Reports

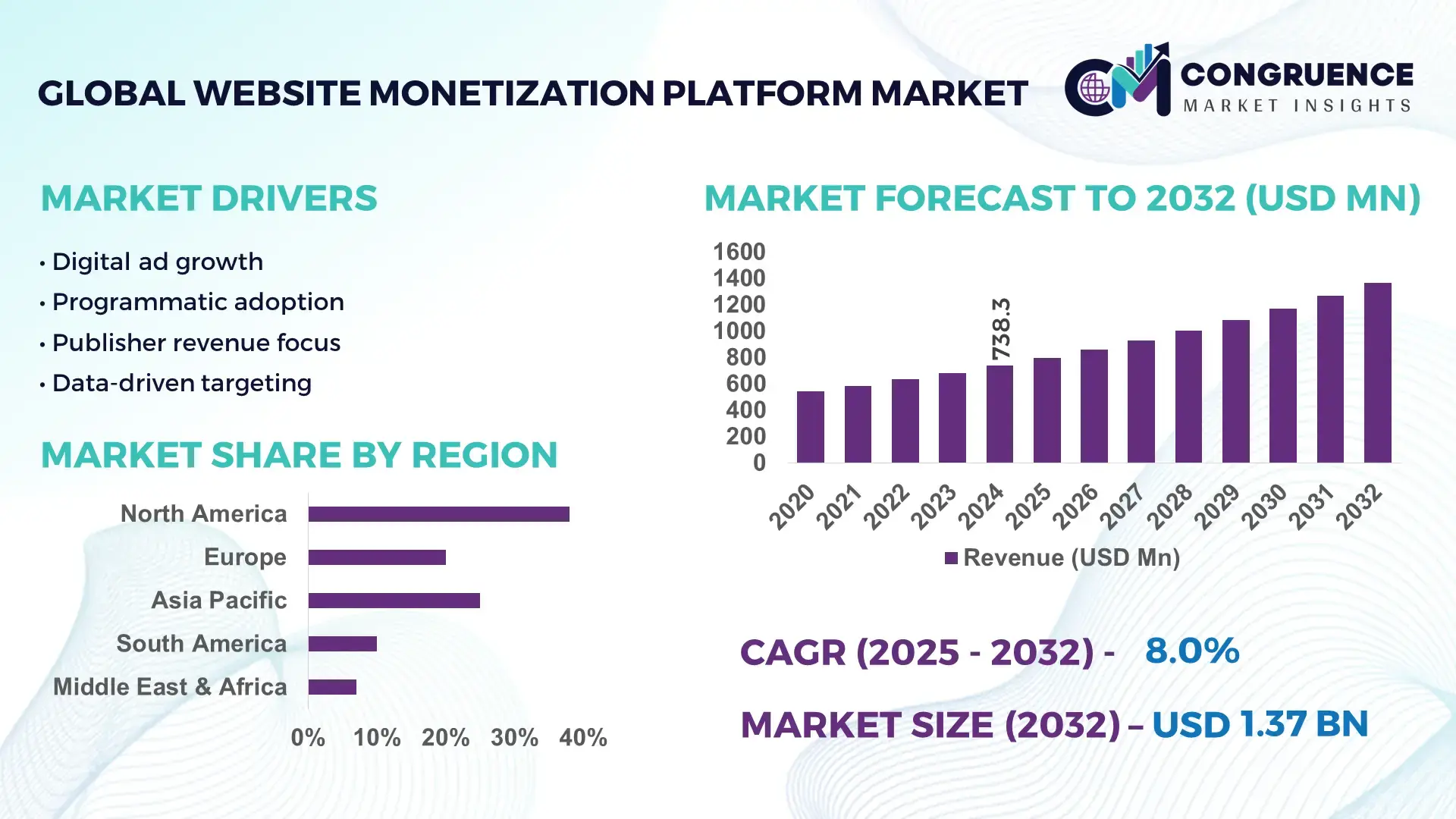

The Global Website Monetization Platform Market was valued at USD 738.33 Million in 2024 and is anticipated to reach a value of USD 1366.59 Million by 2032 expanding at a CAGR of 8% between 2025 and 2032. This growth is primarily driven by rising digital content consumption and the increasing need for diversified, performance-based revenue optimization tools among publishers and enterprises.

The United States dominates the Website Monetization Platform Market, supported by a mature digital advertising ecosystem and high platform innovation intensity. Over 65% of large-scale global publishers operate monetization stacks partially developed or hosted in the U.S., with annual platform-related investments exceeding USD 6.8 billion. Advanced AI-driven ad optimization, header bidding infrastructure, subscription management tools, and data-driven personalization engines are widely deployed. The country also leads in SaaS-based monetization deployments, accounting for over 45% of enterprise-level implementations globally. Key application areas include media & entertainment, e-commerce content platforms, online education portals, and gaming websites, with mobile-first monetization tools witnessing adoption rates above 58% among U.S.-based publishers.

Market Size & Growth: Valued at USD 738.33 Million in 2024, projected to reach USD 1366.59 Million by 2032 at a CAGR of 8%, driven by scalable digital publishing models and AI-powered monetization optimization.

Top Growth Drivers: Programmatic advertising adoption (62%), AI-based revenue optimization deployment (48%), growth in subscription-based digital platforms (41%).

Short-Term Forecast: By 2028, platform-driven revenue efficiency is expected to improve by approximately 22% through advanced analytics and real-time bidding optimization.

Emerging Technologies: AI-driven yield optimization, server-side header bidding, privacy-centric contextual targeting, and dynamic paywall technologies.

Regional Leaders: North America projected to reach USD 510 Million by 2032 with advanced AI adoption; Europe to reach USD 395 Million driven by privacy-compliant monetization tools; Asia-Pacific to reach USD 325 Million supported by mobile-first publisher growth.

Consumer/End-User Trends: Digital publishers, OTT platforms, and content-driven e-commerce websites increasingly adopt hybrid monetization models combining ads, subscriptions, and micropayments.

Pilot or Case Example: In 2024, a large media publisher pilot using AI-based yield optimization improved ad fill rates by 19% and reduced latency by 27%.

Competitive Landscape: Google leads with an estimated 34% platform presence, followed by Meta, Amazon, Microsoft, PubMatic, and Criteo.

Regulatory & ESG Impact: Data privacy regulations such as GDPR and evolving cookie restrictions accelerate adoption of consent-driven and contextual monetization solutions.

Investment & Funding Patterns: Over USD 9.2 billion invested globally in monetization technologies during 2023–2024, with strong venture funding in AI-driven ad-tech platforms.

Innovation & Future Outlook: Integration of AI, blockchain-based transparency tools, and omnichannel monetization frameworks is shaping next-generation platform architectures.

The Website Monetization Platform Market serves key industry sectors including digital media & publishing, e-commerce content platforms, online gaming, and education portals, collectively contributing over 70% of total demand. Advertising-based monetization remains dominant, while subscription and hybrid models are gaining traction. Technological innovations such as AI-powered yield management, privacy-first targeting, and real-time analytics are redefining platform capabilities. Regulatory frameworks around data privacy and cookie usage significantly influence platform design and deployment strategies. Regionally, North America and Europe exhibit mature adoption, while Asia-Pacific shows accelerated growth driven by mobile content consumption and expanding creator economies. Future market evolution will be shaped by deeper AI integration, cross-platform monetization convergence, and the rise of creator-focused revenue optimization tools.

The Website Monetization Platform Market holds growing strategic relevance as digital publishers, enterprises, and content-driven businesses prioritize sustainable, privacy-compliant revenue optimization. Monetization platforms are no longer tactical ad-serving tools; they are now embedded into enterprise digital strategy, combining data analytics, AI, subscription management, and omnichannel optimization. AI-driven yield optimization delivers up to 28% improvement compared to traditional rule-based ad-serving standards, enabling measurable efficiency gains.

From a regional standpoint, North America dominates in volume, supported by large-scale enterprise deployments and advanced ad-tech infrastructure, while Asia-Pacific leads in adoption with approximately 54% of digital-first publishers actively using multi-format monetization platforms, driven by mobile content growth and creator economies. By 2028, AI-powered contextual targeting and predictive pricing engines are expected to improve monetization efficiency KPIs such as fill rate and engagement by 25–30%, particularly in cookie-restricted environments.

Compliance and ESG considerations increasingly shape platform strategies. Firms are committing to data minimization and energy-efficient cloud processing, targeting 30% reduction in data storage intensity by 2030 through optimized data pipelines and greener hosting models. In 2024, a U.S.-based media network achieved a 21% reduction in ad latency and a 17% improvement in consented traffic monetization through server-side AI bidding optimization. Looking ahead, the Website Monetization Platform Market is positioned as a critical pillar of digital resilience, regulatory compliance, and scalable, sustainable growth across global content ecosystems.

The rapid expansion of digital content ecosystems significantly drives the Website Monetization Platform Market. Global digital content consumption has increased by over 45% since 2020, intensifying the need for efficient monetization frameworks. Publishers managing multi-format content—text, video, audio, and interactive media—require unified platforms to optimize revenue across channels. Mobile content accounts for more than 60% of total web traffic, pushing adoption of mobile-first monetization technologies. Additionally, over 70% of mid-to-large publishers now deploy at least two monetization models simultaneously, increasing platform complexity and demand for automation. These structural shifts directly elevate reliance on advanced monetization platforms capable of managing scale, personalization, and performance optimization.

Stringent data privacy regulations present a key restraint for the Website Monetization Platform Market. Frameworks such as GDPR and evolving consent requirements limit user-level tracking, reducing addressable inventory and targeting precision. Cookie deprecation can reduce behavioral targeting effectiveness by 20–40%, impacting short-term monetization outcomes. Compliance implementation also raises operational costs, with enterprises allocating up to 18% higher IT budgets toward consent management and data governance. Smaller publishers face disproportionate challenges due to limited technical resources, slowing platform adoption and innovation cycles. These constraints require continuous platform adaptation, increasing complexity and slowing uniform market expansion.

AI-driven contextual monetization presents significant growth opportunities for the Website Monetization Platform Market. Contextual targeting solutions now achieve up to 90% relevance accuracy without relying on personal identifiers, making them highly attractive in privacy-first environments. Adoption of AI-based content classification has increased by over 35% among enterprise publishers since 2022. Emerging markets in Asia-Pacific and Latin America show strong demand for lightweight, cloud-native monetization tools tailored for mobile audiences. Additionally, integration of commerce-linked content and shoppable media opens new revenue pathways, enabling publishers to diversify beyond advertising while improving engagement and monetization stability.

Platform complexity remains a major challenge for the Website Monetization Platform Market. As monetization stacks integrate AI analytics, consent frameworks, multiple demand partners, and cross-channel delivery, system management becomes increasingly resource-intensive. Large publishers report managing 15–25 active monetization integrations simultaneously, increasing latency risks and operational overhead. Technical skill shortages further compound the issue, with over 40% of digital publishers citing lack of in-house expertise as a barrier to advanced deployment. Additionally, performance optimization across geographies with varying infrastructure quality adds cost and execution risk, challenging consistent scalability and long-term efficiency.

Growing Adoption of AI-Driven Yield Optimization: Website monetization platforms are increasingly integrating AI and machine learning to enhance real-time decision-making. Around 63% of large digital publishers now deploy AI-based yield optimization tools to dynamically adjust ad placements, pricing, and formats. These systems have demonstrated efficiency gains of 20–30% in fill rates and engagement metrics. AI-driven predictive analytics is also reducing manual intervention by nearly 35%, enabling scalable monetization across high-traffic websites and multi-format content environments.

Acceleration of Privacy-First and Cookieless Monetization Models: Privacy-centric monetization has become a defining trend as over 70% of global internet users are now subject to stricter data protection frameworks. Contextual targeting adoption has increased by approximately 42% since 2022, with platforms reporting up to 90% content relevance accuracy without personal data usage. Consent-based monetization frameworks have improved opt-in rates by 18–22%, supporting stable performance while aligning with regulatory compliance and consumer trust expectations.

Expansion of Subscription and Hybrid Monetization Architectures: Subscription-based and hybrid monetization models are gaining momentum, particularly among premium content publishers. Nearly 48% of mid-to-large websites now operate a hybrid model combining advertising, subscriptions, and transactional content. Flexible paywalls and dynamic pricing engines have increased average user retention by 15–20%. This trend reflects a strategic shift toward diversified monetization portfolios that reduce dependency on single income streams and improve long-term stability.

Rise of Cloud-Native and Modular Monetization Platforms: Cloud-native deployment is reshaping platform scalability and cost efficiency. Approximately 58% of new monetization platform implementations are cloud-based, enabling faster deployment cycles and reducing infrastructure overhead by up to 25%. Modular platform architectures allow publishers to activate specific monetization components based on regional or content needs, improving operational agility. Adoption of modular systems has shortened integration timelines by nearly 30%, particularly among fast-growing digital media and creator-led platforms.

The Website Monetization Platform Market demonstrates a structured segmentation landscape based on type, application, and end-user adoption, reflecting varying monetization maturity levels across digital ecosystems. Platform types differ by deployment architecture and monetization logic, with cloud-based and AI-driven systems gaining wider enterprise preference. Application-wise, digital publishing and content media platforms represent the core demand base due to high traffic volumes and diversified monetization needs, while emerging use cases such as creator-led commerce and gaming platforms are reshaping monetization strategies. End-user segmentation highlights strong adoption among large media enterprises and e-commerce content operators, alongside accelerating uptake by SMEs and independent creators seeking scalable monetization tools. This segmentation underscores a shift from single-format monetization toward integrated, multi-channel optimization frameworks aligned with privacy compliance, performance efficiency, and audience engagement goals.

The market by type is primarily segmented into cloud-based monetization platforms, on-premise monetization platforms, and hybrid or modular monetization systems. Cloud-based monetization platforms lead the segment, accounting for approximately 52% of total adoption, driven by scalability, faster deployment cycles, and reduced infrastructure dependency. These platforms support real-time analytics, AI-based yield optimization, and seamless integration with multiple demand partners, making them the preferred choice for high-traffic publishers. Hybrid and modular monetization systems represent the fastest-growing type, expanding at an estimated CAGR of 11.6%, fueled by demand for flexible configurations that allow publishers to activate specific monetization components without full platform overhauls. On-premise platforms, while declining in relative adoption, continue to serve regulated industries and legacy media groups requiring higher data control. Collectively, on-premise and niche self-hosted systems contribute around 28% of total adoption.

By application, digital media and online publishing platforms dominate the Website Monetization Platform Market, representing nearly 46% of overall application-based adoption. This leadership is supported by sustained growth in news portals, entertainment websites, and video-streaming platforms that rely on diversified monetization models to manage fluctuating traffic volumes. E-commerce content platforms, including affiliate-driven blogs and shoppable media sites, are the fastest-growing application area, expanding at an estimated CAGR of 12.4%, supported by rising integration of content, commerce, and performance-based monetization tools. Gaming and interactive entertainment websites hold approximately 14% of application share, benefiting from in-game advertising and subscription-based premium content. Educational and professional content platforms account for a combined 18%, leveraging paywalls and membership-driven monetization.

End-user segmentation shows large media enterprises and digital publishers as the leading group, accounting for roughly 49% of total platform adoption. These organizations operate complex monetization ecosystems across multiple geographies and content formats, necessitating advanced analytics, automation, and compliance-ready solutions. Small and medium-sized enterprises represent the fastest-growing end-user segment, expanding at an estimated CAGR of 13.1%, driven by increased access to SaaS-based monetization platforms with lower upfront costs and simplified integration. Independent content creators and creator networks collectively contribute about 17% of adoption, supported by the rise of subscription tools, micropayments, and audience-supported monetization models. E-commerce operators and online service providers make up the remaining 21%, integrating monetization platforms to support content-led customer acquisition strategies.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

North America’s leadership is supported by enterprise-level platform penetration exceeding 65% among large digital publishers and strong deployment of AI-enabled monetization solutions. Europe followed with nearly 27% market share in 2024, driven by privacy-centric platform demand and regulatory-aligned monetization practices. Asia-Pacific represented approximately 23% of total market volume, supported by a digital population exceeding 3.1 billion users and rapid growth in mobile-first content ecosystems. South America and the Middle East & Africa together contributed close to 12%, supported by rising adoption of localized media platforms and mobile monetization models. Regional performance varies significantly based on regulatory maturity, infrastructure readiness, and consumer digital behavior.

How is enterprise-scale digital transformation accelerating platform adoption?

North America accounts for approximately 38% of the Website Monetization Platform Market, reflecting advanced digital infrastructure and high enterprise adoption intensity. Key demand-driving industries include digital media, OTT streaming, financial services, healthcare content platforms, and online education portals. Regulatory shifts toward data transparency and consent management have increased deployment of first-party data monetization systems. Technological advancements such as server-side bidding, real-time analytics, and AI-driven yield optimization are widely implemented, with over 60% of large publishers relying on automated optimization engines. In 2024, a major regional platform provider expanded its AI monetization suite, enabling publishers to reduce latency by 20% and improve engagement metrics across high-traffic websites. Regional consumer behavior shows higher enterprise adoption in finance and healthcare-related content, where compliance and performance reliability are critical.

Why is regulatory alignment reshaping monetization strategies?

Europe represents nearly 27% of the global Website Monetization Platform Market, led by Germany, the United Kingdom, and France. Strong regulatory oversight has increased demand for explainable, transparent, and privacy-first monetization platforms. Sustainability and digital responsibility initiatives across the region promote energy-efficient cloud infrastructure and minimized data processing. Contextual targeting and consent-based monetization adoption has surpassed 58% among European publishers. In 2024, a regional ad-tech company introduced cookieless optimization tools supporting multilingual monetization across more than 20 European markets. Consumer behavior in this region reflects higher privacy awareness, driving preference for transparent value-exchange monetization models and reduced tolerance for intrusive advertising formats.

How is mobile-first consumption redefining monetization priorities?

Asia-Pacific holds approximately 23% of global market volume and ranks as the fastest-growing region by adoption pace. China, India, and Japan together account for over 70% of regional demand. Smartphone penetration exceeds 75% of internet users, making mobile-optimized monetization platforms essential. Regional innovation hubs in India, Singapore, and South Korea are advancing AI-based personalization, multilingual monetization tools, and lightweight cloud deployments. In 2024, a leading regional provider launched scalable monetization solutions supporting more than 1 million creator-led websites. Consumer behavior across Asia-Pacific is driven by e-commerce integration, mobile advertising, in-app subscriptions, and microtransaction-based monetization models.

What role does localized digital media play in platform adoption?

South America contributes approximately 7% of the Website Monetization Platform Market, with Brazil and Argentina as the primary markets. Expansion of mobile broadband and affordable data plans has increased digital content creation by over 30% since 2021. Government-backed digital inclusion programs further support platform adoption. Regional monetization solutions emphasize language localization, regional ad demand integration, and mobile-first optimization. In 2024, a Brazil-based digital platform enhanced its monetization stack to support Portuguese and Spanish content, improving engagement across regional news and entertainment websites. Consumer behavior in South America is closely tied to localized media, culturally relevant advertising, and social-driven content monetization.

How is digital modernization unlocking new monetization opportunities?

The Middle East & Africa region accounts for close to 5% of global demand, with growth concentrated in the UAE, Saudi Arabia, and South Africa. National digital transformation programs and smart city initiatives are accelerating adoption of website monetization platforms. Over 55% of newly launched digital media projects in the Gulf region now integrate monetization platforms at inception. Technological modernization includes cloud migration, AI-enabled content analytics, and multilingual monetization capabilities. In 2024, a UAE-based digital media group deployed a unified monetization platform to support Arabic, English, and French content delivery. Consumer behavior varies widely, with strong preference for video-based and mobile monetization formats in urban markets.

United States Website Monetization Platform Market – 32% share: Dominance driven by advanced digital infrastructure, high enterprise adoption, and strong AI integration across publishing platforms.

China Website Monetization Platform Market – 14% share: Leadership supported by a massive mobile-first user base, high digital content consumption, and rapid deployment of scalable monetization technologies.

The Website Monetization Platform market exhibits a moderately consolidated yet highly competitive structure, characterized by the presence of both global technology leaders and specialized ad-tech providers. More than 120 active competitors operate globally, ranging from full-stack monetization platform vendors to niche players focused on programmatic advertising, subscription management, or contextual targeting. The top five companies collectively account for approximately 58% of total platform adoption, indicating consolidation at the enterprise level, while the remaining market remains fragmented with regional and use-case-specific providers.

Competition is primarily driven by innovation in AI-driven yield optimization, privacy-first monetization architectures, and cloud-native scalability. Strategic initiatives such as partnerships with demand-side platforms, integration with consent management tools, and frequent product upgrades are common. Over 40% of leading vendors launched major platform enhancements between 2023 and 2024, focusing on cookieless targeting and real-time analytics. Mergers and acquisitions remain selective but impactful, aimed at expanding regional reach or strengthening AI and data capabilities. Differentiation increasingly depends on latency reduction, cross-channel monetization support, and regulatory readiness, making technology depth and ecosystem integration key competitive advantages.

Google Ad Manager

Meta Platforms

Amazon Publisher Services

Microsoft Advertising

PubMatic

Criteo

Magnite

Sovrn

Media.net

InMobi

Technology evolution is a central force shaping the Website Monetization Platform Market, with platforms increasingly built on advanced analytics, artificial intelligence, and cloud-native architectures. AI and machine learning are now embedded across monetization workflows, supporting real-time bidding optimization, predictive pricing, and dynamic content placement. Approximately 62% of enterprise-level platforms deploy AI-based yield optimization engines, enabling improvements of 20–30% in fill rates and engagement metrics while reducing manual configuration requirements by nearly 35%.

Privacy-first technologies have become critical as third-party cookie usage declines. Contextual targeting engines using natural language processing and semantic analysis now achieve up to 90% content relevance accuracy without relying on personal identifiers. Consent management platforms are increasingly integrated directly into monetization stacks, supporting compliance automation and improving consented traffic monetization by more than 15%. Server-side monetization frameworks are also gaining traction, reducing page load times by 18–25% compared to client-side implementations.

Cloud-native and microservices-based architectures are reshaping scalability and deployment flexibility. Around 58% of new platform deployments leverage containerized environments, enabling faster feature rollouts and regional customization. Modular design allows publishers to activate advertising, subscription, or commerce monetization independently, shortening integration timelines by nearly 30%. Emerging technologies such as blockchain-based ad verification are being tested to improve transparency and reduce invalid traffic, which currently represents an estimated 8–10% of digital ad impressions. Looking ahead, deeper AI integration, cross-platform identity frameworks, and energy-efficient data processing are expected to further enhance performance, compliance readiness, and long-term operational resilience across the Website Monetization Platform ecosystem.

• In 2023, Google AdSense rolled out new AI-powered ad personalization formats designed to analyze user interaction patterns and deliver contextual ads in real time, with early testing showing a 27% increase in click-through rates and a 22% boost in publisher engagement across mobile and desktop traffic.

• In mid-2023, Amazon Associates expanded its influencer monetization suite by enabling seamless affiliate link integration into live streams, stories, and reels, resulting in over 46% of content creators reporting higher earnings from video-based product placements and a 33% rise in mobile affiliate link clicks.

• In 2024, Taboola introduced native video carousel ads for mobile and content-rich platforms, achieving a 38% higher interaction rate compared with static ad formats and strengthening engagement metrics for publishers focused on video monetization.

• In 2024, PubMatic expanded strategic partnerships with premium streaming brands including Roku, Disney+ Hotstar, TCL, and Xumo, working with 80% of the top 30 streaming publishers and growing its Activate customer base nearly six-fold, while supply path optimization represented 53% of total platform activity. (PubMatic Investors)

The Website Monetization Platform Market Report provides a comprehensive examination of the ecosystem that enables publishers, digital platforms, and content creators to optimize revenue from online traffic. The scope covers detailed segmentation by type, such as cloud-based, on-premise, and hybrid modular platforms, and by application across digital media publishing, e-commerce content sites, gaming, and educational portals. It also assesses end-user adoption patterns among large media enterprises, SMEs, and independent creators, with user adoption rates and platform usage statistics highlighting key consumer behavior insights.

The report spans geographic analysis across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering regional metrics on platform penetration, regulatory influences, and technology adoption trends. It includes technology insights focusing on AI-driven yield optimization, server-side header bidding, consent management integration, and first-party data monetization tools, providing measurable data on AI deployment and contextual targeting accuracy. Industry focus areas examined include programmatic advertising enhancements, privacy-first monetization models, mobile and video monetization prioritization, and cloud-native system deployments. Emerging and niche segments such as creator economy platforms, multilingual monetization tools, and blockchain-based verification systems are also outlined, along with competitive landscape insights featuring active competitors, consolidated market positioning, product innovation trends, and strategic initiatives shaping the competitive environment. This structured analysis aids decision-makers in understanding the breadth of technology, application, industry dynamics, and future monetization pathways.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 738.33 Million |

Market Revenue in 2032 | USD 1366.59 Million |

CAGR (2025 - 2032) | 8% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Google Ad Manager, Meta Platforms, Amazon Publisher Services, Microsoft Advertising, PubMatic, Criteo, Magnite, Sovrn, Media.net, InMobi |

Customization & Pricing | Available on Request (10% Customization is Free) |