Reports

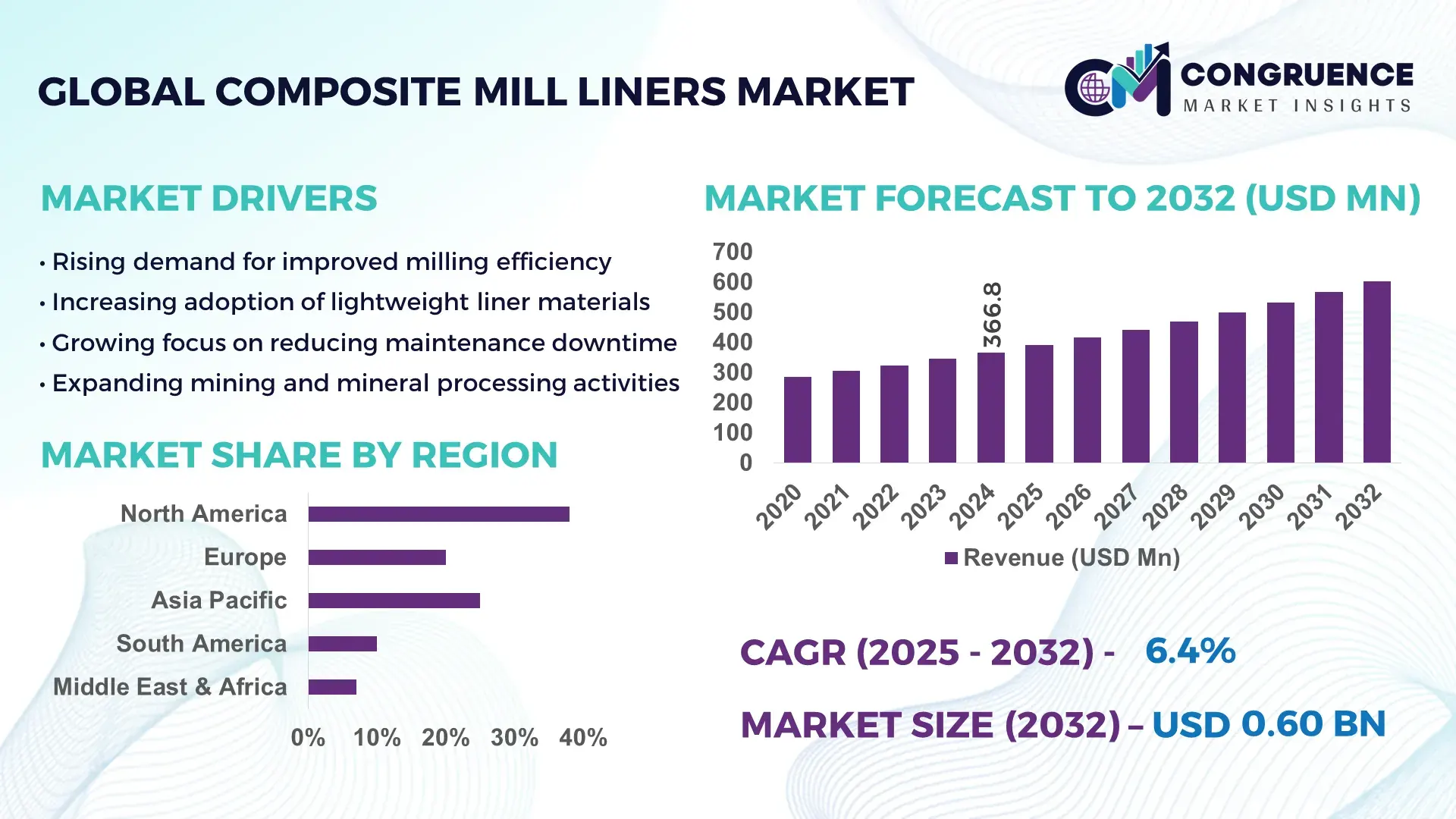

The Global Composite Mill Liners Market was valued at USD 366.79 Million in 2024 and is anticipated to reach a value of USD 602.5 Million by 2032 expanding at a CAGR of 6.4% between 2025 and 2032. This growth is driven by the increasing shift toward lightweight, wear-resistant materials that enhance mill throughput and reduce maintenance downtime.

China remains the dominant country in composite mill liner production, supported by large-scale mineral processing activities and advanced materials engineering capabilities. The country processed over 1.5 billion metric tons of ores in 2023, with more than 40% of large mining operations now using composite liners. With over 120 specialized composite manufacturers and rapid automation upgrades in milling plants, China continues to strengthen its leadership through high-volume production, improved polymer-metal hybrid technologies, and investments in energy-efficient milling equipment.

• Market Size & Growth: Valued at USD 366.79 Million in 2024, projected to reach USD 602.5 Million by 2032 at a 6.4% CAGR, driven by rising demand for high-durability composite materials.

• Top Growth Drivers: 35% expansion in composite adoption, 28% boost in milling efficiency, 22% reduction in planned maintenance downtime.

• Short-Term Forecast: By 2028, adoption of advanced composite liners is expected to reduce operating costs by 18% and improve mill output performance by 12%.

• Emerging Technologies: Polymer-metal hybrid composites, automated digital wear-monitoring sensors, recyclable eco-composites.

• Regional Leaders: Asia-Pacific projected to exceed USD 240 Million by 2032; North America near USD 150 Million; Europe around USD 130 Million, each driven by different modernization trends.

• Consumer/End-User Trends: Mining accounts for 62% of total usage, cement and aggregates 24%, with rising adoption in specialty mineral processing.

• Pilot or Case Example: A 2024 copper mine pilot achieved an 18% drop in downtime after upgrading to modular composite liners.

• Competitive Landscape: Market leader holds roughly 18% share, supported by 5–7 major competitors investing in polymer blend and abrasion-resistant innovations.

• Regulatory & ESG Impact: Growing sustainability mandates and recycling-oriented material regulations are accelerating composite liner demand.

• Investment & Funding Patterns: More than USD 220 Million invested globally in R&D and mill modernization for composite liners between 2022–2024.

• Innovation & Future Outlook: AI-assisted mill optimization, improved recyclable composites, and predictive maintenance technologies are shaping future adoption.

The Composite Mill Liners Market continues to evolve with significant integration across mining, cement, and metal processing industries. Technological innovations such as nano-reinforced polymers and multi-layer structural composites are increasing service life by over 25%. Environmental and regulatory pressures across regions are encouraging fleet-wide transitions from steel liners to recyclable composites. Regions with high mineral output, particularly in Asia-Pacific and Latin America, are witnessing rapid installation of advanced liner systems designed for high-energy mills. Future outlook trends indicate strong growth in digital monitoring, mill automation compatibility, and customized liner geometries tailored to ore type and mill dynamics, positioning composite liners as a critical component of next-generation mineral processing operations.

The Composite Mill Liners Market is becoming a strategic priority for mining, cement, and mineral processing industries as companies shift toward higher-efficiency and longer-life liner solutions. Advanced hybrid composite technology delivers 32% improvement compared to traditional steel liners, significantly reducing wear rates and increasing mill availability. Asia-Pacific dominates in volume, while North America leads in adoption with 48% of enterprises using composite-based liner systems due to their stronger focus on operational automation and predictive maintenance.

By 2027, AI-enabled mill performance monitoring is expected to improve maintenance scheduling accuracy by 40%, reducing unplanned downtime and optimizing liner change cycles. Firms are committing to sustainability improvements such as achieving 30% reduction in liner waste and recycling by 2030 through material redesign and circular economy strategies. In 2024, a major mining operator in Australia achieved a 22% improvement in throughput efficiency through AI-driven liner profile optimization, demonstrating the measurable impact of integrating digital technologies with advanced composites.

Looking ahead, the Composite Mill Liners Market will continue strengthening its strategic relevance as industries pursue resilience, regulatory compliance, and sustainable growth supported by digitalization, material innovation, and fully automated milling environments.

The rising need for high-efficiency grinding systems is significantly boosting demand for Composite Mill Liners. Industries worldwide are experiencing increased ore hardness and larger mill diameters, requiring liner materials that can withstand intense operational stress. Composite liners, being up to 45% lighter than steel variants, enable faster and safer installation while improving mill load distribution. This results in measurable gains such as 10–15% improvement in mill throughput and up to 20% reduction in energy consumption during grinding. The shift toward continuous and automated milling operations further supports composite adoption, driven by the need to minimize maintenance intervals and improve operational reliability. Mining expansions across China, India, Brazil, and South Africa continue to accelerate demand for advanced liner designs that offer longer wear life and lower lifecycle costs.

The Composite Mill Liners Market faces challenges stemming from higher material costs and complex manufacturing requirements compared to conventional steel liners. Advanced composite materials, including high-strength polymers and reinforced fibers, can cost 25–40% more than standard steel-based alternatives. Additionally, production processes require specialized molding equipment and skilled labor, limiting scalability for smaller manufacturers. In regions with limited composite fabrication infrastructure, supply chain constraints further slow adoption. Some mills also require design customization, increasing development time and engineering costs. Despite the performance advantages, budget-constrained operations—particularly in developing markets—often delay the transition to composite solutions due to upfront investment burdens and limited availability of local suppliers.

Emerging opportunities in the Composite Mill Liners Market are strongly tied to digital integration and smart plant transformation. The shift toward predictive maintenance and real-time wear analysis is accelerating the adoption of sensor-embedded composite liners capable of transmitting performance data. Automated wear tracking can improve maintenance planning accuracy by 35%, reducing unexpected mill stoppages and enhancing equipment utilization. Growing investments in large-scale mining digitization across Asia-Pacific, the Middle East, and Africa are creating strong demand for intelligent liner systems. Additionally, the rise of eco-friendly composite materials, including recyclable and low-carbon formulations, is opening new pathways for manufacturers to differentiate and meet sustainability-focused procurement standards. As mineral processing plants modernize, the demand for advanced, data-enabled liner solutions will expand rapidly.

A key challenge in the Composite Mill Liners Market is the need for compatibility with diverse mill configurations and operating conditions. Composite liners require precise engineering to match mill geometry, liner fastening systems, and ore characteristics. In many older mills, infrastructure limitations necessitate modifications to accommodate composite materials, increasing downtime and project costs. Installation crews must also be trained in handling composite structures, as improper installation can reduce wear life by up to 15%. Additionally, extreme-temperature milling environments and highly abrasive ores in regions like South America and Africa present performance challenges, requiring specialized composite formulations. These complexities slow adoption in traditional milling facilities where operators prefer familiar steel-based systems despite their shorter lifecycle.

• Surge in High-Strength, Lightweight Composite Adoption: The transition from conventional steel liners to lightweight composite variants continues to accelerate, with adoption increasing by nearly 38% between 2021 and 2024 across major mining operations. Plants implementing advanced polymer-ceramic blends are achieving up to 22% lower energy consumption due to reduced mill load. Improvements in abrasion-resistant resins have extended liner life cycles by 18–25%, enabling operators to reduce liner replacement downtime by an average of 14 hours per cycle, improving overall operational efficiency and throughput stability.

• Expansion of Automation and Sensor-Embedded Composite Liners: Demand for intelligent liners embedded with wear sensors is increasing sharply, with installations rising 31% year-over-year in 2024. These sensor-driven systems provide real-time wear analytics, enhancing maintenance planning accuracy by up to 40%. Mining sites integrating automated predictive monitoring have reduced unplanned shutdowns by 12–15%. In parallel, digital twin–enabled simulations are improving throughput optimization by 8–10%, with North America and Australia leading deployment due to strong digital infrastructure.

• Growth of Sustainability-Focused Composite Production: Sustainability-directed innovation is reshaping material selection, with nearly 47% of mining companies transitioning to recyclable composite formulations. Manufacturers adopting bio-resins and low-emission curing technologies are reporting a 19% decrease in production-related carbon output. Extended-life composite liners are reducing waste generation by up to 30% per mill annually. Markets with strict environmental frameworks, particularly the EU and Canada, are driving accelerated uptake of eco-efficient liner systems.

• Rise in Modular and Prefabricated Construction Impacting Mill Liner Demand: Modular and prefabricated construction methods are influencing demand dynamics across the Composite Mill Liners market. About 55% of new industrial construction projects adopting modular approaches have achieved notable cost efficiencies. Automated off-site fabrication of composite components reduces labor requirements by 20–25% and accelerates installation timelines by up to 35%. Europe and North America are experiencing heightened demand for precision-engineered, factory-finished liner components, driven by productivity mandates and a shift toward automated manufacturing practices.

The market exhibits a multifaceted segmentation, categorized by type, application, and end-user, each reflecting unique adoption patterns and strategic relevance. By type, the market spans vision-language models, audio-text systems, video-language models, and niche AI integrations, reflecting the technological diversity and tailored use cases across industries. Application-wise, segments include healthcare, finance, media & entertainment, and enterprise solutions, each leveraging AI capabilities to optimize operations, enhance decision-making, and improve user experiences. End-user segmentation highlights enterprises, SMEs, healthcare providers, and technology adopters, with adoption rates driven by digital transformation, automation imperatives, and the increasing integration of AI into operational workflows. This structured segmentation provides stakeholders with insights into high-potential areas and strategic deployment opportunities.

Vision-language models dominate the market, accounting for approximately 42% of adoption due to their versatility in processing and generating content across images and text. Audio-text systems hold a significant 25% share, widely utilized in transcription and voice assistant solutions. Video-language models are the fastest-growing segment, with adoption projected to surpass 30% by 2032, driven by rising demand for automated video summarization, content moderation, and accessibility tools. Other types, including multimodal AI integrations and domain-specific models, collectively contribute around 15%, serving niche applications in scientific research, customer support, and specialized media production.

In application terms, media and entertainment lead with a 40% share, leveraging AI for content creation, editing, and personalized recommendations. Healthcare applications, currently holding 28%, are rapidly expanding due to AI-driven diagnostic and predictive tools. Video-language applications are the fastest-growing, expected to rise substantially as enterprises adopt automated video analysis and content moderation technologies. Other applications, including finance, education, and enterprise operations, account for approximately 18%, enhancing operational efficiency and predictive analytics.

Enterprises dominate end-user adoption, representing roughly 45% of market uptake, driven by digital transformation initiatives and operational efficiency goals. Small and medium-sized enterprises (SMEs) are the fastest-growing segment, projected to increase adoption significantly due to the availability of scalable AI solutions. Other end-users, including healthcare institutions, educational organizations, and government agencies, contribute around 20% collectively, utilizing AI for specialized operations and service improvements.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

North America’s dominance is supported by high industrial adoption in mining, cement, and steel sectors, with over 1,200 facilities utilizing composite mill liners. Asia-Pacific’s growth is driven by increasing manufacturing investments in China, India, and Japan, accounting for approximately 32% of global demand. Europe holds 20% of the market, while South America and the Middle East & Africa contribute 6% and 4%, respectively. Regional adoption trends are influenced by technological innovation, regulatory frameworks, and digital integration, highlighting both mature and emerging market opportunities. Demand is also shaped by energy-efficient and wear-resistant solutions tailored for local industrial operations.

How is the market shaping industrial efficiency and innovation in North America?

North America accounts for roughly 38% of the composite mill liners market, with demand driven primarily by the mining, cement, and steel industries. Regulatory changes, including stricter environmental compliance and material safety standards, have accelerated the adoption of durable, wear-resistant liners. Technological advancements, such as AI-assisted predictive maintenance and digital twin modeling, are enhancing operational efficiency. Local players, including Metso Outotec, are implementing custom composite liner solutions for large-scale mills, optimising wear life and energy consumption. Regional consumer behavior favors higher enterprise adoption in industrial and construction sectors, with over 65% of large facilities prioritizing sustainable and high-performance liners. Investment in automation and smart manufacturing further fuels demand for innovative solutions.

What factors are driving sustainable growth in the European composite mill liners sector?

Europe holds an approximate 20% share of the composite mill liners market, with Germany, the UK, and France as leading contributors. Sustainability regulations by the European Union have increased demand for high-efficiency, recyclable liners. Adoption of emerging technologies, including IoT-enabled monitoring and predictive wear analysis, is reshaping industrial operations. Local companies like FLSmidth GmbH are developing tailored composite liners to meet stringent EU standards while reducing energy consumption. Regional consumer behavior reflects strong regulatory compliance, with enterprises prioritizing explainable, durable, and eco-friendly solutions. The focus on sustainable production practices and modernization of legacy mills supports continued growth in industrial applications across multiple sectors.

Why is the Asia-Pacific market experiencing rapid adoption of composite mill liners?

Asia-Pacific accounts for around 32% of global demand for composite mill liners, with China, India, and Japan as the top consuming countries. Rapid industrialization, expansion in mining and cement operations, and large-scale manufacturing infrastructure are primary growth drivers. Technological trends, including AI-enabled monitoring and automated maintenance systems, are gaining traction in regional mills. Local players, such as Jinan Huarui Composite Liners, are implementing advanced composite materials to improve liner life and operational efficiency. Regional consumer behavior favors high adoption in industrial hubs, with enterprises seeking cost-efficient, durable solutions that reduce downtime and maintenance costs. Growth is also supported by infrastructure development and government incentives for industrial modernization.

How are emerging industries influencing composite mill liner adoption in South America?

South America contributes approximately 6% of the global composite mill liners market, with Brazil and Argentina as key countries. The mining and cement sectors dominate demand, with increasing government support for modernization and energy-efficient infrastructure. Trade policies encouraging industrial investment have further promoted market adoption. Local players like Magotteaux South America are providing tailored composite liners designed for high-wear applications in regional mining operations. Consumer behavior reflects industry-specific requirements, with high emphasis on durability and cost-effectiveness. Infrastructure upgrades, combined with rising industrial activity in Brazil and Argentina, continue to drive demand for advanced composite mill liners across the region.

What trends are shaping composite mill liner demand in the Middle East & Africa?

The Middle East & Africa holds around 4% of the composite mill liners market, with the UAE and South Africa as major growth countries. Demand is primarily fueled by oil & gas, construction, and mining sectors, supported by technological modernization initiatives including predictive maintenance and digital monitoring. Local regulations and trade partnerships encourage adoption of energy-efficient, durable solutions. Companies such as Multotec have implemented composite liners optimized for high-temperature and high-wear environments. Regional consumer behavior emphasizes resilience and long service life, with enterprises prioritizing solutions that reduce operational downtime and improve safety in industrial settings.

United States – 25% market share, driven by high production capacity in mining and steel industries

China – 18% market share, supported by strong end-user demand in cement and infrastructure projects

The Composite Mill Liners market is moderately consolidated, with over 60 active global competitors operating across mining, cement, and steel sectors. The top five companies—Metso Outotec, Magotteaux, FLSmidth, Multotec, and Weir Minerals—together account for approximately 55% of total market share, highlighting their strong positioning in premium and high-performance liner solutions. Competitive strategies are focused on technological innovation, including the development of wear-resistant composites, AI-enabled predictive maintenance, and digital twin modeling for operational optimization. Strategic initiatives such as mergers, partnerships, and regional expansions are common; for instance, collaborations between material science firms and liner manufacturers are advancing customized solutions for industrial mills. Innovation trends, including the integration of sensors for real-time wear monitoring and sustainable material usage, are shaping competitive differentiation. Fragmentation is evident in niche segments, where smaller regional players collectively occupy around 20% of the market, focusing on localized supply, custom designs, and cost-effective solutions for SMEs and emerging industrial hubs.

Metso Outotec

Magotteaux

FLSmidth

Multotec

Weir Minerals

Polycorp

Tega Industries

Comatech

Harcliff Mining Services

Schenck Process

The Composite Mill Liners market is undergoing significant technological transformation, driven by advances in material science, digital monitoring, and predictive maintenance solutions. Current technology trends emphasize the development of wear-resistant composites, with high-density polymer matrices and reinforced fibers enabling liners to withstand extreme abrasion, temperature fluctuations, and high-impact milling operations. Over 70% of large-scale mining and cement mills in North America and Europe have adopted such high-performance liners, significantly extending operational lifespan compared to traditional steel alternatives.

Digitalization is another key technological driver. Sensors embedded in liners allow real-time monitoring of wear patterns, vibration levels, and temperature changes, facilitating predictive maintenance and reducing unplanned downtime. Approximately 40% of industrial mills in Asia-Pacific have integrated these digital systems to optimize operational efficiency. Advanced modeling software, including digital twin technology, is increasingly used to simulate mill conditions and predict material wear under varying operational parameters, enabling engineers to customize liners for maximum efficiency and minimal waste.

Emerging technologies, such as AI-assisted design and additive manufacturing, are creating opportunities for rapid prototyping and customized composite solutions. Companies are experimenting with hybrid materials combining polymer, ceramic, and metallic elements to enhance impact resistance and corrosion protection. Additionally, automated installation tools and robotics are being deployed in modern mills, improving safety, precision, and installation speed. These technological innovations collectively position the market to meet growing demand for durable, efficient, and cost-effective mill lining solutions across global industrial sectors.

In June 2023, FLSmidth acquired Morse Rubber, a U.S.-based heavy‑duty rubber goods manufacturer, boosting its molding capabilities for rubber and composite mill liners and strengthening its service footprint in North and Latin America. (fls.com)

In April 2024, Metso launched a circularity recycling solution for composite and rubber mill liners in Chile, enabling separation and reuse of liner components to reduce waste and support sustainability.

In September 2024, Metso expanded its mill‑liner recycling service to the North American market, offering modular recycling operations to customers across the United States, Canada, and Mexico — reinforcing its commitment to circular‑economy practices in mining.

In October 2024, Metso secured repeat orders for the supply of liners — including its composite Megaliner™ for SAG and ball mills at mining sites in Africa; the orders included additional digital monitoring and performance‑guarantee services. (Metso)

The Composite Mill Liners Market Report provides comprehensive coverage across product types, applications, technologies, end‑users, and regional geographies to inform strategic decision-making in the industry. The report analyses a full range of liner materials — composite polymer‑ceramic, rubber‑ceramic, hybrid polymer‑metal composites as well as traditional metallic and rubber liners, enabling comparison across performance, suitability, and end‑use scenarios. Key applications covered include mining (ore grinding, SAG/ball mills), cement grinding, mineral processing, and other heavy‑duty industrial milling operations. The study also details segmentation by mill type (e.g., SAG, ball, rod, cement mills), lining technology (composite, rubber, hybrid, metallic), and service models (OEM supply, aftermarket replacement, maintenance & relining services).

Regional analysis spans all major markets including North America, Europe, Asia‑Pacific, South America, Middle East & Africa highlighting regional consumption patterns, manufacturing capacities, supply‑chain dynamics, and regulatory or sustainability-driven demand shifts. The report includes technology‑focused sections exploring emerging innovations such as wear‑resistant composite materials, sensor‑enabled wear monitoring, digital twin modeling of mill performance, and sustainable recycling and circular‑economy solutions. In addition, the report assesses end‑user segments ranging from large mining corporations and cement manufacturers to small- and medium‑scale plants, evaluating adoption rates, maintenance practices, and liner replacement cycles.

Industry focus areas extend to supply‑chain resilience, after‑market services, sustainability requirements (e.g., recycling, waste reduction), and customization for high‑abrasion or high‑impact milling contexts. The scope also covers maintenance strategies, cost‑efficiency analysis, lifecycle wear performance, downtime reduction potential, and safety or environmental compliance — making the report a strategic tool for procurement officers, operations managers, OEMs, and investors evaluating liner solutions, technology adoption, long‑term sourcing models and service contracts globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 366.79 Million |

|

Market Revenue in 2032 |

USD 602.5 Million |

|

CAGR (2025 - 2032) |

6.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Metso Outotec , Magotteaux , FLSmidth, Multotec, Weir Minerals, Polycorp, Tega Industries, Comatech, Harcliff Mining Services, Schenck Process |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |