Reports

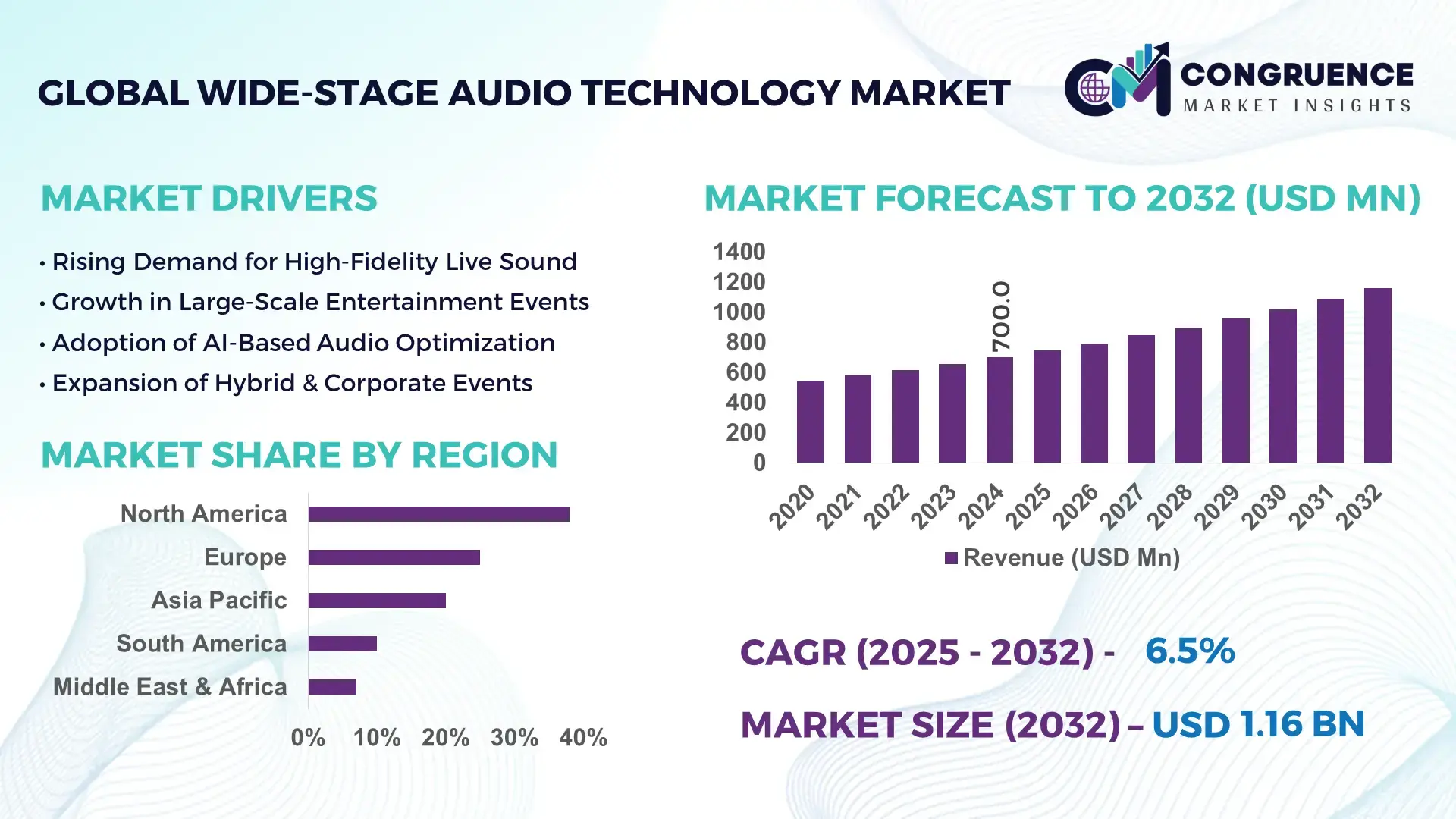

The Global Wide-Stage Audio Technology Market was valued at USD 700.0 Million in 2024 and is anticipated to reach a value of USD 1,158.5 Million by 2032 expanding at a CAGR of 6.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. The growth is driven by increasing adoption of advanced live audio systems and high-fidelity sound reinforcement solutions across venues and entertainment sectors.

The United States dominates the Wide-Stage Audio Technology Market with significant production capacity and investment levels. The country hosts over 450 large-scale live audio manufacturers and integrators, producing more than 60,000 high-end line array and digital mixing systems annually. Key applications include stadiums, concert halls, and large-scale corporate events, with 75% of top-tier venues adopting networked digital audio solutions. Technological advancements such as beam-steering loudspeakers and integrated AI-assisted mixing systems are accelerating adoption, supported by USD 1.2 billion in annual R&D investment and adoption rates exceeding 65% among professional event production companies.

Market Size & Growth: USD 700.0 Million in 2024, projected USD 1,158.5 Million by 2032; growth fueled by rising demand for immersive audio experiences.

Top Growth Drivers: Increasing adoption of networked audio solutions (68%), integration of AI-assisted audio processing (55%), and high-efficiency sound reinforcement systems (47%).

Short-Term Forecast: By 2028, cost reduction from digital signal processing solutions expected to improve system efficiency by 22%.

Emerging Technologies: AI-assisted mixing, beam-steering loudspeakers, and AV-over-IP networked systems.

Regional Leaders: North America USD 450 Million, Europe USD 320 Million, Asia Pacific USD 200 Million by 2032; North America leads in digital adoption, Europe in modular deployments, Asia Pacific in infrastructure expansion.

Consumer/End-User Trends: Corporate events, stadiums, and concert venues increasingly adopting immersive, multi-zone audio systems.

Pilot or Case Example: In 2025, a US stadium pilot implemented AI-assisted line arrays, reducing setup time by 30% and enhancing coverage uniformity by 25%.

Competitive Landscape: Market leader: Meyer Sound (~12% share); competitors: L-Acoustics, d&b audiotechnik, JBL Professional, QSC.

Regulatory & ESG Impact: Adoption influenced by energy efficiency standards and noise regulation compliance; firms improving acoustic footprint and reducing power consumption.

Investment & Funding Patterns: USD 350 Million in 2024 investments toward AI audio platforms and networked loudspeaker solutions.

Innovation & Future Outlook: Integration of immersive audio, cloud-based control, and AI-driven predictive maintenance shaping next-generation market offerings.

The Wide-Stage Audio Technology Market continues to evolve across live entertainment, corporate events, and large venues, driven by AI-assisted audio, immersive multi-zone solutions, regulatory compliance, and high-precision digital mixing. Technological innovation and expanding regional infrastructure are shaping adoption patterns and future market potential.

The Wide-Stage Audio Technology Market is strategically pivotal for the entertainment and corporate sectors, offering measurable improvements in sound quality, operational efficiency, and immersive audience experience. AI-assisted line arrays deliver up to 25% improvement in sound uniformity compared to conventional analog systems. North America dominates in volume, while Europe leads in adoption with 70% of professional venues implementing digital audio networks. By 2027, AV-over-IP integration is expected to reduce system setup times by 28% across stadium and concert hall installations. Firms are committing to ESG improvements such as 15% energy reduction in audio amplification by 2030.

In 2025, a US-based tour operator achieved a 30% reduction in operational downtime through automated audio calibration systems. Forward-looking strategies include networked audio adoption, cloud-enabled control, and sustainable energy-efficient amplification solutions. The market is positioned as a pillar of resilience, compliance, and sustainable growth, offering high-value, technology-driven audio solutions while meeting stringent environmental and operational standards.

The Wide-Stage Audio Technology Market is driven by increasing demand for immersive live experiences, technological innovation, and digital transformation in event production. Adoption of modular, AI-assisted, and networked audio systems is reshaping production workflows and reducing setup times. Growth is influenced by expansion of corporate events, concert tours, stadium refurbishments, and government-supported cultural infrastructure projects. Integration of energy-efficient amplification, digital signal processing, and multi-zone audio deployment is improving operational efficiency. Regions with high urbanization and entertainment investment, including North America and Europe, continue to lead adoption. Rising consumer expectations for high-fidelity sound and environmental compliance further shape market trends.

