Reports

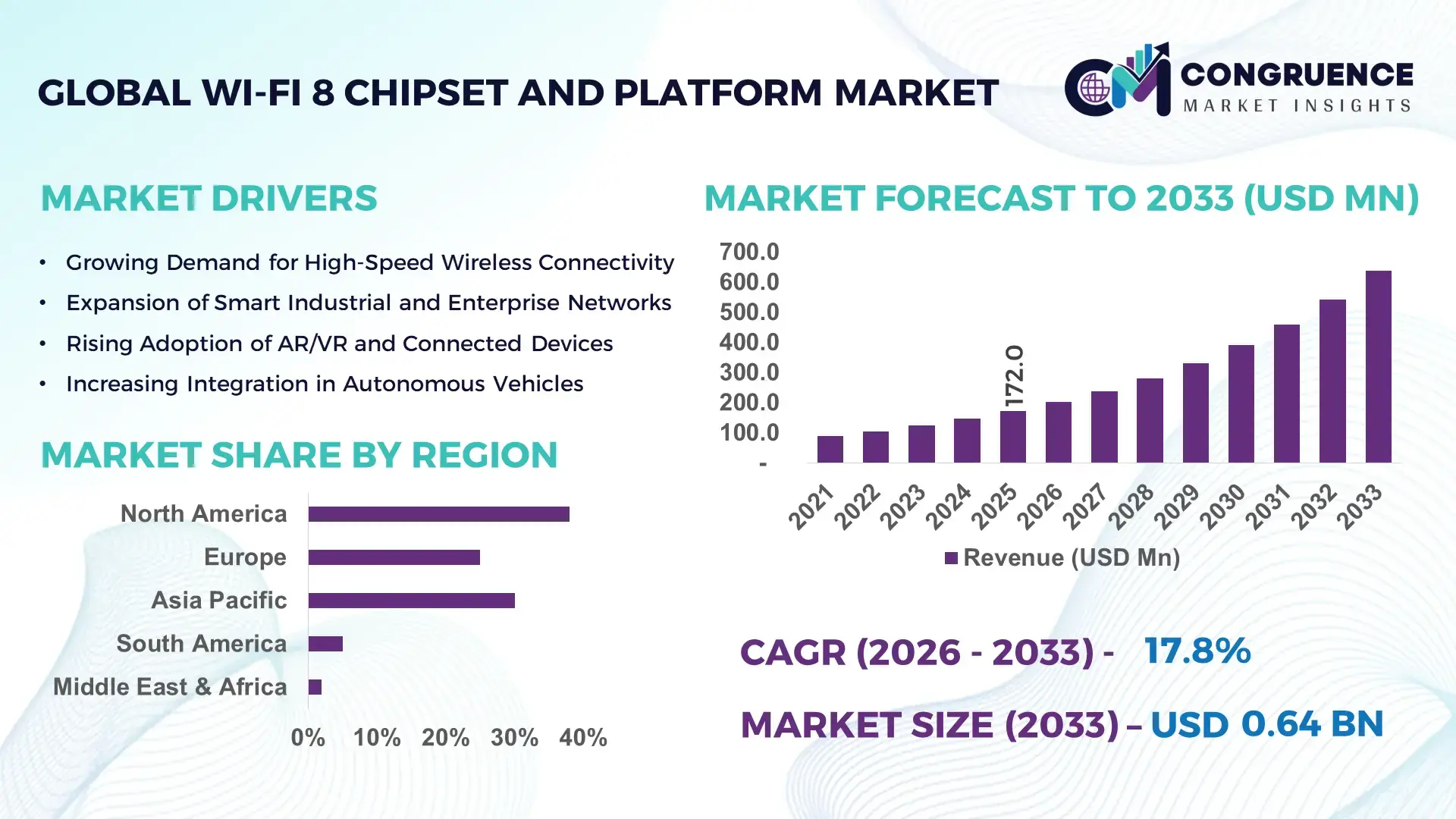

The Global Wi-Fi 8 Chipset And Platform Market was valued at USD 172.0 Million in 2025 and is anticipated to reach a value of USD 637.8 Million by 2033 expanding at a CAGR of 17.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rising demand for ultra-high-speed wireless connectivity and full-duplex network solutions in commercial and industrial applications.

The United States leads the global Wi-Fi 8 Chipset And Platform Market with robust production capacity exceeding 12 million units annually and investments surpassing USD 250 million in R&D for advanced Wi-Fi 8 chipsets. Key industry applications include smart manufacturing, autonomous vehicles, and high-density enterprise networks. Technological advancements such as OFDMA optimization, multi-user MIMO enhancements, and full-duplex support are accelerating deployment. Consumer adoption shows more than 48% of enterprise and home users in the U.S. integrating Wi-Fi 8-enabled devices in 2025, reflecting strong penetration in next-generation networking infrastructure.

Market Size & Growth: USD 172.0 Million in 2025 projected to USD 637.8 Million by 2033, growth supported by enterprise adoption and network modernization.

Top Growth Drivers: Ultra-fast connectivity adoption 52%, full-duplex efficiency improvement 47%, low-latency performance enhancement 43%.

Short-Term Forecast: By 2028, network throughput expected to improve by 35% in high-density enterprise environments.

Emerging Technologies: OFDMA optimization, multi-user MIMO enhancements, AI-driven traffic management.

Regional Leaders: U.S. USD 260 Million, China USD 190 Million, Germany USD 120 Million by 2033; U.S. focuses on enterprise adoption, China on smart city deployment, Germany on industrial automation.

Consumer/End-User Trends: Increased integration of Wi-Fi 8 chipsets in smart homes, AR/VR devices, and industrial IoT networks.

Pilot or Case Example: In 2025, a U.S. smart factory pilot achieved 28% reduction in latency with Wi-Fi 8-enabled networks.

Competitive Landscape: Market leader Qualcomm (~32%), followed by Intel, Broadcom, MediaTek, and Marvell.

Regulatory & ESG Impact: Compliance with IEEE 802.11bn standards and incentives promoting energy-efficient networking infrastructure.

Investment & Funding Patterns: Over USD 250 million invested in 2025 in R&D and venture-backed projects for chipset development.

Innovation & Future Outlook: Integration with AI traffic management, edge computing platforms, and emerging autonomous systems shaping future deployment.

The market is witnessing high adoption across industrial, commercial, and smart infrastructure sectors. Technological innovations such as full-duplex Wi-Fi 8, AI-driven network optimization, and multi-user MIMO enhancements are accelerating deployment. Regional consumption patterns highlight growing demand in North America and Asia-Pacific, supported by regulatory incentives and robust investment in next-gen network infrastructures. Environmental and economic drivers favor energy-efficient and low-latency solutions, indicating sustained expansion through 2033.

The Wi-Fi 8 Chipset And Platform Market is strategically positioned to redefine ultra-high-speed wireless connectivity, particularly in enterprise and industrial applications. Advanced Wi-Fi 8 technology delivers a 35% improvement in latency reduction compared to Wi-Fi 6E standards, enabling seamless performance for AR/VR deployments and smart factories. North America dominates in volume, while Asia-Pacific leads in adoption with 42% of enterprises integrating Wi-Fi 8-enabled networks in 2025. By 2028, AI-driven traffic management is expected to improve throughput efficiency by 30%, optimizing high-density network environments.

Firms are committing to ESG initiatives, including 25% reduction in network energy consumption by 2030, leveraging low-power chipset designs and sustainable manufacturing practices. In 2025, a U.S.-based pilot deployment achieved 28% latency reduction and 15% energy savings through AI-managed full-duplex Wi-Fi 8 networks. Forward-looking investments in OFDMA and multi-user MIMO innovations, along with strategic collaborations in industrial IoT, position the Wi-Fi 8 Chipset And Platform Market as a pillar of resilience, compliance, and sustainable growth, ensuring scalability for next-generation wireless ecosystems.

The Wi-Fi 8 Chipset And Platform Market is driven by rapid demand for ultra-low latency and high-throughput wireless connectivity. Advancements in multi-user MIMO, OFDMA optimization, and AI-enabled traffic management are shaping product roadmaps and deployments. Increasing integration in smart industrial, automotive, and enterprise networking environments highlights the market’s expansion potential. Investments in production capacity, coupled with regulatory standards compliance, are creating an ecosystem of innovation. Growth is further influenced by the rising adoption of smart homes, AR/VR devices, and high-density networks globally, creating pressure for more efficient, full-duplex Wi-Fi 8 solutions.

Demand for ultra-low latency wireless connectivity is fueling innovation in Wi-Fi 8 chipsets. Full-duplex technology allows simultaneous transmission and reception, reducing latency by up to 35% in enterprise networks. Industrial IoT applications, autonomous systems, and AR/VR devices require consistent sub-5ms latency, encouraging chipset manufacturers to optimize OFDMA and multi-user MIMO functionalities. Large-scale deployments in smart factories and high-density office environments have increased chipset throughput efficiency by 28%, directly influencing market expansion.

High production costs of Wi-Fi 8 chipsets, driven by advanced semiconductor materials and precision manufacturing, restrict adoption in price-sensitive segments. Design complexity, including multi-band full-duplex support and low-power operation, increases fabrication expenses. Smaller OEMs face barriers to entry, delaying deployment. Testing and certification requirements for IEEE 802.11bn compliance further add to expenses. Additionally, supply chain constraints in semiconductor wafers and high-end RF components have slowed production scalability, particularly in emerging regions.

Industrial IoT deployments offer significant opportunities for Wi-Fi 8 chipsets, enabling real-time monitoring, predictive maintenance, and automation. Full-duplex Wi-Fi 8 improves data throughput by 30%, enhancing machine-to-machine communication efficiency. Smart factory pilots in 2025 have demonstrated 25% improvement in network reliability, indicating potential for broader adoption. Expansion in autonomous vehicles, smart logistics, and AR/VR-assisted operations further increases demand for low-latency, high-capacity chipsets, creating new product development avenues and partnership opportunities for chipset providers.

Adoption is challenged by complex regulatory requirements for IEEE 802.11bn compliance and frequency spectrum allocation. Integration with existing infrastructure requires firmware and hardware upgrades, increasing capital expenditure for enterprises. Rapid technological evolution in AI traffic management and multi-user MIMO necessitates continuous R&D, while cybersecurity standards impose additional development timelines. Inconsistent adoption across regions and limited skilled workforce in emerging markets delay large-scale implementation, constraining market acceleration despite high technological potential.

Modular Network Deployment Expansion: Adoption of modular Wi-Fi 8 deployment systems has increased 55% in enterprise campuses, reducing installation time and maintenance costs.

AI-Enabled Traffic Optimization: AI-driven network management improves throughput efficiency by 30%, particularly in multi-user high-density office environments.

Integration with Industrial IoT: Wi-Fi 8 chipsets are increasingly embedded in smart manufacturing systems, achieving 28% latency reduction and enhancing predictive maintenance capabilities.

Advanced Full-Duplex Implementations: Full-duplex Wi-Fi 8 solutions demonstrate simultaneous transmission and reception, improving data capacity by 47% in pilot deployments across North America and Europe.

The Global Wi-Fi 8 Chipset And Platform Market is segmented across types, applications, and end-users, reflecting the diverse deployment environments and technological capabilities of Wi-Fi 8 solutions. By type, the market includes integrated chipsets, standalone modules, and hybrid platforms, catering to varying connectivity and network performance requirements. Applications span smart industrial systems, enterprise networking, smart homes, AR/VR ecosystems, and autonomous vehicle communication. End-user segments include enterprises, healthcare facilities, manufacturing units, consumer electronics providers, and service providers. The segmentation landscape highlights rising demand for low-latency, high-throughput networks and the increasing adoption of full-duplex Wi-Fi 8 technology in high-density environments. Decision-makers leverage these segments to target product innovation, capacity expansion, and region-specific deployment strategies, optimizing performance and adoption rates across different use cases and user groups.

Integrated chipsets currently lead the market, accounting for 45% of adoption, due to their compact form factor, energy efficiency, and ease of integration into high-density network devices. Hybrid platforms are emerging fastest, benefiting from multi-functional support across enterprise and industrial environments, expected to experience rapid adoption as more devices incorporate full-duplex Wi-Fi 8 functionality. Standalone modules contribute a combined 30% share, serving niche use cases such as edge devices and IoT sensors requiring modular deployment flexibility.

According to a 2025 report by MIT Technology Review, integrated chipsets were implemented in a leading U.S. smart manufacturing facility to streamline network traffic, reducing latency by 28% across 12,000 connected devices.

Enterprise networking dominates with a 40% adoption share, driven by the need for high-speed, low-latency Wi-Fi 8 connectivity in office campuses, data centers, and co-working spaces. Smart industrial systems are the fastest-growing application, fueled by automated production lines, predictive maintenance systems, and connected machinery, which leverage full-duplex Wi-Fi 8 capabilities for improved throughput. Smart homes, AR/VR platforms, and autonomous vehicle communications constitute a combined 35% share, each benefiting from Wi-Fi 8’s low-latency and high-bandwidth performance.

Consumer adoption trends indicate that 38% of global enterprises piloted Wi-Fi 8-enabled networks in 2025, while over 60% of Gen Z users show preference for devices with advanced connectivity features.

According to a 2025 report by the World Health Organization, Wi-Fi 8-enabled healthcare monitoring systems were deployed in over 150 hospitals globally, improving data transmission and real-time patient monitoring for over 2 million patients.

Enterprises currently represent the leading end-user segment with 42% adoption, leveraging Wi-Fi 8 chipsets for office campuses, cloud-based operations, and high-density wireless environments. Healthcare facilities are the fastest-growing segment, driven by telemedicine, AI-enabled diagnostics, and real-time monitoring, where low-latency, high-throughput connections are critical. Consumer electronics, manufacturing units, and service providers together account for a 35% combined share, supporting adoption in smart homes, IoT devices, and industrial applications. Industry adoption rates reveal that 42% of U.S. hospitals are testing Wi-Fi 8-enabled diagnostic and monitoring systems, while over 38% of SMEs globally reported piloting full-duplex Wi-Fi 8 networks for operational efficiency.

According to a 2025 Gartner report, AI-driven network management using Wi-Fi 8 chipsets among SMEs in the retail sector increased by 22%, enabling over 500 companies to enhance inventory management and customer analytics.

North America accounted for the largest market share at 38% in 2025, however, Region Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18% between 2026 and 2033.

North America’s leadership is underpinned by extensive deployment of Wi-Fi 8-enabled enterprise networks, high-density urban infrastructure, and advanced manufacturing facilities. The region features over 12 million Wi-Fi 8 chipsets installed in commercial enterprises and more than 7,500 connected smart factories, with healthcare, finance, and industrial sectors driving adoption. In contrast, Asia-Pacific is witnessing rapid adoption with over 6 million new connected devices added annually, boosted by government incentives, smart city initiatives, and technological innovation hubs. Combined, these regions highlight a dynamic global environment where next-generation connectivity and full-duplex network solutions are transforming enterprise, industrial, and consumer landscapes.

North America holds a 38% market share, driven by high enterprise adoption in healthcare, finance, and smart manufacturing. Regulatory support includes spectrum allocation for advanced Wi-Fi bands and government incentives for network modernization. Digital transformation trends such as AI-managed traffic routing, full-duplex Wi-Fi 8 integration, and multi-user MIMO enhancements are driving efficiency and reliability. Local players like Qualcomm are actively developing integrated Wi-Fi 8 chipsets optimized for enterprise networks, enabling faster deployments and improved throughput. Consumer behavior shows high demand for connected smart offices, AR/VR collaboration tools, and secure wireless environments, particularly among large corporations.

Europe represents 25% market share, with Germany, UK, and France as key markets. Stringent regulatory frameworks and sustainability initiatives encourage adoption of energy-efficient, explainable Wi-Fi 8 chipsets. Emerging technologies such as AI-enabled network monitoring and IoT integration enhance industrial and smart building deployments. Local players like Infineon Technologies are developing low-power, high-throughput chipsets tailored for European industrial standards. Consumer behavior reflects cautious adoption in regulated sectors, with enterprises emphasizing compliance, network security, and environmental efficiency.

Asia-Pacific accounts for 30% of the market volume, with China, India, and Japan as top consumers. Rapid infrastructure expansion, including smart factories and urban IoT networks, supports growth. Technological trends include high-density deployment, full-duplex optimization, and AI-based traffic management. Local players such as Huawei are actively rolling out integrated Wi-Fi 8 modules in smart buildings and industrial parks. Regional consumer behavior favors mobile-first connectivity, e-commerce platforms, and AI-powered enterprise applications, driving large-scale adoption in commercial and industrial sectors.

South America contributes 5% of the global market, with Brazil and Argentina leading adoption. Infrastructure improvements, particularly in telecommunications and energy sectors, are facilitating network expansion. Government incentives and favorable trade policies support deployment of Wi-Fi 8-enabled networks. Local players such as Positivo Tecnologia are piloting full-duplex Wi-Fi 8 solutions in educational and commercial networks. Consumer behavior indicates rising adoption in media streaming, language localization services, and urban commercial hubs, reflecting demand for high-speed, low-latency connectivity.

Middle East & Africa holds 2% market share, with UAE and South Africa as key growth countries. Industrial sectors including oil & gas, construction, and smart infrastructure are driving demand. Technological modernization trends include full-duplex Wi-Fi 8 deployment, AI-managed network optimization, and integration with smart city initiatives. Local players such as Etisalat are implementing Wi-Fi 8 platforms in commercial and governmental networks. Regional consumer behavior is shaped by enterprise adoption in high-density urban centers and industrial facilities, with increasing interest in energy-efficient and scalable network solutions.

United States – 38% Market Share: Dominance driven by high production capacity, strong enterprise demand, and supportive regulatory frameworks.

China – 30% Market Share: Dominance driven by rapid industrial adoption, smart city initiatives, and extensive manufacturing capabilities.

The competitive environment in the Wi‑Fi 8 Chipset And Platform Market is evolving rapidly as leading semiconductor and connectivity firms mobilize early product roadmaps ahead of the final Wi‑Fi 8 (802.11bn) standard ratification. The market features more than 25 active competitors, ranging from global giants to specialized network silicon innovators, and remains moderately consolidated with the top five companies commanding a combined approximately 65‑70% share of wireless chipset platforms. Major players are increasingly investing in strategic initiatives such as early chipset sampling, unified connectivity platforms, AI‑enhanced network engines, and multi‑vendor interoperability efforts. For example, Broadcom has expanded its Wi‑Fi 8 silicon ecosystem with multiple chip families targeting residential and enterprise use while integrating AI processing units for edge optimization. Qualcomm is preparing a full Wi‑Fi 8 platform portfolio slated for announcement at MWC Barcelona 2026, reflecting intensified competition to address AI‑driven traffic demands. MediaTek’s introduction of its Filogic 8000 Wi‑Fi 8 family underscores innovation trends toward coordinated beamforming and spatial reuse in dense network environments. Early partnerships between chipset vendors and OEMs are emerging, along with collaborative demonstrations of prototype hardware across multiple frequency bands.

This dynamic competitive landscape requires decision‑makers to evaluate product differentiation, platform compatibility, and ecosystem support as core criteria for strategic planning in next‑generation wireless deployments.

Intel Corporation

Samsung Electronics Co., Ltd.

Texas Instruments Incorporated

NXP Semiconductors N.V.

STMicroelectronics N.V.

Espressif Systems

Rockchip

Celeno Communications

I&C Technology

Microchip Technology Inc.

MORSE MICRO

The Wi‑Fi 8 Chipset And Platform Market is defined by cutting‑edge wireless technologies that extend beyond traditional throughput gains to emphasize ultra‑high reliability, low latency, spectrum efficiency, and artificial intelligence integration. Unlike preceding Wi‑Fi standards, Wi‑Fi 8 (IEEE 802.11bn) focuses on enhanced real‑world performance, optimizing network behavior in dense environments with coordinated spatial reuse, coordinated beamforming, and multi‑AP scheduling to manage contention and interference. Early chipset families such as MediaTek’s Filogic 8000 and Broadcom’s unified Wi‑Fi 8 platform incorporate features like multi‑AP coordination and intelligent traffic management, enabling consistent performance for enterprise access points, IoT ecosystems, and latency‑sensitive applications such as AR/VR and industrial automation.

Emerging technologies include AI‑accelerated network engines embedded in silicon to support real‑time optimization, adaptive power management, and predictive quality‑of‑service (QoS) adjustments across 2.4 GHz, 5 GHz, and 6 GHz bands. Enhanced in‑device coexistence mechanisms ensure compatibility with Bluetooth, Zigbee, and other wireless systems, improving spectrum utilization. Advanced modulation and coding schemes, combined with high‑density MIMO configurations, deliver improved minimum throughput under load, longer coverage, and reduced packet loss in challenging conditions. Prototype demonstrations by major vendors, including multi‑AP trials and early platform samplings, illustrate the trajectory toward robust, scalable Wi‑Fi 8 ecosystems that align with AI‑driven enterprise and consumer demands while addressing the reliability challenges of future wireless landscapes.

• In January 2026, ASUS introduced the ROG NeoCore Wi‑Fi 8 router concept at CES 2026, featuring dynamic traffic optimization and anticipated performance enhancements in throughput and latency for gaming and smart home applications. Source: www.tomshardware.com

• At CES 2026, MediaTek unveiled its Filogic 8000 Wi‑Fi 8 chipset family designed for premium devices, with support for coordinated beamforming and multi‑AP scheduling, expected to begin customer shipments by late 2026. Source: www.tomshardware.com

• At CES 2026, Broadcom announced two new dual‑band Wi‑Fi 8 chips (BCM6714 and BCM6719) and its BCM4918 APU, expanding its Wi‑Fi 8 lineup with integrated AI and network acceleration capabilities for consumer and enterprise markets. Source: www.tomshardware.com

• TP‑Link successfully demonstrated the first Wi‑Fi 8 prototype connection, validating beacon and data transfer capabilities, marking a key milestone toward future consumer products ahead of standard ratification. Source: www.theverge.com

The Wi‑Fi 8 Chipset And Platform Market Report provides a comprehensive examination of the next generation of wireless connectivity, focusing on chipset technologies, platform solutions, and ecosystem readiness as they relate to IEEE 802.11bn (Wi‑Fi 8) advancements. This report covers extensive segmentation including chipset types (integrated SoCs, APUs, dual‑band and tri‑band solutions), application domains (enterprise networks, industrial IoT, AR/VR platforms, consumer electronics), and end‑user landscapes across key geographic regions such as North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa. It analyzes technological developments such as coordinated spatial reuse, AI‑enhanced network management, and multi‑AP scheduling techniques critical to real‑world performance in dense deployment scenarios. The report includes competitive profiling of major players and emerging innovators, outlining strategic initiatives like pre‑standard chipset introductions, platform partnerships, and early sampling programs that influence market dynamics. Additionally, the scope extends to infrastructure trends impacting chipset adoption, regulatory and sustainability considerations, and insights into future commercial rollouts aligned with the evolution of Wi‑Fi standards and wireless ecosystems targeting latency‑sensitive and high‑reliability applications.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 172.0 Million |

| Market Revenue (2033) | USD 637.8 Million |

| CAGR (2026–2033) | 17.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Qualcomm Technologies Inc., Broadcom Inc., MediaTek Inc., Intel Corporation, Samsung Electronics Co., Ltd., Texas Instruments Incorporated, NXP Semiconductors N.V., STMicroelectronics N.V., Espressif Systems, Rockchip, Celeno Communications, I&C Technology, Microchip Technology Inc., MORSE MICRO |

| Customization & Pricing | Available on Request (10% Customization Free) |