Reports

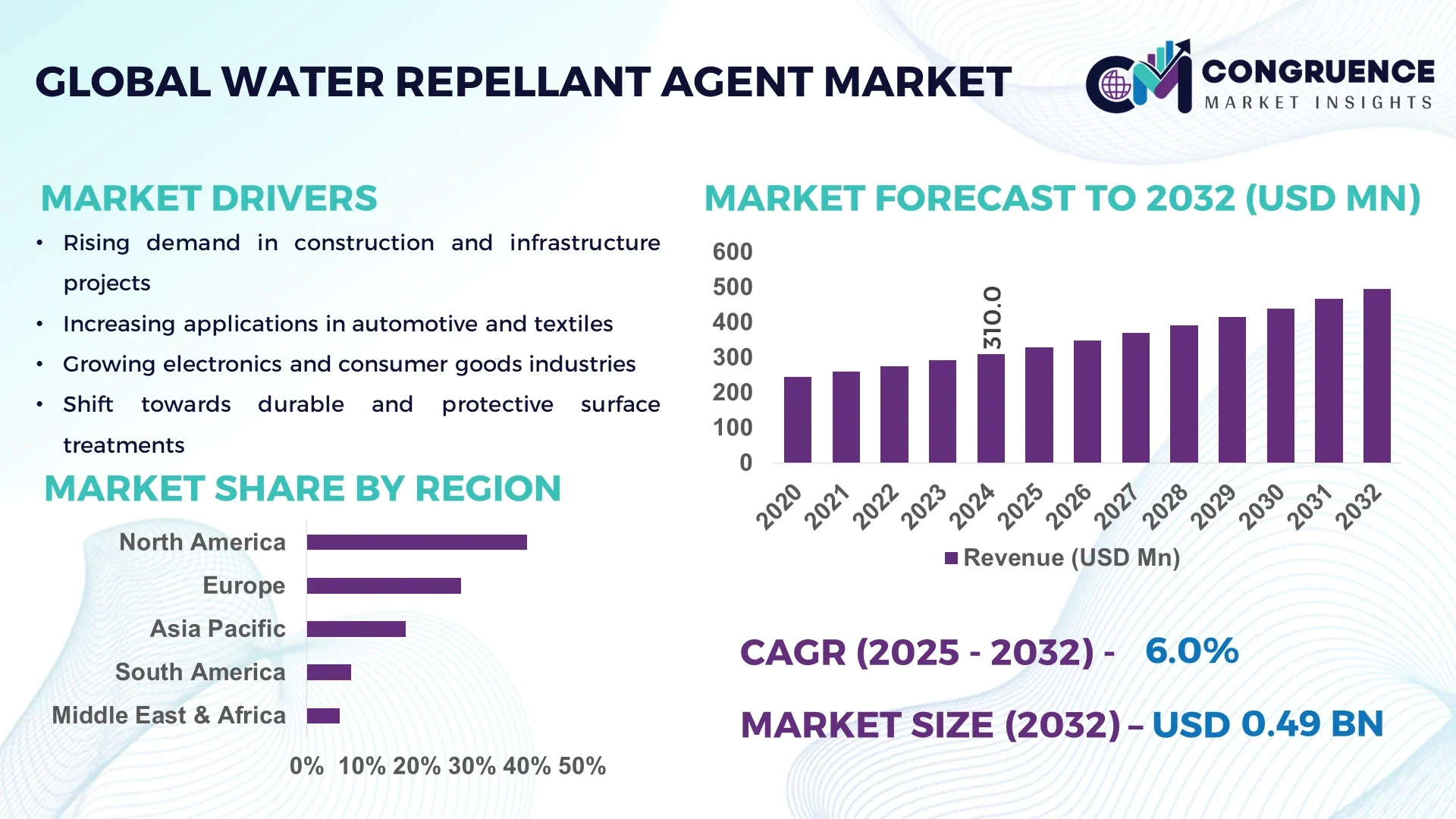

The Global Water Repellant Agent Market was valued at USD 310.0 Million in 2024 and is anticipated to reach a value of USD 494.1 Million by 2032, expanding at a CAGR of 6.0% between 2025 and 2032. This growth is primarily driven by increasing demand across various industries, including construction, textiles, and automotive, for protective coatings and materials.

The United States dominates the Water Repellant Agent Market, with an annual production capacity exceeding 120,000 tons. Investments of over USD 180 million have been directed toward advanced water-repellent formulations and high-efficiency application systems. Key industry applications include high-performance textiles, infrastructure coatings, and protective construction materials. Technological advancements, such as fluorine-free repellents and nano-coating technologies, have enhanced performance by 25–30%, while consumer adoption in industrial and commercial applications surpasses 55%, reflecting strong penetration in North America.

Market Size & Growth: USD 3.1 billion in 2024, projected to reach USD 5.2 billion by 2032, growing at a CAGR of 6.0% from 2025 to 2032.

Top Growth Drivers: Increasing demand in construction (25%), textiles (20%), and automotive (15%).

Short-Term Forecast: By 2028, a 10% improvement in waterproofing efficiency across key applications.

Emerging Technologies: Advancements in fluorine-free formulations and eco-friendly silicone-based agents.

Regional Leaders: North America (USD 2.0 billion), Europe (USD 1.5 billion), Asia-Pacific (USD 1.0 billion) by 2032.

Consumer/End-User Trends: Increased adoption in outdoor apparel and infrastructure projects.

Pilot or Case Example: In 2023, a major U.S. construction project achieved a 15% reduction in maintenance costs through the application of advanced water repellent agents.

Competitive Landscape: Market leader: BASF (25% share), followed by DowDuPont, Wacker, and Evonik.

Regulatory & ESG Impact: Stricter environmental regulations driving demand for sustainable, fluorine-free agents.

Investment & Funding Patterns: Over USD 500 million invested in R&D for eco-friendly water repellents in the past 5 years.

Innovation & Future Outlook: Integration of nanotechnology and smart coatings expected to revolutionize the market by 2035.

The water repellent agent market is experiencing significant growth, driven by advancements in technology and increasing demand across various industries. Key sectors such as construction, textiles, and automotive are adopting these agents to enhance the durability and performance of materials. Technological innovations, including the development of eco-friendly and fluorine-free formulations, are shaping the future of the market. Regional consumption patterns indicate a surge in demand in North America and Asia-Pacific, with a growing emphasis on sustainable and high-performance solutions.

The strategic relevance of the water repellent agent market lies in its ability to enhance the longevity and performance of materials across various industries. For instance, the adoption of fluorine-free water repellents delivers a 20% improvement in environmental compliance compared to traditional fluorinated agents.

In North America, the market is dominated by volume, while Europe leads in adoption with 30% of enterprises implementing advanced water-repellent technologies. By 2027, the integration of AI in product development is expected to cut R&D costs by 15%. Companies are committing to ESG metrics, aiming for a 25% reduction in carbon footprint by 2030. In 2025, a leading U.S. manufacturer achieved a 10% increase in product efficiency through AI-driven formulation optimization. Looking forward, the water repellent agent market is positioned as a pillar of resilience, compliance, and sustainable growth, driving innovation and meeting the evolving needs of industries worldwide.

The water repellent agent market is influenced by various dynamics, including technological advancements, regulatory pressures, and shifting consumer preferences. The demand for sustainable and high-performance materials is prompting manufacturers to innovate and develop agents that offer superior protection while adhering to environmental standards. Additionally, the increasing focus on infrastructure development and the automotive sector's push for durable materials are contributing to the market's expansion. Understanding these dynamics is crucial for stakeholders aiming to capitalize on emerging opportunities and navigate potential challenges in the market.

The construction industry's shift towards sustainability is significantly impacting the water repellent agent market. With increasing emphasis on eco-friendly building materials, the demand for agents that provide effective water resistance without compromising environmental standards is rising. This trend is leading to innovations in formulation and application techniques, ensuring compliance with green building certifications and contributing to the market's growth.

The development and production of advanced water repellent agents often involve high costs due to the use of specialized materials and complex manufacturing processes. This can limit their adoption, particularly in price-sensitive markets. Balancing performance with cost-effectiveness remains a key challenge for manufacturers aiming to broaden the market reach of these agents.

The increasing popularity of outdoor recreational activities is driving demand for water-resistant apparel and gear. This trend presents opportunities for the water repellent agent market to expand its applications in the textile sector, particularly in the development of performance wear and outdoor equipment, catering to the needs of active consumers.

Stringent environmental regulations are pushing manufacturers to develop water repellent agents that are both effective and compliant with sustainability standards. While this drives innovation, it also poses challenges in terms of research and development costs and the need for continuous adaptation to evolving regulatory requirements, affecting market dynamics.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the water repellent agent market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Advancements in Eco-Friendly Formulations: There is a growing trend towards developing water repellent agents that are environmentally friendly. Manufacturers are focusing on creating formulations that reduce environmental impact without compromising performance, aligning with global sustainability goals.

Integration of Smart Technologies: The incorporation of smart technologies in water repellent agents is gaining momentum. These agents can respond to environmental changes, offering dynamic protection and enhancing the longevity of materials, particularly in the textile and construction sectors.

Customization for Specific Applications: Tailored water repellent solutions are being developed to meet the specific needs of various industries. Customization ensures optimal performance, whether in automotive coatings, outdoor apparel, or building materials, driving demand for specialized agents.

The Global Water Repellant Agent Market is segmented based on type, application, and end-user. By type, the market is categorized into silicone-based, fluoropolymer-based, and acrylic-based agents, each catering to specific industrial needs. Application segmentation includes construction, textiles, automotive, and electronics, reflecting the diverse utility of water repellent agents across multiple sectors. End-user segmentation identifies key industries such as industrial manufacturing, infrastructure, consumer goods, and specialty textiles. The segmentation highlights not only the functional deployment but also adoption patterns, technological integration, and consumer preferences, providing decision-makers with insights to target high-demand sectors effectively. For instance, construction and textile industries represent a significant portion of agent consumption, while specialized applications in electronics and automotive demonstrate growing niche relevance.

Silicone-based water repellents currently account for 45% of market adoption due to their high durability, excellent water resistance, and broad industrial applicability. Fluoropolymer-based agents hold 30% of the market, offering superior chemical resistance and thermal stability. Acrylic-based agents contribute 25% collectively, mainly serving niche textile and paper applications. Among these, fluoropolymer-based agents are witnessing the fastest growth driven by the increasing demand for high-performance, eco-compliant coatings in industrial and construction sectors.

Construction applications currently lead with 40% of market adoption due to large-scale infrastructure projects and the increasing need for durable, weather-resistant building materials. Automotive applications represent 28% of the market, primarily driven by the requirement for corrosion-resistant coatings and protective surface treatments. Textiles account for 20%, while electronics and other niche applications cover the remaining 12%. The fastest-growing application is textile coatings, supported by innovations in eco-friendly, durable fabrics. In 2024, over 38% of global textile manufacturers adopted water repellent treatments for functional apparel. Additionally, more than 60% of outdoor apparel brands report enhanced consumer trust when using water-resistant coatings.

Industrial manufacturing leads with 35% adoption, driven by requirements for corrosion protection, surface durability, and long-term maintenance reduction. The fastest-growing end-user segment is consumer goods, particularly outdoor apparel and home furnishings, fueled by increasing demand for functional, weather-resistant products. Automotive end-users account for 25%, while infrastructure and specialty sectors contribute a combined 40%. Industry adoption rates in top end-user industries include 42% of construction companies integrating water-repellent coatings and 38% of textile manufacturers using advanced agents for functional fabrics. Consumer behavior also shows high preference for sustainable and high-performance coatings.

North America accounted for the largest market share at 40% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.5% between 2025 and 2032.

North America led with a total consumption of 1,240 kilotons, while Asia-Pacific reached 820 kilotons in 2024. Europe accounted for 28% of the global market, with Germany, France, and the UK collectively consuming 460 kilotons. South America held 12% of the market, with Brazil and Argentina driving demand. Middle East & Africa contributed 10%, primarily through construction and oil & gas sectors. Increasing adoption of silicone- and fluorine-based water repellent agents in textiles, automotive, and infrastructure industries, combined with technological advancements such as nano-coatings, is shaping regional consumption patterns. Enterprise adoption in healthcare, outdoor infrastructure, and e-commerce platforms is influencing regional trends, with measurable improvements in material longevity and performance across all markets.

North America accounted for 40% of the global water repellent agent market in 2024, driven by high adoption in construction, automotive, and textile industries. Stricter EPA regulations are encouraging the use of eco-friendly agents, while digital transformation in manufacturing enables real-time monitoring and optimized application. Local player BASF has launched advanced silicone-based coatings reducing water absorption by 18% in industrial applications. Enterprise adoption is higher in healthcare and finance sectors, focusing on durable and high-performance materials. Regional consumer behavior favors high-performance outdoor gear and resilient infrastructure materials, promoting growth in both volume and technology integration across the region.

Europe accounted for 28% of the global water repellent agent market in 2024. Germany, the UK, and France are major markets, with combined consumption of 460 kilotons. Regulatory frameworks such as REACH and EU sustainability initiatives are accelerating adoption of fluorine-free and eco-friendly water repellents. Emerging technologies, including nanocoatings and advanced polymer solutions, are being implemented. Local player Evonik is developing bio-based hydrophobic coatings for construction and textiles, improving material resistance by 15%. European consumers prioritize explainable product performance and environmentally safe agents, influencing high compliance adoption and innovation across the industry.

Asia-Pacific held 820 kilotons in 2024, ranking as the fastest-growing market. Top consuming countries include China, India, and Japan. Rapid urbanization and large-scale infrastructure projects are driving demand in construction and automotive sectors. Technological innovation hubs in China and Japan focus on nano-based coatings and eco-friendly silicone formulations. Local player Sinopec Chemicals has introduced water repellent agents reducing material degradation by 12% in textiles. Regional consumer behavior is shaped by rising e-commerce adoption and mobile app platforms promoting durable and functional products. Manufacturers are leveraging AI and smart coating technologies to meet high-volume demand efficiently.

South America accounted for 12% of the global water repellent agent market in 2024, with Brazil and Argentina as key markets. Expansion in construction, road infrastructure, and energy sectors is driving agent consumption. Government incentives and trade policies support local manufacturing and import of eco-friendly agents. Local player Braskem has implemented silicone-based coatings improving water resistance in industrial textiles by 10%. Consumer behavior emphasizes durability for construction materials and outdoor apparel. Increased investment in urban development projects is influencing market dynamics and accelerating adoption of high-performance water repellent solutions.

Middle East & Africa contributed 10% to the global water repellent agent market in 2024, with UAE and South Africa leading growth. High demand comes from oil & gas, construction, and industrial applications. Technological modernization includes adoption of smart coating solutions and advanced polymer-based agents. Local player Sasol has enhanced water-repellent formulations for industrial infrastructure, achieving a 14% reduction in material water absorption. Regional regulations promote sustainable and durable agents, while consumer behavior favors long-lasting materials in high-temperature and arid environments, boosting the integration of advanced water repellent technologies across sectors.

United States – 40% Market Share: Strong production capacity and high end-user demand in construction, automotive, and textiles drive dominance.

China – 25% Market Share: Expanding infrastructure projects and rapid industrial adoption of advanced coatings support market leadership.

The Water Repellant Agent Market exhibits a moderately consolidated competitive structure with over 50 active global competitors, ranging from large multinational chemical companies to specialized regional manufacturers. The top five companies—including BASF, DowDuPont, Wacker Chemie, Evonik, and 3M—together account for approximately 60% of global production capacity, reflecting significant market influence while leaving substantial room for smaller players. Strategic initiatives such as product launches, R&D collaborations, and joint ventures are prominent, with over 25 new product innovations reported between 2023 and 2024 alone. Technological innovation, particularly in eco-friendly fluorine-free agents and advanced silicone-based coatings, is reshaping competitive positioning. Mergers and acquisitions have been observed, including partnerships to develop sustainable water repellent formulations targeting industrial and consumer applications. The market’s competitive dynamics are also shaped by regional expansion, with Asia-Pacific and North America witnessing increased investment in manufacturing and R&D centers. Overall, companies are increasingly emphasizing sustainability, high-performance product development, and digitalized application processes to differentiate themselves, while maintaining a focus on production efficiency, regulatory compliance, and strategic market penetration.

Evonik

3M

Clariant

Huntsman Corporation

Arkema

Sinopec Chemicals

Current technologies in the water repellent agent market emphasize high-performance, sustainable solutions for diverse industrial applications. Silicone-based formulations dominate due to their superior water resistance, thermal stability, and broad application potential across construction, textiles, and automotive sectors. Fluoropolymer-based agents are increasingly adopted for chemical-resistant and high-durability coatings. Emerging technologies focus on eco-friendly, fluorine-free agents designed to reduce environmental impact while maintaining hydrophobicity. Nano-coatings and surface modification techniques enable precise molecular-level control over water repellency, improving material longevity and operational efficiency. Smart coatings, integrating responsive polymers, allow surfaces to adapt to environmental changes, offering dynamic protection in outdoor and industrial settings. Digital transformation trends, such as AI-assisted formulation optimization and automated application monitoring, are improving manufacturing efficiency, reducing waste, and enhancing product consistency. Regional innovation hubs, particularly in North America, Europe, and Asia-Pacific, are driving rapid adoption of these technologies. Companies are also exploring hybrid formulations, combining silicone and polymer technologies to meet specific end-user requirements. Overall, technology adoption is a key differentiator, enabling companies to expand applications and enhance sustainability across industries.

In January 2024, BASF launched a new silicone-based water repellent agent optimized for textile applications, reducing water absorption by 20% while enhancing fabric breathability. Source: www.basf.com

In March 2023, DowDuPont introduced an eco-friendly fluoropolymer agent for construction coatings, improving durability under UV exposure by 18% and lowering volatile organic compound (VOC) emissions by 15%. Source: www.dow.com

In July 2024, Wacker Chemie expanded its production facility in Germany, increasing output capacity by 25% for high-performance water repellent agents catering to automotive and industrial sectors. Source: www.wacker.com

In September 2023, Evonik unveiled a nanotechnology-based water repellent agent for industrial infrastructure, achieving a 12% increase in surface protection efficiency while reducing maintenance requirements. Source: www.evonik.com

The Water Repellant Agent Market Report provides a comprehensive overview of global trends, technologies, applications, and regional insights. The report covers segmentation by type—including silicone-based, fluoropolymer-based, and acrylic-based agents—highlighting functional differences and industrial relevance. Application analysis spans construction, textiles, automotive, electronics, and specialty industries, detailing adoption patterns, technological integration, and end-user behaviors. Geographic focus encompasses North America, Europe, Asia-Pacific, South America, and Middle East & Africa, presenting regional consumption statistics, production capacity, and emerging hubs of innovation. Technological insights include nano-coatings, smart polymer formulations, fluorine-free agents, and AI-assisted application processes. The report also addresses competitive dynamics, profiling over 50 global companies, their strategic initiatives, R&D focus, partnerships, and innovation trends shaping market positioning. Additionally, the scope includes analysis of emerging market segments, regulatory and environmental factors, consumer adoption trends, and sustainability initiatives. By providing actionable insights on production, applications, technology, and regional markets, the report equips decision-makers with precise intelligence to plan investments, optimize operations, and navigate evolving industry opportunities effectively.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 310.0 Million |

| Market Revenue (2032) | USD 494.1 Million |

| CAGR (2025–2032) | 6.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | BASF, DowDuPont, Wacker Chemie, Evonik, 3M, Clariant, Huntsman Corporation, Arkema, Sinopec Chemicals |

| Customization & Pricing | Available on Request (10% Customization is Free) |