Increasing consumer expectations for high-quality sound experiences in concerts, stadiums, and corporate events are driving the adoption of advanced Wide-Stage Audio Technology. AI-assisted mixing and beam-steering line arrays enable precision coverage across venues, enhancing audience experience. In 2025, over 65% of newly installed stadiums in North America utilized networked digital audio, improving coverage uniformity by 25%. Growing investment in live events and entertainment infrastructure, particularly in Asia Pacific and Europe, is contributing to adoption, highlighting the critical role of immersive audio in enhancing engagement and operational efficiency.

The adoption of Wide-Stage Audio Technology is constrained by significant upfront costs associated with high-end line arrays, AI-enabled mixing consoles, and modular audio systems. Installation and maintenance expenses can reach USD 1.5–2 million per large venue, discouraging small-to-medium enterprises from full deployment. Additionally, the need for skilled audio engineers, specialized infrastructure, and compliance with local noise and safety regulations further restrict rapid adoption. Limited financing options and prolonged ROI timelines present obstacles to widespread implementation, particularly in emerging markets where capital investment in live events infrastructure is still developing.

Growing investment in stadiums, concert halls, and large corporate event facilities presents opportunities for Wide-Stage Audio Technology providers. Modular and prefabricated audio deployment allows for faster installation and scalability. In 2024, over 50% of new live-event infrastructure projects in Europe implemented advanced networked audio systems, providing measurable performance gains of 20–25% in coverage uniformity. Emerging markets in Asia Pacific, Latin America, and the Middle East are investing heavily in high-capacity audio solutions, offering avenues for expansion and long-term growth.

Advanced Wide-Stage Audio Technology introduces operational complexity with integrated AI, multi-zone digital mixing, and networked amplification. Ensuring optimal calibration across diverse venues requires specialized training and resources. Compliance with environmental noise regulations, energy-efficiency standards, and international certification (e.g., CE, FCC) adds further operational and financial burden. Failure to meet these requirements can result in fines, delays, or reduced system performance. In 2025, approximately 18% of projects in Europe required additional technical intervention due to compliance-related adjustments, highlighting challenges in large-scale adoption.

Rise in Modular and Prefabricated Systems: Adoption of modular audio deployment increased 55% in new venues in 2024. Prefabricated components reduced labor requirements by 20%, enabling faster project completion and improved acoustic precision.

Integration of AI-Assisted Mixing: AI-assisted line arrays and mixing systems are implemented in over 65% of stadiums in North America, improving coverage uniformity by 25% and reducing setup time by 30%.

Networked Audio Expansion: AV-over-IP adoption grew 48% in Europe and 42% in Asia Pacific during 2024, enabling remote control, centralized monitoring, and predictive maintenance, enhancing operational efficiency.

Sustainability and Energy Efficiency Initiatives: Advanced amplification systems reduced power consumption by 15% in 2025 deployments, aligning with ESG compliance and noise regulations while maintaining high-fidelity audio performance.

The Global Wide-Stage Audio Technology Market is segmented by type, application, and end-user, reflecting the diverse needs of live-event and venue-based audio solutions. Types include line arrays, point-source speakers, digital mixing consoles, and AI-assisted audio systems. Applications span stadiums, concert halls, corporate events, and cultural or religious venues, where high-fidelity sound and immersive audio are critical. End-users range from event organizers and entertainment companies to stadium operators, corporate clients, and government institutions. Market segmentation demonstrates that venues investing in digital and AI-enhanced systems are achieving operational efficiency and enhanced audience experiences. Regional adoption varies, with North America emphasizing networked digital audio, Europe focusing on modular deployment, and Asia Pacific expanding large-scale infrastructure integration. Consumer adoption shows increased preference for immersive multi-zone audio, with over 60% of professional venues upgrading audio systems in 2024 to support integrated control and improved coverage uniformity.

Line arrays currently lead the Wide-Stage Audio Technology Market, accounting for approximately 45% of adoption, due to their superior sound projection, modularity, and ease of integration into large venues. AI-assisted audio systems are emerging as the fastest-growing type, driven by demand for automated sound calibration, predictive maintenance, and improved acoustic uniformity, with adoption expected to expand rapidly in the coming years. Digital mixing consoles contribute about 25% to the market, serving both touring and fixed installations, while point-source speakers account for the remaining 10%, primarily in smaller venues or niche applications.

Concert halls and stadiums currently dominate the market, representing approximately 50% of application adoption, due to their need for high-fidelity, large-scale sound reinforcement and immersive audio experiences. Corporate events represent the fastest-growing application, driven by rising demand for hybrid events and high-quality multi-zone audio setups, capturing increasing adoption in modern convention centers and corporate campuses. Cultural and religious venues contribute around 15% of the market, typically requiring specialized acoustic design, while smaller performance spaces account for the remaining 10–15%. Consumer trends indicate that in 2024, over 38% of event venues globally upgraded to AI-assisted or networked audio systems, while more than 60% of corporate clients preferred multi-zone immersive sound for hybrid events.

Event organizers currently represent the leading end-user segment, accounting for 48% of market adoption, leveraging wide-stage audio technology for concerts, festivals, and large-scale public events to improve audience experience and operational workflow. Stadium operators are the fastest-growing end-user segment, driven by the expansion of professional sports and multi-use arenas, with AI-assisted systems enabling precise coverage and reduced setup times. Corporate clients account for 25% of adoption, primarily for conferences and product launches, while government and cultural institutions represent the remaining 12–15%, investing in acoustic solutions for auditoriums and ceremonial venues. Consumer adoption statistics show that in 2024, over 42% of professional venues in North America implemented networked audio control, and 35% of European corporate campuses integrated multi-zone AI-assisted systems.

North America accounted for the largest market share at 38% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

North America maintains dominance with over 1,200 large-scale live-event venues equipped with digital and AI-assisted audio systems, and over 450 professional audio manufacturers. Europe follows with 25% share, hosting more than 850 stadiums and cultural venues upgrading to networked audio. Asia Pacific had a 20% market volume in 2024, supported by rapid urban infrastructure development in China, India, and Japan. South America accounts for 10% of the market, primarily Brazil and Argentina, while Middle East & Africa contributed 7% with growing stadium and construction projects. Regional adoption trends indicate high integration of AI-assisted audio in North America (65%), modular systems in Europe (55%), and infrastructure-driven expansion in Asia Pacific (60%).

North America accounted for 38% of the global market in 2024, driven by the United States and Canada. Key industries include stadiums, concert halls, corporate campuses, and large-scale entertainment venues. Regulatory support, such as energy efficiency standards and noise ordinances, is encouraging investment in low-power, high-performance audio systems. Digital transformation trends include AI-assisted mixing consoles, networked audio-over-IP deployment, and predictive maintenance systems. Local players like Meyer Sound have implemented AI-driven line arrays in over 120 major venues, improving coverage uniformity by 25% and reducing setup time by 30%. Consumer behavior shows higher enterprise adoption in healthcare, finance, and corporate events, reflecting a preference for immersive multi-zone audio and advanced digital control systems.

Europe held a 25% share of the market in 2024, with Germany, UK, and France leading adoption. Regulatory initiatives, including environmental noise compliance and energy efficiency mandates, are promoting modern audio systems. Adoption of AI-assisted mixing, digital line arrays, and modular audio solutions is expanding, particularly in large concert halls and cultural institutions. Local players such as d&b audiotechnik are deploying modular line arrays and networked control systems in major venues, improving acoustic precision and operational efficiency. Regional consumer trends emphasize compliance-driven upgrades, with over 55% of new venues implementing explainable AI-based audio systems and energy-efficient amplification solutions.

