Reports

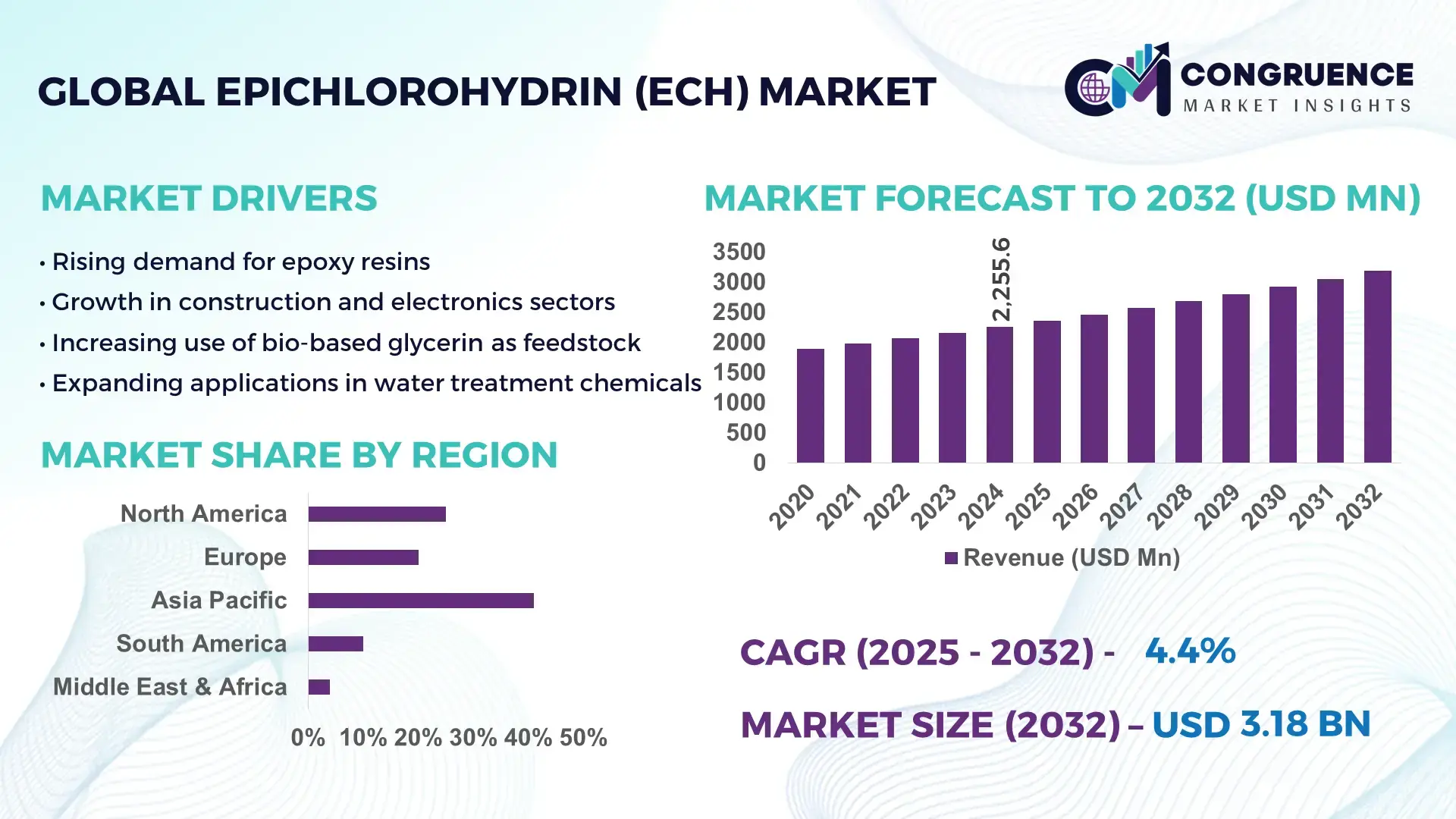

The Global Epichlorohydrin (ECH) Market was valued at USD 2255.62 Million in 2024 and is anticipated to reach a value of USD 3183.24 Million by 2032 expanding at a CAGR of 4.4% between 2025 and 2032. This growth is driven by rising demand from epoxy resin and water-treatment chemical manufacturers.

China maintains a leading position in the Epichlorohydrin (ECH) market due to its extensive production capacities exceeding 600 kilotons annually, supported by sustained investments in glycerin-based ECH technologies. The country operates advanced petrochemical clusters serving electronics, automotive coatings, and industrial adhesives. Capacity additions of over 150 kilotons during 2023–2024 strengthened supply reliability, while technological adoption in glycerol-to-ECH conversion surpassed 70% in 2024, improving energy performance and enabling large-scale export capability.

• Market Size & Growth: Valued at USD 2255.62 Million in 2024 and projected to reach USD 3183.24 Million by 2032 at a 4.4% CAGR, supported by expanding epoxy resin applications.

• Top Growth Drivers: 28% rise in epoxy resin adoption, 18% gain in chemical processing efficiency, 22% growth in water-treatment chemical demand.

• Short-Term Forecast: By 2028, production efficiencies expected to improve by 15% through feedstock optimization and upgraded catalytic systems.

• Emerging Technologies: Accelerated uptake of glycerin-based ECH production, advanced catalytic oxidation platforms, and low-emission chlorination technologies.

• Regional Leaders: Asia-Pacific projected at USD 1.4 Billion by 2032 with high industrial consumption; Europe at USD 680 Million driven by demand for sustainable resins; North America at USD 520 Million supported by specialty coating applications.

• Consumer/End-User Trends: Strong consumption by epoxy resin, electronics, and industrial coatings manufacturers, with rising preference for low-VOC and bio-based intermediates.

• Pilot or Case Example: A 2027 green-glycerin pilot achieved a 12% energy reduction and 19% output efficiency gain.

• Competitive Landscape: Market leader holds ~16% share, with major competitors including Olin Corporation, Solvay, Shandong Haili Chemical, and Aditya Birla Chemicals.

• Regulatory & ESG Impact: Emission-reduction mandates, incentives for bio-based feedstocks, and stricter wastewater norms accelerating adoption.

• Investment & Funding Patterns: Over USD 320 Million invested in capacity expansions, process modernization, and sustainable feedstock projects.

• Innovation & Future Outlook: Advancements in circular feedstocks, digitalized plant controls, and evolving epoxy applications shaping long-term development.

Unique developments in the Epichlorohydrin (ECH) Market show strong demand across electronics, automotive, construction, and water-treatment sectors, each contributing significantly to consumption volumes. Innovations in bio-based ECH, advanced chlorination systems, and emission-controlled reactors are redefining production practices. Regulatory emphasis on cleaner intermediates and sustainable resin manufacturing is fuelling technology upgrades worldwide. Regional consumption patterns reveal rapid uptake in Asia alongside steady modernization in Europe and North America. Future market growth will be driven by expanded epoxy resin usage, renewable feedstock integration, and upgraded chemical processing infrastructure.

The Epichlorohydrin (ECH) Market holds strong strategic relevance as it underpins essential value chains such as epoxy resins, water-treatment chemicals, electronic laminates, and advanced coatings. Its future pathways are increasingly shaped by technological modernization, circular feedstock innovation, and regulatory transitions toward lower-emission chemical synthesis. New catalytic oxidation technology delivers a 22% efficiency improvement compared to the older thermal-chlorination standard, enabling higher yields with reduced energy requirements. Asia-Pacific dominates in production volume, while Europe leads in sustainable technology adoption with 41% of enterprises integrating low-emission ECH processes. By 2027, AI-driven process automation is expected to improve plant resource efficiency by 18%, significantly reducing downtime and waste outputs. Firms are committing to ESG-linked improvements such as achieving a 25% reduction in chlorinated waste discharge by 2030, aligned with tightening global environmental frameworks. In 2024, a leading chemical producer in Japan achieved a 17% reduction in operational emissions through digital-twin-enabled reactor optimization. Collectively, these advancements are steering the sector toward greener production, increased reliability, and competitive scalability. The Epichlorohydrin (ECH) Market is poised to evolve as a pillar of industrial resilience, regulatory compliance, and long-term sustainable growth.

The growing need for high-performance epoxy materials is a major driver of the Epichlorohydrin (ECH) Market. Epoxy resins consume a substantial share of global ECH output, supported by their expanding use in electronics, composites, protective coatings, wind-energy components, and construction materials. Global electronics manufacturing alone recorded a more than 12% increase in epoxy-based laminates in 2024, significantly boosting ECH requirements. Industrial coatings and adhesives continue to show steady consumption growth, reinforced by infrastructure expansion and automation in manufacturing units. As industries pursue durability, chemical resistance, and lightweighting, ECH-based epoxy solutions provide measurable performance advantages, reinforcing the sustained upward demand. The transition to more advanced epoxy grades further strengthens ECH consumption volumes within key sectors.

Stringent environmental norms concerning chlorinated emissions, wastewater discharge, and hazardous by-products present notable restraints for the Epichlorohydrin (ECH) Market. Production processes generate regulated compounds that require advanced treatment, raising compliance costs and operational complexity. Disposal standards for chlorinated organics have tightened across major economies, increasing the need for continuous monitoring and high-performance filtration systems. Rising energy costs for high-temperature operations further impact production efficiency, while plant modernization timelines often delay capacity additions. Additionally, fluctuations in key feedstocks such as glycerin and propylene influence process stability and output consistency. Collectively, these regulatory, environmental, and operational pressures create measurable constraints for producers navigating evolving compliance landscapes.

The Epichlorohydrin (ECH) Market stands to gain significantly from the rapid adoption of bio-based and circular feedstocks, which offer measurable reductions in emissions and resource consumption. Glycerin-based ECH production presents an opportunity for improved process efficiency, delivering up to 20% lower energy use than conventional petro-based pathways. This shift aligns with global initiatives promoting green chemical manufacturing. Technological upgrades such as catalytic oxidation, digitalized plant controls, and heat-recovery systems provide further opportunities for capacity enhancement and cost reduction. Growing demand for sustainable epoxy resins in automotive, renewable energy, marine, and electronics applications supports long-term market expansion. These emerging opportunities position producers to capture new demand segments and strengthen competitiveness through innovation-led strategies.

The Epichlorohydrin (ECH) Market faces significant challenges linked to rising production costs, capital-intensive technology transitions, and complex regulatory requirements. Upgrading conventional plants to low-emission systems requires substantial investment, often exceeding multi-million-dollar thresholds per unit. Energy-intensive operations amplify pressure in regions with fluctuating electricity and fuel prices. Compliance with evolving environmental standards demands continuous adoption of advanced monitoring, treatment, and recovery technologies, adding operational load. Volatile feedstock pricing also influences production planning and long-term cost stability. Additionally, workforce skill gaps in advanced catalytic processes and digital automation can slow modernization. These interlinked challenges create structural hurdles that producers must navigate to maintain efficiency, competitiveness, and regulatory alignment.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand patterns in the Epichlorohydrin (ECH) market, supported by the increasing use of epoxy-based adhesives, coatings, and composite materials essential for prefabricated components. Data indicates that nearly 55% of new modular projects reported measurable cost benefits linked to prefabrication. Automated off-site production of pre-bent and cut structural elements has reduced on-site labor requirements by approximately 18% and accelerated completion timelines by nearly 22%. Demand for precision-engineered epoxy systems continues to strengthen in Europe and North America, where construction efficiency and performance reliability remain strategic priorities for infrastructure developers.

• Expansion of Bio-Based ECH Production Technologies: The push toward greener chemical manufacturing is accelerating investments in glycerin-to-ECH technologies. Bio-based ECH output increased by more than 30% between 2022 and 2024, supported by process improvements that delivered up to 20% lower energy consumption compared to conventional petro-based routes. Adoption rates in Asia surpassed 40%, driven by large-scale industrial integration and environmental compliance targets. Chemical producers are actively upgrading catalytic systems, achieving yield gains of 12–15% while simultaneously reducing controlled emissions by nearly 10%, positioning bio-ECH as a strategic pathway for sustainable growth.

• Digitalization and AI-Enabled Plant Optimization: Digital-twin models, sensor-driven monitoring, and AI-enhanced predictive maintenance are transforming production ecosystems within the Epichlorohydrin (ECH) market. By 2024, more than 35% of large production facilities had integrated some level of automation to improve throughput stability. Plants utilizing AI-based operational analytics reported a 14% reduction in downtime and an 11% improvement in energy efficiency. Advanced process-control algorithms now optimize reactor temperature, pressure, and feedstock ratios in real time, strengthening output consistency and reducing waste volumes by up to 9% across modernized facilities.

• Growth in High-Performance Epoxy Applications: The rising use of high-performance epoxy systems in electronics, wind turbine blades, industrial coatings, and automotive lightweighting continues to expand ECH consumption. Electronics manufacturing recorded a 12% year-over-year increase in epoxy laminate utilization in 2024, directly elevating upstream ECH demand. Wind energy installations contributed additional structural demand, with epoxy-rich composites increasing by 16% across new turbine deployments. Industrial coating manufacturers reported productivity improvements of 10–13% through enhanced curing technologies, reinforcing the need for consistent ECH supply to support next-generation high-strength resin formulations.

The segmentation of the Epichlorohydrin (ECH) Market spans product types, applications, and end-user categories, each shaped by evolving industrial demand, technology transitions, and regulatory pressures. Types of ECH increasingly reflect diversification toward bio-based variants and advanced petro-derived formulations. Applications remain concentrated in epoxy resin manufacturing, water-treatment chemicals, elastomers, and specialty intermediates, each displaying distinct adoption behaviors. End-user insights reveal strong utilization across electronics, automotive, construction, and chemical processing sectors, supported by rising consumption volumes and modernization initiatives. Together, these segments illustrate the market’s structural evolution driven by efficiency targets, sustainability compliance, and growth in performance-centric industries.

The Epichlorohydrin (ECH) Market comprises petro-based ECH, bio-based ECH, and specialty-grade formulations designed for high-performance applications. Petro-based ECH remains the leading type, accounting for approximately 67% of total adoption, driven by its established production infrastructure, broad availability, and compatibility with large-scale epoxy resin manufacturing. Bio-based ECH is the fastest-growing type, supported by expanding glycerin-to-ECH pathways and environmental mandates, and is projected to grow at a CAGR of 8.2%, reinforced by a 20% improvement in energy performance compared with traditional routes. Specialty ECH variants, including high-purity and low-chloride grades, hold the remaining 14% combined share, serving electronics, composites, and precision coating applications where stringent material specifications are required.

Applications of Epichlorohydrin (ECH) span epoxy resins, water-treatment chemicals, elastomers, and other specialty intermediates. Epoxy resin production dominates with nearly 71% share, reinforced by escalating use of epoxy laminates in electronics, protective coatings, wind-blade composites, and structural adhesives. Water-treatment chemicals represent a significant application area with 19% share, supported by rising municipal and industrial treatment requirements. Elastomers, flame retardants, and fine-chemical intermediates collectively contribute the remaining 10%, reflecting niche yet essential uses across industrial value chains. The fastest-growing application is advanced epoxy systems, projected to expand at a CAGR of 7.4%, driven by increased demand for high-performance composites and low-VOC coating formulations.

End-user adoption of Epichlorohydrin (ECH) is concentrated in chemicals, electronics, automotive, construction, and water-treatment industries. The chemical processing sector leads with around 48% share, driven by its extensive epoxy resin and intermediate production requirements. Electronics follows with 24% share, reflecting demand for laminates, coatings, and specialty resin systems used in semiconductors and printed circuit boards. Automotive and construction collectively contribute 22%, supported by lightweighting initiatives, composite use in vehicle parts, and performance coatings. Water-treatment and other industrial users account for the remaining 6%, primarily for epichlorohydrin-based flocculants and specialty additives. The fastest-growing end-user category is electronics, projected to expand at a CAGR of 7.9%, supported by increased dependence on high-performance epoxy laminates and encapsulation resins essential for miniaturization and thermal management.

Asia-Pacific accounted for the largest market share at 48.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The Asia-Pacific market benefitted from strong production capacity exceeding 1.2 million tons, substantial demand from epoxy resins, water treatment chemicals, and rapidly expanding electronics manufacturing clusters. Europe held a 23.4% share, supported by stringent regulatory frameworks and chlor-alkali modernization projects. North America captured 18.7%, driven by advanced coatings, automotive, and pharmaceutical industries. South America and the Middle East & Africa collectively represented nearly 10% of global consumption, with rising industrialization and resin applications supporting regional expansion.

What Factors Are Driving the Accelerating Demand for Epichlorohydrin in This Market?

The North American Epichlorohydrin (ECH) market held an estimated 18.7% share in 2024, supported by strong demand from the automotive, aerospace, electronics, and pharmaceutical sectors. Industries such as epoxy resins for composites, water treatment chemicals, and specialty elastomers remain major consumers. Regulatory updates promoting cleaner chemical production and chlorine-derived product efficiency are shaping market behavior. Digital transformation across chemical plants, including automation and predictive monitoring, is enhancing production throughput. Local players like Westlake Corporation expanded resin-grade ECH supply to serve high-performance coatings. Consumer behavior trends show higher enterprise adoption in healthcare and finance, boosting demand for ECH-based materials used in diagnostic devices, adhesives, and engineered components.

How Is Industrial Sustainability Influencing the Demand for Epichlorohydrin Across Key Industries?

The Europe Epichlorohydrin (ECH) market accounted for 23.4% of global consumption in 2024, with Germany, the UK, France, and Italy serving as leading demand centers. The region benefits from mature automotive, construction, and electronics sectors, all driving ECH usage for epoxy resins and intermediates. EU regulatory bodies such as ECHA and REACH continue to push sustainability compliance, encouraging a shift toward bio-based glycerin-derived ECH. Technological adoption includes automated chlorine handling systems and closed-loop purification lines. Local chemical manufacturers, including Solvay, expanded their production efficiency programs supporting high-purity ECH grades. Consumer behavior emphasizes regulatory-compliant, eco-focused chemicals, with demand increasing for explainable and traceable chemical sourcing patterns.

What Key Industrial Shifts Are Strengthening the Growth Outlook for Epichlorohydrin in This Region?

The Asia-Pacific Epichlorohydrin (ECH) market ranked highest globally by volume, contributing nearly 48.2% of total demand in 2024. China, India, Japan, and South Korea are top consumers, supported by massive manufacturing clusters, expanding electronics production, and large-scale epoxy resin capacity. Infrastructure investment, particularly in chemicals and construction, continues to push consumption upward. The region is also a hub for innovation in bio-based ECH and cost-optimized chlor-alkali expansion projects. Companies such as Shandong Haili Chemical are strengthening domestic supply with higher-capacity ECH units. Consumer behavior trends are shaped by rapid digitalization, with growth driven by e-commerce, mobile technology, and electronics assembly industries that rely on ECH derivatives.

Which Emerging Industrial and Policy Drivers Are Shaping Growth in the Epichlorohydrin Market?

The South America Epichlorohydrin (ECH) market, led by Brazil and Argentina, accounted for approximately 6.1% of global demand in 2024. Regional consumption is influenced by the expansion of construction materials, coatings, and energy sector applications. Infrastructure development, particularly in civil engineering, has supported increased epoxy resin usage. Government incentives promoting industrial modernization and trade policies supporting chlorine-based manufacturing are enhancing supply stability. Local chemical producers in Brazil have expanded distribution networks for resin intermediates. Consumer behavior trends show rising demand for ECH-linked materials due to media growth, digital device penetration, and language localization sectors that require adhesives, coatings, and electrical components.

How Are Industrial Investments and Modernization Efforts Reshaping the Epichlorohydrin Market Landscape?

The Middle East & Africa Epichlorohydrin (ECH) market represented nearly 4.0% of global demand in 2024, driven primarily by oil & gas, construction, water treatment, and electronics assembly. Countries such as the UAE, Saudi Arabia, and South Africa are major contributors, supported by industrial expansion and chemical sector modernization. Advancements in chlorine-alkali technologies and environmental compliance systems are boosting local production quality. Trade partnerships and government initiatives promoting downstream petrochemicals are strengthening market foundations. Local manufacturers in the UAE continue to expand access to high-purity intermediates for coatings and composites. Consumer behavior patterns reflect rising demand for engineered materials due to construction growth and industrial diversification.

• China – 32% market share

High dominance due to extensive epoxy resin production capacity and strong electronics and construction sector demand.

• India – 12% market share

Leadership supported by rapidly expanding chemical manufacturing, strong glycerin-based ECH production momentum, and growing infrastructure consumption.

The Epichlorohydrin (ECH) market is moderately consolidated but characterized by both multinational leaders and substantial regional producers, with about 12–15 major active competitors globally. The top five firms — including Solvay, Dow Chemical Company, Shandong Haili Chemical Industry Co., Ltd., Samsung Fine Chemicals Co., Ltd., and Spolchemie A.S. — account collectively for roughly 50% of global production capacity, indicating a moderate concentration among a few large players.

Competition centers around capacity expansion, sustainability, product purity, and vertical integration. Several firms have launched new bio-based or high-purity ECH grades to meet evolving regulatory and industry demands. Strategic initiatives include capacity extensions, acquisitions, technology licensing deals, and partnerships with downstream epoxy resin producers to secure stable off‑take. Innovation trends such as glycerin-based (bio‑ECH) processes, membrane-based wastewater treatment, and low-emission chlorination systems have become differentiators, allowing early adopters to outperform in efficiency and compliance metrics.

Given regulatory pressure on emissions and increasing demand for sustainable chemicals, companies investing in green‑chemical technologies and modern production lines are gaining competitive advantage. Market fragmentation among smaller regional producers keeps entry barriers moderate, but the dominance of the top 5 with half the capacity skews bargaining power. As a result, competitive pressure is high, innovation cycles rapid, and consolidation through strategic alliances or capacity scaling is common.

Solvay

Samsung Fine Chemicals Co., Ltd.

Formosa Plastics Corporation

Hexion Inc.

Sumitomo Chemical Co., Ltd.

The Epichlorohydrin (ECH) market is increasingly influenced by technological advancements across production processes, environmental management, and downstream application integration. Conventional petrochemical-based ECH production remains dominant, but the adoption of glycerin-based bio-ECH technologies has expanded rapidly, contributing to a 30% increase in bio-based output between 2022 and 2024. These processes offer energy efficiency gains of up to 20% compared to traditional thermal-chlorination routes while reducing chlorinated by-product generation by nearly 15%, aligning with stricter regulatory frameworks. Advanced catalytic oxidation systems have become standard in high-purity ECH production, improving selectivity and reducing reactor downtime by approximately 12–14%. Process digitalization, including sensor-driven monitoring and predictive analytics, is now employed in over 35% of large-scale plants, enabling real-time optimization of feedstock ratios, temperature, and pressure, reducing energy consumption by nearly 10%.

Emerging membrane-based separation and wastewater recovery technologies are also reshaping ECH production, allowing plants to recycle up to 18% of previously discarded by-products and lower environmental emissions. In downstream applications, epoxy resin manufacturers are adopting high-performance curing and formulation technologies that improve material strength by 10–12%, further driving demand for high-purity ECH. The integration of AI-enabled predictive maintenance and digital-twin modeling is expected to continue transforming operational efficiency, while pilot projects in Asia have demonstrated 15% improvements in yield and 8% reductions in waste. Collectively, these technological insights indicate a market increasingly shaped by sustainable production, process optimization, and high-performance application requirements.

In 2024, Epigral Limited in India approved expansion of its Epichlorohydrin capacity to reach 100,000 TPA — adding 50,000 TPA — at its Dahej facility.

In 2024, Hexion Inc. announced expansion of its ECH production at its Pernis site in the Netherlands, adding 25,000 metric tons per year using bio‑based renewable feedstocks; start-up is scheduled for late 2024. (chemxplore.com)

In 2024, Covestro AG formed a partnership with Neste Corporation to develop bio‑based ECH production using renewable feedstocks, aiming to commercialize sustainable routes that significantly reduce carbon footprint.

In 2023, global production of glycerin-based (bio‑based) ECH surpassed 410,000 metric tons, up from 350,000 metric tons in 2022, reflecting growing shift toward sustainable chemical production pathways.

This Epichlorohydrin (ECH) Market Report covers a comprehensive range of dimensions including production routes, geographic regions, application sectors, technology trends, and end‑user industries. It analyzes both propylene-based and bio‑based glycerin-derived ECH production routes, assessing technical capacities, process efficiencies, and feedstock transition dynamics. The regional scope spans North America, Europe, Asia-Pacific, Latin America, Middle East & Africa — evaluating regional demand drivers, capacity distribution, and consumption patterns across diverse industrial economies. Application-focused segments include epoxy resins, water-treatment chemicals, elastomers and specialty intermediates, adhesives, coatings, composites, and other downstream products. The report further profiles end-user industries such as electronics, automotive & aerospace, construction, infrastructure, water treatment, and consumer goods — highlighting variations in adoption behavior, regulatory influence, and growth potential. On the technology front, it examines adoption of advanced catalytic oxidation, closed‑loop wastewater and by‑product recycling systems, membrane-based separation, digital‑twin modelling, AI‑enabled process optimization, and high‑purity ECH grades tailored for electronics and aerospace composites. Geographic analysis incorporates regional regulatory pressure, sustainable‑chemistry incentives, import‑substitution initiatives, and local production developments. Emerging and niche segments such as bio‑based ECH, sustainable water‑treatment flocculants, high‑performance epoxy composites for wind turbines and aerospace, and integrated chlor‑alkali‑derived specialty chemicals are included to illustrate future growth pathways. The breadth of the report is designed to provide decision-makers with actionable data on supply‑chain shifts, technology adoption, end‑market demand trends, regional competitive positioning, and potential investment or partnership opportunities across the global Epichlorohydrin (ECH) value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2255.62 Million |

|

Market Revenue in 2032 |

USD 3183.24 Million |

|

CAGR (2025 - 2032) |

4.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Solvay, Dow Chemical Company, Shandong Haili Chemical Industry Co., Ltd., Samsung Fine Chemicals Co., Ltd., Formosa Plastics Corporation, Aditya Birla Chemicals, Hexion Inc., Sumitomo Chemical Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |