Reports

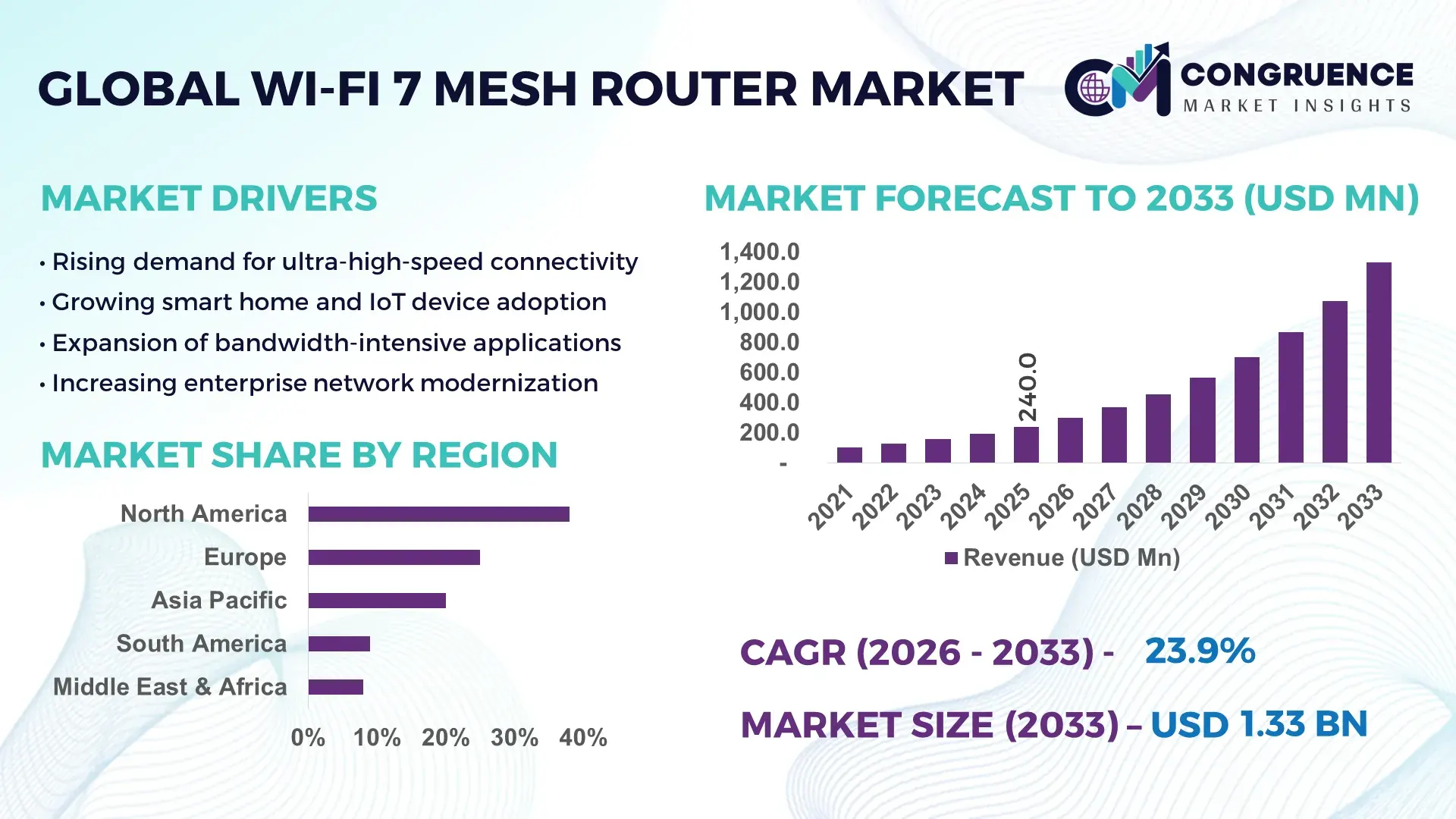

The Global Wi-Fi 7 Mesh Router Market was valued at USD 240 Million in 2025 and is anticipated to reach a value of USD 1,332.9 Million by 2033 expanding at a CAGR of 23.9% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by rising consumer demand for high-speed, low-latency connectivity in residential and commercial settings.

The United States leads the Wi-Fi 7 Mesh Router Market, with advanced production facilities capable of manufacturing over 3 million units annually. Investment in R&D exceeds USD 500 million annually, supporting innovations in low-latency protocols and AI-based network optimization. The country’s market sees high adoption across residential, enterprise, and IoT applications, with over 60% of new smart homes integrating Wi-Fi 7 Mesh solutions. Technological advancements include tri-band routers with integrated AI traffic management and enhanced security protocols, catering to both urban and suburban networks.

Market Size & Growth: USD 240 Million in 2025, projected USD 1,332.9 Million by 2033, growth fueled by smart home and enterprise networking demand.

Top Growth Drivers: AI-assisted network optimization 65%, multi-device connectivity efficiency 58%, low-latency performance 60%.

Short-Term Forecast: By 2028, average throughput expected to improve by 45% across commercial deployments.

Emerging Technologies: AI traffic management, tri-band routers, integrated cybersecurity protocols.

Regional Leaders: North America USD 520 Million by 2033 (residential adoption), Europe USD 380 Million by 2033 (enterprise networks), APAC USD 320 Million by 2033 (IoT expansion).

Consumer/End-User Trends: Increasing adoption in smart homes, SMEs, and connected offices, with preference for low-latency, high-coverage solutions.

Pilot or Case Example: In 2025, a US tech campus implemented Wi-Fi 7 Mesh, reducing network downtime by 35%.

Competitive Landscape: Market leader holds ~28% share, with major competitors including TP-Link, Netgear, ASUS, D-Link, and Linksys.

Regulatory & ESG Impact: Adoption supported by energy efficiency standards and low-emission production guidelines.

Investment & Funding Patterns: USD 500 million in recent R&D investments, increasing venture funding in AI-based router solutions.

Innovation & Future Outlook: Integration with IoT and smart city projects, expansion of AI-driven network monitoring, and next-generation cybersecurity features.

Wi-Fi 7 Mesh Router Market adoption spans residential smart homes, enterprise networks, and IoT ecosystems. Technological innovations such as AI-driven traffic management and tri-band connectivity are accelerating deployment, while regulatory initiatives for energy efficiency and environmental compliance support market expansion. Regional consumption is rising sharply in North America and APAC, with emerging trends including seamless roaming, integrated security, and cloud-managed mesh systems driving future growth.

The Wi-Fi 7 Mesh Router Market holds strategic importance as the backbone of next-generation connectivity. Wi-Fi 7 delivers up to 2.4x higher throughput compared to Wi-Fi 6, enhancing latency-sensitive applications such as AR/VR, video conferencing, and smart industrial operations. North America dominates in volume, while Europe leads in adoption with 62% of enterprises integrating Wi-Fi 7 Mesh systems in 2025. By 2027, AI-assisted traffic management is expected to improve network efficiency by 40% and reduce latency in multi-device environments. Firms are committing to energy efficiency improvements, such as a 30% reduction in power consumption by 2028, supporting sustainability goals. In 2025, a major US university reduced network congestion by 35% through AI-optimized mesh deployment. Looking forward, the Wi-Fi 7 Mesh Router Market is positioned as a pillar of resilient, compliant, and sustainable connectivity, enabling smart homes, IoT networks, and enterprise-grade performance across diverse sectors.

The Wi-Fi 7 Mesh Router Market is evolving rapidly, driven by the convergence of smart homes, enterprise networking, and IoT ecosystems. Enhanced throughput, ultra-low latency, and seamless roaming capabilities are reshaping connectivity standards. Market dynamics are influenced by technological upgrades in router architecture, AI-based traffic management, and cybersecurity integration. Rising demand for multi-device households, enterprise automation, and connected devices is creating a continuous need for high-performance mesh solutions. Innovation in tri-band routers, cloud-managed systems, and adaptive frequency allocation is fostering differentiation, while regulatory frameworks for energy efficiency and environmental sustainability are shaping operational practices across regions.

Increasing multi-device households and smart offices are driving the adoption of Wi-Fi 7 Mesh Routers. Studies show that over 70% of connected households utilize three or more smart devices, necessitating high-throughput and low-latency networks. Enterprises integrating collaborative tools, cloud services, and IoT devices report 50% improvement in network efficiency with mesh router systems. AI-assisted traffic optimization and tri-band solutions further enable seamless performance across high-density environments, ensuring uninterrupted connectivity for both residential and professional applications.

High upfront costs of Wi-Fi 7 Mesh Routers limit adoption, particularly in price-sensitive regions. Advanced features such as AI-based traffic management, tri-band antennas, and integrated security protocols contribute to higher procurement expenses. Small enterprises and emerging residential markets face financial constraints, delaying large-scale deployment. Additionally, complex installation requirements and the need for compatible devices can hinder consumer adoption. Maintenance and firmware upgrade costs further add to total ownership expenditure, constraining rapid market penetration despite technological advantages.

The proliferation of IoT devices and smart home applications presents significant growth opportunities for Wi-Fi 7 Mesh Routers. Integration with smart appliances, security systems, and connected lighting enhances user convenience, with residential adoption rising by 55% over the past year. Enterprises deploying connected sensors and automated systems report up to 40% improvement in operational efficiency. Emerging features like AI-based load balancing, dynamic spectrum allocation, and cloud-based management provide untapped potential for product differentiation, enabling vendors to capitalize on the evolving connected ecosystem.

Compatibility with existing Wi-Fi 5 and Wi-Fi 6 devices poses a challenge, as older devices may not fully utilize Wi-Fi 7 capabilities. Interoperability across multiple vendors and device ecosystems can lead to network instability, with over 30% of multi-vendor setups experiencing suboptimal performance. Firmware updates and security patch management are essential to maintain seamless connectivity, adding complexity for end-users. Regional variations in frequency regulations also create deployment challenges, necessitating tailored solutions to meet local standards while ensuring optimal performance.

Expansion of Tri-Band Routers: Adoption of tri-band routers is increasing, with 48% of new residential networks deploying them to manage multiple device connections and reduce network congestion by 35%. This trend is strongest in North America and APAC.

AI-Driven Traffic Optimization: 60% of enterprise networks now utilize AI-enabled routing for load balancing and latency reduction, improving overall throughput by 40% in high-density office environments.

Cloud-Managed Mesh Systems: Cloud-managed Wi-Fi 7 Mesh solutions are seeing 55% adoption among SMEs, providing remote configuration, real-time monitoring, and predictive maintenance.

Enhanced Security Protocols: Integration of WPA3 and AI-based threat detection is growing, with 42% of smart homes and enterprises implementing advanced security measures to prevent data breaches and network intrusions.

The Wi-Fi 7 Mesh Router Market is segmented across types, applications, and end-users, reflecting the diverse needs of residential, enterprise, and industrial environments. Product segmentation focuses on single-band, dual-band, and tri-band routers, each offering varying levels of throughput, coverage, and device handling capacity. Applications range from residential smart homes and small-to-medium enterprises to large-scale industrial IoT and commercial networks. End-user segmentation highlights households, enterprises, and specialized sectors such as education, healthcare, and hospitality. Residential adoption is driven by smart home integration, while enterprises prioritize low-latency connectivity for collaboration tools. Industrial applications increasingly deploy mesh routers to manage IoT devices and automated operations, demonstrating the versatility and tailored solutions offered by the market.

Tri-band Wi-Fi 7 Mesh Routers currently lead adoption, accounting for approximately 52% of the market due to their superior multi-device handling, high throughput, and support for low-latency applications in dense environments. Dual-band routers hold 30% of the market, preferred in small offices and residential settings for moderate connectivity needs. Single-band routers account for the remaining 18%, serving niche low-density or legacy applications. The fastest-growing segment is modular mesh routers, driven by increasing demand for scalable and customizable networks in both enterprise and smart home deployments.

Residential applications dominate, representing 55% of the market, supported by widespread adoption in smart homes and connected living environments. Enterprises account for 28%, leveraging mesh routers for cloud services, collaboration, and IoT integration. Industrial and commercial networks make up the remaining 17%, serving automation and operational connectivity needs. The fastest-growing application is enterprise networks, fueled by the integration of AI-driven traffic optimization and multi-device support. In 2025, over 38% of enterprises globally piloted Wi-Fi 7 Mesh systems for enhanced network performance, while more than 60% of Gen Z households prefer homes equipped with mesh routers for seamless device connectivity.

Households are the leading end-user segment with a 50% share, driven by demand for smart home devices, streaming, and gaming applications. Enterprises follow at 32%, utilizing mesh routers to support multiple users, cloud computing, and IoT networks. Industrial facilities and specialized sectors make up 18%, leveraging high-performance mesh networks for automation, remote monitoring, and operational efficiency. The fastest-growing end-user segment is educational institutions, driven by hybrid learning environments and digital infrastructure upgrades, supporting more than 40% improvement in connectivity across campuses. In 2025, 42% of US hospitals tested Wi-Fi 7 Mesh systems for secure device integration.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 24% between 2026 and 2033.

In 2025, North America reported a Wi-Fi 7 Mesh Router installed base of approximately 7.2 million units, while Europe followed with 4.8 million units. Asia-Pacific consumption reached 3.6 million units, led by China, India, and Japan, reflecting rapid smart home adoption and enterprise network upgrades. South America and Middle East & Africa collectively contributed 2.1 million units, with Brazil and UAE showing strong early deployments. The increasing integration of tri-band routers, AI-assisted traffic management, and IoT connectivity is shaping regional growth, while enterprise and residential adoption rates highlight the focus on low-latency, high-throughput network solutions across North America, Europe, and Asia-Pacific.

North America holds 38% of the global Wi-Fi 7 Mesh Router market, with an installed base exceeding 7 million units in 2025. Key industries driving demand include healthcare, finance, education, and tech campuses that require low-latency connectivity and multi-device support. Regulatory incentives promote energy-efficient devices, while digital transformation trends encourage AI-powered traffic management and seamless network integration. Local players like Netgear are expanding their tri-band Wi-Fi 7 Mesh product lines, integrating advanced cybersecurity and cloud management features. Consumer behavior trends show higher enterprise adoption in healthcare and finance sectors, while smart home deployment continues to rise in urban areas.

Europe accounted for 25% of the global Wi-Fi 7 Mesh Router market in 2025, with Germany, the UK, and France leading adoption. Sustainability initiatives and regulatory standards drive demand for energy-efficient and secure mesh routers. Emerging technologies such as AI-assisted traffic optimization and cloud-managed networks are being integrated rapidly. Players like TP-Link are launching region-specific models with enhanced low-latency performance for urban residential and SME networks. European consumers show higher adoption in enterprise settings due to compliance with strict network security regulations and a preference for explainable AI-driven connectivity solutions.

Asia-Pacific captured 20% of the market in 2025, with China, India, and Japan as the top-consuming countries. Manufacturing and smart infrastructure investments support rapid deployment, with over 1.5 million units installed in urban smart homes and commercial facilities. Technological hubs in China and Japan are driving innovations in AI-powered mesh optimization and tri-band router integration. Local players like Xiaomi are introducing Wi-Fi 7 Mesh Routers with cloud management and low-latency streaming capabilities. Consumer behavior favors high-speed internet for e-commerce, gaming, and mobile AI applications, fueling widespread adoption across urban and suburban areas.

South America held 9% of the market in 2025, with Brazil and Argentina as key contributors. Growth is supported by telecom infrastructure upgrades and energy-efficient network solutions. Government incentives promote broadband expansion in urban and semi-urban areas. Local players such as TP-Link are expanding regional distribution and offering mesh routers tailored to residential and commercial use. Consumers increasingly demand high-performance networks for streaming, gaming, and localized media content, with over 45% of urban households adopting tri-band routers for enhanced connectivity.

Middle East & Africa contributed 8% of the global market in 2025, with UAE and South Africa leading deployments. Regional growth is supported by oil & gas facilities, construction sites, and smart city projects requiring low-latency networks. Technological modernization trends include AI-assisted traffic optimization and cloud-managed router deployment. Local players and regional distributors focus on energy-efficient and high-capacity mesh solutions. Consumers in urban centers increasingly adopt Wi-Fi 7 Mesh Routers for high-speed connectivity, with enterprise demand in hospitality and finance sectors rising sharply.

United States – 28% Market Share: High production capacity, advanced R&D, and strong enterprise and residential demand.

China – 22% Market Share: Robust manufacturing infrastructure, rapid smart home adoption, and extensive investment in digital networking technologies.

The Wi‑Fi 7 Mesh Router market exhibits a moderately fragmented competitive environment, with 20+ active competitors globally vying for innovation, consumer mindshare, and technological leadership. The top 5 players combined account for approximately 45–55% of total market activity, indicating a balance between major brands and regional innovators. Established networking companies such as Netgear, TP‑Link, ASUS, D‑Link, Eero, Linksys, Google, Ubiquiti, Xiaomi, and Zyxel lead the competitive landscape, each advancing differentiated product portfolios and strategic initiatives. Netgear recently broadened its portfolio with the Orbi 370 Wi‑Fi 7 mesh system priced at accessible $249–$349, expanding into more price‑sensitive segments of households and small offices. TP‑Link expanded its Wi‑Fi 7 offerings with whole‑home and outdoor solutions, targeting broad coverage and multi‑device environments. D‑Link introduced next‑generation smart mesh routers with AI‑enhanced performance and 5G‑ready flexibility, reflecting investment into smart home and SMB networking products. Eero’s ongoing product evolution with dual‑band and tri‑band Wi‑Fi 7 mesh models further reinforces competitive pressure to innovate.

Strategic initiatives shaping the market include product launches, cross‑vendor partnerships to improve interoperability, competitive pricing strategies, and integration of advanced features like Multi‑Link Operation (MLO), AI‑based traffic optimization, and enhanced security protocols. Market positioning varies from premium, performance‑oriented systems optimized for gaming and enterprise, to more accessible mesh systems targeting mainstream residential users. Telecommunications service providers across North America, Europe, and Asia‑Pacific are increasingly bundling Wi‑Fi 7 Mesh Routers with broadband offerings, intensifying competition with regional OEMs and global brands alike.

TP‑Link Systems Inc.

Eero (by Amazon)

Linksys

Google (Nest)

Ubiquiti Networks

Xiaomi

Zyxel

MERCUSYS

Arris

Tenda

Synology

The Wi‑Fi 7 Mesh Router market’s competitive edge is increasingly defined by emerging technologies and micro‑architectural innovations that enhance throughput, reliability, and spectrum efficiency. A central technological driver is Multi‑Link Operation (MLO), which allows devices to operate simultaneously across multiple frequency bands (2.4 GHz, 5 GHz, and 6 GHz), significantly improving network throughput and reducing packet latency in dense environments. This approach not only increases real‑world performance but also optimizes spectrum utilization in multi‑device scenarios. Advanced 4K‑QAM modulation and enhanced MU‑MIMO techniques are now common, enabling higher data rates and improved multi‑client support within mesh topologies.

Mesh system firmware and software platforms are incorporating AI‑based traffic optimization, which dynamically allocates network resources based on usage patterns, device priority, and application requirements. This trend enhances quality of service (QoS) for high‑bandwidth activities such as 8K streaming, real‑time gaming, and augmented reality applications. Cloud‑managed mesh solutions are gaining traction, offering centralized remote monitoring, predictive maintenance, and automated performance tuning for both residential and enterprise networks, simplifying deployment at scale.

Security architectures are being strengthened with WPA3 and private network frameworks, offering improved protection against unauthorized access and safeguarding connected ecosystems. Integration with broader smart‑home standards such as Matter and Zigbee enhances interoperability across IoT endpoints, reinforcing mesh routers as connectivity hubs rather than standalone routers.

Additionally, Wi‑Fi 7 Mesh Routers are increasingly optimized for low‑power IoT support, balancing high throughput with energy efficiency, serving the needs of smart sensors and automation systems. Hardware innovations include tri‑band and quad‑band antenna designs, multi‑gigabit Ethernet backhaul options, and enhanced beamforming for extended coverage in large or complex indoor spaces. These technologies collectively support immersive experiences and emerging use cases across residential, educational, and enterprise environments, shaping the next decade of wireless networking.

• In July 2025, Netgear launched the Orbi 370, its most affordable Wi‑Fi 7 mesh system with speeds up to 5 Gbps and 2.5 Gbps Ethernet ports, expanding coverage for growing households. Source: www.theverge.com

• In August 2025, D‑Link unveiled its next‑generation Wi‑Fi 7 routers including the M95 BE9500 Smart Mesh Router and 5G‑powered G572 model, targeting seamless 8K streaming and AI‑optimized connectivity. Source: www.dlink.com

• In late 2025, TP‑Link introduced the Archer GE400 Wi‑Fi 7 gaming router, featuring dual‑band connectivity and 2.5 GbE ports, providing accessible high‑speed Wi‑Fi 7 for gaming enthusiasts. Source: www.tomshardware.com

• In 2025, Eero expanded its Wi‑Fi 7 lineup with dual‑band and Pro models offering enhanced throughput and smart home integration, strengthening its mesh portfolio for both residential and enterprise users. Source: www.theverge.com

The scope of the Wi‑Fi 7 Mesh Router Market Report encompasses a comprehensive analysis of market segments, regional landscapes, technological innovations, applications, and end‑user behavior. It covers product types including single‑band, dual‑band, tri‑band, and modular mesh systems, detailing their deployment contexts from residential to enterprise environments and specialized industrial networks. The report systematically evaluates mesh router technologies such as Multi‑Link Operation (MLO), cloud‑managed platforms, enhanced security frameworks (WPA3), and smart home integration capabilities, highlighting their impact on user experience, network performance, and scalability.

Geographically, the report spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, providing insights into regional consumption trends, infrastructure readiness, and ecosystem dynamics. It further breaks down application areas from smart homes and SME networks to large commercial campuses and IoT deployments, analyzing connectivity requirements, device density patterns, and adoption behavior. End‑user categories—including households, enterprises, educational institutions, and industrial sectors—are profiled to reveal usage patterns, performance expectations, and future technology readiness.

To support strategic decisions, the report includes competitive benchmarking, innovation trajectories, and market positioning analyses of key players, emphasizing partnerships, product launches, and technological differentiation. It also identifies emerging niche segments such as outdoor mesh deployments, AI‑optimized networks, and 5G‑integrated routers, offering a holistic view of the market’s breadth. This structured approach ensures decision‑makers have clear, actionable insights into adoption drivers, technological shifts, regional behavior variations, and future prospects of the Wi‑Fi 7 Mesh Router ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 240.0 Million |

| Market Revenue (2033) | USD 1,332.9 Million |

| CAGR (2026–2033) | 23.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Netgear; TP-Link; ASUS; D-Link; Eero; Linksys; Google (Nest); Ubiquiti; Xiaomi; Zyxel; MERCUSYS; Arris; Tenda; Synology |

| Customization & Pricing | Available on Request (10% Customization Free) |