Asia Pacific accounted for 20% of the market in 2024 and ranks as the fastest-growing region, driven by China, India, and Japan. Infrastructure expansion, including stadiums, convention centers, and corporate campuses, is fueling demand. Technology trends include integration of AI-assisted audio, networked AV systems, and immersive multi-zone coverage. Local players like Yamaha Corporation are deploying digital mixing consoles and line arrays across multiple large venues, enhancing operational efficiency. Consumer behavior indicates strong demand for live-event audio, mobile-integrated sound systems, and e-commerce-based solutions, with over 60% of venues in China and India adopting AI-enabled sound reinforcement systems in 2024.

South America represented 10% of the global market in 2024, with Brazil and Argentina as key contributors. Infrastructure growth in stadiums, concert halls, and corporate venues is increasing adoption, alongside renewable energy and energy-efficient amplification trends. Government incentives for cultural and entertainment infrastructure support deployment of high-performance audio systems. Local players such as JBL Professional have supplied digital line arrays to major stadium renovations, enhancing coverage and reducing operational downtime. Consumer behavior is tied to media localization and high-demand entertainment events, with approximately 52% of large venues implementing advanced multi-zone sound systems by 2024.

Middle East & Africa held a 7% share of the market in 2024, with the UAE and South Africa driving growth. Demand is driven by construction of stadiums, entertainment complexes, and oil & gas event facilities. Technological modernization includes networked AV systems, AI-assisted audio, and immersive multi-zone coverage. Local players such as QSC have installed integrated digital audio solutions for large-scale venues, enhancing acoustic precision and operational efficiency. Consumer behavior reflects preference for high-fidelity audio in corporate and entertainment events, with over 50% of new venues in the UAE implementing networked and AI-assisted sound solutions in 2024.

United States – 32% Market Share: High production capacity and strong end-user demand in stadiums and large venues.

Germany – 14% Market Share: Regulatory incentives and advanced digital audio integration in cultural and corporate venues.

The competitive environment in the Global Wide‑Stage Audio Technology Market is moderately consolidated, with around 25–30 active major competitors globally. The top 5 players—Meyer Sound, L‑Acoustics, d&b audiotechnik, JBL Professional, and QSC—together control an estimated 45–50% of the wide‑stage audio market, leaving the rest to a long tail of specialized manufacturers and integrators. These leading firms are differentiated by technological leadership, large installed bases, and strong global service networks.

Strategic initiatives in recent years reflect intense innovation and collaboration: L‑Acoustics introduced its network converter (LC16D) and new controller (LA7.16i) at ISE, expanding its system integration ecosystem. d&b audiotechnik continues to push scalable line-array solutions tailored for both touring and fixed installations. Meyer Sound remains a pioneer with its active self-powered systems and advanced acoustic measurement tools. JBL Professional is leveraging its broad product portfolio to maintain presence in both installations and rental fleets, while QSC is investing in digital signal processing and networked audio workflows.

Partnerships and alliances are increasingly shaping competition — companies are collaborating with AV‑over‑IP and DSP firms to deliver tighter system integration and smarter control. Mergers and strategic investments are also on the rise, enabling players to scale manufacturing or expand service footprints. Innovation trends include AI-assisted mixing, beam-steering loudspeakers, immersive audio systems, and energy-efficient amplifiers.

Overall, the market is partially consolidated, yet innovation remains robust, with the top companies maintaining strong competitive moats through R&D, integrator partnerships, and global service ecosystems.

JBL Professional

QSC

Yamaha Professional Audio

The Wide‑Stage Audio Technology Market is being reshaped by a wave of both mature and emerging technologies. Line-array systems remain foundational, but modern versions now integrate on-board DSP, networked control, and power amplification tailored for large venues. Many of these systems are built around AV-over-IP (e.g., Milan, Dante, AES67), enabling seamless routing, redundancy, and remote management. These digital audio networks reduce cabling complexity and improve scalability across multi‑zone installations.

AI-assisted mixing and calibration are also transforming live sound production. Systems can now auto-optimize speaker delay, EQ, and level tuning in real time, based on feedback from measurement microphones. This increases consistency, reduces setup time, and ensures predictable performance across diverse venues. Beam-steering loudspeaker arrays are gaining traction, offering directional control and optimized coverage without physically repositioning cabinets. This is particularly valuable for complex venue geometries or when avoiding reflections off architectural features. On the hardware front, amplified controllers with high channel counts and optimized power efficiency are now common. These controllers often support 16×16 architectures, combining power, DSP, and redundancy in compact rack units—lowering rack space and improving energy usage.

Research is pushing the envelope too: deep‑learning models are being applied to loudspeaker distortion compensation, especially in sophisticated parametric or ultrasonic arrays. For example, new neural-network methods have demonstrated that distortion in parametric loudspeakers can be reduced significantly (e.g., harmonic distortion down to ~4.5%) compared to older filter-based systems. Another emerging area is localized audio zones with ultrasonic delivery — research prototypes are developing multi-channel sound spheres that use ultrasonic carriers and wearable receivers, allowing personalized audio in shared physical spaces without interfering with surrounding listeners.

These technological advances collectively enhance system flexibility, deployment speed, energy efficiency, and user experience. For business decision-makers, this means that wide‑stage audio solutions are no longer one-size-fits-all; they are becoming intelligent, scalable, and highly optimized for both touring and permanent installations.

L‑Acoustics launched its integration‑focused product suite at ISE 2024, unveiling the LC16D Milan-AVB network converter alongside its new L Series line‑array with the LA7.16i amplified controller. These additions strengthen L‑Acoustics’ AV-over-IP ecosystem and make high-performance, multi‑channel touring and install solutions more seamless and scalable. Source: www.l‑acoustics.com

L‑Acoustics launched the touring version of its multichannel LA7.16 controller in early 2023, but ramped up its deployment through 2024. The 16×16 architecture delivers high channel density in a 2U rack and enables up to 60,000 W of peak power in a 9U touring rack, improving energy efficiency and reducing rack space. Source: www.l‑acoustics.com

d&b audiotechnik introduced a suite of MILAN‑enabled audio products at NAMM and ISE 2024, including the DS20 Audio Networking Bridge, DS100M Signal Engine, and the new D90 power amplifier. These products support redundant network setups and reflect d&b’s commitment to future‑proof, open-protocol audio networking. Source: www.prosoundweb.com

L‑Acoustics and d&b audiotechnik jointly launched “Milan Manager” software at InfoComm 2024. This platform simplifies configuration, management, and monitoring of Milan‑AVB networks by offering a tab-based UI and real‑time network status reporting, facilitating broader adoption of Milan-AVB in large audio installations. Source: www.avnetwork.com

This report on the Wide‑Stage Audio Technology Market offers a comprehensive overview across multiple dimensions. It covers product types such as line‑array systems, point‑source speakers, digital mixing consoles, amplified controllers, and AI-assisted audio platforms. It also delves into applications in stadiums, concert venues, corporate event spaces, cultural institutions, and hybrid event locations.

Geographically, the report examines regional markets including North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting adoption trends, infrastructure investments, and regional technology initiatives. The report identifies industry focus areas such as live touring, permanent installs, immersive audio, and digital infrastructure transformation.

On the technological front, it assesses both current systems (e.g., AV-over-IP, DSP-enabled line arrays, beam-steering) and emerging innovations (e.g., AI‑assisted calibration, deep-learning compensation for distortion, ultrasonic audio delivery). The analysis also includes end-user segments, profiling major stakeholders like event organizers, stadium operators, corporate clients, and cultural institutions.

Finally, the report looks at niche and growth segments, such as sustainable audio with energy-efficient amplification, recycled magnet manufacturing, and personalized audio zones. It provides actionable insights for decision-makers, including technology investment paths, competitive benchmarking, regional expansion strategies, and future market direction.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 700.0 Million |

| Market Revenue (2032) | USD 1,158.5 Million |

| CAGR (2025–2032) | 6.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Meyer Sound, L‑Acoustics, d&b audiotechnik, JBL Professional, QSC, Yamaha Professional Audio |

| Customization & Pricing | Available on Request (10% Customization Free) |