Reports

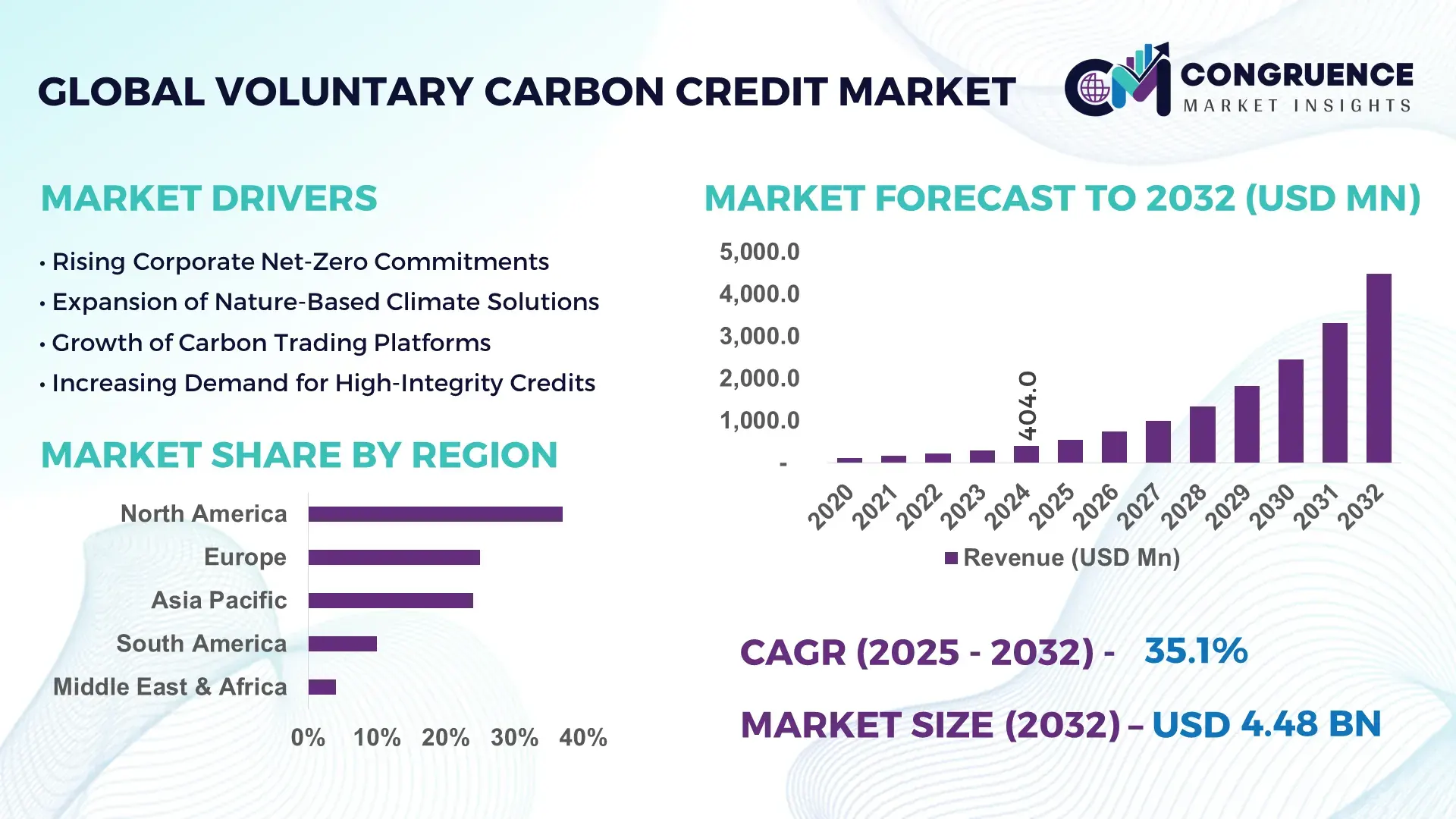

The Global Voluntary Carbon Credit Market was valued at USD 404.0 Million in 2024 and is anticipated to reach a value of USD 4,483.6 Million by 2032 expanding at a CAGR of 35.1% between 2025 and 2032, according to an analysis by Congruence Market Insights. This surge is driven by rapidly expanding corporate net-zero commitments and accelerated demand for high-integrity removal and nature-based credits.

The United States is the dominant market for voluntary carbon credits in terms of buyer demand and market activity. The U.S. shows broad corporate participation across energy, tech, and finance sectors, with hundreds of large corporate purchasers and trading platforms supporting primary and secondary market activity; North America’s voluntary market infrastructure includes thousands of corporate buyers, exchange platforms, and registries that together facilitate large-scale procurement and trading. The U.S. registered institutional initiatives and market mechanisms supporting project financing and carbon procurement, with reported deployment of purchase commitments and platform listings numbering in the hundreds across 2023–2024.

Market Size & Growth: USD 404.0 Million (2024) → USD 4,483.6 Million (2032), CAGR 35.1% — driven by corporate net-zero procurement and demand for removals.

Top Growth Drivers: Corporate procurement adoption 42%; investor allocation to nature-based projects 28%; demand for removals 30%.

Short-Term Forecast: By 2028, primary market liquidity expected to improve, reducing project time-to-market by ~18% via streamlined verification and digitized registries.

Emerging Technologies: Tokenized credit registries, remote sensing + satellite MRV, and direct-air capture (DAC) integration.

Regional Leaders: North America ~USD 1,600M (2032) — high corporate demand; Latin America ~USD 1,200M — strong project supply; Asia-Pacific ~USD 900M — rapid buyer adoption.

Consumer/End-User Trends: Large enterprises and financial institutions lead purchases; SMEs and product-level offsetting pilots are rising.

Pilot or Case Example: 2024 pilot of remote-sensing MRV reduced verification cycle time by 24% and improved sampling coverage by 38%.

Competitive Landscape: Market leader (platform/registry) ~25% share, followed by 3–5 major registries, broker-dealers, and project developers.

Regulatory & ESG Impact: Strengthening integrity initiatives, registry standards, and corporate disclosure requirements are driving demand for high-quality credits.

Investment & Funding Patterns: Billions committed to project pipelines and technology platforms in 2023–2024, with blended finance and pay-for-performance structures scaling.

Innovation & Future Outlook: Growth of removal credits, nature-based verification tech, and interoperability between voluntary registries will define next-generation market architecture.

Sector demand is shifting toward nature-based and engineered removal credits; forestry and land-use supply remains significant while DAC and soil carbon pilots scale. Technological innovations (satellite MRV, blockchain registries) and new financing models (results-based payments, pre-purchase financing) are accelerating liquidity and enabling faster capital flows into high-integrity projects.

The voluntary carbon credit market sits at the intersection of corporate climate strategy, project finance for mitigation/removal, and emerging market infrastructure. Strategically, the market enables companies to operationalize interim decarbonization pathways while internal abatement continues. From a measurable perspective, corporate net-zero commitments declared through 2023–2024 have translated into multi-year purchase pledges that underpin forward offtake finance for projects; improved primary-market mechanisms and blended finance instruments have shortened project financing cycles by an estimated 15–25% in pilot jurisdictions.

Technology is a key lever: remote-sensing MRV and automated verification pipelines deliver X% improvements in monitoring coverage compared to ground-only measurement (remote sensing can increase spatial monitoring coverage by 30–50% versus sample-based ground surveys), while tokenized registries reduce reconciliation time by up to 40% in platform pilots. Regionally, North America dominates in buyer volume, while Latin America leads in project supply and issuance, reflecting a separation of demand (buyers) and supply (project host countries). By 2027, integration of satellite MRV and automated registry reconciliation is expected to cut verification lead times by ~20%, enabling faster issuance and reducing working capital requirements for developers.

Compliance and ESG dimensions are reshaping behaviors: corporates are committing to improved disclosure and to prioritizing credits that meet strict integrity criteria (e.g., permanence guarantees, robust baselines). Micro-scenarios demonstrate operational impact: in 2024, a multinational buyer structured pre-purchase financing that reduced developer capital costs by 18%, enabling an accelerated build-out of reforestation projects. Looking forward, the voluntary market will act as a complement to mandatory instruments, providing resilience and innovative financing for nature-based and technology-enabled removals while maturing governance, comparability, and integrity standards that align voluntary supply with corporate and societal climate goals.

The Voluntary Carbon Credit Market is characterized by a dynamic interplay between supply-side project development (forestry, agriculture, renewable energy, methane avoidance, carbon removal) and demand-side corporate procurement and investor activity. Key influences include evolving integrity standards and registry interoperability, prices that reflect project vintage and methodology quality, and regulatory signals that affect demand composition (e.g., preference for removals). Market liquidity is shaped by broker activity, exchange platforms, and corporate forward-purchase commitments; project pipelines are affected by financing access, MRV innovation, and host-country permitting. As verification technologies improve and standards converge, the market’s ability to scale high-integrity credits and reduce issuance lead times will be a principal determinant of long-term viability and corporate uptake.

Corporate net-zero pledges and expanded sustainability procurement programs have materially increased demand for voluntary credits. Large enterprises across energy, technology, finance, and consumer goods sectors have announced multi-year offtake commitments, leading to predictable forward demand that supports project financing. For example, buyer commitments and corporate procurement pilots in 2023–2024 have allowed project developers to secure pre-finance, reducing time-to-construction and accelerating issuance pipelines. Institutional investors are also allocating capital toward carbon-finance vehicles, and new procurement models (e.g., pay-for-performance and blended public-private deals) further underpin demand. The resulting effect is professionalization of the market, increased participation by financial intermediaries, and growing appetite for high-integrity removal credits.

Lack of universally accepted standards and concerns about additionality, permanence, and double counting constrain buyer confidence and slow purchase decisions. Heterogeneous methodologies across registries and discrepancies in MRV practices create pricing dispersion and liquidity fragmentation. Developers face higher transaction costs and longer timelines when aligning projects to multiple registries or enhanced verification protocols. Market participants also report governance uncertainty when national policy signals change (e.g., when host countries revise accounting rules), which can deter long-term investment or delay issuances. These structural frictions increase working capital needs for developers and create buyer hesitancy for large-scale, long-dated offtake commitments.

Improving MRV automation (satellite imagery, AI-driven analytics) and building interoperable, digital registries create an opportunity to scale credits faster and at lower cost. Automated MRV can expand monitoring coverage and reduce field verification frequency while increasing transparency—pilots indicate potential reductions in verification costs and issuance lead times. Interoperable registries and standardized metadata schemas can simplify cross-platform reconciliation, enhance buyer confidence, and enable novel financial instruments (e.g., tradable forward contracts, yield-bearing carbon investment products). These innovations can unlock capital for early-stage project developers and permit the market to scale high-integrity removals alongside nature-based supply.

Project developers in many regions face high upfront costs for validation, monitoring equipment, and community engagement—expenses that can consume a large share of early-stage capital. Limited access to concessional finance and the complexity of pay-for-performance arrangements increase developers’ financing risk. Additionally, fragmentation of demand—many small buyers vs. a few large offtakers—creates mismatch in contract size and tenor. These financial and structural challenges slow project pipeline maturation, especially for emerging removal technologies that require significant capex before credits can be issued and monetized.

Expansion of high-integrity removals and engineered solutions: Demand for engineered removal credits (e.g., DAC, enhanced weathering) rose in 2023–2024, with project pipelines and pre-purchase commitments growing by double digits in many portfolios. Removal pilots and early commercial DAC facilities reported increasing offtake interest and investment commitments, signaling a measurable shift in buyer preferences toward permanent sinks and engineered solutions.

MRV modernization using remote sensing and AI: Adoption of satellite-based MRV and AI analytics increased coverage and cadence of verification—pilot programs reported monitoring coverage improvements of 30–50% and potential reductions in ground-field costs. These tools improve detection of leakage and baseline drift and support higher confidence in vintage tracking and outcomes reporting.

Registry interoperability and marketplace innovation: Market infrastructure evolved with new registry features (API synchronization, tokenized credits) and marketplace platforms offering standardized metadata and escrow services; early pilots reduced reconciliation time by ~25–40%, improving secondary market liquidity and enabling faster settlement.

Shift in supply geography and buyer behavior: Supply remained concentrated in select tropical and temperate countries for nature-based credits while buyer demand consolidated in developed markets; project diversification and blended finance models expanded access in previously underserved regions, increasing the number of verified projects and host-country participants.

The Voluntary Carbon Credit Market is segmented by Type, Application, and End-user, each reflecting distinct supply-chain, verification, and procurement dynamics. By Type covers forestry & land-use (afforestation/reforestation, IFM, REDD+), renewable-energy and fuel-switching avoidance credits, methane and waste-capture projects, household/community devices, and engineered removals (DAC, BECCS, enhanced weathering). By Application includes corporate offsetting (supply-side offtake contracts and voluntary retirements), product-level carbon neutrality programs, aviation/transport pilots, and finance/investor portfolios (secondary trading, forward contracts). End-users range from large corporates and financial institutions to SMEs, airlines, and consumer-facing brands, plus public-sector purchasers and project developers acting as intermediaries. Key segmentation decisions hinge on verification needs, project duration, and procurement tenor: avoidance credits dominate supply pipelines, while removals are increasingly the strategic focus for buyers seeking permanence and durability.

Nature-based forestry & land-use credits remain the largest product type in the voluntary market, representing roughly ~49% of reported issuance/retirement volumes in recent reporting—driven by longstanding project pipelines in tropical and temperate regions and large-scale afforestation, reforestation, and improved-forest-management (IFM) programs. Renewable-energy and avoidance credits (including cookstoves and household/community devices) constitute another major block of supply and are commonly used for near-term corporate offsetting needs. Engineered removals (DAC, BECCS, mineralization) are the fastest-growing product class as buyers seek durable sinks; direct-air-capture related markets have been modelled with very high projected growth rates (industry reports show DAC markets with mid-to-high-double-digit projected CAGRs in forecast windows), reflecting growing investment and pre-purchase programmes. Other niche types—blue-carbon, soil carbon, and agroforestry—together make up the remaining share (approx. ~15–25% combined), serving regional and co-benefit priorities (biodiversity, local livelihoods).

Corporate voluntary procurement dominates demand-side applications: general corporate offsetting and supply-chain/product neutrality initiatives account for the largest application use, driven by multi-year offtake commitments, product-level offset programmes, and investor ESG mandates. Aviation and transport programmes (including CORSIA-related pilots and voluntary airline retirements) are visible but represent a smaller share of total retirements. Financial instruments (secondary trading, structured forward contracts, and pre-purchase financing) are expanding as market infrastructure professionalizes. Consumer/brand programmes (product-level carbon neutrality and retail offset options) are growing as brands integrate traceable credits into product claims. In 2024, despite a marked decline in transaction volumes, retirements held relatively steady — indicating corporate end-use demand for credits continued even as trading liquidity contracted. Consumer adoption trends show increasing anonymous retirements and selective purchasing for high-integrity removal credits; many buyers now prioritize permanence and co-benefits when procuring credits. Consumer/Adoption statistics: In 2024 transaction volumes fell by ~25% from 2023 while retirements remained elevated (retirements in the 160–190 million credit range), showing a steady base of corporate end-use despite lower secondary trading.

Large corporates and financial institutions are the leading end-users, representing the majority of voluntary credit retirements through purchase programmes, multi-year offtake contracts, and investor-led funds. Corporates in energy, technology, consumer goods, and finance are consistently the largest buyers, using credits for portfolio-level pledges, product neutrality, and interim compensation for residual emissions. SMEs and brands are increasingly entering the market via bundled offset products and marketplace platforms, while airlines and transport operators remain important niche purchasers for route-specific offsets. Project developers and intermediaries (brokers, registries, and exchanges) are also active end-users in the secondary market, holding credits for resale or structured financing. Industry adoption metrics show a significant portion of retirements are either disclosed corporate buys or anonymous retirements executed via intermediaries; buyer behavior shifted in 2024 toward prioritizing high-integrity removals and forestry projects with verifiable co-benefits. The combined share of non-corporate end-users (SMEs, NGOs, community buyers) constitutes a smaller but growing segment (approx. ~20–30% of retirements when including household/community devices and local initiatives).

North America accounted for the largest market share at 37% in 2024 however, it is expected to register the fastest growth, expanding at a CAGR of 35.1% between 2025 and 2032.

In 2024 this translated to an approximate issuance-and-retirement activity footprint reflecting tens of millions of credits transacted and hundreds of active corporate buyers and intermediaries across exchanges and registries. North America reported roughly 160–190 million credits retired globally in 2024 (total retirements range), supported by 700+ corporate purchase programmes, 400+ registered project developers, and dozens of trading platforms and retail marketplaces. By project type, forestry & land-use projects accounted for a large share of retired volumes (high-volume vintages), while renewable-avoidance projects and household/technology projects comprised the next largest issuance blocks. Market infrastructure indicators include high registry penetration (multiple registries synchronizing API access), significant forward-offtake commitments (multi-year contracts numbering in the hundreds), and strong secondary market liquidity in select vintages — all pointing to concentrated buyer demand, structured offtake pipelines, and active issuance pipelines in 2024.

North America held about 37% of the voluntary carbon credit market in 2024 and recorded large volumes of both issuance and retirements. Market activity is concentrated in the United States, which accounts for the majority of regional retirements and corporate offtake. Key industries driving demand include technology, finance, consumer goods, and aviation—together responsible for a substantial portion of corporate purchase commitments (hundreds of multi-year contracts). Notable regulatory and policy dynamics include enhanced disclosure expectations, voluntary programme alignments with federal and state-level climate initiatives, and increased scrutiny of credit integrity — prompting buyers to favor higher-quality, verified credits. Technological trends center on improved MRV (satellite and AI analytics), tokenized registry features, and automated registry reconciliation; uptake of these tools in North America is high relative to other regions. A local example: large registry and trading platforms expanded digital registry features and API connectivity in 2023–2024 to support faster reconciliation and escrow services for corporate buyers. Regional consumer behavior shows higher enterprise adoption in healthcare, finance, and tech, plus significant interest from financial institutions structuring carbon-focused investment vehicles.

Europe accounted for roughly 25% of the global voluntary carbon credit activity in 2024, with major national markets including Germany, the UK, and France collectively representing the lion’s share of European purchases and retirements. Key sectors driving demand include energy, manufacturing, and consumer brands that integrate product-level neutralization programmes. Regulatory momentum — stronger corporate disclosure standards, supply-chain due diligence, and national climate strategies — has increased demand for traceable, high-integrity credits and spurred adoption of sustainability verification tools in ~30–40% of large firms. Technology adoption emphasizes explainable MRV, independent verification, and metadata transparency; several European registries and platforms rolled out enhanced traceability features to support cross-border procurement. A notable regional example: a European project developer scaled on-the-ground verification teams and launched satellite-backed MRV pilots to accelerate issuance timelines. Consumer behavior in Europe leans toward conservative, compliance-aware purchasing and preference for credits with clear co-benefits (biodiversity, community outcomes).

Asia-Pacific accounted for about 24% of global voluntary carbon credit activity in 2024, with top consuming countries including China, India, and Japan. The region shows large and growing corporate interest—particularly among technology, manufacturing, and export-oriented firms—though buyer sophistication varies by country. Infrastructure and project trends include an expanding pipeline of renewable-avoidance and landfill/methane capture projects, rising issuance in community energy-efficiency programmes, and increased participation by regional project developers expanding supply capacity. Tech and innovation hubs in East and South Asia have piloted remote-sensing MRV, and several regional registries introduced enhanced digital features in 2023–2024 to support buyer-seller matching and pre-purchase financing. A regional example: a large Asia-based developer scaled community-based clean-cookstove projects and integrated digital verification tools to improve reporting cadence. Consumer behavior varies: urban corporate buyers show high acceptance of digital registry products, while smaller domestic buyers are price-sensitive and favor bundled project offerings.

South America delivered significant project supply in 2024 and accounted for roughly 10% of global voluntary carbon credit activity by conservative volume metrics, with Brazil and Argentina as primary contributors. The region remains a key supplier of forestry, REDD+, and land-use credits — large vintage pipelines, extensive forest estates, and high-volume issuance characterize South American supply. Infrastructure trends include increasing engagement with international buyers through long-term offtake agreements and growing use of blended finance to de-risk project development. Government incentives and regional trade policies in several countries eased export and certification pathways, enabling larger-scale project development; select subnational initiatives also aggregated credits for international markets. A South American developer example: a Brazil-based state programme packaged multi-year reforestation credits into sovereign-backed offers to attract institutional purchasers. Regional consumer behavior leans toward supply-side development and project co-benefit communication (biodiversity, social outcomes) to appeal to international buyers.

Middle East & Africa represented about 4% of voluntary carbon market activity in 2024, with notable pockets in the UAE, South Africa, and selected North African nations. Regional demand is influenced by oil & gas transition planning, infrastructure investments, and sovereign or corporate decarbonization commitments in Gulf states. Supply-side activity includes methane capture, renewable energy, and nascent nature-based projects; several countries invested in registry-readiness and MRV capacity-building through partnerships and donor-funded programmes. Technological modernization efforts—telemetry for monitoring, tele-radiology-like remote MRV pilots, and digital registry integration—have been funded as part of capacity-building initiatives. Example regional activity: a logistics node and cold-chain for registry operations was established in a Gulf hub to facilitate export of verified avoidance/removal credits. Consumer behavior varies widely: GCC corporate buyers show early adoption and willingness to pre-purchase credits, while many African markets focus on developing project pipelines and institutional capacity before large-scale corporate procurement.

United States — 34% Market Share: The United States dominates buyer activity with high numbers of corporate offtake commitments, advanced trading infrastructure, and a large concentration of institutional purchasers and registries in the country.

Brazil — 12% Market Share: Brazil leads as a major project-supplier country with extensive forest and land-use project pipelines, large-area conservation initiatives, and state-level programmes aggregating credits for international buyers.

The Voluntary Carbon Credit Market features a diverse competitive set spanning registries, project developers, data/ratings firms, exchanges, and advisory platforms. Industry players number in the low hundreds globally (project developers, brokers, platforms and registries combined), with roughly 20–40 organizations operating at significant international scale and many dozens of regional specialists. Market positioning splits into (a) registry/standards providers that enable issuance and tenure management; (b) large project developers and aggregators that supply forestry, avoidance and removal credits; (c) data & rating specialists that provide project-level quality scores; and (d) trading platforms and broker-dealers that enable primary and secondary market liquidity.

Strategic initiatives in 2023–2024 included major equity rounds and capacity investments, registry rule updates and digital tool rollouts, and new regional hubs to scale project origination. Innovation trends accelerating competition are remote-sensing MRV, AI-driven project analytics, registry API/tokenization for faster reconciliation, and the emergence of engineered-removal project portfolios. The top-tier is moderately consolidated: the combined share of the top 5 companies and registries is estimated at ~45–60% of professional market flows (issuance, corporate offtakes, platform-traded volumes), while the remainder is fragmented among niche and regional providers. Key competition metrics: dozens of strategic partnerships announced in 2023–24 between data firms and registries, multiple platform feature launches to support escrow and forward contracts, and increased M&A/partnership activity as incumbents secure origination pipelines and MRV capabilities. For decision-makers, this means dominant players control scale and liquidity while specialized firms drive quality, verification, and technology differentiation.

Verra

Gold Standard

Climate Impact X

NCX (formerly SilviaTerra)

Natural Capital Partners

Carbon Direct

Technology is a primary enabler for scaling quality, transparency, and liquidity in the voluntary market. Remote sensing (satellite imagery, LiDAR, UAVs) combined with machine-learning analytics now delivers more frequent spatial monitoring, enabling project developers and verifiers to move from periodic field sampling to near-continuous monitoring. Pilots show remote sensing can increase spatial coverage by tens of percent compared with ground-only sampling and materially reduce field verification cost and time. Automated MRV pipelines ingest satellite feeds, apply change-detection and biomass-estimation models, and produce standardized metrics used in issuance workflows.

Registry modernization and digital interoperability are accelerating: registries increasingly offer APIs, standardized metadata, and tokenization pilots to speed reconciliation between issuer, buyer, and secondary-market systems. Tokenized credits, when paired with robust metadata and custodial escrow, can reduce settlement friction and enable programmable forward contracts and delivery-linked financing. Blockchain-like ledgers are being trialed to provide immutable transaction trails and reduce double-counting risk while retaining off-chain verification outputs.

On the removal side, engineered technologies (direct air capture, mineralization, biochar, BECCS) are moving from pilot to early commercial deployment. These technologies bring high capital intensity and require advanced measurement systems (continuous CO₂ monitoring, site-level permanence verification) plus long-term stewardship mechanisms. Tech-enabled finance is emerging—pre-purchase contracts and results-based payments are being coupled with digital MRV triggers that release tranche payments upon verified outcomes.

Data and analytics firms now provide standardized scoring, vintage risk assessments, and co-benefit quantification (biodiversity, social impact) to help buyers compare credit vintages and project integrity. The integration of these scoring systems into procurement platforms reduces due-diligence timelines. Finally, hybrid solutions that combine nature-based projects with technology-enabled MRV and blended finance structures (mixing grant, concessional debt, and commercial offtake) are proving effective at de-risking early-stage projects and accelerating issuance pipelines.

For executives, the tech takeaway is clear: investments in MRV automation, registry interoperability, and robust data governance materially reduce issuance lead times, increase buyer confidence, and enable more sophisticated financial instruments that improve project bankability.

(April 3, 2024), Pachama secured a purchase from Shopify’s Sustainability Fund to reforest ~200 hectares in Brazil’s Atlantic Forest; the project is expected to remove ~45,000 tonnes CO₂ over 17 years and supports local restoration and monitoring investments. Source: www.pachama.com

(April 25, 2024), South Pole announced completion of an investment round with participation from major shareholders (including GenZero/Temasek affiliates) to scale project origination, finance-first-of-a-kind assets and deepen regional operations. Source: www.southpole.com

(effective Jan 1, 2024), Verra published updated AFOLU non-permanence risk tool requirements and related clarifications requiring new reporting procedures for relevant land-use projects to standardize risk assessment and non-permanence accounting. Source: www.verra.org

(May 2024), Sylvera rolled out a procurement-focused Project Catalog and Screening feature that aggregates registry data and ratings to help buyers shortlist and compare projects more rapidly, reducing sourcing time and standardizing screening metrics. Source: www.sylvera.com

The report covers the global voluntary carbon credit ecosystem across project types (forestry & land-use, blue carbon, agriculture & soil carbon, renewable-energy avoidance, methane & waste capture, community energy-efficiency, and engineered removals such as DAC, BECCS, and mineralization), issuance and retirement processes, and registry standards and program rules. It examines demand-side segmentation—corporate procurement (portfolio-level and product-level neutrality), financial instruments (secondary trading, forward and structured contracts), consumer-facing retirement programs, and public-sector/NGO buyers. The geographic lens spans North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level observations for key markets, host-country project pipelines, and regional infrastructure indicators (registry adoption, MRV capacity, and buyer concentration metrics).

Technology and operational focus areas include MRV systems (satellite, aerial, and ground sensors), registry digitization (API/tokenization pilots and metadata standards), data & rating platforms (quality scoring, vintage risk analysis), and finance mechanisms (pre-purchase contracts, blended finance, and pay-for-performance structures). The report assesses stakeholder roles—registries, developers, brokers, exchanges, data/rating providers, financial intermediaries—and maps go-to-market strategies, procurement workflows, and contract templates.

Coverage also includes risk and governance dimensions: permanence and reversal risk management, additionality testing, leakage accounting, co-benefit verification, legal and contracting frameworks, and the evolving landscape of voluntary vs. compliance interactions. Niche topics examined are bundled carbon+co-benefit products, corporate supply-chain traceability pilots, sovereign aggregation vehicles, and early commercial deployments of engineered removals. Designed for corporate sustainability leads, investors, project developers, and policy teams, the report delivers actionable insights for sourcing strategy, project selection, technology investments, registry engagement, and structuring finance to scale verified mitigation and removal supply.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 404.0 Million |

| Market Revenue (2032) | USD 4,483.6 Million |

| CAGR (2025–2032) | 35.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, End-User Behavior Analysis, Regulatory & Integrity Standards Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Pachama, South Pole, Sylvera, Verra, Gold Standard, Climate Impact X, NCX (formerly SilviaTerra), Natural Capital Partners, Carbon Direct |

| Customization & Pricing | Available on Request (10% Customization Free) |