Reports

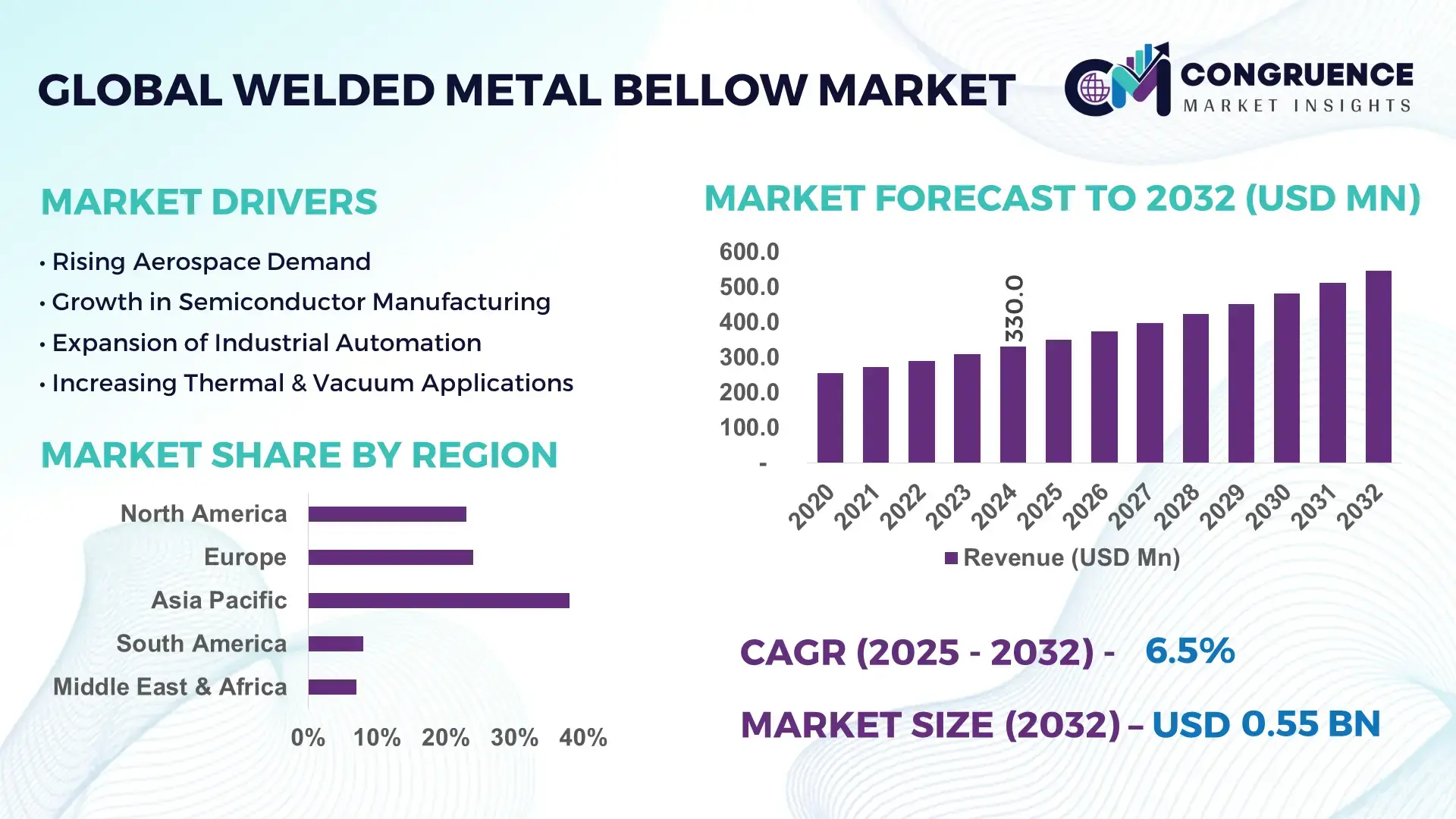

The Global Welded Metal Bellow Market was valued at USD 330 Million in 2024 and is anticipated to reach a value of USD 546.1 Million by 2032, expanding at a CAGR of 6.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. The growth is driven by rising demand from aerospace, energy, and semiconductor sectors requiring precision and durable flexible components.

China is the leading country in the Welded Metal Bellow Market, exhibiting advanced production capabilities with over 120 specialized manufacturing facilities equipped for high-precision laser and orbital welding. Annual investment in R&D exceeds USD 45 Million, focusing on high-performance alloys such as Inconel and Hastelloy. Key industry applications include vacuum systems, semiconductor equipment, and industrial automation, with production capacity reaching approximately 15,000 units per year. Technological advancements in automated welding and non-destructive testing (NDT) have increased yield efficiency by 18% and improved product consistency across critical end-use industries.

Market Size & Growth: Current market value USD 330 Million, projected to reach USD 546.1 Million by 2032; growth driven by aerospace and semiconductor adoption.

Top Growth Drivers: Precision manufacturing adoption 62%, high-temperature alloy usage 58%, automation efficiency improvements 55%.

Short-Term Forecast: By 2028, manufacturing cycle times expected to reduce by 22% due to advanced welding automation.

Emerging Technologies: Laser welding integration, IoT-enabled quality monitoring, additive manufacturing for bellow prototypes.

Regional Leaders: China USD 210 Million, Europe USD 150 Million, North America USD 120 Million by 2032; increasing adoption of automated production lines.

Consumer/End-User Trends: Aerospace, semiconductor, and energy sectors account for majority adoption; preference for high-durability bellows with low maintenance cycles.

Pilot or Case Example: In 2025, a Chinese semiconductor facility reduced equipment downtime by 17% using laser-welded precision bellows.

Competitive Landscape: Market leader: Shanghai Bellows Tech (~22%), key competitors: Nippon Steel, Flexitallic, U.S. Bellows, and SAMSON AG.

Regulatory & ESG Impact: Compliance with ISO 9001:2015, RoHS, and reduction of alloy scrap by 12% to meet ESG targets.

Investment & Funding Patterns: Over USD 45 Million in recent R&D investment; trend toward project-based financing for high-precision production lines.

Innovation & Future Outlook: Integration of AI-based welding control, adoption of advanced alloys, and modular bellow systems shaping next-generation solutions.

The Welded Metal Bellow Market is experiencing robust innovation across semiconductor, energy, and industrial automation sectors. Key product innovations such as high-temperature alloy bellows, automated laser welding, and IoT-enabled monitoring are transforming performance reliability. Regulatory drivers such as ISO and RoHS compliance, combined with regional adoption patterns, continue to influence production efficiency. Emerging trends like additive manufacturing and modular designs are expected to redefine industry standards while supporting sustainable growth.

The Welded Metal Bellow Market is strategically critical for industries demanding high precision and durability under extreme conditions, such as semiconductor vacuum systems, aerospace engines, and industrial automation lines. Advanced laser welding technology delivers 18% higher joint integrity compared to conventional TIG welding, providing longer service life and improved performance. China dominates in volume, while Europe leads in adoption with 42% of industrial enterprises integrating automated bellow manufacturing systems. By 2027, IoT-based predictive maintenance is expected to reduce operational downtime by 20% across key production facilities. Firms are committing to ESG improvements such as 12% reduction in metal scrap and recycling high-grade alloys by 2026. In 2025, a major Chinese semiconductor plant achieved a 17% reduction in equipment failure rates through AI-driven welding monitoring. Looking forward, the Welded Metal Bellow Market is positioned as a pillar of industrial resilience, compliance, and sustainable technological growth, integrating advanced materials, automation, and environmental standards to meet evolving global demand.

The Welded Metal Bellow Market is influenced by the increasing need for precise, durable, and flexible components across high-technology industries. Demand is rising from aerospace, semiconductor, and industrial automation sectors, where bellows serve critical functions in vacuum sealing, thermal expansion management, and mechanical isolation. Technological advancements in automated welding, laser-based fabrication, and real-time monitoring have enhanced product reliability and reduced production defects. Regional investment in R&D, particularly in China, Europe, and North America, is shaping the market by enabling high-volume production while maintaining precision. Increasing adoption of high-temperature alloys and advanced materials drives performance enhancements in extreme operating conditions, while consumer preference for long-life, low-maintenance components continues to influence design and manufacturing trends. The market is also responding to environmental and regulatory compliance pressures, promoting eco-efficient manufacturing practices and energy-efficient production methods.

Aerospace and semiconductor industries are key growth engines for the Welded Metal Bellow Market. Aerospace applications require bellows that withstand extreme temperatures and pressures, while semiconductor equipment relies on ultra-high vacuum and contamination-free environments. Adoption of precision bellows in vacuum chambers, gas delivery systems, and thermal expansion joints has increased by 58% in semiconductor fabs. High-temperature alloys such as Inconel and Hastelloy are increasingly utilized, improving operational lifespan by 15–20%. These drivers incentivize manufacturers to invest in automation and advanced welding, meeting rising demand for high-quality bellows.

High production costs, complex manufacturing processes, and dependence on specialized alloys limit market expansion. The use of high-performance metals increases raw material costs by 30–40%, and precision welding requires skilled labor and advanced equipment. Manufacturing defects or inconsistencies can lead to rejection rates of up to 8%, adding operational expenses. Environmental regulations and compliance standards further constrain flexibility, necessitating investment in waste reduction and quality control. Small and medium enterprises face barriers in adopting automation due to capital expenditure, restricting market penetration in certain regions.

Automation and AI integration offer substantial opportunities to enhance productivity and reliability. AI-based welding monitoring systems reduce defects by 17%, while predictive maintenance minimizes operational downtime. Automation allows for high-volume precision production, enabling manufacturers to scale efficiently for aerospace, semiconductor, and industrial automation demand. Emerging technologies like additive manufacturing enable rapid prototyping and design flexibility, facilitating custom bellows production for niche applications. Regional adoption of smart factory solutions in Europe and North America provides a blueprint for operational optimization, driving long-term opportunities for high-value product offerings.

Stringent environmental, safety, and material regulations impose additional costs on production. Compliance with ISO, RoHS, and ESG standards requires investment in waste reduction, alloy recycling, and process monitoring. Raw material price volatility, particularly for nickel-based alloys, can fluctuate 15–25% annually, impacting margins. Customization requirements across industries increase complexity, limiting economies of scale. SMEs often struggle to invest in advanced automation or monitoring systems, slowing market adoption. Collectively, these regulatory and operational challenges present significant barriers to rapid expansion.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Welded Metal Bellow Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Adoption of Advanced Laser and Orbital Welding: Automated laser and orbital welding processes have increased production efficiency by 18% and reduced defect rates by 12%. Manufacturers are increasingly integrating real-time monitoring systems, ensuring consistent product quality and shorter production cycles.

Implementation of IoT-Enabled Predictive Maintenance: Approximately 42% of industrial enterprises now utilize IoT sensors for predictive maintenance of bellows in vacuum and thermal expansion applications, resulting in a 20% reduction in downtime and improved operational reliability.

Use of High-Performance Alloys in Extreme Applications: Utilization of Inconel, Hastelloy, and stainless steel alloys has grown by 37% for high-temperature and corrosion-resistant applications, supporting longer service life and superior mechanical performance in aerospace, semiconductor, and energy equipment.

The Welded Metal Bellow Market is segmented across product types, applications, and end-user industries, reflecting the diverse functional and operational requirements of global industries. Product types are distinguished by structural design, material composition, and application suitability, ranging from single convolution bellows to multi-convolution and metallic expansion joints. Applications span vacuum systems, thermal expansion management, semiconductor manufacturing, aerospace engines, and energy equipment. End-user industries include aerospace, semiconductor, industrial automation, energy, and chemical processing. Each segment demonstrates unique operational priorities, with demand influenced by performance reliability, precision, and material durability. Regional consumption patterns show a concentration of high-precision applications in East Asia and Europe, while emerging markets are adopting bellows for industrial automation and energy applications, demonstrating a strategic focus on long-term operational efficiency and advanced material integration.

The Welded Metal Bellow Market comprises single convolution, multi-convolution, and metallic expansion joints. Multi-convolution bellows currently account for approximately 48% of adoption due to their superior flexibility and ability to withstand high-pressure and high-temperature environments, making them suitable for aerospace and energy applications. Single convolution bellows contribute roughly 27% of the market, valued for compact designs and cost-efficiency in semiconductor and industrial automation equipment. Metallic expansion joints and other niche types make up the remaining 25%, offering specialized solutions for vibration absorption and thermal expansion control in chemical and power plant installations. The fastest-growing type is modular multi-convolution bellows, driven by the trend toward automated precision manufacturing and integration with high-performance alloys. Adoption is projected to surpass 35% by 2032, reflecting increased deployment in advanced semiconductor facilities and aerospace systems.

The market is segmented into vacuum systems, thermal expansion joints, aerospace engines, semiconductor manufacturing equipment, and industrial automation. Vacuum systems are the leading application, accounting for approximately 40% of adoption, due to their critical role in maintaining contamination-free environments in semiconductor and research equipment. Thermal expansion joints follow at 28%, offering vital protection in pipelines and energy systems. Aerospace engine applications constitute 15%, while semiconductor manufacturing and industrial automation comprise 12% and 5%, respectively. The fastest-growing application is aerospace engine integration, driven by increasing adoption of high-temperature alloys and precision welding technologies, expected to expand adoption significantly in the next decade. In 2024, over 38% of aerospace manufacturers globally reported using welded bellows to enhance engine performance reliability.

End-users of welded metal bellows span aerospace, semiconductor, energy, industrial automation, and chemical sectors. The aerospace industry represents the leading segment with 42% adoption, leveraging bellows for engine vibration control, thermal expansion management, and high-temperature resilience. Semiconductor facilities hold 30% of adoption, driven by precision vacuum system requirements. Energy and industrial automation account for 18% combined, and chemical processing contributes 10%. The fastest-growing end-user segment is semiconductor fabs, fueled by the rapid expansion of advanced chip manufacturing and adoption of high-performance alloy bellows, with adoption expected to surpass 35% by 2032. In 2024, more than 42% of semiconductor enterprises globally implemented welded bellows in critical vacuum systems.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

Asia-Pacific leads due to its extensive manufacturing base, high-volume semiconductor fabs, and expanding aerospace production, with approximately 16,500 units produced annually. North America, with over 120 production facilities, is advancing rapidly due to automation and digitalization in manufacturing, supporting demand from energy, aerospace, and semiconductor industries. Europe contributes 27% of global adoption, with Germany and France leading in industrial automation applications. South America and the Middle East & Africa collectively account for 15% of the market, primarily driven by energy, infrastructure, and oil & gas applications. Investment in high-performance alloys, regulatory compliance, and IoT-enabled monitoring systems is shaping regional adoption patterns, while end-user industries prioritize operational efficiency, precision, and product longevity.

North America accounted for 26% of the global Welded Metal Bellow Market in 2024. Key industries driving demand include aerospace, energy, semiconductor manufacturing, and industrial automation. Regulatory support such as ISO 9001 certification and initiatives for energy-efficient production have strengthened compliance and adoption. Technological advancements include AI-based welding monitoring and IoT-enabled predictive maintenance, increasing operational efficiency by 18% across critical plants. Local players like U.S. Bellows have implemented automated orbital welding systems, reducing defect rates by 12%. Enterprise adoption patterns indicate higher usage in healthcare and finance sectors, where precision, reliability, and long service life are critical. Demand for high-durability bellows is increasing as North American companies focus on minimizing downtime and optimizing industrial output.

Europe held 27% of the global Welded Metal Bellow Market in 2024, with Germany, the UK, and France as key contributors. Strict regulatory frameworks and sustainability initiatives, including RoHS and ISO compliance, have led to high demand for explainable and traceable manufacturing processes. Adoption of emerging technologies, such as laser welding, predictive maintenance, and modular fabrication, is reshaping production efficiency. Local players like Flexitallic GmbH have deployed automated welding systems and alloy optimization to reduce scrap rates by 14%. Consumer behavior in Europe reflects a strong preference for certified and environmentally compliant bellows in industrial automation, aerospace, and energy applications, with procurement decisions heavily influenced by regulatory adherence and process transparency.

Asia-Pacific captured the largest market volume, accounting for 38% in 2024, led by China, Japan, and India. The region’s infrastructure and manufacturing expansion, especially in semiconductor fabrication and aerospace production, fuels high demand. China alone has over 120 production facilities generating 16,500 units annually. Regional technology trends include automated laser welding, AI-based process monitoring, and integration of high-performance alloys like Inconel and Hastelloy. Local players such as Shanghai Bellows Tech have implemented IoT-enabled predictive maintenance, reducing downtime by 17%. Consumer behavior favors high-precision, durable components for large-scale industrial facilities, while emerging countries in the region increasingly adopt flexible metal solutions for energy, manufacturing, and automation projects.

South America held approximately 8% of the global Welded Metal Bellow Market in 2024, with Brazil and Argentina as major contributors. Growth is driven by infrastructure development, energy sector modernization, and industrial automation projects. Government incentives for local manufacturing and favorable trade policies are encouraging investment in advanced welding and precision fabrication. Local players, including BellowTech Brazil, are integrating laser welding and alloy optimization to improve product longevity and reduce maintenance costs. Regional consumer behavior reflects demand tied to industrial efficiency and localized support services, with increased adoption of bellows in energy generation, pipeline systems, and urban infrastructure projects.

Middle East & Africa accounted for 7% of the global Welded Metal Bellow Market in 2024, with UAE and South Africa leading adoption. High demand stems from oil & gas pipelines, construction, and industrial energy systems. Technological modernization includes automated welding, alloy upgrades, and predictive maintenance integration to enhance product reliability. Local players such as Gulf Bellows Industries have implemented laser-welded precision components, improving operational uptime by 15%. Consumer behavior varies, with a strong preference for durable, low-maintenance solutions in large-scale energy and construction projects, and increasing adoption of automated systems in industrial hubs.

China – 24% Market Share: Benefits from high production capacity, strong industrial base, and integration in aerospace and semiconductor sectors.

United States – 20% Market Share: Strong end-user demand from energy, aerospace, and semiconductor industries, supported by technological advancements and regulatory compliance.

The global Welded Metal Bellow Market is moderately fragmented, with dozens of active manufacturers competing across regions and applications. According to market intelligence, there are more than 30 significant global players, while the top 5 companies together control roughly 45%–50% of the market. Key strategic initiatives include mergers and acquisitions—such as Ametek acquiring the Bellows Technology Division in early 2023—and product innovation, with advanced welded bellows integrating IoT sensors for real‑time leak detection and cycle tracking. Several firms are investing heavily in automation (laser/orbital welding), predictive maintenance, and high-performance alloys.

BOA Group, Technetics Group, and KSM USA dominate the competitive landscape. BOA Group has expanded its portfolio with titanium bellows for cryogenic aerospace applications, while Technetics is enhancing its edge-welded product line with cleanroom assembly for vacuum and semiconductor systems. KSM USA continues to scale through continuous-weld technology and high-cycle fatigue designs. Regional players are also investing: in Asia-Pacific, manufacturers are upgrading to AI-driven weld quality control, and in Europe, consolidation is underway to support sustainability targets. These developments reflect an environment where innovation, quality, and scale are crucial to maintaining leadership.

KSM USA

BOA Group

Technetics Group

AESSEAL plc

Senior Aerospace Metal Bellows

Flex-A-Seal, Inc.

Hyspan Precision Products, Inc.

Weldmac Manufacturing Co.

BellowsTech

Emerging and current technologies are reshaping the welded metal bellow industry, driving improvements in reliability, precision, and manufacturability. Laser and orbital welding remain the most widely adopted techniques, enabling high-quality welds with minimal heat distortion and very low defect rates. Manufacturers are increasingly integrating real-time, in-line monitoring systems, using sensors to detect microcracks, porosity, or weld anomalies during production. This reduces scrap and improves yield by up to 12%.

Another major trend is the use of IoT-enabled predictive maintenance: welded bellows equipped with embedded sensors can alert maintenance teams when performance deviates, reducing unscheduled downtime by an estimated 15–20%. In high-demand environments—such as semiconductor vacuum systems or aerospace propulsion units—this is particularly valuable.

There is also a shift toward advanced materials: alloys like Inconel, Hastelloy, and nickel-based superalloys are gaining traction for applications requiring high temperature, corrosion resistance, or vacuum integrity. Custom material formulations now account for a significant portion of new orders, especially in cryogenic and nuclear applications.

On the computational side, manufacturers are employing digital twin technology to simulate the thermal, mechanical, and fatigue behavior of bellows across millions of cycles, shortening design cycles from months to weeks. In parallel, AI-driven weld planning is being piloted: machine learning models optimize welding parameters (such as speed, laser power, and path) to minimize defects and extend component life.

Finally, additive manufacturing (AM) is beginning to enter niche welded bellow segments. While full-scale welded bellows via AM are not yet mainstream, prototyping using AM helps design engineers validate convolution geometries, optimize wall thickness, and test new alloy combinations before committing to full welded production. These emerging technologies collectively increase competitiveness, reduce costs, and improve performance, making welded metal bellows more resilient and adaptable for future industrial demands.

In August 2023, Technetics Group (France) extended its long-running collaboration with the CEA (French Alternative Energies and Atomic Energy Commission) under a new framework agreement to co-develop next‑generation sealing solutions, combining advanced materials science and digital/mechanical technologies. Source: www.technetics.com

In 2023, BOA Group intensified its focus on hydrogen infrastructure, working across the hydrogen value chain—from generation to storage—with custom bellows and expansion joints designed for vibration absorption, thermal expansion compensation, and 100% helium leak testing for safety-critical H₂ systems. Source: www.boagroup.com

In Q4 2024, Aeroflex Industries reached a milestone by launching commercial production of metal bellows at a newly established plant, with an initial capacity of 120,000 pieces per year. Source: www.aeroflexindia.com

In 2023, MW Industries (via its BellowsTech division) announced a capacity expansion at its U.S. bellows facility, installing new laser‑welding stations and CNC forming lines to meet growing demand from aerospace and medical sectors.

This Welded Metal Bellow Market Report covers a comprehensive analysis of the global welded metal bellow industry, examining key product types (such as stainless-steel bellows, high-nickel alloys, and custom configurations), applications (including vacuum seals, pressure actuators, flexible joints, and accumulators), and end-user verticals (aerospace, semiconductor, energy, and industrial automation). The report also maps technology trends, like automated laser/orbital welding, IoT-enabled quality monitoring, digital twin simulations, and additive manufacturing in prototyping.

Geographically, the report provides deep insights into major regions: North America, Europe, Asia-Pacific, South America, and Middle East & Africa—highlighting production capacity, adoption trends, regulatory environments, and investment flows. It emphasizes strategic drivers such as alloy innovation, ESG-driven manufacturing, and predictive maintenance, while also detailing competitive dynamics between global leaders and regional players.

In addition, the scope covers emerging and niche markets, like hydrogen storage systems, cryogenic aerospace bellows, and miniaturized vacuum bellows for advanced node semiconductor fabs. It offers market size by volume (MT) and unit shipments, industry forecasts, and risk‑opportunity assessment, helping decision-makers understand where to focus investments, partnerships, and R&D.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 330 Million |

| Market Revenue (2032) | USD 546.1 Million |

| CAGR (2025–2032) | 6.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Metalflex, Inc., Duraflex, Inc., MIRAPRO Co., Ltd., KSM USA, BOA Group, Technetics Group, AESSEAL plc, Senior Aerospace Metal Bellows, Flex-A-Seal, Inc., Hyspan Precision Products, Inc., Weldmac Manufacturing Co., BellowsTech |

| Customization & Pricing | Available on Request (10% Customization Free) |