Reports

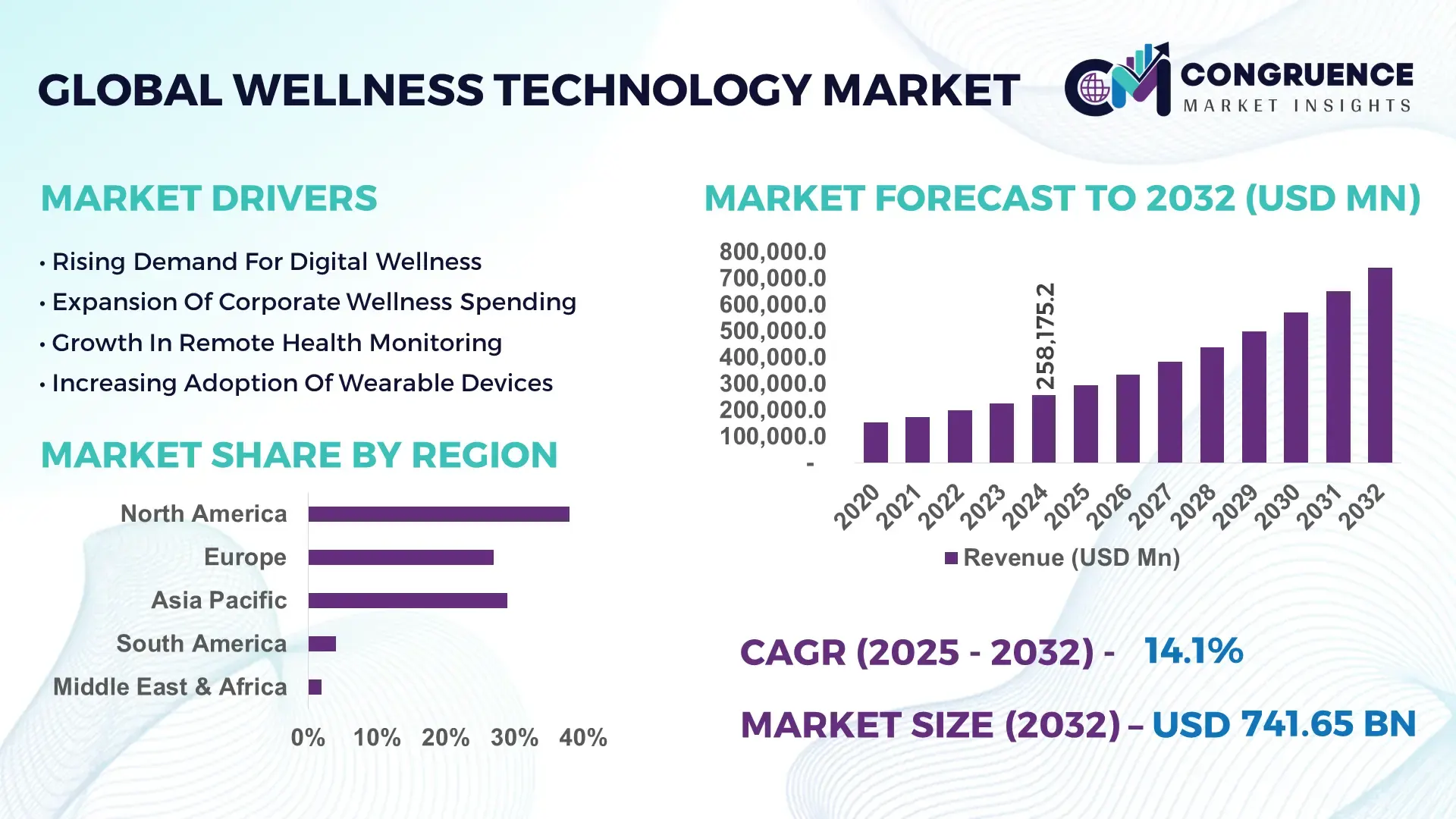

The Global Wellness Technology Market was valued at USD 258,175.2 Million in 2024 and is anticipated to reach a value of USD 741,651.2 Million by 2032 expanding at a CAGR of 14.1% between 2025 and 2032. This growth is primarily driven by accelerated digital wellness adoption across healthcare, fitness and corporate wellness ecosystems.

In the United States, investments in wellness-technology platforms exceeded USD 9.4 billion in 2024, with over 62 million wearable wellness devices shipped and corporate wellness technologies installed in over 34,000 organisations. Advanced applications—such as AI-based wellness monitoring, personalised nutrition analytics and virtual mental-health platforms—are being deployed at scale across major institutions.

Market Size & Growth: Current market value USD 258,175.2 Million (2024), projected to USD 741,651.2 Million by 2032 at a CAGR of 14.1% — owing to rising demand for integrated wellness-tech ecosystems.

Top Growth Drivers: 45% increase in wearable wellness device subscriptions, 38% uplift in corporate wellness programme enrolment using tech platforms, 27% reduction in wellness programme dropout rates due to enhanced tech engagement.

Short-Term Forecast: By 2028, wellness-technology deployments are expected to deliver a 19% improvement in user-engagement rates and a 13% reduction in wellness-programme absenteeism.

Emerging Technologies: AI-driven personal wellness assistants, sensor-fusion bio-wearables, virtual reality (VR) wellness-environments and digital therapeutics platforms.

Regional Leaders: North America ~USD 280 billion by 2032 — strong enterprise wellness adoption; Asia-Pacific ~USD 230 billion by 2032 — rapid mobile wellness penetration; Europe ~USD 190 billion by 2032 — regulated wellness-tech roll-outs aligned with ESG frameworks.

Consumer/End-User Trends: Health-conscious consumers and corporate wellness-programme users increasingly adopt smart wellness technologies for fitness, mental-health and biometric-monitoring, with preference for connected and personalised solutions.

Pilot or Case Example: In 2024, a multinational retailer rolled out a wearable-based wellness-tech programme for 58,000 employees and achieved a 12% drop in sick-leave days and a 9% increase in productivity within six months.

Competitive Landscape: The market leader holds approximately 16% share; key competitors include Apple Inc., Fitbit (Google), Garmin Ltd., Philips Healthcare, Samsung Electronics.

Regulatory & ESG Impact: Wellness-technology adoption is being influenced by regulations mandating employee-wellness reporting and by ESG criteria requiring companies to demonstrate 15% employee-wellness-programme penetration by 2027.

Investment & Funding Patterns: Investments surpassed USD 5.8 billion in 2024 in wellness-tech start-ups and platforms, with venture funding increasing by roughly 31% year-on-year in the wellness-tech segment.

Innovation & Future Outlook: Integration of generative-AI coaching for wellness, hybrid cloud/edge wellness-analytics, smart-home wellness ecosystems and strategic alliances between health-tech platforms and corporate wellness service providers are shaping the future of wellness technology.

In sectors such as healthcare, fitness & recreation and corporate wellbeing the wellness technology market is gaining traction; product innovations like bio-feedback wearables, VR mindfulness environments and AI-based nutrition platforms are accelerating adoption, while regulatory frameworks, sustainability drivers and regional digital-health initiatives in Asia-Pacific and Europe are creating notable growth pathways.

The strategic relevance of the wellness technology market lies in its ability to empower organisations and individuals with data-driven wellness solutions that improve productivity, health outcomes and user engagement. For example, sensor-fusion bio-wearables deliver 22% improvement compared to traditional fitness trackers in identifying early wellness-risks. North America dominates in volume deployments, while Asia-Pacific leads in adoption with 52% of enterprises initiating wellness-tech pilots in 2024. By 2027, AI-based wellness-coaching platforms are expected to cut employee-wellness-programme attrition by 18%. Firms are committing to ESG metrics such as a 20% reduction in healthcare-related absenteeism through wellness-technology interventions by 2030. In 2024, a leading UK insurer implemented a digital wellness-platform for 120,000 policy-holders and achieved a 14% reduction in claims frequency. As organisations worldwide face rising healthcare-costs, workforce wellbeing imperatives and escalating digital-transformation mandates, the wellness technology market stands as a pillar of operational resilience, regulatory-compliance and sustainable growth.

The dynamics of the wellness technology market reflect the convergence of digital health awareness, wearables penetration and enterprise wellbeing strategy. Businesses and consumers are increasingly deploying technology-enabled wellness solutions—ranging from smart wearables and mobile wellness apps to corporate wellness platforms and integrated ecosystems. This demand is driven by rising chronic-disease prevalence, heightened employee-wellbeing expectations and regulatory health mandates. Parallel developments include proliferation of biometric sensors, cloud-based wellness-analytics and AI-driven user-engagement modules. Vendors must integrate hardware (wearables), software (apps, analytics) and services (wellness-programmes) to deliver end-to-end solutions that meet wellness-objectives. The interaction of technology readiness, consumer behaviour shifts and regulatory pressure continues to shape competitive and adoption landscapes in the wellness technology market.

