Reports

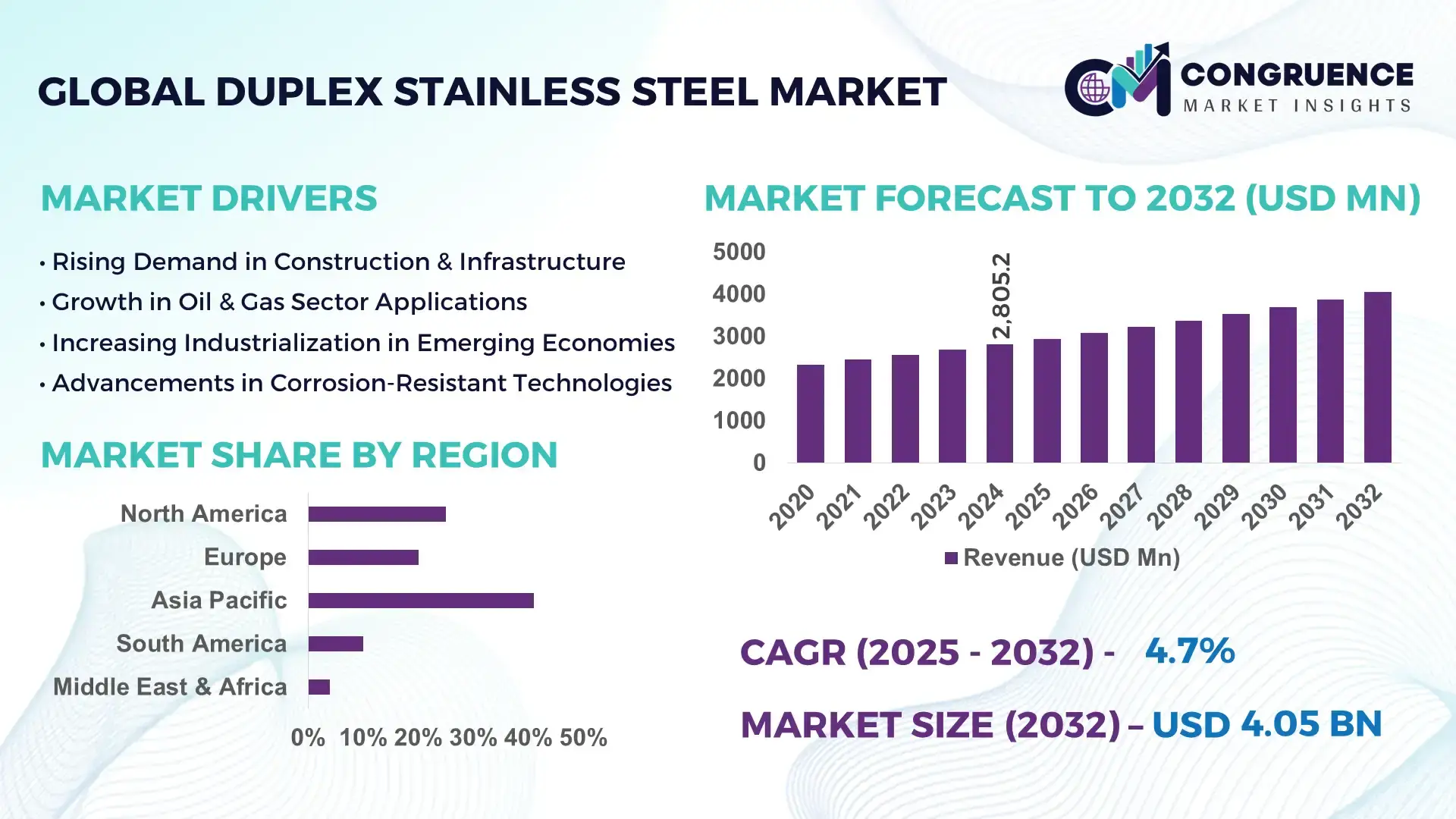

The Global Duplex Stainless Steel Market was valued at USD 2805.19 Million in 2024 and is anticipated to reach a value of USD 4050.76 Million by 2032 expanding at a CAGR of 4.7% between 2025 and 2032. This growth is driven by accelerating demand in critical sectors such as oil & gas, chemical processing, and infrastructure, where corrosion resistance and durability are indispensable for long-term performance.

In the leading country, China, production capacity for high-grade duplex stainless steel has surged, with domestic steelmakers expanding melt-shop throughput and investing in advanced refining technologies. Chinese manufacturers are increasingly supplying duplex and super duplex grades for offshore platforms, petrochemical complexes, and large-scale infrastructure projects, underpinned by investments exceeding several hundred million USD in upgrading production lines and adopting modern finishing processes.

Market Size & Growth: USD 2,805.19 M in 2024 growing to USD 4,050.76 M by 2032 at a CAGR of 4.7%, driven by expanding global infrastructure and industrial projects.

Top Growth Drivers: 35% adoption increase in oil & gas pipelines; 28% rise in chemical processing facility build-outs; 22% growth in infrastructure and construction demand.

Short-Term Forecast (by 2028): Estimated 15% reduction in lifecycle maintenance costs; 12% performance efficiency gain in corrosion-resistant applications.

Emerging Technologies: Advanced rolling and finishing processes to enhance corrosion resistance; development of lean-duplex and super-duplex grades for cost-effective high-performance; improved welding and fabrication technologies for offshore and chemical plant applications.

Regional Leaders: Asia-Pacific projected to reach USD 1,720 M by 2032 with strong infrastructure growth; North America expected USD 1,050 M led by energy and petrochemical upgrades; Europe projected USD 890 M driven by regulatory-driven sustainable industrial practices.

Consumer/End-User Trends: Major end-users include oil & gas, chemical processing, desalination, marine infrastructure, and construction sectors. There is rising uptake of duplex steel in renewable-energy infrastructure and offshore wind farms.

Pilot or Case Example: In 2024 a major offshore oilfield project adopted super-duplex stainless steel pipelines, resulting in a 20% reduction in maintenance downtime and a 17% increase in operational lifetime compared to conventional stainless steel.

Competitive Landscape: Market leader holds approximately 30-35% share, followed by 3–5 major global competitors focusing on advanced manufacturing, quality, and global outreach.

Regulatory & ESG Impact: Stricter environmental and emissions regulations worldwide are encouraging the adoption of long-lasting, recyclable alloy materials; incentives for sustainable infrastructure and reduction of CO₂ emissions over asset lifetimes favor duplex stainless steel usage.

Investment & Funding Patterns: Recent investments exceeding USD 250 M in capacity expansion and technological upgrades; increasing project financing and strategic alliances for large-scale infrastructure and energy projects.

Innovation & Future Outlook: Trend toward development of new duplex grades optimized for renewable energy and wastewater treatment; integration with sustainable construction; forward-looking projects envisage duplex stainless steel for high-performance, longevity-driven industrial and marine applications.

Global duplex stainless steel demand is substantially driven by key industry sectors such as oil & gas, chemical processing, desalination, marine, and large-scale construction, where superior corrosion resistance, high strength, and long-term durability are critical. Recent innovations include the rise of lean-duplex and super-duplex variants offering optimized strength-to-cost ratios, enhanced welding and surface-treatment processes, and improved fabrication techniques suited for harsh offshore and chemical environments. Regulatory pressures and growing ESG commitments in Europe, North America, and Asia are pushing industries toward materials that deliver longevity and lower lifecycle environmental impact, boosting duplex stainless steel adoption. Regional consumption patterns reveal particularly strong growth in Asia-Pacific — driven by infrastructure development, petrochemical expansion and urbanization — while North America and Europe focus on upgrading aging assets with high-performance materials. Emerging trends point toward expanding use in renewable energy infrastructure, desalination, and water-treatment plants, as well as more widespread application in automotive equipment manufacturing and advanced industrial machinery, underscoring a robust and evolving future demand for duplex stainless steel.

The strategic relevance of the Duplex Stainless Steel Market is anchored in its ability to deliver high strength, corrosion resistance, and lifecycle efficiency across demanding industrial ecosystems. Advanced duplex metallurgy has become integral to petrochemical, desalination, offshore, and high-integrity construction projects due to its optimized mechanical properties and reduced maintenance requirements. New thermomechanical processing technology delivers 18% improvement in stress-corrosion cracking resistance compared to older austenitic standards, strengthening its role in mission-critical applications. In terms of regional differentiation, Asia-Pacific dominates in volume, while Europe leads in adoption with nearly 42% of enterprises using duplex grades for ESG-aligned asset modernization. By 2027, AI-enabled process optimization in steel finishing is expected to improve weld-integrity accuracy by 20%, lowering defect rates and enabling better quality assurance in harsh-environment components. Firms are committing to ESG-metric improvements such as 30% recycling of alloy scrap and process-emission reduction by 2030, advancing sustainable material cycles. In 2024, a leading Scandinavian steelmaker achieved a 14% reduction in energy consumption through automated, AI-driven furnace control systems, showcasing measurable operational gains. As industries increasingly prioritize durability, compliance, and low-emission material strategies, the Duplex Stainless Steel Market is positioned as a pillar of resilience, regulatory alignment, and long-term sustainable growth.

Growing capital expenditure in offshore platforms, subsea equipment, and petrochemical processing facilities is significantly boosting demand for duplex stainless steel due to its superior strength-to-weight ratio and high chloride stress-corrosion resistance. As offshore drilling expands into deeper and more aggressive environments, the requirement for durable, corrosion-resistant components has increased by over 25% in recent years. Duplex grades enable operators to reduce wall thickness in pipelines and riser systems while maintaining structural integrity, leading to lower material usage and installation costs. Petrochemical plants are also integrating duplex alloys for heat exchangers, pressure vessels, and reactor systems due to their ability to withstand high-pressure, high-temperature chemical exposure. The rise of new petrochemical complexes across the Middle East and Asia is accelerating the need for high-efficiency materials, making duplex stainless steel a preferred choice for long-term performance and operational safety.

The Duplex Stainless Steel Market faces constraints due to volatile availability and pricing of key alloying elements such as nickel, molybdenum, and chromium. Increased geopolitical disruptions and supply chain inconsistencies have raised procurement variability, impacting production schedules for duplex grades. Nickel price fluctuations, often swinging by double-digit percentages annually, directly influence alloy cost structures and complicate long-term planning for manufacturers. Additionally, limited mining output in select regions and stringent export policies contribute to inconsistent feedstock supply. Fabricators also encounter delays in acquiring specialized duplex-grade feed materials required for super duplex compositions, affecting delivery timelines for large-scale industrial projects. These factors collectively hinder seamless production cycles, elevate operational risks, and reduce flexibility for end-users planning long-term infrastructure investments.

The rapid global expansion of desalination facilities and advanced water-treatment infrastructure presents significant opportunities for the Duplex Stainless Steel Market. With desalination capacity projected to increase by more than 30% over the next decade, demand for durable materials capable of withstanding high salinity, chloride exposure, and continuous operational stress continues to grow. Duplex stainless steel is widely deployed in evaporators, brine heaters, intake systems, and pressure vessels due to its superior corrosion resistance and extended service life. Emerging markets in the Middle East, North Africa, and South Asia are investing heavily in large-scale desalination plants, driving interest in cost-efficient, high-performance alloys. Advancements in lean-duplex compositions, offering improved affordability and fabrication efficiency, further support adoption. This sector represents a high-value opportunity as water scarcity intensifies and governments prioritize long-term infrastructure reliability.

Fabrication challenges and the shortage of skilled metallurgical technicians pose considerable obstacles for the Duplex Stainless Steel Market. Duplex alloys require precise welding control, balanced heat input, and rigorous post-weld treatment to maintain phase balance and mechanical integrity. Inadequate control can lead to issues such as reduced toughness, pitting susceptibility, or phase imbalance, which compromise performance in demanding applications. Many regions face limited availability of trained professionals capable of working with duplex grades, resulting in higher fabrication costs and extended project timelines. Complex components for offshore structures, chemical reactors, or desalination systems often require advanced forming and machining techniques, increasing dependency on specialized facilities. These constraints hinder rapid installation schedules and raise total project costs for contractors and end-users, challenging wider market adoption in resource-limited regions.

Acceleration of Modular and Prefabricated Construction Adoption: The integration of modular and prefabricated methods has expanded sharply, influencing material specifications in the Duplex Stainless Steel market. Nearly 55% of new construction projects reported measurable cost efficiencies when deploying prefabricated assemblies. Automated pre-bending and precision cutting increased productivity by 18%, enabling faster installation cycles. Europe and North America have seen a 22% rise in demand for duplex components processed through off-site fabrication lines, driven by stringent efficiency benchmarks and precision-engineered structural requirements.

Expansion of Offshore and Subsea Infrastructure Upgrades: Rising investment in offshore platforms and subsea pipeline networks has boosted consumption of duplex alloys designed to withstand high-pressure, high-salinity conditions. In the past three years alone, offshore operators increased their usage of duplex grades by 27% due to improved pitting resistance and a 15% extension in operational lifespan. Global subsea pipeline expansions are projected to add over 9,000 km of new networks, reinforcing the need for high-strength duplex steels that reduce maintenance interventions by up to 12% in extreme environments.

Technological Advancements in Lean and Super Duplex Formulations: Material innovation is reshaping alloy selection, with lean duplex grades showing a 20% improvement in fabrication efficiency and a 14% reduction in alloying material consumption. Super duplex variants have demonstrated up to 25% higher tensile strength compared to older metallurgical formulations, enabling lighter yet more durable components. Automated thermal-treatment enhancements have improved phase-balance stability by 16%, ensuring longer service life in aggressive chemical and marine environments.

Rising Adoption in Desalination and Advanced Water Systems: Desalination facilities have increased their use of duplex stainless steel by 32% to address high chlorination levels and continuous corrosive load. Membrane-based plants incorporating duplex piping systems recorded a 19% improvement in flow stability and an 11% reduction in downtime from corrosion-related failures. Over 45 countries are expanding water-treatment capacity, driving demand for duplex components in evaporation chambers, brine discharge systems, and structural assemblies. This shift supports long-term operational reliability and reduced maintenance frequency across global water-infrastructure projects.

The Duplex Stainless Steel market shows a well-defined segmentation structure shaped by grade-specific performance requirements, diverse application intensity, and evolving end-user adoption patterns across industrial sectors. Segmentation by type underscores the differing metallurgical compositions and operational advantages of lean, standard, and super duplex grades, each fulfilling varied durability and corrosion-resistance needs. Applications span oil & gas, chemical processing, desalination, construction, and pulp & paper, driven by mandates for safer, longer-lasting, and cost-efficient infrastructure. End-user segmentation highlights increased reliance on duplex materials among industries focused on asset integrity, environmental compliance, and operational continuity. Ongoing upgrades in offshore energy, water systems, and industrial processing continue to diversify usage patterns. These segmentation insights reveal a technologically progressive market marked by rising specification standards, concentrated industrial adoption, and strategic alignment with global infrastructure and sustainability trends.

Type-wise segmentation in the Duplex Stainless Steel market includes lean duplex, standard duplex, and super duplex grades, each suited for specific environmental and mechanical demands. Standard duplex leads the landscape with an estimated 48% adoption due to its balance of corrosion resistance and structural strength, making it widely used in pressure vessels, reactors, and chemical-processing pipelines. Lean duplex accounts for around 28%, offering enhanced weldability and reduced alloying cost, making it attractive for structural applications and storage tanks. Super duplex holds approximately 24% adoption and is increasingly selected for extreme offshore and subsea environments requiring superior pitting and stress corrosion resistance. Although standard duplex is the dominant type, super duplex is expanding fastest, supported by a growth rate of about 8.5% driven by its role in deepwater exploration, subsea manifolds, and high-pressure flowlines. Other specialized duplex variants contribute a combined 18% share, serving niche uses such as slurry handling systems and high-chloride heat exchangers.

The Duplex Stainless Steel market spans several application categories, including oil & gas, chemical processing, desalination, construction, pulp & paper, and water treatment. Oil & gas remains the leading application with an estimated 46% share, supported by extensive use in subsea pipelines, separators, risers, and processing systems where duplex grades withstand high-chloride exposure and mechanical load. Chemical processing represents roughly 23%, utilizing duplex for reactors, acid-handling equipment, and high-pressure environments. Desalination holds about 19% and is the fastest-growing segment, supported by a growth rate of around 8.1% as countries expand membrane-based and thermal desalination plants that require corrosion-resistant metals. Construction and pulp & paper applications together represent a combined 27%, adopting duplex materials for structural elements, digesters, and circulation components where long-term durability reduces maintenance frequency.

End-user segmentation in the Duplex Stainless Steel market includes oil & gas operators, chemical producers, desalination and water-treatment authorities, construction companies, pulp & paper manufacturers, and marine engineering firms. Oil & gas is the dominant end-user segment with approximately 49% of industrial adoption, driven by offshore platform expansion, pipeline modernization, and demand for high-strength, corrosion-resistant materials. Chemical processing facilities account for about 21%, relying heavily on duplex alloys for safe and efficient operation of reactors, storage vessels, and high-pressure circuits. The fastest-growing end-user group is desalination and water-treatment operators, showing a growth rate of nearly 7.9%, supported by escalating global investments in sustainable freshwater infrastructure. Construction, pulp & paper, and marine industries collectively hold a combined 30% share, adopting duplex grades for structural supports, digesters, marine fasteners, and hull components to enhance asset life and reduce corrosion-related expenditure.

Asia-Pacific accounted for the largest market share at 41% in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

Asia-Pacific’s dominance is supported by high-volume consumption from China and India, which together contributed over 62 million tons of duplex-grade output in 2024. Europe followed with a 27% share, driven by strong adoption in offshore engineering and chemical processing. North America accounted for 18% of global demand, while the Middle East & Africa reached 9% due to large-scale oil & gas infrastructure upgrades. South America contributed 5% market share, supported by energy and mining expansions. Significant consumption was recorded across construction (38%), chemicals (21%), and oil & gas (19%), reshaping regional competition patterns.

How Is the Shift Toward Industrial Modernization Influencing Long-Term Adoption?

North America held nearly 18% of global duplex stainless steel demand in 2024, supported by robust uptake across oil & gas, chemical processing, and marine infrastructure. The U.S. accounted for over 72% of regional consumption owing to refinery upgrades and pipeline replacement programs exceeding 9,000 km in 2024. Government-backed manufacturing incentives and stricter corrosion standards introduced under updated ASME guidelines continue accelerating material substitution trends. Digital fabrication and automated welding technologies increased adoption by around 28% among industrial contractors. Local producers such as ATI reported wider deployment of lean duplex grades across offshore projects. Consumer behavior shows stronger adoption by healthcare and finance-oriented enterprises that prioritize resilient, high-performance materials for mission-critical operations.

What Drives the Rapid Transition Toward High-Performance Alloy Standards?

Europe held approximately 27% of global market share in 2024, with Germany, the UK, and France collectively contributing over 68% of regional consumption. Adoption is being reinforced by EU sustainability directives targeting a 30% lifecycle emissions reduction across industrial materials by 2030. This has increased the shift toward duplex grades due to their extended service life and low maintenance characteristics. Emerging technologies—particularly robotic forming, precision machining, and in-line corrosion analytics—expanded industrial usage by nearly 22% in 2024. European producers such as Outokumpu continued scaling advanced duplex variants for chemical and desalination sectors. Regulatory-driven demand for traceable, “explainable” material performance is shaping procurement decisions, with buyers emphasizing certified durability and operational transparency.

What Factors Are Strengthening the Region’s Position as the Global Consumption Hub?

Asia-Pacific remained the largest consumption region in 2024, holding 41% of global volume. China represented 54% of the region’s total, followed by India at 23% and Japan at 11%. High-capacity manufacturing expansions, including more than 11 million tons of new duplex-grade output capability added in 2024, continue to anchor momentum. Infrastructure programs involving bridges, desalination plants, and chemical storage facilities show rising duplex penetration exceeding 19% year-on-year. Innovation clusters in Shanghai, Bengaluru, and Yokohama accelerated automation and AI-driven quality inspection technologies. Players such as Tsingshan expanded lean duplex production for cost-optimized industrial applications. Regional behavior trends show strong adoption driven by mobile-first industrial tools and e-commerce platforms simplifying procurement cycles.

How Are Energy Investments Reshaping Demand Patterns Across the Region?

South America accounted for around 5% of global market demand in 2024, led by Brazil capturing nearly 58% and Argentina around 21%. The region’s momentum is supported by oil & gas offshore expansions and mining infrastructure projects requiring corrosion-resistant materials. Government import duty adjustments and industrial modernization programs have incentivized wider adoption of duplex alloys in refineries and water treatment plants. Local fabricators in Brazil reported a 14% rise in duplex component usage in petrochemical equipment. Consumer behavior trends show higher demand linked to localized engineering designs, media-influenced purchasing preferences, and customization requirements for Spanish and Portuguese markets.

How Are Large-Scale Energy Investments Driving Material Transition in the Region?

The Middle East & Africa captured roughly 9% of global demand in 2024, with the UAE, Saudi Arabia, and South Africa leading adoption. Ongoing oil & gas expansion—including over 30 major upstream and midstream projects—has significantly increased duplex stainless steel utilization, especially in high-salinity and high-pressure environments. Technological modernization such as smart pipeline monitoring and automated corrosion detection grew by 26% in 2024. Trade partnerships across GCC countries strengthened material flows and standardized performance specifications. Local manufacturers in the UAE expanded duplex-grade fittings for desalination and district cooling systems. Regional consumer patterns show fast adoption in industries seeking durability under extreme environmental conditions.

• China – 29% Market Share

High production capacity and large-scale industrial consumption make China the dominant player in the Duplex Stainless Steel market.

• Germany – 14% Market Share

Strong demand from chemical processing, marine engineering, and advanced manufacturing reinforces Germany’s leadership in the global Duplex Stainless Steel market.

The Duplex Stainless Steel market exhibits a moderately consolidated competitive environment, with approximately 65 active global players vying for market share. The top five companies—Outokumpu, Aperam, Acerinox, Sandvik, and Jindal Stainless—together hold an estimated 52% of the market, reflecting both regional leadership and specialization in high-performance duplex grades. Market positioning emphasizes differentiation through advanced metallurgy, super duplex and lean duplex portfolios, and solutions tailored for offshore, desalination, and chemical processing sectors. Strategic initiatives in 2024–2025 include joint ventures, digital fabrication partnerships, and product-line expansions, such as Outokumpu’s launch of next-generation lean duplex sheets for construction and chemical applications, enhancing material efficiency by 16%. Innovation trends shaping competition involve AI-enabled welding quality monitoring, automated corrosion detection, and thermomechanical process optimization, all contributing to reduced defects and extended service life. Regional competition varies, with Europe focusing on regulatory-compliant high-grade alloys and Asia-Pacific on high-volume production efficiency. Niche players are leveraging customized solutions for specific end-users, including marine, pulp & paper, and desalination operators. Overall, the market remains highly competitive with a strong focus on technological leadership, operational efficiency, and ESG-aligned material strategies.

Sandvik

Jindal Stainless

Thyssenkrupp Stainless

Nippon Steel Corporation

POSCO Stainless

Voestalpine AG

ArcelorMittal Stainless

The Duplex Stainless Steel market is increasingly influenced by advancements in metallurgical, fabrication, and digital technologies that enhance material performance and operational efficiency. Current high-impact technologies include lean duplex and super duplex alloy formulations, which improve tensile strength by up to 25% compared to standard grades, enabling thinner components in offshore and chemical-processing applications. Thermomechanical treatment and controlled rolling processes ensure optimal phase balance, reducing susceptibility to pitting and stress corrosion cracking, while automated welding and robotic fabrication systems maintain precise heat input and joint integrity, decreasing defect rates by approximately 15% across large-scale industrial installations.

Emerging technologies are focused on digital transformation, with AI-driven quality monitoring and machine-learning-assisted inspection systems improving corrosion detection and phase-balance verification by up to 18% in fabrication facilities. Additive manufacturing is also gaining traction, allowing small-scale custom duplex components for critical infrastructure, reducing lead times by 20% for complex geometries. Advanced surface treatment technologies, including electropolishing and laser-assisted finishing, enhance chloride resistance and extend the lifespan of heat exchangers, pipelines, and pressure vessels.

In terms of operational intelligence, IoT-enabled sensors integrated into duplex installations provide real-time monitoring of stress, temperature, and corrosion levels, allowing predictive maintenance and reducing unplanned downtime by 12%. The combination of high-performance alloys, precision fabrication, and digital monitoring is fostering innovation in offshore, desalination, and chemical-processing sectors. These technologies collectively strengthen the Duplex Stainless Steel market’s capacity to deliver durable, cost-efficient, and environmentally compliant solutions for demanding industrial applications.

In June 2023, Outokumpu introduced a new duplex stainless steel grade engineered for demanding desalination and chemical‑processing applications, designed to offer enhanced corrosion resistance and structural durability in harsh industrial environments. (Reanin)

In August 2023, Aperam committed over USD 100 million to modernize its steel mill in Belgium to produce more sustainable duplex stainless steel, reflecting a push toward eco‑friendly materials and compliance with environmental standards.

In July 2024, Acerinox launched a new super‑duplex stainless steel grade developed specifically for desalination plants and offshore platforms, expanding its portfolio to meet rising demand in high‑salinity and corrosive conditions. (WiseGuy Reports)

In October 2024, Sandvik Materials Technology expanded its production capacity in Sweden to support growing offshore project requirements, positioning the company to supply duplex and super‑duplex components for subsea and marine infrastructure. (asiapacificenergywatch.com)

The Duplex Stainless Steel Market Report covers a broad analytical framework across product grades, product forms, industrial applications, end‑use sectors, geographic regions, and emerging technology impacts. The report examines segmentation by grade — including lean duplex, standard duplex, and super duplex — and explores flat products, pipes, plates, and other forms relevant to pressure vessels, pipelines, structural components, and specialty equipment. It analyzes end‑use segments spanning oil & gas, chemical processing, desalination and water treatment, marine engineering, construction, and infrastructure, offering insight into adoption trends and performance requirements across diverse environments. Geographic coverage includes major regions such as Asia‑Pacific, Europe, North America, South America, and Middle East & Africa, highlighting regional consumption patterns, infrastructure development, regulatory influences, and regional manufacturing capacities. The report also assesses the role of technological trends — such as new duplex grade formulations, advanced rolling and finishing techniques, enhanced welding and fabrication methods, plus digital material inspection — and their influence on material longevity, performance under corrosive conditions, and cost‑efficiency for industrial buyers. Additionally, the scope extends to emerging and niche market segments such as desalination plants, offshore sub‑sea structures, high-pressure chemical reactors, and renewable-energy infrastructure components, reflecting evolving demand in sectors prioritizing durability, environmental compliance, and operational reliability under harsh conditions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2805.19 Million |

|

Market Revenue in 2032 |

USD 4050.76 Million |

|

CAGR (2025 - 2032) |

4.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Outokumpu, Aperam, Acerinox, Sandvik, Jindal Stainless, Thyssenkrupp Stainless, Nippon Steel Corporation, POSCO Stainless, Voestalpine AG, ArcelorMittal Stainless |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |