Reports

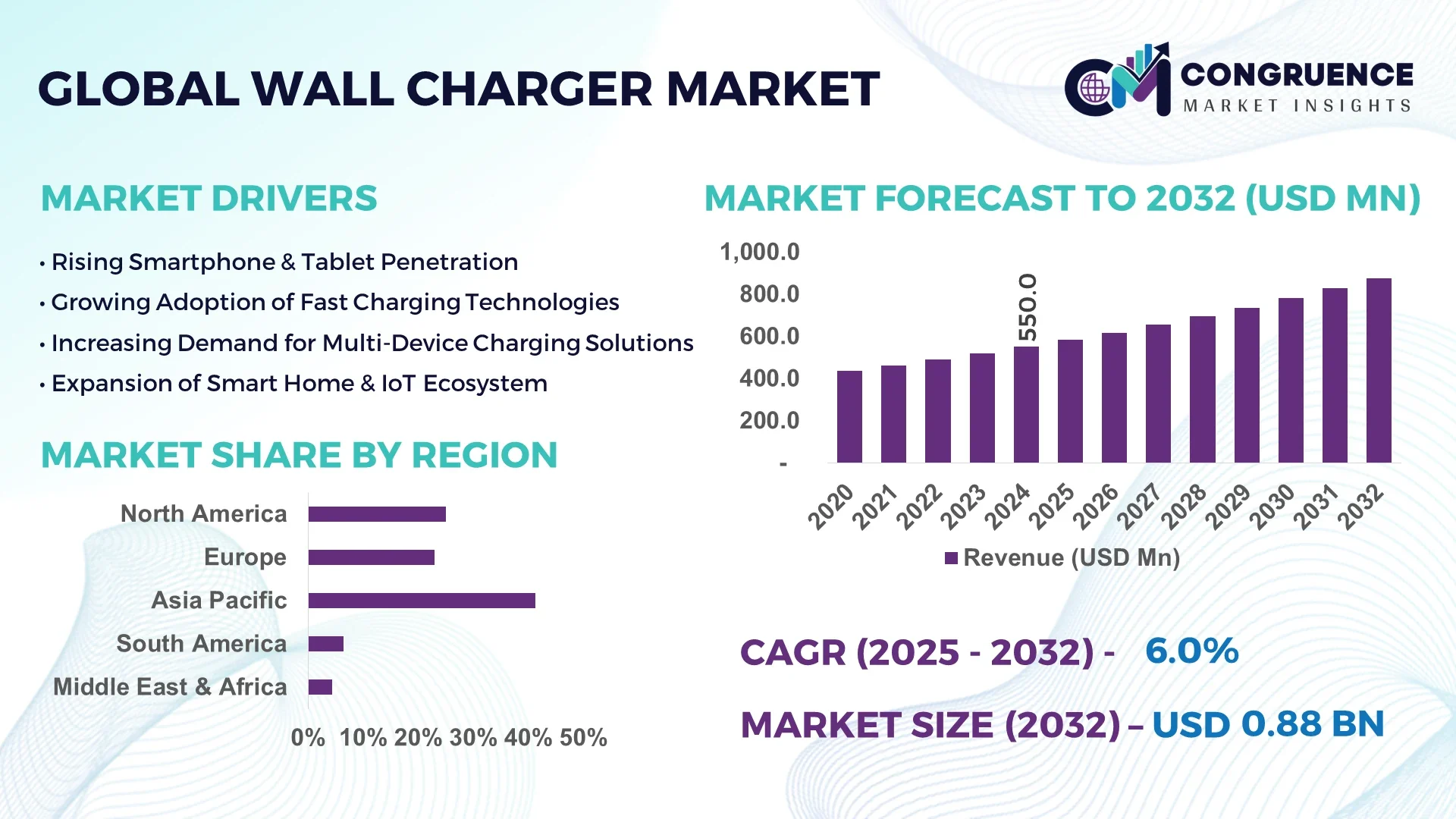

The Global Wall Charger Market was valued at USD 550.0 Million in 2024 and is anticipated to reach a value of USD 876.6 Million by 2032 expanding at a CAGR of 6.0% between 2025 and 2032.

China leads global production capacity, investing heavily in state-of‑the‑art manufacturing facilities and high‑throughput assembly lines for wall chargers. Its industry has scaled to mass‑produce charging units for consumer electronics, automotive, and IoT device segments. Recent capital expenditures exceed USD 500 million in advanced assembly automation, and R&D centers are advancing thermal management, GaN semiconductors, and miniaturization technologies to support high-precision manufacturing and product reliability.

Across the Wall Charger Market, key industry sectors include the residential, commercial, and industrial segments. The residential sector accounts for around 55% of total unit volume, driven by growing demand for fast-charging smartphones and tablets, while commercial installations—such as in offices and retail environments—contribute about 30%, and industrial and specialized applications—including EV charging infrastructure and IoT devices—account for the remaining ~15%. Technological innovations shaping the market include GaN-based fast chargers, USB Power Delivery (PD) protocols, and multi-port intelligent charging modules that reduce charging times by up to 50%. Regulatory drivers such as mandated USB‑C compatibility in major markets and energy efficiency standards are influencing product specifications and certification requirements. Environmental and economic trends include the phasing out of inefficient chargers with high standby power drain (idle losses of 10–15%) and rising adoption of eco‑friendly recyclable materials. Regionally, North America leads consumption, followed by Europe and Asia Pacific, with growth fueled by widespread device penetration. Emerging trends such as integration of smart connectivity (Wi‑Fi, Bluetooth, app control), modular charger form‑factors for adaptable installation, and the increasing prevalence of fast‑charging technologies signal sustained demand. The future outlook highlights continued expansion of product diversification, rising specifications for charge density and thermal efficiency, and increasing customization for vertical sectors like smart homes and commercial infrastructure.

AI is reshaping the Wall Charger Market by enabling intelligent, predictive, and adaptive charging solutions across product design, manufacturing, and user experience. Within the production environment, AI-driven quality control systems—employing machine vision and anomaly detection—have reduced defect rates in wall charger assembly lines by over 30%, enhancing reliability and reducing scrap. Operational performance in testing stations has improved as AI algorithms optimize burn-in time and thermal profiling, resulting in throughput gains of 15–20%.

In consumer applications, AI-embedded chargers now dynamically adjust charging current in response to device battery health, temperature, and usage patterns—extending battery life and reducing thermal stress. Smart wall charger units with built-in AI monitor cable resistance, ambient temperature, and voltage fluctuations, and can throttle power delivery to prevent overheating events by up to 25%. Some advanced models include AI-based load balancing for multi‑port configurations, distributing power according to real-time demand and preventing overloads in multi-device charging scenarios.

On the logistics and supply chain side, AI forecasting tools analyze shipment volumes and component lead times to automate inventory reorder triggers—cutting lead‑time variability by up to 40%. Predictive maintenance in production lines identifies failing tools or component misalignments before failure occurs, minimizing downtime through AI alerting.

In summary, AI deployment across the Wall Charger Market is driving operational efficiency, product reliability, and user‑centric smart features. These gains translate into tangible cost reductions, enhanced safety, and differentiated product value propositions for industry stakeholders.

“In mid-2024, a leading electronics manufacturer rolled out an AI‑powered charger model that reduced thermal shutdown incidents by 24 % during stress tests by dynamically modulating power delivery based on real‑time temperature and load sensors.”

The Wall Charger Market is experiencing dynamically evolving trends driven by technology integration, regulatory shifts, and changing consumption patterns. Rising adoption of smartphones, tablets, laptops, and IoT devices continues to elevate demand for efficient and fast wall charging solutions. Technological trends such as GaN semiconductor adoption, USB‑C Power Delivery standards, and multi‑port intelligent modules are redefining product specifications and user expectations. Regulatory mandates—such as EU requirements for universal USB‑C compatibility—are influencing redesign and compliance prioritization. Regional consumption is highest in North America and Europe, where infrastructure maturity and high device per capita penetration drive sales. Meanwhile, Asia Pacific sees growing investment in manufacturing and adoption. Environmental concerns around standby power waste, safety certifications, and electronic waste regulations are shaping product features and development priorities. Innovation is shifting toward modular, high-efficiency, connected chargers tailored to verticals like smart homes, workplaces, and EV infrastructure. The competitive environment is marked by consolidation among major players and partnerships with consumer device makers to embed optimized charging systems. These dynamics collectively position the Wall Charger Market for continued transformation focused on speed, safety, sustainability, and smart capabilities.

Advances in GaN (Gallium Nitride) components and multi‑port configurations are accelerating product performance capabilities. GaN-based wall chargers now deliver higher power density with reduced thermal footprint, enabling units rated above 100 W in compact form factors. Manufacturers report up to 40 % reductions in charger size and weight, while multi‑port units supporting simultaneous high‑wattage charging for up to four devices have seen 35 % increased adoption among professionals and tech enthusiasts. This driver elevates user experience, supports expanding device portfolios, and lowers logistic and packaging costs—enhancing market competitiveness and value proposition in the Wall Charger Market.

A significant restraint in the Wall Charger Market is the energy inefficiency associated with idle power dissipation. Industry analysis shows that many low-cost chargers waste 10–15 % of input power in idle mode, contributing to unnecessary electricity consumption. In highly regulated regions, tightening energy efficiency standards and requirements for low‑power standby modes increase design complexity and compliance costs. Legacy charger lines lacking intelligent standby control are increasingly de‑prioritized, forcing manufacturers to redesign products or face regulatory pushbacks. This challenge raises packaging and component cost burdens and slows adoption of less‐efficient legacy units across markets.

There's a growing opportunity within the Wall Charger Market for smart, connected chargers that support app‑based monitoring, over‑the‑air firmware updates, and dynamic power allocation based on user behavior. Smart models captured over 65 % of revenue in adjacent EV charging devices in 2024, suggesting strong consumer appetite. Integrating Wi‑Fi, Bluetooth, and over‑current protection in residential and commercial wall chargers enhances utility and user engagement. Additionally, enterprise clients are evaluating networked charging stations for office buildings and hotels, presenting a new vertical segment. Emerging IoT-linked functionality and predictive diagnostics further expand horizons—creating white-label partnership opportunities with device OEMs and smart home platforms.

Meeting diverse global standards—including UL, CE, IEC, and newer USB‑C mandates—imposes significant certification demands on manufacturers in the Wall Charger Market. Designed products must pass thermal safety, EMI/EMC, efficiency, and interoperability tests; compliance to EU’s USB‑C mandates for smartphones and tablets, effective from late 2024, required rapid product reengineering. Navigating varied national and regional regulations increases testing cycles and time‑to‑market. Certification delays can stall product rollouts by several months, adding inventory carrying costs. Smaller players and new entrants may struggle to absorb these costs, limiting innovation diffusion and increasing reliance on established, certified manufacturers.

Expansion of GaN‑based Compact Fast Chargers: GaN semiconductor technology use has surged, enabling high‑wattage wall chargers (up to 100 W) in compact enclosures. Manufacturers report product volume increases of over 30 % in GaN models during 2024, particularly in multi‑port variant offerings. This shift is reshaping consumer expectations regarding form factor and charging speed.

Surge in Multi‑Port and Smart Charger Adoption: Multi‑port designs capable of charging multiple devices simultaneously grew by approximately 27 % in new product launches in early 2025. These units often incorporate AI‑based load balancing, optimizing current per port and improving efficiency in office and consumer use cases.

Integration of Smart Connectivity Features: Chargers featuring Wi‑Fi and Bluetooth connectivity with mobile app control now represent around 65 % of new product introductions. These allow firmware updates, usage monitoring, and remote diagnostics—adding value in residential and commercial segments.

Shift Toward Modular Construction and Installation: The adoption of modular mounting solutions—such as prefabricated wall charger enclosures and plug‑and‑play mounting kits—is increasing, especially in Europe and North America. Builders and facility managers are specifying high‑precision prefabricated charger housings, reducing labor and onsite installation time by up to 25 %, aligning with construction automation trends.

The Wall Charger Market is segmented across three critical dimensions: type, application, and end-user. Each segment reveals unique usage patterns, innovation focuses, and emerging demand drivers. In terms of type, wall chargers range from traditional USB-A models to advanced GaN-based and multi-port USB-C chargers, catering to varied voltage and power needs. Applications span consumer electronics, electric mobility, industrial systems, and IoT environments, with usage shaped by device compatibility and power density requirements. End-users include residential, commercial, and industrial sectors, each adopting wall chargers for tailored energy solutions. The diversification in device ecosystems, growing preference for fast and intelligent charging, and regional infrastructure developments all influence segment performance. Evolving customer expectations for safety, speed, and sustainability further steer innovation within each segment. This segmentation provides strategic clarity for stakeholders targeting market opportunities with differentiated product offerings and solutions aligned to sector-specific trends.

The Wall Charger Market offers several product types, including standard USB wall chargers, USB-C chargers, GaN (Gallium Nitride) chargers, wireless charging stations, and multi-port smart chargers. Among these, USB-C wall chargers are the leading type, owing to their universal compatibility, faster charging speeds, and integration with a wide array of modern devices including smartphones, tablets, and laptops. Their compact form factor and ability to deliver high wattage make them a top choice across consumer and professional domains.

The fastest-growing type is the GaN-based wall charger. GaN technology allows for higher energy efficiency, compact size, and better thermal management. Its adoption is accelerating as tech-savvy users and professionals seek high-performance charging solutions, particularly for multi-device setups. GaN chargers are gaining traction for their ability to deliver over 100W power in devices nearly half the size of traditional silicon-based models.

Other types, like standard USB-A wall chargers and wireless chargers, continue to serve niche segments. USB-A remains relevant in legacy device charging, while wireless wall chargers are favored for convenience in low-to-medium power environments, such as bedside or office desks, though they are currently limited by slower charging speeds and compatibility constraints. Each type holds strategic value depending on target usage scenarios and infrastructure compatibility.

Wall chargers are applied across several key domains, including smartphones, tablets, laptops, wearable devices, electric vehicles (for accessory charging), smart home systems, and industrial automation equipment. The smartphone application dominates the Wall Charger Market due to the sheer volume of mobile device usage globally and the increasing demand for fast, reliable daily charging solutions. USB-C PD and GaN-based fast-charging units have become standard accessories in this space.

The fastest-growing application is in the laptop and computing segment. With the rising prevalence of remote work, education digitization, and BYOD (Bring Your Own Device) trends, the demand for high-wattage chargers capable of supporting laptops and hybrid devices has surged. These applications require 60W–100W power delivery, favoring advanced charger types that ensure speed and safety.

Other applications, such as wearables and smart home devices, are also contributing to demand. While their individual power requirements are lower, their increasing proliferation in residential and professional settings supports steady charger consumption. Industrial applications, particularly in automation and sensor networks, require ruggedized wall chargers that offer reliability and constant uptime. As the use cases diversify, so does the design and deployment of wall chargers in each application vertical.

The Wall Charger Market is driven by three principal end-user segments: residential consumers, commercial facilities, and industrial environments. Residential users are the leading end-user group, primarily due to the widespread daily use of personal electronics including smartphones, tablets, laptops, and wearable devices. Convenience, speed, and aesthetic appeal are major decision factors in this segment, with consumers increasingly opting for compact, multi-port, and fast-charging models.

The fastest-growing end-user segment is the commercial sector, which includes offices, co-working spaces, airports, retail environments, and hospitality facilities. As digital device dependency grows in these spaces, there's a heightened demand for wall-mounted charging stations, embedded USB-C outlets, and networked smart charging hubs. Businesses are investing in solutions that enhance customer experience and employee productivity by ensuring access to reliable charging infrastructure.

Industrial end-users contribute by demanding robust, efficient wall chargers for powering devices like sensors, handheld scanners, and monitoring systems in logistics, manufacturing, and healthcare. These chargers must meet strict safety, durability, and uptime standards. The evolving landscape of end-user requirements underscores the market’s transition from basic functionality toward specialized, intelligent, and high-performance wall charging solutions tailored to each usage context.

Asia-Pacific accounted for the largest market share at 41.3% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.7% between 2025 and 2032.

The Wall Charger Market shows strong regional variation in adoption, driven by differences in consumer electronics usage, regulatory policies, manufacturing ecosystems, and technological readiness. Asia-Pacific dominates in volume and production capabilities, supported by dense consumer bases and large-scale industrial manufacturing in China, India, and Japan. Meanwhile, North America is accelerating in innovation and commercial deployment of smart wall charging infrastructure. Europe continues to prioritize eco-compliant product development, with USB-C mandates and stringent efficiency standards shaping product design. South America, though still emerging, shows potential due to increased consumer electronics penetration and energy reform efforts, particularly in Brazil and Argentina. In the Middle East & Africa, rising investments in infrastructure, construction, and energy diversification are expanding opportunities for wall charger deployment, especially in commercial and industrial verticals. These regional trends collectively define a diversified and opportunity-rich landscape for stakeholders in the Wall Charger Market.

North America held 25.6% of the global Wall Charger Market share in 2024, largely driven by high demand across commercial and residential sectors. Key industries fueling market expansion include consumer electronics, smart home systems, and enterprise technology solutions. Regulatory policies such as mandatory USB-C standardization and energy efficiency labeling are pushing manufacturers to enhance compliance and adopt greener technologies. U.S. government funding through infrastructure modernization programs is also stimulating demand for smart, connected charging solutions in public buildings, transportation hubs, and federal facilities. Additionally, widespread adoption of AI-enhanced chargers and advanced power management systems is accelerating digital transformation in the sector. The region is a pioneer in integrating wireless charging stations and USB-C ports into furniture and commercial interiors, positioning North America as a technologically progressive and innovation-centric Wall Charger Market.

Europe accounted for 20.4% of the global Wall Charger Market in 2024, with Germany, the UK, and France leading in adoption. The region’s market is shaped by aggressive sustainability mandates, including universal USB-C implementation and e-waste reduction frameworks. Regulatory bodies such as the European Commission continue to set rigorous energy performance benchmarks, influencing product design and manufacturing approaches. Smart chargers integrated with over-voltage protection, sleep modes, and recyclable materials are gaining traction. Emerging technologies like GaN-powered units and wireless charging pads are being rapidly adopted in both consumer and professional environments. Local manufacturing hubs and R&D centers are focused on eco-conscious innovation, driving Europe's reputation as a green-tech leader in the Wall Charger Market.

The Asia-Pacific region contributed the highest volume share of 41.3% in the Wall Charger Market in 2024, led by powerhouse economies such as China, India, and Japan. China continues to dominate production, with significant investments in GaN technology, high-speed assembly lines, and automated testing infrastructure. India’s rising smartphone penetration and government-backed digital inclusion programs are fueling domestic demand. Japan is at the forefront of integrating compact, multi-device chargers into smart home and mobility solutions. The region is a hub for charger design optimization, including heat dissipation systems and miniaturization strategies. Rapid urbanization and 5G expansion further amplify demand for high-performance, fast-charging devices, consolidating Asia-Pacific’s leadership in both consumption and innovation.

South America’s Wall Charger Market is gaining traction, particularly in Brazil and Argentina, which collectively held approximately 6.1% of the global market share in 2024. With expanding access to electricity and increased smartphone adoption, the demand for wall chargers is rising steadily. Public and private sector investments in digital connectivity infrastructure are fueling the growth of residential and commercial charging installations. In Brazil, smart city initiatives are promoting the use of energy-efficient chargers integrated into new housing and municipal developments. Trade liberalization policies are encouraging imports of advanced charging technologies. While domestic production is still limited, there’s growing focus on partnerships with Asian suppliers and regional distribution networks to meet rising demand.

The Middle East & Africa region contributed approximately 6.6% to the global Wall Charger Market in 2024, with notable growth concentrated in the UAE, Saudi Arabia, and South Africa. Demand is being driven by expanding urban development, particularly in commercial and hospitality sectors. The region’s construction boom includes integrated digital infrastructure, with wall chargers being installed as standard components in offices, malls, and luxury residential complexes. Government-backed smart city programs are creating demand for connected and AI-enabled charging devices. Technological modernization across telecom, education, and healthcare sectors is further enhancing market appeal. Local regulations are increasingly aligning with international standards for electrical safety and energy efficiency, promoting adoption of globally certified wall charging solutions.

China – 31.5% Market Share

High production capacity, technological scale, and vertical integration across electronics manufacturing.

United States – 18.2% Market Share

Strong end-user demand driven by commercial installations, innovation in smart charger solutions, and digital infrastructure expansion.

The Wall Charger Market is highly competitive, featuring over 150 active manufacturers and suppliers operating across regional and global levels. The competitive environment is defined by rapid product innovation, brand positioning, and diversification of charger designs tailored for varied voltage outputs, port types, and user applications. Leading players consistently introduce next-generation chargers with integrated features such as GaN technology, overcurrent protection, and smart chipsets to enhance safety and charging efficiency. Strategic initiatives like mergers, partnerships with tech giants, and R&D collaborations are key tactics employed by market leaders to strengthen their positions. In 2024, multiple companies expanded their product lines to include fast-charging and multi-port USB-C wall chargers in response to growing demand from both consumer electronics and enterprise sectors. Market participants are also investing in sustainable manufacturing, with biodegradable materials and recyclable packaging becoming a differentiator. This highly dynamic landscape reflects a strong emphasis on digital compatibility, miniaturization, and global certification compliance, intensifying the competition in both developed and emerging markets.

Anker Innovations Technology Co., Ltd.

Belkin International, Inc.

AUKEY Technology Co., Ltd.

Baseus Technology Co., Ltd.

Samsung Electronics Co., Ltd.

Xiaomi Corporation

RavPower

Ugreen Group Limited

AmazonBasics

Spigen Inc.

Shenzhen Mcdodo Industrial Co., Ltd.

Mophie Inc.

Technological innovation is playing a pivotal role in shaping the Wall Charger Market, with key advances aimed at faster charging, safety, compatibility, and sustainability. GaN (Gallium Nitride) technology has emerged as a transformative force, enabling the development of compact chargers with higher power efficiency and reduced heat output. These GaN-based chargers are capable of delivering up to 100W+ in smaller form factors, making them ideal for charging laptops, smartphones, and tablets simultaneously.

The shift to universal USB-C connectivity is accelerating, driven by both regulatory mandates and consumer demand. This standard supports Power Delivery (PD) protocols, allowing dynamic voltage adjustments and fast charging across multiple devices. Additionally, multi-port wall chargers, often combining USB-A and USB-C outputs, are gaining traction among professionals and travelers for convenience.

Smart features such as over-voltage protection, temperature sensors, and AI-powered current regulation have become standard in high-end models. Wireless wall-mounted chargers, though still a niche, are emerging with integrated Qi technology and magnet-assisted alignment, catering to premium device users.

There is also rising interest in eco-friendly technologies, such as chargers made from recycled plastics and biodegradable packaging. Manufacturers are adopting RoHS and Energy Star standards to enhance environmental compliance and marketability, particularly in Europe and North America.

In February 2024, Anker launched its Nano II 100W GaN charger with upgraded power allocation, enabling simultaneous charging of laptops and smartphones through dual USB-C ports in a pocket-sized form.

In May 2024, Belkin unveiled a new range of wall chargers featuring integrated over-temperature protection and support for USB PD 3.1, enabling ultra-fast charging of newer Apple and Android devices.

In October 2023, AUKEY introduced a 4-port 120W wall charger using the latest GaNFast™ chips, offering enhanced thermal management and 30% reduction in size compared to previous models.

In December 2023, Xiaomi revealed its next-generation wall charger with AI-powered power delivery adjustment, supporting adaptive charging based on device battery health and type.

The Wall Charger Market Report comprehensively analyzes key market dynamics across various verticals, offering a detailed exploration of the product, regional, application, technology, and end-user segments. The scope of the report covers diverse product types including single-port chargers, multi-port chargers, GaN-based chargers, and fast-charging solutions. It includes market assessments of major applications such as residential usage, commercial deployment in offices and airports, and specialized applications in healthcare and industrial automation.

Geographically, the report provides insights across five primary regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—with country-level analysis for major markets such as the United States, China, Germany, India, and Brazil. The technology section delves into innovations like GaN, USB-C PD standards, and AI-powered charging systems, examining their integration in mainstream products and upcoming solutions.

The end-user segmentation spans both individual consumers and businesses, with a focus on demand patterns in sectors such as IT, consumer electronics, hospitality, and public infrastructure. The report also highlights emerging market opportunities in wireless wall chargers, biodegradable charger housings, and smart grid-integrated solutions. Collectively, the report serves as a strategic tool for decision-makers, offering actionable intelligence and forward-looking insights into the Wall Charger Market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 550.0 Million |

| Market Revenue (2032) | USD 876.6 Million |

| CAGR (2025–2032) | 6.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Technological Insights, Segment Analysis, Regional and Country-Wise Analysis, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Anker Innovations Technology Co., Ltd., Belkin International, Inc., AUKEY Technology Co., Ltd., Baseus Technology Co., Ltd., Samsung Electronics Co., Ltd., Xiaomi Corporation, RavPower, Ugreen Group Limited, AmazonBasics, Spigen Inc., Shenzhen Mcdodo Industrial Co., Ltd., Mophie Inc. |

| Customization & Pricing | Available on request (10% Customization is Free) |