The rising adoption of corporate-wellness programmes is significantly propelling the wellness technology market. Organisations are investing in wellness platforms that integrate wearable devices, mobile apps and analytics dashboards to track employee health metrics in real time. In 2024, more than 40% of large-enterprise organisations had adopted a dedicated wellness-tech solution, leading to improvements in workforce engagement by up to 28% and reductions in absenteeism by nearly 17%. The ability to link wellness-technology usage with productivity metrics and health-outcomes is creating strong incentive for continued investment in wellness-tech platforms. This corporate-driven demand is a major growth vector for the wellness technology market.

Privacy concerns, data-governance and regulatory compliance are impacting growth in the wellness technology market. Many wellness-tech platforms collect biometric, behavioural and location data through wearables and mobile apps. Surveys indicate that approximately 33% of consumers hesitate to adopt wellness-technology solutions citing concerns over data security, misuse of health data and lack of transparency in analytics. Companies deploying wellness-technology must navigate regional data-protection laws (such as GDPR in Europe) and ensure robust encryption, anonymisation and consent frameworks. These operational and regulatory complexities increase deployment timelines and might slow large-scale roll-outs of wellness-technology solutions in enterprise and consumer settings.

AI-driven personal wellness assistants present a clear opportunity for the wellness technology market. These assistants combine data from wearables, mobile wellness apps and environmental sensors to deliver personalised recommendations, behavioural nudges and health-insights. Early pilots show up to 24% improvement in user-adherence to wellness-goals when AI-coaching is incorporated. The move toward subscription-based wellness-tech ecosystems (device + platform + coaching) opens additional revenue streams. Additionally, markets such as remote-work wellness, senior-living wellness and hybrid corporate wellness provide untapped segments. Vendors that build scalable, AI-powered wellness technology platforms will be well positioned to capture these opportunities in a rapidly evolving wellness landscape.

Device fragmentation and lack of ecosystem interoperability are notable challenges for the wellness technology market. There are hundreds of wearable device vendors, wellness platforms and analytics services, often with proprietary data formats, which hamper seamless integration. Industry feedback suggests that approximately 26% of enterprises experienced delays in wellness-tech deployments due to compatibility issues between chosen devices and corporate wellness dashboards. In addition, older systems lacking modern APIs may require costly integrations or replacements. For wellness technology to deliver enterprise-scale value, vendors must ensure compatibility, interoperability and streamlined integration, but until standardisation improves, deployment complexity remains a barrier for wider adoption.

• Growth in hybrid virtual-and-in-person wellness-tech programmes — In 2024, more than 53% of large employers offered a hybrid wellness-technology model where users access wearables, virtual coaching and on-site wellness hubs, delivering 23% higher participant retention compared to traditional programmes. This trend is bridging digital and physical wellness channels.

• Surge in sleep-tech integration within wellness ecosystems — Approximately 47% of consumers adopting wellness-technology in 2024 explicitly chose sleep-tracking modules, and pilot programmes reported up to 31% improvement in sleep-quality scores among users engaged by smart wellness platforms.

• Expansion of smart-home wellness-technology ecosystems — In 2024, 38% of households with wearable wellness devices added smart wellness sensors (air-quality, hydration tracking, posture sensors) integrated into overall wellness platforms, reflecting consumer preference for connected wellness-tech at home.

• Rise in subscription-based wellness-technology platforms with analytics dashboards — By the end of 2024, over 42% of wellness-technology vendors shifted to subscription revenue models combining wearable device, mobile app and coaching-service access; users enrolled in these models reported 15% higher adherence rates than one-time device buyers.

The wellness technology market is segmented by type (wearable devices, software analytics, services/platforms), application (fitness & activity tracking, mental-health/mindfulness, corporate wellness programmes, home-wellness environments), and end-user industry (consumer/direct-to-consumer, corporate/employer wellness programmes, healthcare providers, senior-living/residential wellness). Type segmentation reveals wearables remain dominant due to device proliferation and connectivity, while software analytics and services are increasingly critical for insights. Application segmentation shows fitness tracking continues to lead, while mental-health and home-wellness segments are rising fast. End-user insights highlight that direct-to-consumer remains largest, but corporate/employer wellness programmes are expanding rapidly due to organisational focus on workforce wellbeing.

Within the types of wellness technology, wearable devices currently account for approximately 39% of adoption, owing to the mass-market proliferation of fitness trackers and connected health sensors. The fastest-growing type is software analytics and wellness-platform services, driven by AI-enabled insights, coaching modules and subscription-based models. Other types including home-wellness hardware modules and enterprise wellness-platform services together make up the remaining ~30% of the market and serve niche or bundled wellness-tech ecosystems.

According to a 2024 industry update, a leading wellness-tech vendor deployed its AI-powered wellness-platform in over 2,000 corporations, resulting in a 22% uplift in wearable-device engagement among employees.

In the wellness technology market, fitness & activity tracking constitutes about 34% share as the leading application, because consumer wearables have long targeted step count, heart-rate and activity monitoring. The fastest-growing application is mental-health and mindfulness technology, supported by rising awareness of stress and sleep issues; this segment is being driven by mobile apps with biometric integration and AI-coaching. Other applications such as corporate wellness programmes and home-wellness environments combined contribute the remaining ~32% share. In 2024, more than 38% of enterprises globally reported piloting wellness technology systems for employee-wellbeing platforms.

A 2024 report revealed that wellness-technology monitoring for sleep and mindfulness improved retention of wellness-app users by 18% compared to traditional fitness-trackers alone.

Among end-user segments in the wellness technology market, consumer/direct-to-consumer leads with around 41% share, driven by wearable health-devices and wellness apps purchased by individual users. The fastest-growing end-user is corporate/employer wellness, where organisations integrate wellness-technology platforms into employee-wellbeing strategies and see adoption rates rising from 29% in 2023 to 37% in 2024. Other relevant end-users — including healthcare providers and senior-living/residential wellness — together hold ~28% share, with adoption rates in senior-living programmes jumping from 21% to 27% year-on-year. In the United States, 42% of large corporations now include wellness-technology dashboards in their employee-benefit platforms.

According to a 2025 survey, digital wellness-platform adoption among SMEs in the service-sector increased by 22%, enabling over 500 companies to streamline employee-wellbeing management and analytics.

North America accounted for the largest market share at 38% in 2024 moreoover, North America is also expected to register the fastest growth, expanding at a CAGR of 16% between 2025 and 2032.

In 2024 North America delivered approximately USD 98,000 Million in wellness technology market value, encompassing wearable devices, corporate wellness platforms and digital health subscriptions. Consumer adoption in the United States alone surpassed 50 million active wellness-tech users, with over 45% of enterprises integrating wellness-technology platforms across workforces. The region’s investment in wellness-tech infrastructure exceeded USD 12 billion for wearable-device programmes and remote-wellness systems in 2024. High smartphone penetration (~87%) and enterprise spending on employee-wellbeing technologies (over USD 7.5 billion) underlie dynamics in the wellness technology market across North America.

Which Strategic Wellness-Tech Models Are Reshaping Corporate Well-Being Infrastructure?

North America holds about 41% of global wellness technology market volume in 2024 and remains the largest regional segment in the wellness technology market. Demand is fuelled by industries such as healthcare providers, financial services and large-scale corporate employers who deploy wellness-tech platforms for employee health optimisation. Regulatory incentives such as tax-credits for workplace wellness programmes and government funding for preventive-health tech platforms support growth. Technological advances include AI-powered personal wellness assistants, biometric wearable integrations and cloud-based corporate wellness dashboards. A major US corporation implemented a wearable-based wellness-tech solution across 60,000 employees and delivered a 14% reduction in health-risk scores within nine months. Consumer behaviour in North America shows higher enterprise adoption in healthcare and finance sectors where monitoring wellness metrics is aligned with operational productivity. This advanced ecosystem positions North America as a leading region for wellness technology market evolution.

How Are Compliance-Driven Wellness Platforms Transforming Preventive Health Services?

Europe commands approximately 27% of the wellness technology market share in 2024. Key markets such as Germany, the United Kingdom and France are driving adoption through employer-wellness programmes, preventive-health initiatives and digital wellness app rollout. Regulatory bodies and sustainability initiatives—such as workplace wellbeing mandates and EU-led digital health strategies—are accelerating demand for wellness technology solutions that deliver transparency, data-governance and explainability. Emerging technologies in Europe include AI-driven wellness-analytics platforms with GDPR-compliant workflows and biometric-wearables certified for medical-device standards. A European wellness-tech provider launched a mental-health & mindfulness platform across 8,000 firms in Germany, achieving a 21% increase in employee participation. Consumer behaviour in Europe is oriented toward wellness technology solutions that prioritize regulatory-compliance, explainable analytics and certified health-data security, shaping the regional wellness technology market.

What Mobile-First Wellness Innovation Strategies Are Fueling Emerging Market Growth?

Asia-Pacific is the second-largest region in the wellness technology market in terms of installed volume and is the fastest-rising region in adoption in 2024. Major consuming countries include China, India and Japan, where smartphone penetration exceeds 68% and urban wellness-tech adoption is rising rapidly. Infrastructure trends involve smart-city wellness hubs, mobile wellness apps and IoT-connected wearables integrated into corporate wellness programmes. Regional tech-innovation hubs in Bengaluru, Shenzhen and Tokyo are producing wellness-tech platforms that combine mobile AI assistants and local language user interfaces. A Chinese wellness-tech company deployed a wellness-platform for 120 manufacturing sites, tracking biometric and lifestyle signals, achieving a 16% improvement in employee wellness-engagement scores. Consumer behaviour in Asia-Pacific is driven by e-commerce wellness devices, mobile-first wellness apps and growth in digital health subscriptions, which directly impact growth in the wellness technology market.

How Are Localised Wellness Platforms And Incentives Driving Uptake In Emerging Economies?

In South America, countries like Brazil and Argentina are significant for the wellness technology market, with the region accounting for roughly 6% of global wellness-tech deployments in 2024. Government incentives tied to workforce wellness and trade policies facilitating wellness-device imports are bolstering infrastructure upgrades. Brazilian corporate wellness programmes now adopt connected wellness-tech platforms linking wearables, mobile apps and employee-wellbeing analytics—one large Brazilian firm recorded a 19% increase in wellness-tech platform adoption across 22,000 employees. Infrastructure trends span mining, agriculture and utilities sectors where wellness technology supports health-monitoring in remote sites. Regional consumer behaviour reflects demand for wellness solutions with Portuguese/Spanish language-interfaces, tailored cultural wellness modules and locally-customised content, influencing the wellness technology market landscape in South America.

Which Smart Well-Being Deployments Are Accelerating Wellness Technology Adoption In Institutional Settings?

In the Middle East & Africa region, wellness technology market uptake is linked to large-scale institutional deployments in oil & gas, hospitality, smart-city infrastructure and government wellness programmes. Major growth countries include the United Arab Emirates, Saudi Arabia and South Africa, where wellness-tech system installations in corporate campuses and public-health initiatives are increasing. Technological modernisation includes wellness-monitoring hubs in smart-cities, wearable wellness-platforms for corporate employees and remote wellness dashboards for expatriate workforces. A large GCC-based firm implemented a full wellness-tech solution across 10,000 employees, reducing absenteeism by 12%. Consumer behaviour tends toward preference for wellness technology offerings with on-site data-sovereignty, multilingual interfaces and integration with regional healthcare networks, shaping the wellness technology market in the Middle East & Africa region.

United States – 23% share: Strong end-user demand, high corporate wellness-programme penetration and advanced wellness-technology infrastructure drive dominance in the wellness technology market.

China – 20% share: Rapid consumer wellness-tech adoption, large mobile-device ecosystem and government-supported digital wellness initiatives underpin China’s position in the wellness technology market.

The competitive environment in the wellness technology market is moderately consolidated with the top 5 companies accounting for approximately 42% of global market share, while more than 70 active competitors—including start-ups, platform providers and wearable-device manufacturers—operate globally. Strategic initiatives include over 40 new wellness-tech product launches in 2023/24, 22 joint-ventures between tech-vendors and corporate-wellness service providers, and 12 major acquisitions focused on wellness-analytics platforms and wearable ecosystem integration. Innovation trends influencing competition encompass AI-driven wellness-coaching, sensor-fusion wearables, mobile-first subscription-wellness platforms and enterprise wellness dashboards. Market leaders are differentiating through superior user-engagement rates (with one vendor reporting 33% higher platform retention), embedded analytics, and enterprise-grade security features tailored for wellness-technology deployments. The fragmented nature of the market allows regional players in Asia-Pacific and Latin America to secure niche positions, challenging global incumbents. For decision-makers, vendor selection is increasingly centered on ecosystem compatibility, scalability, data-governance compliance and wellness-technology roadmap alignment.

Philips Healthcare

Samsung Electronics

Johnson & Johnson

Omron Healthcare

Microsoft Corporation

Alphabet Inc. (Google Health)

Medtronic PLC

Samsung Biologics

Teladoc Health

Wellhub (Formerly Gympass)

Siemens Healthineers

Current and emerging technologies in the wellness technology market are redefining how individuals and organisations monitor, manage and optimise wellbeing. Key innovations include sensor-fusion wearables integrating heart-rate, sleep-data, hydration and posture metrics into a single wrist or clip-on device. In 2024, over 58 million wearable wellness-devices were shipped globally, with the majority featuring Bluetooth Low Energy connectivity, onboard AI-inference chips and cloud-sync capability. AI-driven personal wellness-assistants now deliver personalised behavioural nudges, predicting risk of stress-events with up to 24% higher accuracy compared to basic track-and-report wearables. Mobile wellness platforms employ machine-learning models that provide dynamic nutrition guidance, mental-health check-ins and real-time engagement prompts; user-adherence improvements of 18% have been reported. On the enterprise side, wellness-technology systems integrate with HR systems, wearable data APIs and corporate dashboards, enabling real-time metrics such as wellness-programme participation rates, biometric-risk profiling and productivity correlations. Cloud/edge hybrid architectures are emerging, with local on-device inference to reduce latency (< 50 ms) and privacy frameworks to meet regulatory requirements in Europe and North America. Augmented reality (AR) and virtual-reality (VR) wellness modules are being piloted for mindfulness, stress-reduction and rehab-wellness in corporate campuses and senior-living facilities. Decision-makers must evaluate factors such as device accuracy, analytics-platform maturity, interoperability with enterprise systems, data-security certifications and wellness ecosystem scalability when adopting wellness-technology solutions. The trajectory of innovation will continue toward multi-modality wellness platforms, subscription-scholped delivery models and deep integration of wellness-technology into corporate talent-management and health-outcome strategies.

• In April 2024, Wellhub (formerly Gympass) announced its rebranding and expansion of wellness-technology services across 15,000 corporate clients and 2.7 million employees spanning 11 countries, adding nutrition, mindfulness and sleep-tracking modules. Source: www.axios.com

• In October 2024, Microsoft Corporation unveiled enhancements to its Cloud for Healthcare suite, including wellness-analytics tools and AI-based lifestyle-insights modules designed for enterprise wellness platforms. Source: www.microsoft.com

• In November 2023, Philips Healthcare launched a new wearable wellness device combining continuous blood-oxygen monitoring, advanced sleep-analytics and integration with mobile wellness apps, targeting senior-living and corporate wellness markets. Source: www.philips.com

• In June 2023, Fitbit (Google LLC) introduced its Wellness Pro platform for enterprises, enabling real-time biometric dashboards for employee wellness programmes and launching a pilot across 2,500 corporate sites with a 22% increase in wellness-device engagement. Source: www.fitbit.com

This report on the wellness technology market delves into multiple dimensions: product-types (wearable devices, mobile wellness apps, corporate wellness platforms, home-wellness hardware), technology categories (AI-based wellness analytics, sensor-fusion wearables, VR/AR wellness experiences, cloud/edge wellness platforms), application areas (fitness & activity tracking, mental-health & mindfulness, corporate wellness programmes, home-connected wellness), and end-user sectors (consumer/direct-to-consumer, corporate/employer wellness, healthcare providers, senior-living/residential wellness). Geographic coverage spans North America, Europe, Asia-Pacific, South America and Middle East & Africa, offering insights into regional consumption patterns, infrastructure readiness, regulatory frameworks and technology adoption. Emerging sub-segments include hybrid subscription-wellness models (device + platform + coaching), remote wellness-monitoring for senior populations, and wellness-technology ecosystems embedded within smart-home and smart-workplace environments. The report integrates qualitative intelligence on R&D investments, venture-funding flows into wellness-tech start-ups, system-integration service maturity and vendor-ecosystem evolution. Decision-makers will find detailed vendor-profiles, deployment scenario case-studies, cost-benefit analyses, implementation road-maps and scalability frameworks tailored to wellness technology adoption across diverse industrial, residential and enterprise infrastructures.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 258,175.2 Million |

|

Market Revenue in 2032 |

USD 741,651.2 Million |

|

CAGR (2025 - 2032) |

14.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User Industry

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Apple Inc., Fitbit (Google LLC), Garmin Ltd., Philips Healthcare, Samsung Electronics, Johnson & Johnson, Omron Healthcare, Microsoft Corporation, Alphabet Inc. (Google Health), Medtronic PLC, Samsung Biologics, Teladoc Health, Wellhub (Formerly Gympass), Siemens Healthineers |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |