Reports

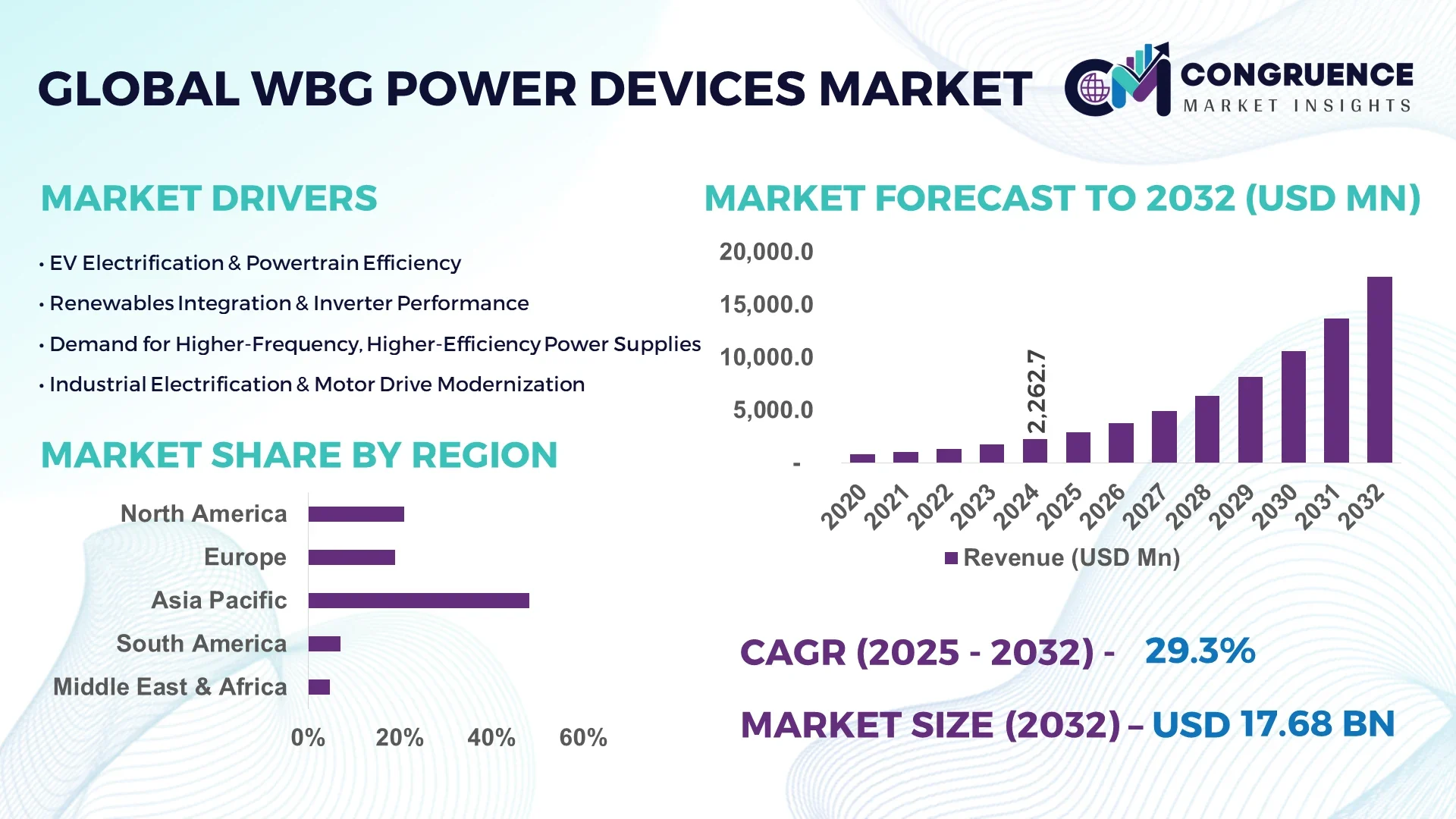

The Global WBG Power Devices Market was valued at USD 2,262.7 Million in 2024 and is anticipated to reach a value of USD 17,677.3 Million by 2032 expanding at a CAGR of 29.3% between 2025 and 2032.

North America holds a commanding position in the WBG Power Devices Market, with the region leading in annual production of SiC and GaN devices. In 2024, North American manufacturers invested heavily in next‑gen fabs, produced hundreds of millions of WBG components, and supported critical applications in automotive traction inverters and renewable energy inverters with advanced packaging and processing technologies.

The WBG Power Devices Market is driven by core sectors such as electric vehicles, renewable energy systems, industrial automation, telecom infrastructure, and data center power supplies. The automotive industry alone consumes over 40% of WBG devices, predominantly SiC MOSFETs and GaN HEMTs used in EV inverters and fast‑charging stations. Recent innovations—such as 1500 V SiC MOSFET platforms and 650‑V GaN GaNPX modules—are enabling higher switching frequencies and improved thermal performance. Regulatory mandates for energy efficiency and emissions reductions are accelerating adoption across utilities and industrial users, especially in regions with stringent environmental standards. Economic stimulus programs in mature economies are further boosting deployment, while Asia‑Pacific continues high-volume consumption for grid inverters and manufacturing. Emerging trends include integrated power modules combining WBG devices with Si drivers, AI‑enhanced assembly lines that ensure yield consistency, and hybrid modules for mixed SiC/GaN applications. Decision‑makers should note increasing demand for compact, high‑peak current designs and robust, high‑voltage packaging tailored for automotive and renewable energy systems.

AI technologies are catalyzing transformational change within the WBG Power Devices Market, significantly improving manufacturing yields, operational efficiency, and product performance. Machine learning models are now employed in wafer fabrication plants to detect and classify defects in SiC and GaN substrates, reducing scrap rates by up to 15%. In assembly, AI‑guided pick‑and‑place systems optimize die placement and soldering accuracy, boosting throughput by 20% while maintaining tight thermal design tolerances. For processing, AI‑driven real‑time analytics monitor temperature and power cycling behavior, enabling faster qualification of new device batches. In field deployment, AI‑enabled control systems dynamically adjust switching parameters to minimize losses in EV traction inverters, improving inverter efficiency by 3–5%.

Within the WBG Power Devices Market, AI also supports predictive maintenance in testing equipment and improves calibration accuracy in high‑voltage test environments. Device manufacturers report reduced failure rates and enhanced consistency across high‑volume production. In addition, AI platforms analyze performance data from deployed inverters to refine packaging algorithms and optimize dielectric layer thicknesses. The WBG Power Devices Market is also benefiting from AI in supply‑chain forecasting, helping firms balance wafer procurement and predict demand spikes in automotive and grid segments. These combined AI‑driven improvements are enabling faster time‑to‑market, reduced costs, and enhanced reliability across SiC and GaN power device portfolios.

“In mid‑2024, Infineon deployed an AI‑based optical inspection system in its new 300 mm GaN wafer fab, achieving a 12% reduction in wafer defect density and increasing usable die count by over 25%.”

The WBG Power Devices Market Dynamics reflect ongoing shifts in efficiency, miniaturization, and systems integration. As the demand for high‑performance power electronics continues to accelerate, both silicon carbide and gallium nitride devices are redefining design parameters for inverters, converters, and power modules. With energy transition agendas intensifying globally, decision‑makers in manufacturing and utility sectors are prioritizing WBG solutions to meet thermal and efficiency thresholds. Additionally, technological convergence—such as combining WBG devices with digital control ICs—enables more compact, scalable systems. Supply‑chain optimization, especially around wafer capacity and packaging supply, also plays a significant role. The market is influenced by the emergence of hybrid SiC/GaN modules, demand for robust high‑temperature packaging, and region‑specific deployment strategies in automotive, telecom, and industrial automation sectors. These dynamics frame strategic opportunities and investment decisions across the value chain.

Demand for electric vehicles and utility‑scale renewable energy is driving explosive uptake in the WBG Power Devices Market. Automotive applications account for more than 40% of device consumption, where SiC MOSFETs enable faster charging and higher power density in traction inverters. Renewable energy applications are rapidly integrating SiC and GaN in solar and wind inverters to improve conversion efficiency and reduce thermal losses. Industrial automation systems use WBG devices in motor drives and robotics for compactness and thermal resilience. Public and commercial fleet electrification, coupled with decarbonization policies, are fueling procurement of advanced power modules.

One restraint in the WBG Power Devices Market is the high complexity and cost associated with SiC and GaN wafer manufacturing. SiC substrates require specialized crystal growth and close tolerances, with fewer than a dozen global 6‑inch and 8‑inch production lines meeting quality thresholds. Yield rates for GaN on silicon substrates remain below 90% for many node geometries. Additionally, specialized packaging that withstands high voltage and temperature loads raises assembly costs. These factors limit wider adoption in cost-sensitive segments like low‑power consumer electronics, making volume scaling challenging. Workforce skill shortages in WBG process engineering further constrain capacity expansion.

An emerging opportunity in the WBG Power Devices Market lies in hybrid module development combining both SiC and GaN devices within a single package. Such modules offer tailored switching performance for mixed-voltage systems—SiC handling high-voltage bus interfaces and GaN addressing mid-to-low range switching tasks. Early prototypes show improved overall energy density, reduced system losses, and lower package volume. Hybrid modules enable manufacturers to optimize performance across automotive, industrial, and telecom power supplies. As system integrators seek more compact, efficient power trains and grid modules, these hybrid solutions could unlock new product lines and integration opportunities.

A key challenge for the WBG Power Devices Market is scaling material supply to meet surging demand. The limited number of certified SiC wafer fabs and specialized GaN foundries creates bottlenecks. Shipping delays for 6‑inch substrates and long lead times for advanced epitaxial layers disrupt production scheduling. Pricing pressure and import tariffs on silicon carbide and gallium nitride materials also pose risks. Furthermore, qualified package suppliers capable of meeting automotive AEC‑Q or utility‑grade standards are scarce. All of these factors constrain timely scaling of production, slowing market expansion in key segments.

Expansion of 300 mm GaN Wafer Production: Multiple manufacturers are moving toward 300 mm GaN wafer capacity. Adoption of 300 mm lines increases die output per wafer by over 2×, reducing unit cost and supporting high-volume consumer and data‑center demand.

Increased Use of Hybrid SiC/GaN Modules: Hybrid modules combining SiC high-voltage switches and GaN mid-voltage devices are now being piloted, delivering 20–30% improved system power density and enhanced thermal performance.

AI‑Enabled Yield Optimization Systems: Fab lines deploying AI‑based optical inspection systems have achieved up to 12% reduction in defect density and yield improvements exceeding 25%, accelerating ramp to production readiness.

Growth of Power Electronics in 5G Infrastructure: WBG devices are increasingly used in telecom base station power supplies and RF frontend modules. GaN‑based components are enabling higher frequency operation and more efficient power conversion in 5G-active deployments.

The WBG Power Devices Market is segmented by type, application, and end-user, each offering distinct growth dynamics and opportunities. By type, silicon carbide (SiC) and gallium nitride (GaN) devices dominate due to their superior performance characteristics in high-frequency and high-voltage environments. In terms of application, sectors like electric vehicles, industrial motor drives, and renewable energy inverters lead demand. End-users include automotive OEMs, energy utilities, industrial equipment manufacturers, and telecommunications providers, each adopting WBG technologies for greater efficiency and size reduction. These segments collectively reflect a shift toward more compact, thermally robust, and efficient power solutions enabled by WBG innovations. Product differentiation, application-specific performance needs, and regulatory alignment continue to influence adoption patterns across these categories.

The WBG Power Devices Market includes key product types such as silicon carbide (SiC) MOSFETs, SiC Schottky diodes, GaN high-electron mobility transistors (HEMTs), and GaN FETs. Among these, SiC MOSFETs hold the dominant position due to their high-voltage handling, thermal stability, and suitability for traction inverters in electric vehicles and power conversion in renewable energy systems. These devices are preferred in automotive platforms requiring 800V systems and beyond, delivering enhanced power density and efficiency.

The fastest-growing type is GaN HEMTs, driven by demand in telecom, data centers, and consumer fast-charging adapters. Their high-frequency switching capabilities and compact size make them ideal for RF applications and compact power supplies. GaN devices are also increasingly used in on-board chargers and AC/DC converters, where footprint and switching speed are critical.

SiC diodes and GaN FETs, while more niche, play vital roles in high-speed rectification and mid-power switching applications, respectively. Their presence supports the design flexibility of power electronics manufacturers building hybrid and application-specific power systems.

The key application areas within the WBG Power Devices Market include electric vehicles, renewable energy systems, industrial motor drives, power supplies, and RF electronics. Electric vehicles (EVs) lead the application segment, with SiC devices integrated into traction inverters, DC/DC converters, and onboard chargers. Their ability to support high-voltage and high-efficiency operation makes them indispensable to next-gen EV architectures.

Renewable energy applications are the fastest-growing segment, especially for SiC inverters used in solar and wind energy conversion. These devices increase energy capture efficiency and reduce total system footprint, enabling better returns on utility-scale installations. Growth in decentralized energy systems and supportive clean energy policies are further accelerating adoption.

Other applications include power supplies for data centers and industrial motor drives, where WBG devices enhance switching speeds and reduce thermal dissipation. RF electronics, particularly in GaN-based components, serve telecom base stations and radar systems with high power density and frequency efficiency.

End-users in the WBG Power Devices Market encompass automotive manufacturers, renewable energy providers, industrial equipment OEMs, data centers, and telecom infrastructure operators. Automotive OEMs are the leading end-user group, adopting SiC-based inverters and GaN fast chargers to support high-efficiency, compact electric drivetrain platforms. EV production scaling and charger standardization are key enablers for this dominance.

Telecom infrastructure providers represent the fastest-growing end-user segment, spurred by 5G rollouts and increasing demand for high-frequency power amplifiers and rectifiers. GaN devices are preferred here due to their small form factor and ability to operate efficiently at high frequencies and voltages, optimizing signal transmission in dense urban environments.

Industrial users and data centers also represent significant contributors. WBG devices are used in robotics, automation systems, and high-performance computing environments to reduce energy losses and improve heat management. Utilities deploying smart grid and inverter-based solutions are another important segment, driving demand for high-voltage, grid-stable power modules.

Asia-Pacific accounted for the largest market share at 48.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 32.1% between 2025 and 2032.

Asia-Pacific’s dominance is attributed to widespread adoption across electric vehicles, power grids, and industrial automation, supported by robust manufacturing infrastructure and government-led technology acceleration. In contrast, North America’s rapid growth is fueled by demand in the EV, aerospace, and renewable energy sectors, along with escalating investments in digital power electronics. Regional shifts in sustainability policies and next-gen semiconductor production are influencing procurement and R&D trends across major economies, creating highly dynamic consumption patterns and innovation cycles in the global WBG Power Devices Market.

North America captured approximately 25.6% of the global WBG Power Devices Market in 2024, with the U.S. leading regional demand. The rise in electric vehicle manufacturing, especially in the U.S. and Canada, is intensifying the use of SiC and GaN components in powertrains and onboard charging systems. Key industries driving growth include automotive, aerospace, and renewable energy. Government programs such as infrastructure modernization funds and EV subsidies are further stimulating demand for high-efficiency power semiconductors. Technological advancements like AI-enhanced predictive power modules and digital twins in energy distribution are accelerating regional adoption. Regulatory backing from the U.S. Department of Energy and a growing base of semiconductor fabs further strengthen North America’s role in global WBG innovation.

Europe held around 17.4% of the global WBG Power Devices Market share in 2024, with Germany, France, and the UK emerging as the key growth territories. Regional markets are seeing high demand from automotive OEMs pivoting toward electrification and grid-connected energy systems. Regulatory forces like the European Green Deal and the Fit for 55 framework are prompting rapid transitions to low-loss power conversion technologies. Furthermore, the EU’s focus on sustainable urban transport, combined with stringent CO₂ emission norms, is encouraging the uptake of SiC devices in rail and public mobility projects. The region also witnesses strong adoption of GaN-based chargers in the consumer electronics space, supported by innovation centers across the Netherlands and Sweden.

Asia-Pacific dominated the global WBG Power Devices Market in 2024, holding a 48.2% market share, driven by high consumption in China, Japan, and India. These nations are investing heavily in advanced manufacturing systems, EV charging networks, and renewable infrastructure. China leads both production and deployment, thanks to its integrated semiconductor supply chain and vast domestic EV market. Japan and South Korea are advancing GaN integration in telecom and power modules for industrial robotics. India’s Make-in-India initiative and rising solar deployment rates are stimulating demand for SiC inverters. Regional innovation clusters in Shenzhen, Tokyo, and Bangalore are fostering new applications in smart mobility and high-density data computing.

South America accounted for approximately 4.1% of the WBG Power Devices Market in 2024, led by Brazil and Argentina. The growing shift towards renewable energy and electric mobility is slowly boosting demand for efficient power devices across the region. Brazil’s energy sector reforms are increasing the adoption of smart grid technologies, where SiC-based modules are preferred. Argentina is witnessing rising interest in localized EV production, further driving need for GaN-based power control units. Government incentives for solar adoption and trade facilitation agreements for clean technologies are easing the path for WBG device imports. However, infrastructure gaps and limited regional production capabilities remain barriers to accelerated growth.

The Middle East & Africa (MEA) WBG Power Devices Market captured roughly 4.7% of global share in 2024. Countries like UAE and South Africa are spearheading demand, driven by large-scale infrastructure upgrades and investments in smart city initiatives. The oil & gas industry in the Gulf region is adopting high-efficiency SiC inverters for energy management systems. Additionally, UAE’s national AI and clean energy strategies are pushing digital power solutions, including GaN-based RF modules for telecom and defense. South Africa's expanding solar grid is integrating SiC power electronics for better load balancing and long-range transmission. Trade partnerships with European and Asian technology providers are facilitating modernization of power distribution networks.

China – 31.5% Market Share

Dominance is driven by its high-volume production capacity and extensive domestic EV deployment network.

United States – 22.8% Market Share

Strong end-user demand from automotive, aerospace, and renewable sectors, supported by innovation funding and advanced manufacturing ecosystems.

The WBG Power Devices Market is witnessing dynamic competition, with over 60 globally active players vying for technological leadership and market share. The competitive environment is shaped by rapid innovation in SiC and GaN technologies, as manufacturers focus on reducing power losses, improving heat tolerance, and scaling high-frequency applications. Market participants are aggressively expanding their production capacities, with many investing in vertically integrated supply chains to mitigate raw material dependencies. Strategic alliances, such as OEM partnerships and collaborations with EV manufacturers, are increasingly common, enabling faster adoption of WBG components in high-growth sectors. Several companies have announced new fabrication facilities in Asia and North America to cater to surging local demand. Mergers and acquisitions have intensified as key players aim to consolidate IP portfolios and enhance R&D capabilities. Innovation trends such as chiplet-based packaging, ultra-thin substrates, and smart gate drivers are further elevating competition. This evolving landscape offers both challenges and opportunities for established players and new entrants.

Infineon Technologies AG

ON Semiconductor Corporation

STMicroelectronics N.V.

Wolfspeed, Inc.

ROHM Co., Ltd.

Toshiba Electronic Devices & Storage Corporation

Nexperia B.V.

Renesas Electronics Corporation

Transphorm Inc.

UnitedSiC (acquired by Qorvo)

Mitsubishi Electric Corporation

GaN Systems

Navitas Semiconductor

GeneSiC Semiconductor

The WBG Power Devices Market is undergoing a technological shift, driven by the growing deployment of Silicon Carbide (SiC) and Gallium Nitride (GaN) devices across multiple industries. SiC devices are increasingly used in high-voltage applications such as electric vehicle inverters, industrial motor drives, and renewable energy systems. They offer up to 80% reduction in power losses compared to traditional silicon-based counterparts and support operations at voltages exceeding 1,200V. GaN devices, on the other hand, are being widely adopted in low- to medium-voltage domains such as fast chargers, consumer electronics, and data centers due to their high switching speeds and compact packaging.

Emerging technologies include GaN-on-Si substrates, which help reduce manufacturing costs while maintaining performance, and SiC trench MOSFETs, which offer improved channel mobility and lower RDS(on). Packaging innovations, such as multi-chip modules (MCMs) and co-packaged drivers, are enabling better thermal management and integration with digital control units. AI-powered design optimization tools and predictive failure diagnostics are also being incorporated into power modules, enhancing product lifecycle and system efficiency. As WBG technology matures, hybrid solutions combining GaN and SiC components are expected to proliferate, offering performance customization across diversified application ecosystems.

• In January 2024, Wolfspeed inaugurated its 200mm SiC fabrication facility in New York, the world’s largest dedicated SiC plant. This strategic expansion aims to meet rising demand from the automotive and renewable sectors and boost annual output capacity significantly.

• In March 2024, STMicroelectronics launched its third-generation 1200V SiC MOSFETs, featuring reduced conduction losses and enhanced switching speeds, optimized for EV powertrains and solar inverters.

• In November 2023, ROHM Co., Ltd. and Delta Electronics announced a partnership to co-develop next-gen GaN-based power modules for industrial applications, focusing on energy savings and compact form factors.

• In April 2024, Infineon Technologies unveiled CoolGaN™ power solutions designed for high-efficiency data center applications, improving energy conversion rates in AC-DC and DC-DC topologies.

The WBG Power Devices Market Report provides a comprehensive and strategic evaluation of the global industry focused on wide bandgap semiconductors, specifically Silicon Carbide (SiC) and Gallium Nitride (GaN) devices. The report covers detailed segmentation across product types (e.g., discrete devices, modules), applications (e.g., EVs, industrial equipment, consumer electronics, renewable energy systems), and end-user industries (e.g., automotive, telecom, aerospace, energy, manufacturing). It includes regional analysis spanning North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, identifying key markets and emerging growth zones.

Special emphasis is placed on technological advancements, manufacturing trends, supply chain dynamics, and evolving regulatory frameworks that influence product adoption. The report also considers niche segments such as GaN RF devices for 5G infrastructure and SiC-based modules for grid-connected storage systems. It identifies leading companies, innovation clusters, and competitive shifts, offering valuable insights for C-level executives, strategic planners, and industry analysts. Additionally, the scope integrates infrastructure developments, government initiatives, and the transition toward energy-efficient power systems that are reshaping the future of semiconductor applications globally.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,262.7 Million |

| Market Revenue (2032) | USD 17,677.3 Million |

| CAGR (2025–2032) | 29.3 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Infineon Technologies AG, ON Semiconductor Corporation, STMicroelectronics N.V., Wolfspeed, Inc., ROHM Co., Ltd., Toshiba Electronic Devices & Storage Corporation, Nexperia B.V., Renesas Electronics Corporation, Transphorm Inc., UnitedSiC (acquired by Qorvo), Mitsubishi Electric Corporation, GaN Systems, Navitas Semiconductor, GeneSiC Semiconductor |

| Customization & Pricing | Available on Request (10 % Customization is Free) |