Reports

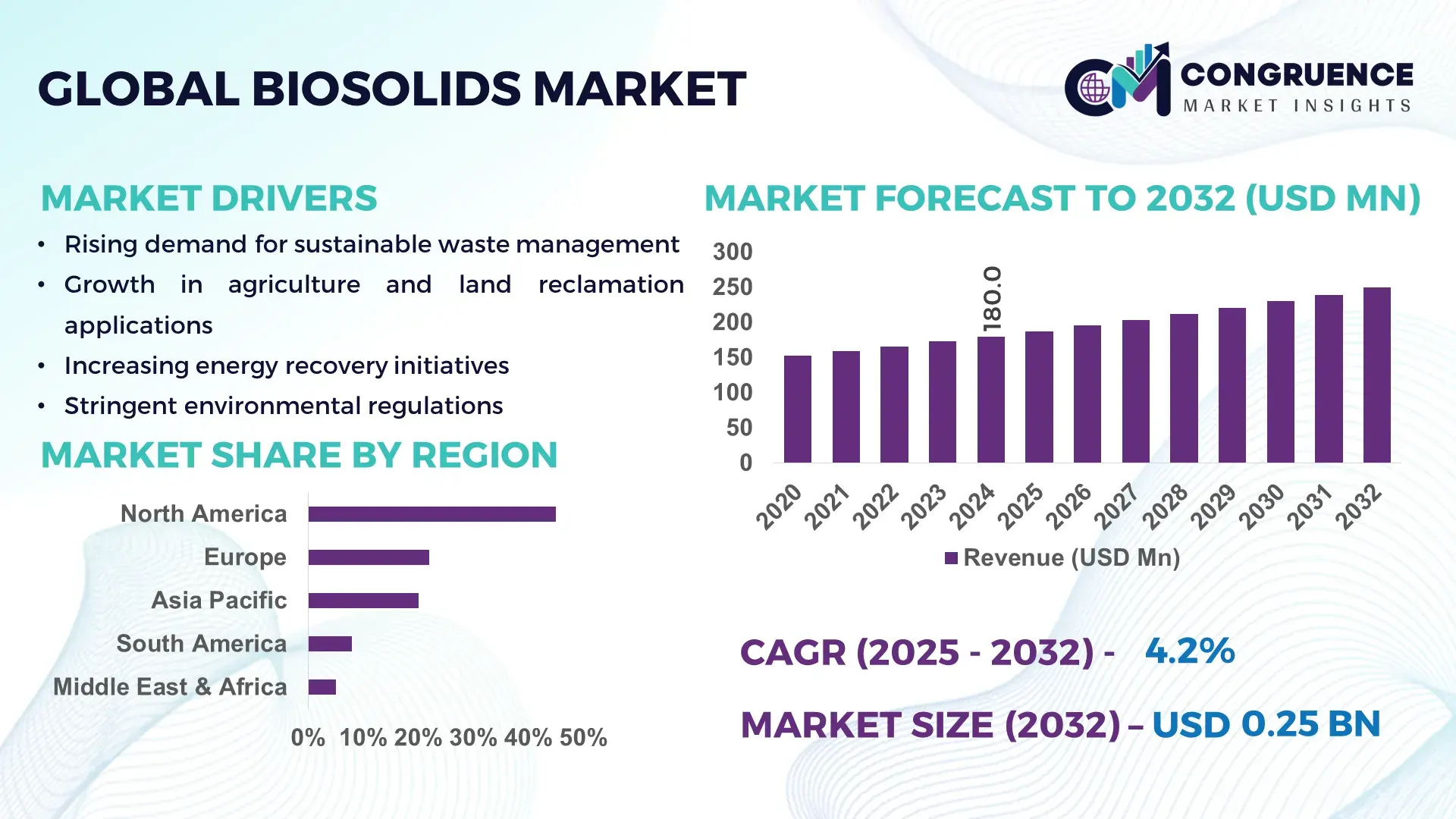

The Global Biosolids Market was valued at USD 180.0 Million in 2024 and is anticipated to reach USD 249.2 Million by 2032, expanding at a CAGR of 4.15% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is primarily driven by rising demand for sustainable wastewater treatment and resource recovery solutions across municipal and industrial sectors.

The United States plays a pivotal role in shaping the global Biosolids Market, supported by advanced treatment infrastructure, high production volumes, and continuous investment in biosolids-to-energy technologies. The U.S. processes over 7 million dry tons of sewage sludge annually, with more than 55% transformed into Class A and Class B biosolids. Substantial federal and state funding—exceeding USD 10 billion annually for wastewater improvements—supports modernization of thermal hydrolysis, anaerobic digestion, and nutrient recovery systems. This has enabled widespread application of biosolids in agriculture, land restoration, and biogas generation, strengthening the country's leadership in the sector.

Market Size & Growth: The market is valued at USD 180.0 million in 2024 and is projected to reach USD 249.2 million by 2032, driven by a 4.15% CAGR supported by rising sustainable waste management practices.

Top Growth Drivers: Increased adoption in agriculture (up 37%), efficiency improvements in advanced digestion systems (up 28%), and wider municipal adoption (up 42%).

Short-Term Forecast: By 2028, operational process optimization is expected to lower treatment costs by 18% through automation and improved digestion yields.

Emerging Technologies: Thermal hydrolysis, nutrient recovery systems, and carbon-neutral biosolids processing are reshaping operational models.

Regional Leaders: By 2032, North America is projected to reach USD 82 million, Europe USD 67 million, and Asia-Pacific USD 59 million, each driven by distinct regulatory and adoption trends.

Consumer/End-User Trends: Municipal utilities, agricultural users, and restoration projects show rising adoption, with nutrient-rich biosolids gaining notable traction.

Pilot or Case Example: A 2027 U.S. pilot achieved a 22% increase in biogas output through integrated thermal hydrolysis and digestion.

Competitive Landscape: The market leader holds approximately 14% share, followed by key competitors such as Veolia, SUEZ, Clean Harbors, Synagro, and Bio-Entech.

Regulatory & ESG Impact: Stricter nutrient discharge limits and ESG-aligned recycling mandates are pushing utilities to adopt circular biosolids utilization models.

Investment & Funding Patterns: Recent investments exceeded USD 1.1 billion globally, emphasizing modernization of treatment facilities and zero-waste treatment technologies.

Innovation & Future Outlook: Innovations in biosolids-to-energy conversion, carbon sequestration, and agricultural-grade pelletized biosolids will shape future market expansion.

The Biosolids Market benefits from diversification across agriculture, landscaping, and land reclamation sectors, supported by advancements in nutrient recovery, thermal processing, and odor-control technologies. Regulatory emphasis on circular economy principles, coupled with rising sustainability demands, continues to fuel adoption across high-consumption regions. Emerging innovations in sludge-to-energy conversion and carbon-neutral processing are redefining industry benchmarks, ensuring stable growth and future resilience.

The Biosolids Market holds strategic importance as global economies shift toward circular resource systems, low-carbon operations, and compliance-driven waste management frameworks. Biosolids contribute to long-term sustainability goals by enabling nutrient recovery, soil enhancement, and renewable energy production. As wastewater treatment plants transition into resource recovery facilities, measurable improvements in operational efficiency continue to emerge. For instance, advanced anaerobic digestion delivers 30% higher energy output compared to conventional digestion methods, establishing a compelling benchmark for utilities seeking optimized performance.

Regional dynamics further shape strategic pathways. North America dominates in volume, driven by high wastewater treatment penetration, while Europe leads in adoption, with over 65% of enterprises utilizing advanced biosolids recycling processes aligned with strict environmental regulations. Short-term projections indicate rapid transformation: By 2027, AI-driven process automation is expected to improve digestion efficiency by 18%, reducing downtime and enhancing throughput for municipal operators.

Compliance frameworks, including ESG commitments, are central to the market’s direction. Firms are targeting 25% improvement in nutrient recycling by 2030, aligning with global decarbonization and circular economy objectives. Real-world scenarios demonstrate measurable progress: In 2026, Denmark achieved a 28% reduction in treatment-related emissions through thermal hydrolysis integration, reinforcing the viability of next-generation processing technologies.

Overall, the Biosolids Market is evolving into a cornerstone of sustainable wastewater management, driven by innovation, regulatory alignment, and increasing emphasis on resource circularity. These factors position the sector as a pillar of resilience, operational efficiency, and environmentally responsible growth over the coming decade.

The Biosolids Market is shaped by a combination of environmental mandates, technological advancements, and expanding end-use applications. Rising population density and urban wastewater loads are increasing demand for scalable biosolids processing solutions. Countries are adopting enhanced digestion, thermal hydrolysis, and nutrient recovery systems to improve operational efficiency and expand agricultural applicability. Growing interest in renewable energy generation from biosolids, including biogas and biofuel production, further strengthens market momentum. Shifts in regulatory frameworks, coupled with increasing emphasis on sustainable land application practices, continue to influence industry behavior and investment decisions across regions.

Advanced treatment technologies such as thermal hydrolysis, high-solids anaerobic digestion, and enhanced dewatering systems are significantly improving processing efficiency in the Biosolids Market. Thermal hydrolysis can increase digestion throughput by over 45%, enabling plants to handle higher sludge volumes without expanding footprint. High-solids digesters generate up to 30% more biogas, supporting renewable energy generation and grid integration. These improvements reduce operational costs, increase resource recovery rates, and enhance the quality of biosolids for agricultural and land restoration applications. The adoption of automation and AI-based monitoring systems has also improved equipment uptime by 20–25%, enabling more predictable operational cycles. As utilities modernize infrastructure to meet evolving environmental standards, demand for advanced treatment systems continues to rise, strengthening the market’s long-term growth trajectory.

Regulatory complexities related to contaminant limits, land application restrictions, and evolving environmental compliance frameworks pose significant restraints on the Biosolids Market. Variability in permissible nutrient levels, pathogen standards, and trace contaminant thresholds increases compliance burdens for utilities and treatment operators. PFAS-related restrictions have prompted states and countries to tighten land application regulations, requiring additional monitoring and advanced treatment processes. Implementing these controls can increase operational costs by 12–18%, particularly for smaller facilities with limited capital resources. Public concerns around odor, environmental impact, and agricultural use further complicate adoption. These regulatory and social pressures slow project approvals, constrain land application areas, and delay infrastructure modernization, collectively restraining broader market expansion despite rising demand.

Renewable energy generation represents a major opportunity for the Biosolids Market as utilities increasingly leverage biosolids for biogas, biomethane, and biochar production. Advanced anaerobic digestion systems can raise energy recovery yields by 25–35%, transforming wastewater treatment plants into net energy producers. Government incentives for renewable natural gas (RNG) and carbon-neutral operations amplify investment in biosolids-to-energy projects. The expansion of co-digestion facilities—where food waste and biosolids are processed together—can boost biogas output by 40% or more, creating new revenue streams for municipalities. Growing demand for low-carbon fuel alternatives and soil-enhancing biochar further enhances market prospects. This shift aligns with global climate targets and supports utilities aiming for energy self-sufficiency and improved sustainability performance.

Infrastructure modernization is a significant challenge due to aging wastewater treatment facilities, high capital costs, and limited public funding. More than 30% of global wastewater plants operate beyond their intended lifecycle, requiring substantial upgrades to meet modern biosolids management standards. Transitioning to advanced treatment systems, such as thermal hydrolysis or enhanced digestion, can require multimillion-dollar investments many municipalities cannot immediately support. Operational disruptions during upgrades further complicate implementation. Additionally, engineering complexity and the need for skilled labor delay modernization timelines. These infrastructure constraints hinder the adoption of higher-efficiency systems and limit the capacity of utilities to scale biosolids processing in line with increasing wastewater volumes.

Adoption of Advanced Thermal Hydrolysis Systems: Utilities worldwide are adopting thermal hydrolysis to improve biosolids quality, achieving up to 45% higher digestion efficiency and 30% greater biogas production. More than 20 countries have commissioned newer THP units since 2020, enabling faster processing cycles and reducing disposal volumes by up to 25%.

Rise in Carbon-Neutral Processing Initiatives: The shift toward carbon-neutral biosolids management is accelerating, with facilities targeting 30–40% reductions in emissions through renewable energy integration and optimized thermal processes. Over 200 facilities globally are transitioning to carbon-reduction roadmaps, incorporating biochar production that sequesters up to 2.8 tons of carbon per ton of biosolids.

Expansion of Agricultural-Grade Pelletized Biosolids: Demand for pelletized biosolids with enhanced nutrient stability is increasing, with agricultural uptake rising 32% since 2021. Modern pelletizing lines can process up to 15 tons per hour, reducing moisture content to below 10% and improving logistics efficiency for long-distance distribution.

Growth in Digital Monitoring and AI-Based Optimization: More than 55% of new projects integrate digital process control, resulting in 18% reductions in operational downtime and 22% improvements in digestion stability. AI-enhanced nutrient modeling supports precision application, enabling farmers to optimize soil conditioning outcomes and reduce environmental impact.

The Biosolids Market is segmented by type, application, and end-user categories, each contributing distinct dynamics shaped by regulatory frameworks, processing capabilities, and end-use requirements. Product types such as Class A, Class B, and advanced thermally treated biosolids play varying roles in agricultural enrichment, land reclamation, and energy recovery initiatives. Application segmentation reflects broad utilization across agriculture, landscaping, and bioenergy sectors, driven by rising sustainability demands and nutrient recovery practices. End-user segmentation includes municipal utilities, agricultural enterprises, industrial processors, and environmental restoration agencies. Growth across all segments is influenced by increasing wastewater outputs, improvements in treatment efficiency, and rising emphasis on circular economy mandates. Shifts in adoption patterns, especially toward high-grade and thermally processed biosolids, underscore the market’s transition toward safer, more consistent, and technologically advanced outputs tailored to evolving regulatory and environmental expectations.

The Biosolids Market comprises Class A biosolids, Class B biosolids, and advanced thermally treated or pelletized biosolids. Class A biosolids currently account for approximately 46% of total adoption, driven by high-quality pathogen reduction, suitability for agricultural applications, and increasingly standardized treatment processes. In contrast, Class B biosolids represent around 34%, largely used in land reclamation and restricted agricultural scenarios due to their lower pathogen treatment level. However, advanced thermally treated biosolids are expanding fastest, projected to grow at a CAGR of 6.9%, supported by rising investment in thermal hydrolysis, enhanced nutrient recovery, and improved dewatering systems. Their adoption is expected to exceed 30% of usage by 2032, reflecting the shift toward higher safety and value-added applications. The remaining types, including composted blends and alkaline-stabilized biosolids, collectively contribute around 20%, serving niche markets focused on specialized soil improvement and landscaping.

The primary applications of biosolids include agriculture, land reclamation, landscaping, and bioenergy production. Agriculture remains the leading segment with about 48% share, driven by high nutrient content, soil conditioning benefits, and growing acceptance among large-scale farming operators. Land reclamation accounts for approximately 27%, primarily used in mining restoration and erosion mitigation projects. Landscaping, holding about 18%, benefits from stable nutrient release and organic matter enhancement. However, bioenergy applications are growing fastest, supported by a CAGR of 7.2%, as utilities adopt anaerobic digestion and co-digestion systems to convert biosolids into biogas and biomethane. Adoption is expected to surpass 30% of advanced biosolids use by 2032, reflecting the global shift toward renewable energy solutions. Consumer and enterprise adoption trends further validate this growth direction. In 2024, over 38% of utilities worldwide reported piloting biosolids-based energy recovery systems, while more than 41% of agricultural cooperatives adopted biosolids as a sustainable soil amendment.

End-users in the Biosolids Market include municipal wastewater treatment plants, agricultural enterprises, industrial processors, and environmental restoration agencies. Municipal utilities remain the dominant end-user group, accounting for nearly 52% of adoption, supported by significant wastewater throughput and regulatory obligations to manage sludge sustainably. Agricultural enterprises represent about 31%, leveraging biosolids for nutrient-rich soil enhancement and cost-effective fertilization. Industrial processors and environmental agencies collectively contribute 17%, applying biosolids in specialized niches such as land rehabilitation, composting, and soil restoration. The fastest-growing end-user segment is agricultural enterprises, projected to grow at a CAGR of 7.1% due to rising fertilizer costs, soil degradation concerns, and greater acceptance of organic amendments. Adoption patterns reflect this shift: In 2024, more than 36% of large-scale farms in North America incorporated biosolids into crop rotation plans, while over 29% of European environmental rehabilitation projects used biosolids in soil renewal strategies.

North America accounted for the largest market share at 45% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

North America maintained the leading position with over 8.2 million dry tons of biosolids processed annually, supported by modern wastewater infrastructure and extensive municipal adoption. Asia-Pacific, led by China, India, and Japan, processed 4.9 million dry tons in 2024, driven by industrial expansion and urban wastewater management. Europe contributed 28% of the global volume, with Germany, UK, and France implementing advanced nutrient recovery initiatives. South America processed 1.5 million dry tons, focusing on agricultural application and energy generation. Middle East & Africa, collectively, accounted for 7%, with key growth in UAE and South Africa. Increasing investments, adoption of digital monitoring, and regulatory incentives are shaping regional dynamics and driving global alignment toward sustainable biosolids management.

North America currently holds 45% market share, with the United States leading biosolids adoption in municipal utilities and agriculture. Key industries driving demand include wastewater utilities, agriculture, and renewable energy production from biogas. Regulatory frameworks such as EPA Part 503 rules and state-level nutrient discharge limits support structured biosolids management, while federal incentives encourage energy recovery projects. Technological advances include thermal hydrolysis, AI-based monitoring, and automated dewatering systems. Synagro Technologies recently upgraded its processing lines to integrate advanced digestion and pelletization, increasing nutrient stability. Enterprise adoption is high in sectors like healthcare and finance, with utilities applying stricter environmental controls and digital monitoring to enhance treatment precision.

Europe commands 28% market share, with Germany, UK, and France as leading contributors. Regulatory pressure from EU directives, including the Sewage Sludge Directive, promotes environmentally compliant biosolids application. Adoption of nutrient recovery systems, pelletization technologies, and anaerobic co-digestion is widespread. Local player Veolia Europe has implemented high-efficiency thermal hydrolysis units in Germany, improving sludge throughput by 35%. European consumers and municipal utilities prioritize explainable and traceable treatment processes, resulting in high adoption of monitoring and quality certification practices. Nutrient-enriched biosolids are increasingly used in sustainable agriculture and land restoration, reflecting regulatory and market-driven adoption trends.

Asia-Pacific accounted for 27% of the global volume in 2024, with China, India, and Japan leading adoption. Infrastructure investments in urban wastewater treatment, anaerobic digestion, and pelletized biosolids are increasing, while technology hubs in Japan and Singapore focus on AI-assisted process optimization. Veolia China recently implemented modular digestion units that process 250,000 tons of sludge annually, enhancing energy recovery. Consumer adoption varies, with industrial enterprises leading in energy production applications and municipal utilities prioritizing large-scale treatment efficiency. Regional trends reflect rapid urbanization, rising agricultural nutrient demand, and governmental incentives for renewable energy integration using biosolids.

South America currently holds 12% of global market share, with Brazil and Argentina as major contributors. Infrastructure expansion in wastewater treatment and energy recovery is gaining momentum, complemented by government incentives for sustainable land application and bioenergy projects. Solví in Brazil has upgraded several plants to include anaerobic co-digestion and nutrient recovery, boosting agricultural application. Consumer behavior shows strong adoption in agriculture-driven regions, where biosolids serve as a reliable source of organic soil enrichment. Energy utilities are also piloting biogas generation programs, highlighting the region’s focus on circular economy practices.

Middle East & Africa accounted for 7% of the global market in 2024, with UAE and South Africa leading adoption. Regional growth is driven by oil & gas, construction, and urban wastewater treatment projects. Technological modernization includes thermal treatment and digital monitoring solutions. Veolia UAE has implemented modular digestion facilities capable of processing 100,000 tons annually, improving compliance and energy output. Local regulations encourage safe land application and energy recovery, while trade partnerships support technology imports. Consumer behavior reflects concentrated adoption in large-scale municipal utilities and industrial parks focusing on ESG compliance and resource efficiency.

United States – 45% Market Share: Dominance driven by high production capacity, advanced wastewater treatment infrastructure, and strong regulatory frameworks for biosolids utilization.

Germany – 12% Market Share: Supported by stringent environmental regulations, adoption of advanced digestion technologies, and widespread use in sustainable agriculture.

The global Biosolids Market is characterized by a moderately consolidated competitive environment with 20–25 active major competitors globally, alongside numerous regional and niche players. The top five companies — including Cambi Group AS, Veolia Environnement S.A., SUEZ S.A., Synagro Technologies, Inc., and Cleanaway Waste Management Ltd. — collectively hold approximately 30–35% of the global market share, indicating a competitive but not fully consolidated sector.

Competition is increasingly shaped by strategic initiatives such as acquisitions, technology upgrades, and expansion of service portfolios. For example, Veolia has expanded its biosolids treatment portfolio to include advanced anaerobic digestion and biogas upgrading systems to deliver renewable gas, offering over 99.5% methane recovery where implemented. Meanwhile, Synagro completed acquisition of a biosolids‑management firm in 2023 to strengthen its footprint in North America and improve its landfill‑diversion and composting capabilities.

Innovation is a key differentiator. Leading firms invest in thermal hydrolysis, nutrient‑recovery solutions, digital process monitoring, and biosolids‑to‑energy conversion technologies. This technological shift is reducing dependence on landfill disposal and enabling value‑added outputs like high-quality compost, pelletized fertilizers, and renewable biogas.

Because many companies operate in overlapping geographies — municipal wastewater, agricultural biosolids reuse, energy recovery — the market dynamics are shaped by service quality, regulatory compliance, and technology adoption rather than sheer size or volume alone. This competitive environment fosters continuous improvements in processing efficiency, environmental compliance, and service diversification, benefiting end-users and creating barriers for smaller or less technologically equipped players.

Synagro Technologies, Inc.

Cleanaway Waste Management Ltd.

The Biosolids Market is undergoing a technological transformation, driven by innovations that enhance treatment efficiency, resource recovery, and regulatory compliance. A key technology is thermal hydrolysis processing (THP), which pre-treats sewage sludge before anaerobic digestion. THP increases sludge dewaterability, improves biogas yield, and reduces pathogen levels — enabling production of higher‑quality biosolids suitable for agricultural use or composting. Many operators now retrofit existing digesters with THP modules to upgrade legacy plants.

Anaerobic digestion (AD) remains the foundational method for biosolids stabilization; however, it is increasingly paired with biogas upgrading systems that convert raw biogas into pipeline‑quality methane or renewable natural gas (RNG). For instance, upgraded systems recover more than 99.5% methane purity, enabling injection into natural gas grids or use as vehicle fuel — providing utilities with new revenue streams while advancing circular economy goals. Digital transformation is also influencing the sector. Operators are deploying real-time monitoring and automation systems — using sensors and process-control software — to optimize digestion conditions, monitor nutrient content, reduce odor emissions, and maintain regulatory compliance. This improves operational uptime, reduces maintenance costs, and ensures consistent quality of biosolids output. Emerging technologies include nutrient recovery systems that extract phosphorus and other valuable elements from sludge, offering fertiliser-grade products that can partly substitute mined phosphate. Recovery of phosphorus via controlled precipitation and struvite extraction is gaining traction, especially where agricultural reuse is prioritized.

Additionally, novel pathways like biosolids-to-biofuel and biosolids-derived biochar are being developed. These enable conversion of stabilized biosolids into renewable energy or soil carbon-sequestering biochar, aligning biosolids management with carbon-neutrality and sustainability objectives. In summary, the evolving technology landscape is shifting the focus of the Biosolids Market from mere sludge disposal to resource recovery, energy generation, and sustainable reuse — making treatment plants into multifunctional resource-recovery hubs rather than end-of-pipe disposal sites.

In May 2024, Synagro Technologies, Inc. launched its SynaPure™ water and wastewater treatment system, designed for modular deployment, capable of processing landfill leachate, industrial wastewater and lagoon wastewater — offering removal of contaminants including nutrients, metals, and emerging pollutants. The system is described as a Water‑as‑a‑Service model, reducing upfront investment for customers. Source: www.synagro.com

In June 2024, Synagro expanded its biosolids capacity by commissioning new composting facilities in New Jersey (Cumberland County) and South Carolina (Holly Hill), with a total investment exceeding USD 50 million; these centers are intended to serve local markets and produce biosolids-based compost. Source: www.synagro.com

In October 2024, Veolia Environnement S.A. signed a contract with the University Area Joint Authority (UAJA) in State College, Pennsylvania, to implement its first biological hydrolysis + advanced anaerobic digestion system in North America — aiming to process biosolids plus food waste, and upgrade generated biogas into renewable natural gas (RNG); the facility alone is expected to produce approximately 150,000 GJ/year of RNG. Source: www.veolia.com

In early 2025, Veolia confirmed that it met all its 2024 environmental and operational targets under its “GreenUp” strategic program — reporting significant reductions in emissions and expanded waste/wastewater treatment operations globally, reinforcing its position as a leading operator managing complex waste (including sludge & biosolids streams) across many facilities. Source: www.veolia.com

The Biosolids Market Report covers a comprehensive scope including product types (e.g., Class A, Class B, pelletized biosolids, composted biosolids), treatment methods (anaerobic digestion, thermal hydrolysis, composting, dewatering, nutrient-recovery processes), and end-products (fertilizer-grade biosolids, soil conditioners, biogas/RNG, biochar). Applications examined span agriculture, land reclamation and restoration, landscaping, municipal waste management, and energy recovery.

Geographically, the report addresses major global regions: North America, Europe, Asia-Pacific, South America, Middle East & Africa — including detailed country-level analysis for leading nations. It also considers different sources of biosolids (municipal wastewater, industrial sludge) and distribution channels (direct supply to agricultural users, contracts with waste-management utilities, renewable energy off-takers).

Moreover, the report highlights technological trends — such as integration of thermal hydrolysis with anaerobic digestion, digital process monitoring and automation, phosphorus and nutrient recovery, and biosolids-to-energy/biofuel conversion. Emerging market niches are covered, including sludge-based renewable energy, sustainable agriculture products, and circular economy-driven waste reuse.

The scope also emphasizes regulatory and ESG-driven drivers: compliance with sludge disposal regulations, nutrient-reuse mandates, carbon-reduction commitments, and sustainable land-application guidelines. The report is designed to aid decision-makers in strategic planning, investment decisions, technology adoption assessments, and competitive benchmarking across global and regional biosolids market landscapes.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 180.0 Million |

| Market Revenue (2032) | USD 249.2 Million |

| CAGR (2025–2032) | 4.15% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Cambi Group AS, Veolia Environnement S.A., SUEZ S.A., Synagro Technologies, Inc., Cleanaway Waste Management Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |