Reports

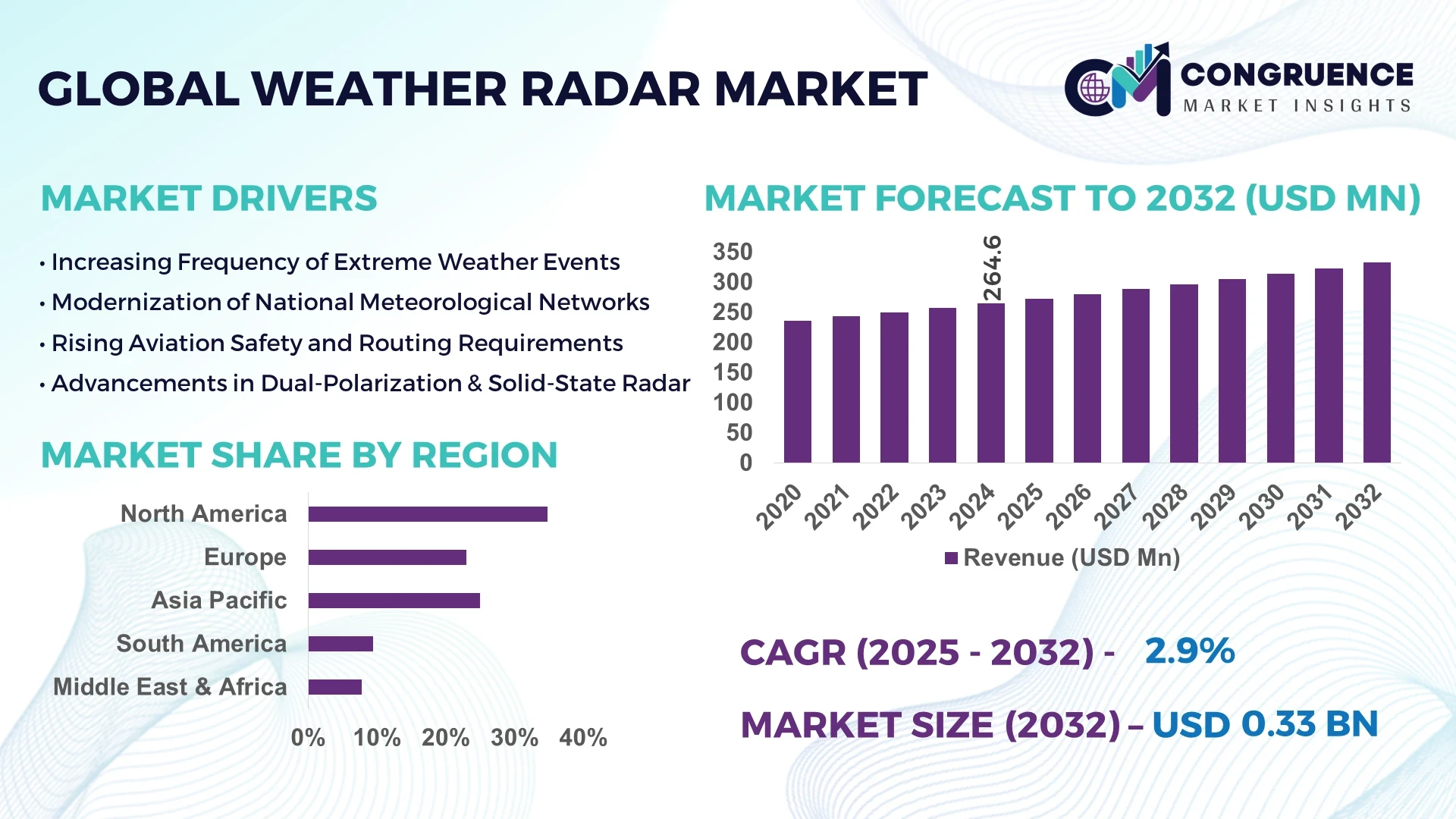

The Global Weather Radar Market was valued at USD 264.6 Million in 2024 and is anticipated to reach a value of USD 332.6 Million by 2032 expanding at a CAGR of 2.9% between 2025 and 2032.

According to estimates, the U.S. weather radar market was valued at approximately USD 72.1 Million in 2024, highlighting strong domestic deployment and institutional funding. The United States leads the Weather Radar Market with extensive investment in modernization programs, major deployments in aviation and military sectors, and expansion of smart infrastructure networks. Manufacturers in the U.S. have scaled production capacity significantly, deploying phased-array and dual-polarization systems across federal and civilian meteorological agencies. In 2024, several U.S.-based radar suppliers secured multimillion‑dollar contracts to deliver next‑generation weather surveillance platforms for airports, military bases, and national research institutions.

The broader Weather Radar Market is driven by demand from meteorology, aviation, military, and hydrology sectors. Aviation and government agencies remain key consumers, while hydrology applications support flood and disaster management. Recent product innovations include solid-state radar technology, micro-Doppler sensors, and dual-polarization systems capable of differentiating precipitation types and reducing false echoes by up to 40%. Regulatory mandates for early warning systems and climate resilience investments have accelerated procurement cycles in developed and developing regions alike. Economic drivers include increasing urbanization and infrastructure development. Regional consumption patterns show North America as mature, Europe investing in upgrades, Asia‑Pacific expanding coverage for agriculture and aviation, and Middle East & Africa beginning deployments. Emerging trends include satellite-integrated radar networks, cloud-based analytics platforms, and software‑defined systems enabling dynamic frequency selection and remote diagnostics.

The Weather Radar Market is experiencing transformative change through the integration of artificial intelligence. AI-powered radar platforms now process raw echo data at the edge, enabling real-time storm detection and classification within milliseconds. Decision-makers in meteorology and aviation report AI-based algorithms reduce false alarms by up to 30% and improve detection sensitivity by nearly 20%, greatly enhancing operational reliability for severe weather forecasting and air traffic safety.

Within the Weather Radar Market, AI systems now autonomously calibrate beam-forming parameters based on changing atmospheric conditions, optimizing scan resolution and conserving power. Predictive analytics models embedded in radar consoles forecast hardware degradation, enabling proactive maintenance scheduling and reducing system downtime by as much as 25%. These advancements also support adaptive scanning strategies, where AI dynamically adjusts pulse repetition frequency and scanning angles to target high-risk regions, improving coverage efficiency and response times.

Moreover, weather services deploying AI-enhanced radar networks report operational gains through automated pattern recognition—such as echo tracking and precipitation phase determination—reducing manual analysis workload by nearly 40%. In hydrology sectors, AI-integrated radars feed high-precision precipitation data into flood modeling tools, shortening warning lead times significantly. Across the Weather Radar Market, strategic deployment of AI enables higher performance, streamlined operations, and intelligent alerting—reshaping expectations for reliability, responsiveness, and predictive insight in both public and commercial use cases.

“In early 2025, the U.S. National Weather Service began field trials of AI-driven phased-array radar systems that automatically adjust scan rates during storm intensification, improving wind shear detection accuracy by 22% compared to conventional scanning protocols.”

The Weather Radar Market Dynamics are shaped by technological innovation, increasing demand from aviation and public safety agencies, and evolving regulatory frameworks. Key trends include the shift toward solid-state and phased-array radars, integration of AI for predictive performance, and expanded dual-polarization deployments. Global climate volatility and increasing frequency of extreme weather incidents are driving investments in radar coverage, especially in flood-prone and storm-sensitive regions. Additionally, collaborations between radar OEMs and research institutions are fostering advances in micro-Doppler sensing and satellite-link integration. Cybersecurity and system interoperability requirements are influencing procurement decisions, while multilateral programs and military-to-civil repurposing of radar assets are expanding use cases across both civil and defense domains.

The most critical driver is the rising demand for high-resolution, real-time severe weather detection systems. The aviation industry, maritime operators, and disaster management agencies require sub-minute updates on atmospheric hazards such as wind shear, hail cores, and tornadic rotation. Advanced phased-array and dual-polarization radars are capable of updating storm dynamics in less than 60 seconds, compared to several minutes with legacy systems. This speed is essential for air traffic control decisions, emergency evacuation protocols, and real-time flood warnings. Moreover, global urbanization has concentrated populations in vulnerable areas, raising the stakes for early warning systems. Governments are increasingly mandating modern radar coverage as part of national disaster resilience strategies, further accelerating market adoption.

Despite technological advances, cost and deployment complexity remain significant restraints. Next-generation weather radars can cost tens of millions of dollars per unit, factoring in antenna arrays, transmitters, site infrastructure, and data integration systems. For many developing countries or smaller municipalities, this represents a prohibitive barrier. Deployment is also lengthy, often involving multi-year procurement cycles, environmental impact assessments, site acquisition challenges, and spectrum licensing negotiations. The burden is particularly heavy for phased-array systems, which require advanced calibration and skilled operators. Budget constraints often lead to reliance on older legacy systems, creating a technology gap between advanced economies and emerging markets.

One of the most transformative opportunities lies in hybrid weather surveillance systems that integrate radar with satellite data, drones, IoT-based mobile sensors, and even crowd-sourced weather apps. By combining ground-based reflectivity data with satellite-derived precipitation and temperature fields, agencies can achieve far more granular spatial and temporal resolution. Pilot projects in the U.S., Japan, and Europe have already demonstrated how multi-sensor fusion improves the accuracy of flash flood forecasts and cyclone tracking. Additionally, the integration of radar with 5G mobile infrastructure is emerging as a potential enabler, with telecom towers serving as supplementary data nodes. This opportunity not only extends coverage to remote or mountainous regions but also supports the development of AI-driven global forecasting platforms with predictive capabilities surpassing traditional radar alone.

The expansion of radar networks is constrained by regulatory fragmentation and technical interoperability challenges. Frequency allocation for weather radar varies across regions, with competing demands from aviation, defense, and telecom industries. This leads to inconsistencies in spectrum availability and limits cross-border radar data sharing, particularly in regions like South Asia or Africa where weather systems often span multiple national boundaries. Moreover, differences in data protocols, calibration standards, and security frameworks complicate multinational projects such as regional flood forecasting systems. Vendors must navigate rigorous compliance requirements, including electromagnetic interference standards, cybersecurity mandates, and national security restrictions on dual-use technologies. Without harmonization, the goal of building integrated, continent-wide weather radar networks remains a complex challenge.

Growth in Dual‑Polarization Radar Deployments: More than 40 major meteorological agencies worldwide adopted dual‑polarization radar in recent years, enabling precise differentiation between precipitation types. This technology has reduced false echo rates significantly and improved rainfall estimation accuracy for hydrological modeling and weather warning systems.

Expansion of Phased‑Array Radar Usage: Phased-array systems are increasingly adopted by aviation and military agencies. These systems support rapid sweeping across sectors within seconds, improving real-time wind shear detection and reducing scanning cycle time by nearly 50%, enhancing decision-making speed for critical flight operations.

Migration to Software‑Defined Radar Architecture: New radar installations now support software-based frequency agility and dynamic beam shaping. Approximately 35% of newly commissioned radar networks in 2024 incorporate software-defined functionality that allows remote reconfiguration and calibration, boosting flexibility and reducing maintenance complexity.

Integration of Cloud‑Based Analytics Platforms: Weather radar systems are increasingly connected to cloud infrastructure for centralized data processing. Network operators leveraging cloud analytics report improved performance insights, with predictive maintenance alerts and spatial weather models accessible through web dashboards—facilitating collaborative forecasting and more efficient radar network management.

The Weather Radar Market is segmented into three principal categories: by type, by application, and by end-user. These segments reflect the diverse usage of radar technologies across industries such as meteorology, aviation, defense, and hydrology. Technological differentiation, operational requirements, and regional demand patterns significantly shape each segment’s growth trajectory. For instance, traditional C-band and X-band radars dominate in aviation and meteorology applications, while newer phased-array and dual-polarization types are gaining traction in research and emergency management. Applications span storm tracking, flight safety, hydrological forecasting, and climate research, with aviation and public safety departments acting as key institutional buyers. End-users include civil weather agencies, defense organizations, airport authorities, and environmental research institutes, each with specific functional needs and budget capabilities. The segmentation reveals a shift toward more integrated, real-time, and AI-driven radar solutions across all user groups.

The Weather Radar Market comprises several radar types including C-band, X-band, S-band, Ka-band, and advanced phased-array systems. Among these, C-band radar remains the leading type due to its balanced performance in medium-range weather detection and wide usage in national weather services and regional storm monitoring. C-band systems offer cost-effective solutions for tracking precipitation and severe weather, making them a preferred choice for government meteorological agencies.

Phased-array radar represents the fastest-growing segment, driven by its capability for rapid scanning, high-resolution data acquisition, and multi-directional tracking without mechanical movement. Its deployment in aviation safety, military airspace monitoring, and emergency weather detection has increased in both developed and emerging economies. The growing need for low-latency, real-time data in high-risk areas is further accelerating phased-array radar installations.

Other radar types like X-band are used in short-range applications such as localized weather detection and airport operations. S-band radars, though less common, are important for long-range and heavy precipitation tracking. Ka-band radars, while still niche, find relevance in specialized research and space-based monitoring due to their compact design and high-frequency capabilities.

Applications within the Weather Radar Market cover a broad spectrum, including meteorology, aviation, hydrology, military, and environmental monitoring. Meteorology is the dominant application, with national weather services and regional forecasting centers relying heavily on radar data for real-time storm tracking, precipitation analysis, and public warning systems. The widespread deployment of dual-polarization radar in meteorology has significantly improved rain-type classification and storm intensity modeling.

Aviation is the fastest-growing application, as global air traffic increases and the demand for enhanced flight safety continues to rise. Modern radar systems are integrated into air traffic control centers and airport infrastructure to detect wind shear, turbulence, and hazardous weather patterns, ensuring safer takeoffs and landings. Recent technological advancements allow airports to access high-resolution weather data in near real-time, reducing delays and improving airspace management efficiency.

Hydrological applications also play a vital role, with radars supporting flood forecasting, river basin monitoring, and dam safety planning. The military sector utilizes weather radar for strategic planning and situational awareness during field operations. Environmental monitoring applications, though smaller in share, contribute to climate studies and long-term ecological modeling, especially when integrated with satellite data.

The Weather Radar Market serves various end-user groups, including national meteorological agencies, defense and military organizations, airport and air navigation authorities, research institutions, and environmental agencies. National meteorological agencies are the leading end-users, supported by structured government funding and mandates to provide accurate public weather forecasting. These agencies operate large-scale radar networks and frequently upgrade to newer technologies for improved accuracy and coverage.

Airport authorities and air navigation service providers represent the fastest-growing end-user group. Their increasing investments in weather surveillance infrastructure stem from heightened air traffic volumes, stricter aviation safety regulations, and a growing need to mitigate weather-related delays. High-resolution radar data supports ground operations, air traffic control, and runway safety protocols, enabling data-driven decision-making.

Defense agencies also remain significant end-users, integrating weather radar for operational readiness, logistics planning, and tactical field deployments. Research institutions leverage radar for academic and applied climate science, while environmental monitoring bodies use radar to support disaster preparedness and ecological forecasting. Each end-user type demands customized radar capabilities suited to their operational goals and data integration systems.

North America accounted for the largest market share at 34.8% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

North America’s dominance is attributed to its highly developed weather infrastructure and strong government investments in climate resilience. Meanwhile, Asia-Pacific is seeing accelerated demand due to climate variability, rapid infrastructure development, and regional investment in weather forecasting and disaster mitigation technologies. Europe remains a stable contributor with significant demand from aviation and environmental monitoring sectors. South America and the Middle East & Africa represent growing markets driven by increased infrastructure modernization and adoption of radar-based forecasting systems in high-risk weather zones.

The North America Weather Radar Market held a dominant 34.8% share in 2024, underpinned by widespread adoption across aviation, military, and meteorological sectors. The United States leads the region due to high-frequency extreme weather events requiring real-time monitoring. The Federal Aviation Administration (FAA) and National Weather Service (NWS) have expanded investments in dual-polarization and phased-array radar networks. Recent regulatory initiatives to upgrade obsolete radar systems have spurred public-private partnerships in weather tech. Canada also contributes significantly with investments in Arctic monitoring. Technological advancements, including AI-integrated systems and networked radar infrastructure, are transforming the efficiency of regional weather surveillance operations across North America.

The Europe Weather Radar Market accounted for approximately 27.3% of the global volume in 2024, led by strong adoption in countries such as Germany, France, and the UK. The aviation and renewable energy sectors are key demand drivers, particularly with increasing focus on wind farm planning and safe airspace operations. The European Organisation for the Exploitation of Meteorological Satellites (EUMETSAT) and the EU’s Green Deal have encouraged modernization of radar networks in support of climate goals. Technological trends like the integration of weather radar with satellite observation systems and real-time data analytics are reshaping the industry. Europe also leads in regulatory frameworks ensuring radar quality standards and data interoperability.

The Asia-Pacific Weather Radar Market is the fastest-growing region, driven by high demand from China, India, and Japan. While not yet the largest, the region’s market volume is expanding rapidly due to climate-induced natural disasters and increasing investment in national weather services. China is enhancing its radar manufacturing capabilities domestically, while India is deploying Doppler radar across coastal regions to strengthen cyclone forecasting. Japan maintains a robust network tied to seismic and meteorological monitoring. Infrastructure expansion, smart city projects, and government funding for climate resilience are driving radar system upgrades. Innovation hubs in Shenzhen, Tokyo, and Bengaluru are advancing AI-enabled radar solutions across weather and disaster response functions.

The South America Weather Radar Market is gaining traction, with Brazil and Argentina emerging as regional leaders. Brazil is modernizing its radar network for improved flood and storm forecasting, especially across the Amazon and Atlantic coastal regions. Argentina has invested in radar infrastructure to support agriculture and aviation sectors. The regional market share remains moderate but is increasing with infrastructure and energy sector developments. National meteorological agencies are collaborating with defense and civil aviation departments to upgrade radar systems. Trade agreements and regional partnerships are also fostering access to advanced weather technologies from North America and Europe.

The Middle East & Africa Weather Radar Market is undergoing steady growth, supported by infrastructure investments in countries like UAE and South Africa. Demand is particularly strong in oil & gas, urban planning, and construction sectors, which require accurate climate intelligence. The UAE has launched initiatives to strengthen its early warning systems for flash floods and dust storms. South Africa is expanding its radar coverage to monitor weather impacts on agriculture and energy infrastructure. Technological modernization is a key trend, with many governments adopting digital radar networks integrated with AI-based analytics. Trade partnerships with European and Asian suppliers are enhancing equipment accessibility and training programs.

United States – 29.5% Market Share

Leads due to advanced infrastructure and large-scale deployment of phased-array and dual-polarization radar systems.

China – 17.1% Market Share

Drives growth through domestic manufacturing capabilities and widespread radar deployment for disaster resilience.

The Weather Radar Market is highly competitive, with over 40 globally active players spanning aerospace, defense, meteorology, and commercial weather systems. The competitive environment is marked by continual innovation in radar accuracy, mobility, and integration with digital platforms. Companies are vying for strategic positioning by focusing on dual-polarization technology, phased-array radar, and AI-powered data processing. Market leaders are expanding their global footprint through multi-million-dollar government contracts, defense collaborations, and infrastructure modernization initiatives. Notably, several firms have engaged in mergers and acquisitions to enhance technological capabilities or gain access to emerging markets. Product diversification remains a key strategy, with a focus on all-weather, all-terrain capabilities to meet rising demand from sectors like aviation, marine, agriculture, and disaster risk management. Emerging players are leveraging software-centric radar platforms and offering real-time analytics integration to differentiate themselves. As climate variability intensifies, competition is expected to heighten further, particularly in developing economies prioritizing weather resilience.

Leonardo S.p.A.

Raytheon Technologies Corporation

EWR Weather Radar

Honeywell International Inc.

Enterprise Electronics Corporation (EEC)

VAISALA Oyj

Selex ES GmbH

GAMIC GmbH

Furuno Electric Co., Ltd.

China Electronics Technology Group Corporation (CETC)

Collins Aerospace

Mitsubishi Electric Corporation

The Weather Radar Market is experiencing rapid technological evolution driven by the need for high-precision atmospheric data and faster real-time analytics. One major advancement is the integration of dual-polarization radar systems, which enhance the detection of precipitation types and improve accuracy in severe weather events. These systems can differentiate between rain, snow, and hail, enabling better disaster preparedness. Another significant trend is the adoption of phased-array radar, offering quicker scan times and enabling the monitoring of fast-moving weather systems like tornados or typhoons.

Solid-state radar is also gaining momentum, especially for mobile applications, due to its compact design and lower maintenance requirements. The transition from analog to digital signal processing has enhanced radar performance, allowing seamless integration with forecasting models. Additionally, radar systems are now being paired with AI and machine learning algorithms for predictive analytics, anomaly detection, and automated decision-making in critical infrastructure sectors.

Emerging technologies include cloud-based radar data aggregation, enabling cross-border data sharing and collaborative forecasting in climate-sensitive regions. Portable and drone-mounted radar units are expanding operational possibilities in remote or high-risk terrains. These advancements reflect a broader industry move toward higher automation, energy efficiency, and interoperability across platforms—critical for scalability in both developed and developing regions.

In March 2024, Leonardo S.p.A. launched a next-generation dual-polarization radar with AI-enhanced real-time storm tracking, designed for integration into urban disaster warning networks across Europe and Asia.

In January 2024, EWR Weather Radar completed the deployment of mobile radar systems for the U.S. National Guard, supporting severe weather detection during large-scale disaster relief missions.

In August 2023, Honeywell unveiled a new X-band weather radar optimized for unmanned aerial systems (UAS), expanding real-time atmospheric data capabilities for autonomous flight operations.

In May 2023, Mitsubishi Electric introduced an advanced phased-array radar platform in Japan aimed at reducing scan time by 50%, significantly improving typhoon and flash flood monitoring across coastal zones.

The Weather Radar Market Report offers a comprehensive analysis of the global landscape, focusing on the technologies, applications, regions, and key stakeholders shaping industry trends through 2032. The report categorizes the market by Type (e.g., Doppler radar, phased-array radar, solid-state radar), Application (e.g., aviation, meteorology, agriculture, maritime, defense), and End Users (e.g., government meteorological departments, airports, military, energy sectors).

Geographically, it covers major regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering granular insights into regional dynamics, infrastructure maturity, and weather-related challenges. It also explores niche opportunities in drone-integrated radar systems, weather-as-a-service platforms, and AI-powered forecast modeling. The scope extends to regulatory influences, technological upgrades, integration with IoT platforms, and emerging use cases in autonomous navigation and smart cities.

The report is designed for decision-makers in manufacturing, aviation, defense, infrastructure, and environmental monitoring sectors. It offers actionable intelligence to assess competitive positioning, technology investments, and strategic expansion into weather-sensitive industries and high-risk geographies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 264.6 Million |

| Market Revenue (2032) | USD 332.6 Million |

| CAGR (2025–2032) | 2.9 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Leonardo S.p.A., Raytheon Technologies Corporation, EWR Weather Radar, Honeywell International Inc., Enterprise Electronics Corporation (EEC), VAISALA Oyj, Selex ES GmbH, GAMIC GmbH, Furuno Electric Co., Ltd., China Electronics Technology Group Corporation (CETC), Collins Aerospace, Mitsubishi Electric Corporation |

| Customization & Pricing | Available on Request (Up to 10% Customization Free) |