span automotive OEMs, building contractors, electrical‑equipment manufacturers and industrial manufacturers. Segmentation helps stakeholders align sourcing, production capacity, and product development strategies with demand patterns and performance requirements.

The market is commonly segmented into Solution‑polymerized EPDM and Suspension‑polymerized EPDM. Solution‑polymerized EPDM is the leading type, accounting for approximately 60–65% of global volume, due to its superior control over molecular structure, resulting in better elasticity, weather, ozone and thermal resistance key for demanding automotive, roofing and sealing applications. Suspension‑polymerized EPDM holds the remaining 35–40%, favored in cost‑sensitive or large‑volume applications where slightly lower performance is acceptable. Solution‑polymerized EPDM remains dominant because its consistent properties and better vulcanization profile meet the durability standards required by OEMs and construction firms. Suspension grades, while less technically robust, are preferred for general‑purpose sealing, hoses, basic insulation and cost‑conscious infrastructure projects. Additionally, there are specialized EPDM blends and compounded grades (e.g. oil‑extended or filler‑reinforced EPDM) used for niche applications.

Applications of EPDM are diverse. The leading application is automotive seals, weather‑stripping, hoses, window and door gaskets, under‑the‑hood hoses, and EV battery‑insulation components consuming around 42–47% of total EPDM use globally. This dominance stems from EPDM’s resilience to heat, ozone, weathering, and vibration — essential for vehicle durability and safety. The construction and building sector is the next major application, representing roughly 22–30% of consumption. In this segment, EPDM is used for roofing membranes, sealing windows and doors, waterproofing systems, and structural seals valued for long life, UV resistance, and low maintenance in building envelopes and green‑roof installations. Other applications include electrical & electronics insulation, wire and cable jacketing, industrial hoses, and weather‑stripping for appliances. Together these “other” areas contribute the remaining share (roughly 20–30% combined).

The largest end‑user segment is the automotive industry, accounting for about 45% of EPDM demand globally. This reflects wide use in OEM vehicle manufacturing for door/window seals, gaskets, hoses, and EV‑specific insulation components. With global EV production and stricter emission/efficiency standards, this segment continues to drive EPDM demand robustly. Construction industry end‑users including commercial and residential builders, roofing contractors, and infrastructure developers — represent around 25–30% of total EPDM consumption. Adoption here is driven by demand for durable, weather‑resistant, low-maintenance materials for roofs, glazing seals, and waterproofing systems in new builds and renovation works. Other end‑users industrial manufacturers, electrical & electronics equipment producers, HVAC system fabricators, and cable/wiring firms — jointly contribute the remainder (approximately 25–30%). These users leverage EPDM for hoses, insulation, seals, and gaskets in machinery, equipment, and consumer appliances.

Asia-Pacific accounted for the largest market share at 48.5% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2025 and 2032.

The dominance reflects rapid industrialization, expanding automotive output, and large-scale infrastructure development across China, India and Southeast Asian nations. High EPDM consumption in automotive sealing, construction membranes, and industrial insulation fuels this leadership. The fast-growth trajectory is supported by increasing production capacities, integration of petrochemical complexes, and growing demand for construction and EV-related EPDM products across the region.

Is demand from automotive and infrastructure sectors driving EPDM uptake?

North America holds approximately 25–27% of global EPDM consumption, with the United States accounting for roughly 78–80% of regional volume. Major demand drivers include automotive manufacturing including seals, gaskets, hoses, EV components and building and construction sectors using roofing membranes and weather-seal systems. Regulatory push toward energy-efficient building materials and tighter building-envelope performance standards have supported EPDM adoption in construction and renovation projects. Technological upgrades such as advanced compounding, bio-based EPDM formulations, and improved weather and UV-resistant grades are increasingly adopted. Local producers are expanding compounder capacity to meet higher-spec demand especially for EV-grade and sustainable-construction materials. Regional consumer behavior shows higher enterprise adoption in construction retrofit, HVAC systems, and automotive aftermarket components.

Is the shift to sustainable and high-performance EPDM accelerating demand in Europe?

Europe represents around 22–28% of the global EPDM market by volume. Leading markets include Germany, France, UK, and Italy, with automotive manufacturing, green building, and infrastructure renovation driving uptake. Strict environmental standards and sustainability initiatives are pushing firms toward low-VOC, recyclable or bio-based EPDM, especially in construction membranes, sealing applications, and electric vehicle components. Emerging technologies such as recycled-content EPDM and improved compounding for UV and ozone resistance are being widely adopted. European automotive and building-material players are investing in sustainable EPDM grades to meet regulatory compliance. Regional customers prioritize high-quality, compliant materials, with demand skewed toward eco-friendly, long-lasting EPDM products for roofing, sealing, and automotive seals.

Is large-scale industrialization and automotive growth fueling EPDM demand in Asia-Pacific?

Asia-Pacific leads global EPDM demand with about 48.5% share in 2024. Top consuming countries include China accounting for nearly 60% of regional consumption, followed by India, Japan, and South Korea. Strong automotive production, booming construction and infrastructure expansion, and rapid urbanization drive EPDM usage in seals, hoses, roofing membranes, electrical insulation, and industrial applications. Integrated petrochemical complexes enable high-volume EPDM output feeding domestic automotive and construction industries. Local manufacturers are scaling up compounding plants and experimenting with advanced EPDM blends suitable for tropical climates and heavy usage. Consumer behavior favors durable, low-maintenance materials for buildings and vehicles, boosting EPDM adoption across residential, commercial, automotive, and industrial sectors.

Does infrastructure expansion and industrial demand support EPDM growth in South America?

In South America, key countries such as Brazil and Argentina are gradually expanding EPDM usage. Market share is smaller compared to other regions, but growth is shaped by infrastructure projects, expanding automotive components manufacturing, and demand for sealing and insulation materials in construction. Industrial growth and energy sector developments such as pipeline sealing and electrical insulation drive EPDM adoption. Government incentives for housing and public infrastructure, plus growing industrialization, create demand for cost-effective elastomer materials like EPDM. Local players are starting to supply EPDM-based membranes and seals for construction and industrial applications, reflecting rising interest among enterprises seeking durable, climate-resistant materials. Consumer behavior tends toward cost-conscious adoption, prioritizing durability and long service life in construction and industrial contexts.

Are construction and energy sector investments driving EPDM demand in Middle East and Africa?

Middle East and Africa register growing EPDM demand fueled by oil and gas infrastructure, construction of urban facilities, and industrial sealing and insulation needs. Major growth countries include UAE, Saudi Arabia, and South Africa. Demand is driven by climate-resistant construction materials, seals for pipelines and industrial plants, and insulation for energy and water-treatment infrastructure. Technological modernization and adoption of heat and UV-resistant EPDM formulations meet regional environmental challenges. Local manufacturers and compounders are supplying tailored EPDM grades for sealing, roofing membranes, and industrial insulation. Regional behavior trends favor materials with extended durability, chemical resistance, and low maintenance, especially for large projects in harsh climatic conditions.

China — approximately 30 percent global market share: due to high production capacity, expansive automotive and construction demand, and integrated petrochemical infrastructure.

United States — around 22 percent of global EPDM demand: driven by strong automotive sector, established industrial base, and infrastructure renovation projects spanning roofing, HVAC, and sealing applications.

The global EPDM market exhibits a moderately consolidated yet competitive structure, with a small number of major producers commanding a substantial portion of total output, while a larger set of regional and niche manufacturers serve local or specialized demand. More than 30 major firms worldwide actively produce EPDM, with the combined share of the top 5 companies accounting for approximately 55–65% of global production volume.

Key industry leaders have pursued strategic initiatives including capacity expansions, sustainability‑oriented product launches, and collaborations. For example, a leading company commissioned a new 160,000-ton EPDM plant in Asia in 2024 to meet surging demand from automotive and construction sectors. Another firm focused on bio‑based EPDM and recyclable formulations to align with tightening environmental regulations, reshaping competitive positioning toward ESG‑compliant supply.

Competition dynamics are influenced by technological innovation: firms investing in advanced polymerization methods, low‑VOC or recycled‑content EPDM, and application-specific grades for EV components, roofing membranes, and industrial seals are increasingly gaining advantage. Regional producers in Asia and emerging markets leverage cost efficiencies, local feedstock access, and proximity to end users. Overall, the environment is best described as a consolidated core plus fragmented periphery: a handful of multinational chemical giants set global standards and influence pricing, while dozens of regional or specialty producers compete on cost, niche applications, or local supply chains. Innovation and sustainability efforts serve as key differentiators for market leadership.

Lion Elastomers LLC

Mitsui Chemicals, Inc.

Kumho Polychem Co., Ltd.

Versalis S.p.A.

SK Global Chemical Co., Ltd.

The EPDM market is increasingly shaped by advanced polymerization, compounding, and formulation technologies that enhance performance, durability, and sustainability. Solution polymerization remains the predominant method, producing over 60% of global EPDM output due to its precise control over molecular weight distribution, resulting in superior elasticity, ozone and weather resistance. Suspension polymerization accounts for approximately 35–40% of production, mainly serving cost-sensitive applications and high-volume, general-purpose products. Emerging technologies include the development of bio-based EPDM and low-VOC formulations, which have been adopted in roughly 18% of new product launches in 2024. These environmentally conscious variants reduce lifecycle carbon emissions by up to 25% while maintaining comparable mechanical and thermal properties to conventional grades. Additionally, recycled-content EPDM is gaining traction, with internal scrap reuse rates reaching 82% in several manufacturing plants, reflecting the market’s push toward circular economy practices.

Advances in application-specific compounding have enabled the creation of EPDM grades tailored for electric vehicle battery insulation, high-temperature under-the-hood automotive components, roofing membranes, and industrial hoses. Precision mixing and extrusion technologies have improved uniformity and reduced production defects by nearly 15% across high-volume manufacturing lines. Digitalization and Industry 4.0 integration, including real-time process monitoring, predictive maintenance, and automated quality control, are enhancing operational efficiency and minimizing downtime by up to 20%. These technological trends collectively position EPDM as a high-performance, sustainable material for automotive, construction, electrical, and industrial applications, meeting evolving market demands and regulatory pressures.

In July 2024, Dow Inc. launched a bio‑based EPDM grade under its NORDEL REN line, aimed at automotive, construction and industrial applications to support sustainable material sourcing and reduce environmental impact.

In March 2024, SK Global Chemical Co., Ltd. completed construction of a new EPDM production facility with annual capacity of 100,000 tons, using advanced process technology to improve product consistency and energy efficiency for export markets.

In 2023, LANXESS AG announced expansion of its EPDM rubber production capacity at its German facility, upgrading output to address growing demand from automotive and construction sectors, and introduced a new EPDM grade with enhanced resistance to oil and temperature.

In 2024, Mitsui Chemicals, Inc. inaugurated a new EPDM production line in Japan, increasing its annual output by approximately 20% to serve increasing demand from Asia‑Pacific automotive and infrastructure industries.

The EPDM Market Report covers global and regional dimensions including North America, Europe, Asia‑Pacific, South America, Middle East & Africa — providing detailed segmentation by product type (standard EPDM, oil‑extended EPDM, specialty grades, thermoplastic‑compatible variants), by application (automotive sealing & hoses, construction membranes and roofing, electrical & cable insulation, industrial hoses, HVAC & infrastructure sealing) and by end-user industry (automotive OEMs, construction & infrastructure firms, electrical/electronics companies, industrial equipment manufacturers). The report assesses technological variations: solution‑polymerized EPDM, suspension‑polymerized EPDM, bio‑based and low‑VOC formulations, recycled‑content EPDM, and application‑specific compounding for EVs, renewable energy installations, and high‑performance sealing requirements. Geographic coverage includes production capacity, consumption patterns, and demand drivers in leading and emerging markets. It examines market dynamics, competition landscape, recent capacity expansions, supply‑chain developments, and innovation trends. The report also highlights niche and emerging segments — for example, EPDM for EV battery sealing, green-building waterproofing membranes, sustainable cable insulation, and recyclable or circular‑economy EPDM products. Focus extends to regulatory and ESG compliance trends, raw material dynamics, and end‑user behavior, giving decision‑makers a comprehensive, actionable view of market breadth, technology variety, application reach, and future potential.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4609.33 Million |

|

Market Revenue in 2032 |

USD 6504.93 Million |

|

CAGR (2025 - 2032) |

4.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

LANXESS AG, ExxonMobil Chemical Company, Dow Inc., Lion Elastomers LLC, Mitsui Chemicals, Inc., Kumho Polychem Co., Ltd., Versalis S.p.A., SK Global Chemical Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |