Reports

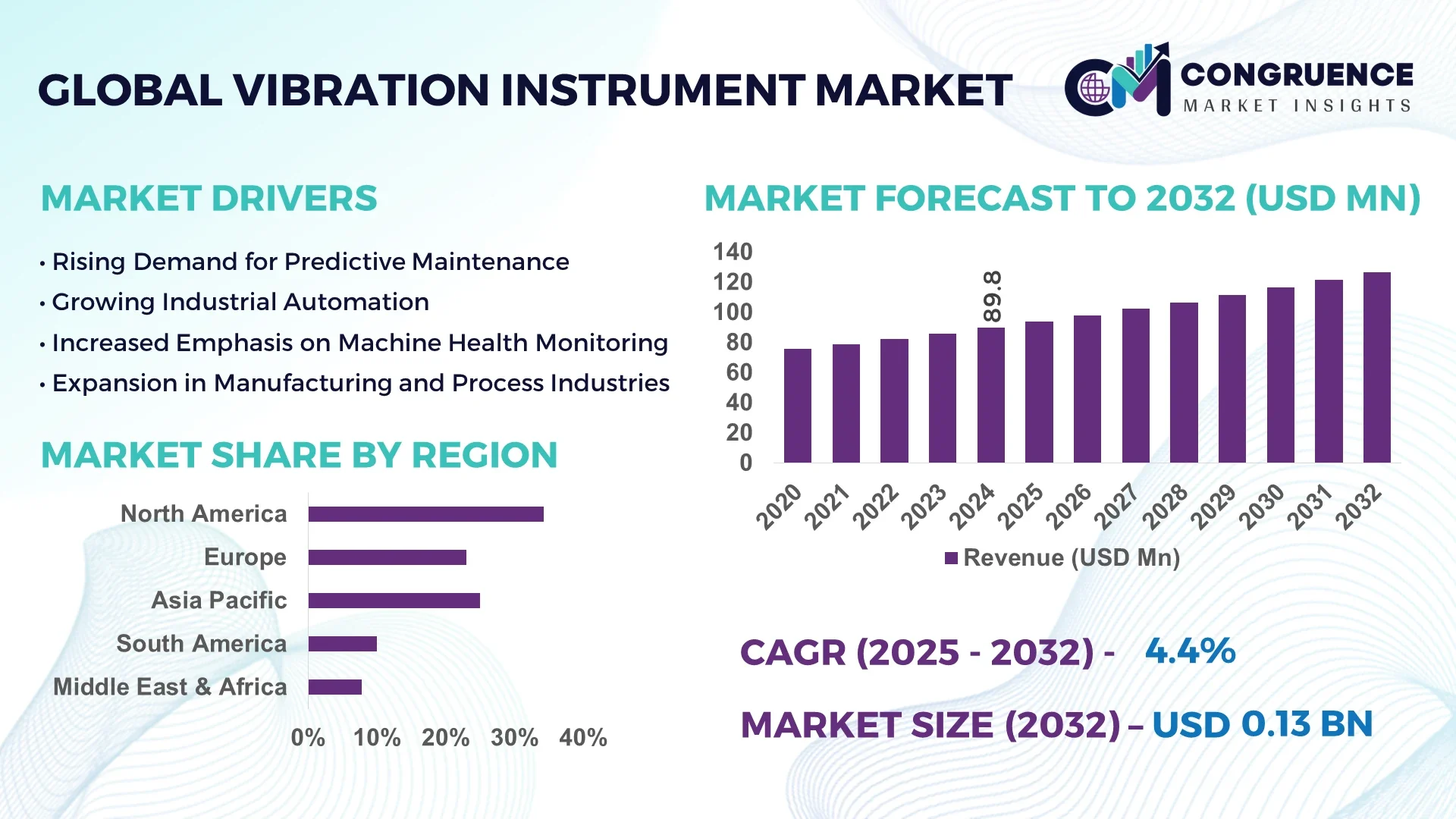

The Global Vibration Instrument Market was valued at USD 89.78 Million in 2024 and is anticipated to reach a value of USD 126.7 Million by 2032, expanding at a CAGR of 4.4% between 2025 and 2032.

Japan, a global leader in precision instrumentation, has significantly boosted its production capacity for vibration instruments by integrating high-frequency response accelerometers and laser Doppler vibrometers in its industrial metrology sector. With strong investments from automotive and aerospace manufacturers, Japan is also pioneering innovations in miniaturized sensor technologies and smart diagnostic systems for predictive maintenance.

The Vibration Instrument Market plays a critical role across diverse industrial domains, including automotive, energy, aerospace, manufacturing, and construction. Vibration analyzers and condition monitoring devices are widely used to detect mechanical faults, prevent equipment failure, and ensure operational safety. Recent advances in non-contact vibration measurement tools and wireless monitoring systems have broadened applications in harsh or remote environments. Additionally, stringent industrial safety regulations and the increasing focus on machinery health monitoring are propelling product demand. Emerging economies are witnessing rapid adoption, supported by infrastructure development and industrial automation initiatives. The market is also witnessing a trend toward integrated systems combining vibration sensors with IoT platforms for real-time analytics. With enhanced regional consumption patterns in Asia-Pacific and Europe, the future outlook remains robust, driven by technological convergence and a growing need for precision monitoring tools in smart factories and process automation.

Artificial Intelligence (AI) is revolutionizing the Vibration Instrument Market by enhancing data acquisition, analytics, and predictive maintenance capabilities. AI-powered vibration analysis systems can now detect anomalies with greater precision, reducing the risk of false positives and unplanned downtime. These intelligent systems integrate with cloud platforms to analyze vibration patterns in real time, offering machine learning-driven diagnostics that learn from past failures to predict future faults more accurately.

One of the most significant impacts of AI in the Vibration Instrument Market is the development of autonomous monitoring systems. These systems use AI algorithms to process large volumes of sensor data from equipment such as turbines, pumps, and motors. The result is faster identification of imbalance, misalignment, or bearing failures—issues that, if undetected, could lead to catastrophic breakdowns. In manufacturing and energy sectors, AI-based solutions are being embedded into existing infrastructure, helping reduce manual inspections and improving safety compliance.

Furthermore, AI facilitates integration with digital twins, where vibration data is used to simulate and optimize the performance of physical assets virtually. This real-time simulation and feedback mechanism empowers companies to enhance asset reliability and streamline maintenance operations. As industries continue to shift toward Industry 4.0, AI will remain at the core of innovation in the Vibration Instrument Market, enabling smarter, more connected, and cost-efficient monitoring solutions.

“In March 2024, a leading industrial equipment manufacturer introduced an AI-driven portable vibration analysis tool that reduced machinery diagnostic time by 48% while improving fault detection accuracy by 35% across 500 industrial plants globally.”

The Vibration Instrument Market is evolving rapidly, shaped by industrial automation, rising maintenance standards, and advancements in sensor technologies. A growing focus on predictive maintenance strategies across heavy industries like manufacturing, oil & gas, and power generation has intensified the need for accurate vibration analysis tools. Increased deployment of real-time condition monitoring systems and the shift from reactive to preventive maintenance practices are major contributors to market growth. The emergence of wireless and IoT-enabled vibration instruments is also transforming data accessibility and equipment diagnostics. In parallel, regulatory compliance requirements in developed markets and growing machinery health awareness in developing economies are bolstering adoption. However, high costs of advanced systems and the technical complexity of interpreting vibration data present ongoing challenges. Nonetheless, continual innovation and integration with AI-driven platforms are expected to reshape the Vibration Instrument Market with smarter and more adaptive solutions.

The growing emphasis on predictive maintenance in industrial sectors is a primary driver for the Vibration Instrument Market. Vibration monitoring is a cornerstone in predictive maintenance frameworks, allowing early detection of equipment wear, imbalance, and potential failure. Industries such as automotive, energy, and aerospace have adopted vibration instruments to monitor rotating machinery and reduce unplanned downtime. According to industrial maintenance case studies, companies leveraging predictive analytics supported by vibration data have achieved up to 25% reduction in maintenance costs and 30% increase in equipment uptime. The push for Industry 4.0 standards is further accelerating integration of intelligent vibration instruments into enterprise asset management systems. This trend enhances asset reliability and operational efficiency, positioning vibration instruments as vital components of modern industrial infrastructure.

One of the major restraints in the Vibration Instrument Market is the lack of technical expertise required to operate and interpret complex vibration analysis tools. Advanced systems, especially those integrating FFT analysis or wireless diagnostics, often necessitate specialized training to ensure accurate readings and insights. Small and medium-sized enterprises (SMEs), particularly in emerging economies, struggle to justify investments in such skilled personnel. Misinterpretation of vibration data can lead to inaccurate diagnostics, ineffective maintenance strategies, or even unnecessary equipment replacement. Additionally, the initial setup of these instruments—including sensor calibration, frequency tuning, and environmental adjustments—requires precision, limiting adoption among non-specialist users. These technical barriers hinder broader deployment, especially in cost-sensitive or low-tech industrial settings.

The increasing use of wireless and IoT-enabled sensors presents a substantial opportunity in the Vibration Instrument Market. These technologies eliminate the need for complex wiring infrastructure and enable remote, continuous monitoring of machinery across geographically dispersed locations. Wireless vibration sensors can transmit real-time data to cloud platforms where machine learning algorithms analyze performance trends and identify anomalies. In sectors like mining, power, and offshore oil rigs, wireless solutions improve safety and reduce the need for manual inspection in hazardous environments. Moreover, IoT integration enhances scalability, allowing multiple sensors to be linked under a single analytics platform. The growing adoption of smart factories and industrial automation is expected to drive demand for these next-generation vibration instruments that offer flexibility, cost-efficiency, and digital integration.

Despite technological advancements, the complex installation and calibration procedures associated with vibration instruments remain a persistent challenge. Precise placement of sensors is critical for accurate measurements, and even minor installation errors can lead to unreliable data. Additionally, calibration must account for variables such as environmental conditions, structural resonance, and machinery type. This process can be time-consuming and demands highly trained technicians, increasing operational costs. In dynamic industrial settings where machines operate under variable loads and speeds, ensuring consistent calibration adds another layer of complexity. Furthermore, the challenge of integrating vibration instruments with existing legacy systems without disrupting ongoing operations limits their seamless deployment. As industries demand quicker setup and plug-and-play diagnostics, the market must overcome these operational hurdles to fully realize growth potential.

Increased Adoption of Wireless Vibration Monitoring Systems: Industries are rapidly shifting toward wireless vibration monitoring solutions to overcome challenges related to complex wiring, sensor placement, and data accessibility. These systems are increasingly used in remote and hazardous environments, such as offshore oil platforms and mining sites. Wireless vibration sensors enable real-time performance tracking and remote diagnostics, improving operational efficiency and reducing the need for manual inspection. Recent industrial deployments indicate that wireless systems reduce monitoring setup time by up to 40%, boosting plant productivity and maintenance accuracy.

Integration with Industrial IoT Platforms: The Vibration Instrument Market is witnessing a strong push toward integration with Industrial Internet of Things (IIoT) ecosystems. Vibration data is now linked to cloud-based analytics platforms that support machine learning models to predict failures before they occur. In manufacturing plants, over 60% of vibration instrument upgrades in 2024 involved integration with IIoT dashboards. These solutions are improving data visualization, asset tracking, and maintenance scheduling, leading to more efficient decision-making and asset lifecycle management.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Vibration Instrument Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision vibration testing instruments is rising, especially in Europe and North America, where construction efficiency is critical. Vibration analysis tools are now essential in assessing the structural integrity and stability of prefabricated elements before deployment on-site.

Miniaturization and Portability of Vibration Instruments: Compact and portable vibration instruments are gaining popularity across sectors such as automotive and aerospace for on-the-go diagnostics. New-generation handheld analyzers can perform complex diagnostics such as FFT analysis and time-domain vibration measurement with improved battery life and rugged designs. These tools are increasingly used during field inspections, offering users accurate real-time data without needing bulky equipment. Recent innovations in microelectromechanical systems (MEMS) have enabled the development of smaller yet highly sensitive sensors, making vibration instruments more accessible and scalable.

The Vibration Instrument Market is segmented by type, application, and end-user, each contributing uniquely to the industry's growth and structure. The type segment includes various instruments such as vibration meters, data loggers, analyzers, and sensors, with sensors showing rising adoption due to their real-time feedback capabilities. From an application perspective, condition monitoring holds the lead, as industries place more value on preventative maintenance, while structural health monitoring is emerging rapidly. In terms of end-users, heavy industries like automotive, power generation, and oil & gas dominate usage, while sectors such as renewable energy and smart infrastructure are accelerating adoption due to their demand for real-time analytics and safety compliance. These segments are shaped by technological integration, operational complexity, and the need for more accurate, remote-capable vibration measurement solutions.

The Vibration Instrument Market encompasses a variety of instrument types including vibration analyzers, meters, sensors, and data loggers. Vibration sensors are currently the leading type, as they form the backbone of real-time monitoring systems across rotating machinery and critical infrastructure. These sensors are embedded within smart manufacturing setups to collect continuous performance data and detect anomalies. The fastest-growing type is vibration data loggers, propelled by the demand for historical data tracking and offline diagnostics in field applications. These devices are particularly valuable in remote or mobile operations where internet connectivity is limited. Vibration analyzers also hold significant market relevance due to their ability to perform in-depth diagnostics using Fast Fourier Transform (FFT) analysis. Meanwhile, portable vibration meters remain popular for on-site checks and low-frequency detection tasks in construction and mechanical maintenance environments. As market demands evolve, the preference is shifting toward integrated multi-function instruments that combine sensing, logging, and analyzing capabilities in compact form factors.

Among application areas in the Vibration Instrument Market, condition monitoring is the most dominant segment due to its critical role in preventive maintenance strategies across industries. The ability of vibration instruments to detect imbalance, misalignment, or bearing wear has made them essential in keeping industrial operations efficient and safe. Structural health monitoring is the fastest-growing application, fueled by rising concerns over infrastructure aging and disaster resilience in bridges, buildings, and tunnels. With urbanization accelerating, governments and private contractors are using vibration tools to ensure the longevity and safety of public infrastructure. Other significant application areas include machinery diagnostics in manufacturing, dynamic balancing in aviation, and vibration compliance testing in electronics. Each application leverages vibration analysis differently—ranging from real-time alerts to detailed forensic-level evaluations—expanding the instrument’s versatility in highly technical environments.

The manufacturing sector remains the leading end-user in the Vibration Instrument Market, accounting for widespread usage across assembly lines, CNC machinery, and robotic systems. The industry's need for continuous production efficiency and asset reliability makes vibration instruments indispensable. The fastest-growing end-user segment is the renewable energy industry, particularly in wind turbine and solar power installations. These sectors require real-time vibration monitoring to detect bearing issues, blade resonance, and structural fatigue—ensuring both safety and energy efficiency. Additionally, the oil & gas sector maintains strong relevance, using vibration tools to monitor compressors, pumps, and drilling rigs in both upstream and downstream activities. Meanwhile, infrastructure and civil engineering projects increasingly deploy vibration analysis tools to evaluate seismic activity impacts and ensure safety compliance. Across all these verticals, the unifying demand is for accurate, portable, and intelligent vibration solutions that align with safety, reliability, and predictive maintenance goals.

North America accounted for the largest market share at 34.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.7% between 2025 and 2032.

The Vibration Instrument Market in North America has been driven by large-scale industrial automation and predictive maintenance practices across oil & gas, aerospace, and automotive sectors. Simultaneously, the Asia-Pacific region is benefiting from rapid infrastructure development, rising manufacturing investments, and widespread digitization in emerging economies like India and China. The integration of AI-powered diagnostic tools and real-time condition monitoring systems is reshaping regional dynamics. Increased demand for cost-effective yet high-performance vibration instruments is further accelerating adoption across both established and emerging markets. With government support for smart factory implementation and growing concerns about operational safety and downtime minimization, vibration instrumentation continues to see heightened strategic deployment across diverse sectors globally.

Technological Upgrades Boost Industrial Equipment Monitoring Demand

North America held a substantial 34.2% share of the global Vibration Instrument Market in 2024, driven by industrial demand across oil & gas, aerospace, and power generation. Major players in these sectors rely on advanced vibration diagnostics to reduce equipment failure and optimize maintenance schedules. Regulatory shifts, such as stricter OSHA guidelines for machinery vibration exposure and compliance with ANSI standards, are encouraging more widespread adoption. Additionally, the region has seen an uptick in funding for digital transformation initiatives, with industrial IoT and wireless vibration solutions gaining traction. Integration of AI into machinery condition monitoring has also become common, particularly in U.S. and Canadian manufacturing plants, where downtime can lead to substantial financial loss. Cloud-based analytics platforms and real-time feedback loops are enhancing decision-making accuracy and operational reliability.

Automation Expansion Spurs High-Precision Monitoring Tools

Europe captured around 28.9% of the total Vibration Instrument Market in 2024, with Germany, the UK, and France leading demand due to their robust manufacturing, automotive, and energy sectors. The push for decarbonization and energy efficiency, backed by the EU’s Green Deal and sustainability goals, is intensifying adoption of predictive maintenance systems. European industries are rapidly digitizing their operations, with vibration instruments being integrated into smart factories for real-time monitoring. Advancements in MEMS sensor technology and the deployment of digital twins in industrial equipment management are key trends shaping regional growth. Moreover, increased investments in railway infrastructure and renewable energy projects across Central and Eastern Europe are expanding the application scope of vibration measurement tools for structural integrity and safety assurance.

Smart Manufacturing Drives Regional Adoption Surge

Asia-Pacific is the fastest-growing region in the Vibration Instrument Market, with China, India, and Japan contributing significantly to volume growth. The region's extensive manufacturing base—ranging from electronics to automotive and heavy machinery—relies heavily on precision vibration monitoring for operational optimization. China leads in industrial automation investment, while India is witnessing growth in predictive maintenance tools due to rapid infrastructure development and smart city initiatives. Japan remains a hub for sensor innovation and high-precision instrument manufacturing. The adoption of Industry 4.0 technologies is advancing quickly in Southeast Asia, where localized production centers are integrating real-time vibration analytics into equipment health monitoring. The growing focus on reliability, safety, and process optimization is expected to continue driving demand across the region.

Infrastructure Development and Energy Sector Investments Fuel Demand

Brazil and Argentina are the key contributors to the South American Vibration Instrument Market, accounting for over 6.8% of the global share in 2024. Brazil's investments in hydroelectric power, oil exploration, and industrial automation are central to regional demand for vibration analysis tools. Vibration instruments are increasingly utilized in power plant turbines, refinery compressors, and manufacturing assemblies. In Argentina, the mining sector is another active adopter of portable and wireless vibration sensors to monitor critical rotating equipment. Trade incentives and tax relief policies aimed at encouraging industrial modernization are further improving accessibility. As infrastructure projects expand across South America, from highway systems to smart grids, vibration monitoring technology is becoming vital in ensuring system longevity and efficiency.

Oil & Gas Sector Drives Strong Instrumentation Demand

Demand for vibration instruments in the Middle East & Africa is shaped largely by oil & gas, petrochemical, and construction industries. Countries such as the UAE and Saudi Arabia are making heavy investments in predictive maintenance tools to improve asset reliability in refineries, drilling platforms, and pipeline systems. South Africa is emerging as a significant adopter due to growing investments in smart manufacturing and mining automation. The regional market held an estimated 5.9% share in 2024. Vibration instruments are increasingly integrated with cloud-based monitoring platforms to support real-time diagnostics across remote and harsh operating conditions. Regulatory bodies are also mandating safety-focused upgrades in machinery, pushing industries to adopt compliant and intelligent vibration monitoring systems.

United States – 29.4% Market Share

High industrial automation adoption and widespread use in aerospace, oil & gas, and manufacturing make the U.S. the global leader in the Vibration Instrument Market.

China – 21.8% Market Share

Strong end-user demand driven by expansive manufacturing infrastructure and growing investments in smart factory technologies fuels China’s leadership position.

The Vibration Instrument market is characterized by a moderately fragmented competitive landscape, comprising over 50 active players globally, ranging from specialized sensor manufacturers to integrated industrial monitoring solution providers. Companies compete primarily on technological sophistication, instrument precision, ease of integration, and multi-parameter sensing capabilities. In 2024, the market saw a surge in strategic partnerships between vibration monitoring firms and predictive analytics software developers, enabling broader deployment across industrial IoT environments.

Product innovation remains central to competition, with leading players introducing AI-enabled, wireless, and real-time vibration analysis tools for both portable and fixed applications. Companies are also investing heavily in R&D to improve sensor durability, frequency range, and calibration accuracy. Additionally, several firms expanded their geographic footprint by launching service centers and localized product lines tailored for the Asian and South American industrial sectors. Mergers and acquisitions have further reshaped the landscape, allowing companies to access proprietary technologies and consolidate their global presence in high-growth end-use industries such as oil & gas, energy, manufacturing, and transportation.

Brüel & Kjær Vibro GmbH

SKF Group

Rockwell Automation, Inc.

Fluke Corporation

Emerson Electric Co.

Honeywell International Inc.

General Electric Company (GE Bently Nevada)

National Instruments Corporation

Schaeffler Technologies AG & Co. KG

Meggitt PLC

The Vibration Instrument Market is undergoing rapid technological evolution, driven by advancements in sensor miniaturization, wireless connectivity, and integration with digital analytics platforms. One of the most transformative developments is the proliferation of MEMS (Micro-Electro-Mechanical Systems) vibration sensors. These compact, cost-effective devices are increasingly favored in industrial settings for real-time condition monitoring of rotating machinery, enabling precise diagnostics with minimal hardware footprint.

AI and machine learning are also reshaping how vibration data is interpreted. Modern systems now feature intelligent algorithms that detect anomalous patterns, predict failures, and recommend corrective actions without manual input. This has proven especially valuable in sectors such as energy, manufacturing, and aerospace, where unscheduled downtime can have critical consequences. Cloud-based platforms have become integral, offering remote access, centralized data logging, and scalable monitoring across multiple sites.

Wireless vibration monitoring systems using Bluetooth Low Energy (BLE), Zigbee, and LoRaWAN protocols are gaining traction for their ability to cover vast industrial floors without invasive wiring. Moreover, integration with digital twins—virtual replicas of physical assets—is enhancing simulation and predictive modeling capabilities. These digital transformations are further supported by advances in battery life, sensor ruggedness, and environmental adaptability, ensuring long-term reliability in harsh operational conditions. Together, these technologies are elevating the precision, accessibility, and intelligence of vibration instrumentation across global industries.

• In January 2024, Fluke Corporation launched the 3563 Analysis Vibration Sensor, combining piezoelectric vibration sensing with cloud-based diagnostics to enable maintenance teams to detect early signs of equipment degradation across industrial operations.

• In September 2023, SKF introduced its Enlight Collect IMx-1, a wireless vibration and temperature monitoring device designed for scalable condition-based monitoring. It allows maintenance teams to optimize inspection intervals and machine uptime in demanding environments.

• In March 2024, Emerson expanded its AMS Asset Monitor line by integrating AI-powered vibration diagnostics, targeting continuous monitoring of compressors and pumps in petrochemical and oil & gas sectors. The upgrade enhances fault detection speed by 30%.

• In December 2023, Brüel & Kjær Vibro deployed its new VCM-3 diagnostic system across multiple European rail networks. The system enhances predictive maintenance by analyzing axlebox vibration data in real-time, improving train safety and maintenance planning.

The Vibration Instrument Market Report offers a comprehensive analysis of the global industry landscape, encompassing product types, applications, technologies, end-user verticals, and regional dynamics. Covering more than 20 key countries across six major regions—North America, Europe, Asia-Pacific, South America, the Middle East, and Africa—the report explores both mature and emerging markets. It presents insights into how vibration instruments are deployed across critical sectors including oil & gas, manufacturing, energy, automotive, aerospace, and construction, with a growing presence in healthcare and precision agriculture. In terms of segmentation, the report evaluates several categories such as handheld vibration meters, fixed monitoring systems, wireless vibration sensors, and real-time diagnostic solutions. It assesses the operational environment for each product type, highlighting their suitability for applications ranging from predictive maintenance and structural health monitoring to fault diagnostics and quality control.

From a technological perspective, the report covers the impact of AI-powered analytics, IoT-based connectivity, cloud-based monitoring platforms, MEMS sensor innovation, and digital twin integration. Furthermore, the report also identifies niche segments such as portable smart sensors for remote installations and vibration instruments tailored for hazardous environments like offshore oil rigs. With a strong focus on industrial automation trends, regulatory safety compliance, and smart factory adoption, the Vibration Instrument Market Report equips business leaders, engineers, and investors with practical insights to navigate technological shifts, regional opportunities, and competitive strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 89.78 Million |

|

Market Revenue in 2032 |

USD 126.7 Million |

|

CAGR (2025 - 2032) |

4.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Stryker Corporation, Getinge AB, Hillrom (now part of Baxter International Inc.), Mizuho OSI, STERIS plc, Skytron LLC, Merivaara Corp., ALVO Medical, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Staan Bio-Med Engineering Pvt Ltd., Famed Żywiec Sp. z o.o., Bıçakcılar Medical Devices |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |