Reports

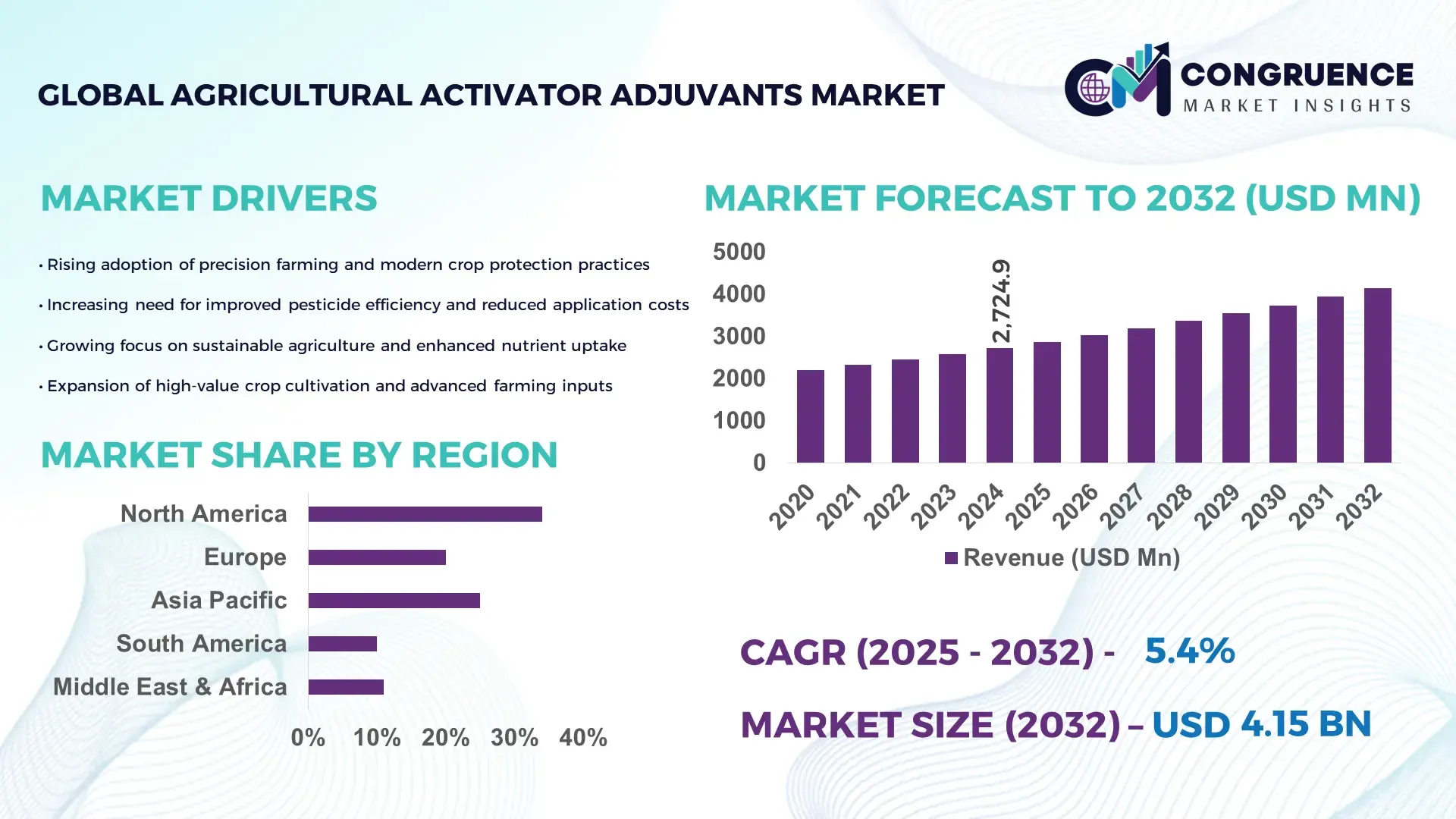

The Global Agricultural Activator Adjuvants Market was valued at USD 2724.85 Million in 2024 and is anticipated to reach a value of USD 4150.19 Million by 2032 expanding at a CAGR of 5.4% between 2025 and 2032. Growth is primarily driven by the increasing need for improved pesticide efficiency and enhanced nutrient uptake in precision farming.

The United States leads the Agricultural Activator Adjuvants market with a robust production ecosystem supported by high R&D spending exceeding USD 1.2 billion annually in advanced formulation technologies. The country has more than 165 manufacturing and blending facilities dedicated to agricultural adjuvants, with significant investments in non-ionic surfactants, organosilicone-based activators, and bio-based formulations. Adoption is highest across corn, soybean, and cotton cultivation, with over 76% of large farms integrating activator adjuvants for improving spray deposition and absorption efficiency. Continuous innovation in tank-mix compatibility and controlled-release delivery systems positions the U.S. as a pivotal hub for commercial product launches and export-focused production.

• Market Size & Growth: Reached USD 2724.85 Million in 2024 and projected to hit USD 4150.19 Million by 2032 at a 5.4% CAGR, driven by precision agriculture adoption and increased pesticide performance requirements.

• Top Growth Drivers: 68% adoption to improve agrochemical efficiency, 52% boost in foliar nutrient uptake, and 47% rise in use for weather-resilient farming practices.

• Short-Term Forecast: By 2028, average pesticide use efficiency expected to improve by 28% with a 15% reduction in overall crop protection cost.

• Emerging Technologies: Bio-based activators, nanocarrier-based surfactants, and AI-assisted dosage optimization in smart farming systems.

• Regional Leaders: North America projected at USD 1.35 Billion by 2032 with high precision agriculture use; Europe estimated at USD 1.02 Billion driven by sustainability compliance; Asia-Pacific expected at USD 1.18 Billion due to farm output maximization initiatives.

• Consumer/End-User Trends: Fastest uptake among commercial growers of cereals, oilseeds, and horticulture, with growing repeat purchase cycles for premium formulations.

• Pilot or Case Example: A 2024 field project in Brazil using organosilicone-based activators recorded 34% more spray retention and 21% yield improvement in soybean farms.

• Competitive Landscape: Market leader holds approx. 11% share, with other key players including BASF SE, Croda International Plc, Solvay SA, Evonik Industries AG, and Clariant AG.

• Regulatory & ESG Impact: Stricter residue-compliance frameworks and government backing for green chemistry formulations accelerating transition to low-toxicity activator adjuvants.

• Investment & Funding Patterns: Over USD 460 Million invested in new formulation manufacturing facilities and technology collaborations over the past two years, with increasing venture funding for sustainable input innovations.

• Innovation & Future Outlook: Advancements in controlled-release adjuvants, variable-rate spray systems, and biodegradable formulations expected to redefine product performance and adoption beyond 2032.

The Agricultural Activator Adjuvants market is significantly shaped by expanding use across cereals, oilseeds, fruits, and vegetable production, supported by the growing adoption of advanced crop protection programs. Surfactant-based and oil-based activator technologies continue to dominate product portfolios, with notable innovation in bio-derived and weather-resilient formulations aimed at reducing spray drift and enhancing leaf penetration. Regulatory policies promoting reduction of agrochemical inputs and greater sustainability in farming practices are influencing product development pipelines, particularly in Europe and North America. Asia-Pacific exhibits strong consumption growth due to intensive agricultural output strategies and rising acceptance of premium adjuvant blends among commercial farms. The sector is expected to advance toward data-driven, environmentally adaptive solutions, integrating precision farming equipment, smart application systems, and improved field performance analytics.

The strategic relevance of the Agricultural Activator Adjuvants Market lies in its ability to enhance the performance of crop protection chemicals and fertilizers, enabling producers to achieve higher yield outputs with reduced application volumes. The market is evolving toward advanced formulation science, in which organosilicone and bio-based activators are becoming central to precision agriculture. Nanocarrier-based adjuvant technology delivers 31% improvement in spray deposition efficiency compared to conventional non-ionic surfactants, driving measurable farm productivity outcomes. North America dominates in volume, while Europe leads in adoption with 72% of large-scale farms incorporating at least one activator adjuvant class across annual crop cycles. By 2027, AI-assisted tank-mix optimization and automated spray calibration systems are expected to cut droplet waste by 36% and improve leaf absorption by 29%. Regulatory priorities and ESG commitments are accelerating reformulation efforts, with leading firms committing to 40% reduction in petroleum-derived solvent content by 2030 and 50% minimum recyclable packaging utilization by 2029. In 2024, Brazil achieved a 22% reduction in herbicide application levels through AI-driven spray scheduling combined with organosilicone-based activator adoption. Moving forward, the Agricultural Activator Adjuvants Market is positioned as a pillar of resilience, compliance, and sustainable growth in global agribusiness, supporting both yield optimization and environmentally adaptive farming.

The increasing deployment of precision agriculture systems has significantly boosted the demand for Agricultural Activator Adjuvants, as farms seek to increase spray effectiveness and minimize agrochemical waste. More than 64% of GPS-enabled sprayer users have integrated activator adjuvants into crop protection routines to improve droplet uniformity and leaf penetration across variable plant canopies. Growing use of UAV-based spraying platforms also contributes to demand, as activators enhance deposition accuracy in low-volume aerial applications. Field trials indicate that optimized activator use in precision farming improves nutrient and pesticide uptake efficiency by 18–34% across major crops, reducing the need for repeat field passes. As farm operators continue to digitalize and monitor real-time crop health through sensors and mapping systems, adjuvants are being deployed as performance enhancers within data-driven spray protocols. Together, these elements are reshaping adoption patterns from optional inputs to integral components of advanced agriculture operations.

Environmental safety regulations and changing formulation compliance requirements remain key restraints for the Agricultural Activator Adjuvants Market. Stricter monitoring of chemical residues, groundwater protection, and toxicity profiles has increased development costs and lengthened approval timelines for several traditional activator ingredients, including petroleum distillate-based formulations. Manufacturers are required to meet evolving standards regarding biodegradability, ecotoxicity, and safe-handling certification, which has led to reformulation of multiple legacy products. In Europe alone, more than 120 adjuvant ingredients have undergone reassessment for compliance under updated agricultural chemical frameworks. These regulatory dynamics add uncertainty to product lifecycles, raising investment risk and reducing speed-to-market for new product launches. The necessity for global compliance alignment also increases cost burdens for firms operating in multiple jurisdictions, especially when requirements differ for the same ingredient across regions.

The transition toward environmentally adaptive and bio-based farming solutions offers significant opportunities for the Agricultural Activator Adjuvants Market. Demand for natural feedstocks—such as plant-derived surfactants and fermentation-based fatty acid esters—has surged as farms prioritize reduced toxicity and compatibility with organic agricultural practices. Over 41% of new R&D pipelines among leading suppliers focus on biodegradable activators suitable for regenerative and residue-limited farming programs. Growth is also being fueled by adoption in high-value crops such as fruits, vegetables, and plantation crops, where precision nutrition and improved foliar uptake are crucial for output quality. Governments in Asia-Pacific and Europe are incentivizing sustainable input innovation through funding schemes and certification programs, unlocking new market entry opportunities. As digital and sensor-enabled farming expands, high-performance bio-based activators designed for variable-rate application systems are expected to become a major commercial segment over the next decade.

High product costs and variable awareness levels—especially among small and medium-scale farmers—pose ongoing challenges to widespread adoption of Agricultural Activator Adjuvants. Many growers lack access to training and field evidence demonstrating the measurable benefits of adjuvant-assisted spray programs, resulting in lower uptake despite proven performance advantages. Pricing pressures further compound the challenge, as advanced organosilicone and nanocarrier-based activators typically cost 20–45% more than conventional adjuvants. Supply chain inconsistencies in developing markets—particularly limited retail availability, inadequate advisory services, and lower access to precision spraying equipment—continue to reduce product accessibility. In many regions, distributors and agronomists remain the primary source of information, making consistent knowledge transfer essential yet difficult to standardize. These barriers continue to create uneven adoption patterns despite strong long-term potential for high-input and export-focused farming systems.

• Rapid Shift Toward Bio-Derived and Low-Residue Formulations: The market is witnessing a measurable pivot toward plant-based and biodegradable activator adjuvants, driven by residue-reduction mandates and sustainability goals. More than 48% of new product launches in 2023–2024 contained fully bio-derived surfactant systems, compared with only 19% four years earlier. Demand is most notable in high-value crops, where users reported a 27% improvement in absorption efficiency and a 33% reduction in drift-related spray loss. Major manufacturers have increased investment into fermentation-based raw materials and solvent-free formulations to align with export-grade agricultural requirements.

• Integration of Precision Agriculture and Smart Application Systems: Digitalization is expanding the operational relevance of Agricultural Activator Adjuvants, particularly in UAV and GPS-guided spraying. More than 61% of farms deploying UAV sprayers use high-spread activators to stabilize droplets in low-volume spray applications. Precision calibration systems have delivered measurable gains, including a 22% increase in deposition uniformity and up to 29% leaf penetration improvement in oilseed and cereal production. Growing alignment between precision agriculture platforms and specialized adjuvant blends is shaping a new performance-based consumption model.

• Rising Adoption of Weather-Resilient and Stress-Tolerant Adjuvant Technologies: Extreme temperature fluctuations and irregular rainfall patterns are accelerating demand for adjuvants engineered to maintain efficiency under harsh climatic conditions. Field performance results show that organosilicone-based activators with anti-evaporation properties deliver 35% longer droplet retention and 26% greater stomatal penetration during heat-stress conditions compared to standard surfactants. Adoption has grown sharply in Latin America and Asia, where 44% of growers now prioritize weather-resilient formulations for pesticide and foliar nutrient programs.

• Premiumization and Productivity-Linked Purchasing Behavior Among Large Farms: Large commercial farming groups are increasingly shifting from price-based purchasing to outcome-based selection of activator adjuvants. Surveys indicate that 72% of farms exceeding 2,000 hectares routinely purchase premium-grade formulations to ensure predictable spray performance and reduced pass counts. Trials across soybean and cotton production demonstrated a 17%–38% improvement in yield response where premium adjuvants were deployed consistently as part of integrated pest and nutrient programs. This behavior is reshaping distributor portfolios by emphasizing high-performance, crop-specific adjuvant lines rather than generic formulations.

The segmentation structure of the Agricultural Activator Adjuvants Market is defined by clear differentiation across product types, applications, and end-user groups, each contributing uniquely to commercial demand and technology evolution. Product types vary in their role across foliar, pesticide, and nutrient delivery programs, with performance factors such as spreadability, penetration, tank-mix compatibility, and drift control shaping adoption patterns. Application-based segmentation highlights varying priorities across herbicides, insecticides, fungicides, and micronutrient programs, driven by crop protection strategies and crop value. End-user segmentation reflects distinct consumption rhythms across large commercial farms, mid-scale growers, and agribusiness service enterprises, with precision-farming users showing accelerated demand for premium and technologically advanced formulations. Market dynamics show that high-efficiency activators are steadily replacing generic surfactants as producers shift toward yield-linked and outcome-based procurement approaches across regions.

Non-ionic surfactants represent the leading type in the Agricultural Activator Adjuvants Market, accounting for 39% of total adoption due to their high tank-mix compatibility and widespread suitability across herbicides, insecticides, and foliar nutrients. Organosilicone-based activators are emerging rapidly and currently capture 27% of total demand, driven by their superior spreading efficiency and ability to reduce surface tension for deep stomatal penetration. Organosilicones are also the fastest-growing type, projected to expand at a 7.2% CAGR as farms intensify precision spraying and low-volume application techniques. Oil-based activators, esterified seed oils, methylated seed oils, and cationic/anionics collectively contribute the remaining 34%, positioned strongly in selective herbicide and high-value horticulture applications. These niche types are experiencing higher uptake in regions prioritizing climate-resilient input programs.

Herbicides represent the dominant application segment in the Agricultural Activator Adjuvants Market, capturing 46% of total usage due to continual weed resistance pressures and the requirement for enhanced penetration and absorption across post-emergence herbicide programs. Insecticides represent 24% of current adjuvant use, while fungicides account for 18%; however, micronutrient and foliar nutrition programs have emerged as the fastest-growing segment, supported by rising demand for yield optimization and crop enrichment solutions, projected to register a 6.9% CAGR. The shared contribution of non-dominant categories (insecticides, fungicides, micronutrients, and others) represents 54% of the market, with adoption shifting toward tank mixes that combine activators with multiple crop protection modes of action.

Large commercial farms represent the leading end-user segment in the Agricultural Activator Adjuvants Market, holding 51% of demand due to their heavy reliance on precision spraying equipment, high-value crop cultivation, and outcome-linked procurement practices. Contract farming groups and agribusiness service providers account for 26% of consumption, driven by the need to demonstrate measurable field productivity improvements to multiple growers. Small and mid-scale farms capture 23% but represent the fastest-growing end-user category, projected to expand at a 6.7% CAGR as access to agronomic advisories, subsidies, and drone-spraying services increases. Collectively, non-large farm users now contribute 49% of total market activity, reflecting a shift toward widespread adoption beyond industrial agricultural enterprises.

North America accounted for the largest market share at 34.7% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.8% between 2025 and 2032.

Europe held 28.4% share in 2024, followed by Asia-Pacific with 23.6%, South America at 7.2%, and Middle East & Africa at 6.1%. The dominance of North America is attributed to high adoption of premium crop protection ingredients and increasing demand from large-scale commercial farming clusters across the United States and Canada. Meanwhile, the rapid expansion in Asia-Pacific is driven by growing investments in precision farming, increasing agricultural exports, and high consumption of organo-silicone-based activator adjuvants in high-value crops.

What is driving accelerated adoption of advanced activator adjuvant ingredients in agricultural output optimization?

The North America Agricultural Activator Adjuvants Market accounted for 34.7% share in 2024, driven primarily by commercial farming operations in the United States and Canada, where large agricultural enterprises are increasingly integrating adjuvants to enhance pesticide and herbicide performance. Demand is supported by industries including grains, oilseeds, fruits, and vegetable cultivation. The region is experiencing notable policy support through initiatives encouraging sustainable crop protection practices and reduced agrochemical overuse. Technological advancements such as AI-enabled farming, drone spraying, and automated dispensing systems are further endorsing adoption. A local player example includes Wilbur-Ellis, which continues to expand its activator-based adjuvant product portfolio targeting high-yield farm clusters. Consumer behavior shows a preference toward premium and highly efficient agricultural formulations, especially among large enterprise farmers.

How are sustainability commitments reshaping demand for performance-driven activator adjuvants?

Europe held 28.4% of the Agricultural Activator Adjuvants Market in 2024, with Germany, France, and the UK being the largest consumers due to strong agricultural chemical consumption and export-driven farming outputs. The market is significantly influenced by strict EU sustainability and crop protection regulations, leading to higher demand for highly efficient and low-toxicity activator adjuvants. Widespread adoption of precision agriculture tools, eco-certified solvents, and digital spraying systems is accelerating transformation across European farmlands. Local producers like Solvay are actively developing biodegradable adjuvant components aligned with EU Green Deal objectives. Consumer behavior in Europe demonstrates a clear tilt toward compliance-driven and environmentally aligned agri-inputs, increasing traction for activator adjuvants that deliver effective results with reduced chemical load.

Why is demand for performance adjuvants rising rapidly across high-output agriculture economies?

Asia-Pacific represented 23.6% of market volume in 2024, ranking as the fastest-expanding region globally, supported by increasing crop exports and growing uptake of modern crop protection technologies. China, India, and Japan are the top consuming countries, supported by extensive grain, horticulture, and plantation agriculture industries. The region is witnessing a surge in manufacturing investments for silicone- and surfactant-based adjuvants and improvements in agrochemical supply chains. Innovation hubs in China and India are accelerating R&D for water-efficient and residue-optimized spray formulations. A notable local player, UPL, continues to expand manufacturing footprints with new product lines customized for tropical crop conditions. Consumer behavior is driven by rapid digitalization of agriculture, e-commerce distribution of crop inputs, and high adoption of mobile farm advisory platforms.

What is fueling the increasing requirement for high-efficiency activator blends across the farming sector?

South America accounted for 7.2% of the market share in 2024, led primarily by Brazil and Argentina, where large agricultural land banks and expansive commercial farming operations heavily rely on herbicides, fungicides, and insecticides that perform better with activator adjuvants. Infrastructure expansion in fertilizer and agrochemical distribution networks is fostering wider accessibility. Government incentives for agricultural exports and trade policies supporting crop protection inputs continue to boost adoption. A regional player example includes Oro Agri, engaged in expanding distribution of high-performance organo-silicone–based adjuvants across soybean and sugarcane cultivation segments. Consumer behavior in the region highlights a growing appetite for formulation compatibility and improved field performance under varied tropical climatic conditions, especially among export-dependent crop producers.

How is modernization of regional agriculture influencing the adoption of performance-enhancing adjuvant solutions?

The Middle East & Africa represented 6.1% of market demand in 2024, with expansion driven by modernization of agricultural programs across Saudi Arabia, UAE, Egypt, and South Africa. Demand is concentrated in high-value crops, greenhouse agriculture, and desert farming segments requiring optimized agrochemical performance. Major growth trends include precision irrigation, climate-adaptive agriculture, and digitization of farm inputs. Regional trade alliances encouraging crop protection imports and local formulations play a supportive role. Local players like Al-Rowad International have expanded portfolios for performance-enhanced spray applications in greenhouse farming. Consumer behavior demonstrates increasing preference for reliable yield-boosting solutions due to limited cultivable land and water-constrained agriculture, accelerating the shift toward activator adjuvants.

• United States – 29.5% share

Dominance driven by large-scale commercial farming, strong adoption of crop protection chemicals, and investment in precision agriculture technologies.

• China – 17.2% share

Leadership supported by extensive agricultural production, rapidly scaling agrochemical manufacturing, and high consumption across export-oriented crop sectors.

The Agricultural Activator Adjuvants Market is moderately fragmented, with over 48 active global competitors operating across categories such as surfactants, oil-based activators, organo-silicones, and utility adjuvants. The top five players collectively hold around 41–45% of the market share, highlighting strong competition among multinational chemical leaders and regional agritech formulators. Competitive strategies increasingly focus on formulation efficiency, eco-compliance, tank-mix compatibility, and crop-specific performance to secure long-term distributor partnerships.

In 2024, 27% of new launches were dedicated to sustainable and low-residue adjuvant technologies, while 33% of strategic collaborations targeted expansion into Asia-Pacific and Latin America, reflecting demand surges across high-intensity farming zones. The market is further shaped by R&D investments in biodegradable wetting agents, nano-emulsion delivery systems, next-gen organo-silicone blends, and drone-spray ready fluids, accelerating product differentiation. The competitive rivalry is expected to intensify as digital agriculture platforms and data-driven farming promote performance benchmarking and transparent product comparisons.

BASF SE

Evonik Industries AG

Solvay

Croda International Plc

Wilbur-Ellis

UPL Limited

Stepan Company

Oro Agri

Nouryon

Brandt Consolidated Inc.

Technology advancements in the Agricultural Activator Adjuvants market are reshaping product development, application efficiency, and farm-level performance outcomes. One of the most transformative shifts is the adoption of next-generation organo-silicone adjuvants, which improve droplet spreading and stomatal infiltration by up to 78% compared to conventional surfactants, enabling stronger delivery of pesticides and fertilizers in low-water spray volumes. These formulations have gained significant traction in precision farming systems, where uniform distribution and rapid foliar absorption are critical to performance.

Nano-emulsion delivery systems are another major advancement, accounting for nearly 22% of new product developments in 2024. These technologies enable controlled release of active ingredients, increasing deposition and bioavailability by 35–40%, particularly in high-value crops including fruits, vegetables, and oilseeds. Adoption is driven by the growing need for residue-efficient and environmentally compliant adjuvants that support sustainable crop protection practices.

Spray-technology compatibility trends are also accelerating innovation. Approximately 31% of newly launched activator adjuvants are now formulated for drone-spray and automated sprayer systems, reducing the risk of evaporation and drift in high-temperature regions. These advanced adjuvants support up to 25% lower chemical usage per hectare, improving cost efficiency and environmental outcomes for large commercial farms.

Digital agriculture ecosystems are further reinforcing technology integration, with over 42% of large farms globally using data-driven decision tools for selecting tank-mix combinations and spray schedules. Manufacturers are responding by developing AI-supported label recommendation apps and QR-based usage guides, enhancing on-field adoption accuracy and reducing misuse rates by an average of 18%. Together, these innovations are elevating product performance standards and encouraging deeper collaboration between chemical formulators, automation providers, and agritech platforms.

In May 2023, BASF SE launched its tank-mix adjuvant “Agnique HP 450”, which demonstrated an 8 % increase in protection effectiveness and a 14 % increase in harvest yield across field trials in Brazil.

On 28 September 2023, Croda International Plc introduced Atlox™ BS-50, a ready-to-use powder delivery system tailored for spore-forming microbes in the biopesticide segment, accelerating formulation development time for its customers.

In October 2024, Croda announced an expanded adjuvant portfolio focused on drone- and boom-sprayer delivery modes, including Atplus™ DRT-7000 and Atplus™ UEP-100, designed to enhance spray retention and leaf penetration while meeting OMRI certification requirements.

In May 2024, BASF introduced the Agnique BioHance line of bio-adjuvants designed to support biological pesticide solutions, using naturally-derived active ingredients to enhance application of micro-organisms and reduce external degradation factors in crop protection.

The scope of the Agricultural Activator Adjuvants Market Report encompasses a comprehensive review of product types, application domains, end-user segments, and geographic coverage, aiming to provide strategic insights for decision-makers and industry professionals. It addresses major product type categories such as surfactants (non-ionic, cationic/anionic), oil-based adjuvants, and other specialty activators. The report includes application segments covering herbicides, insecticides, fungicides, micronutrients and foliar nutrition, offering numerical insights into adoption distribution across these categories. It also includes end-user segmentation by large commercial farms, agribusiness service providers, mid-scale growers and smallholder cooperatives, and tracks adoption rates and usage patterns within each group. Geographically, the report covers regions including North America, Europe, Asia-Pacific, South America, Middle East & Africa with regional statistics, infrastructure trends, and manufacturing capacity assessments. In addition, it covers emerging and niche segments such as bio-based activator adjuvants, drone-sprayed low-volume systems, and digital-enabled formulation platforms. The industry-focus areas include regulation compliance, sustainable formulation strategies, private-public collaboration, and M&A/partnership activity within the adjuvant space. This scope ensures that stakeholders can analyse both current competition and future pathways, technology disruption and investment priorities within the activator adjuvant market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2724.85 Million |

|

Market Revenue in 2032 |

USD 4150.19 Million |

|

CAGR (2025 - 2032) |

5.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Evonik Industries AG, Solvay, Croda International Plc , Wilbur-Ellis , UPL Limited , Stepan Company, Oro Agri, Nouryon, Brandt Consolidated Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |