Reports

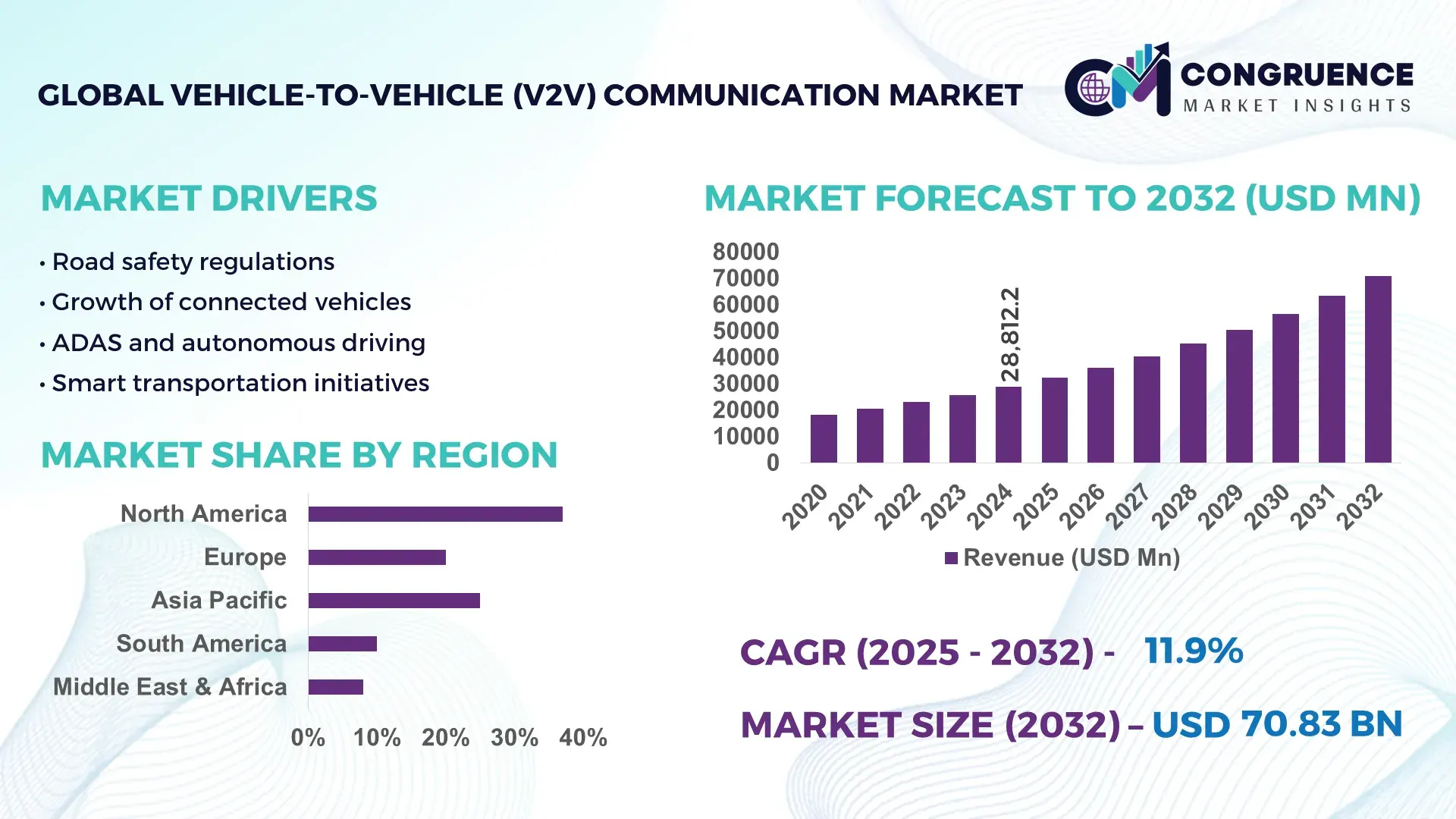

The Global Vehicle-To-Vehicle (V2V) Communication Market was valued at USD 28812.22 Million in 2024 and is anticipated to reach a value of USD 70830.03 Million by 2032 expanding at a CAGR of 11.9% between 2025 and 2032. Growth is driven by rising deployment of connected vehicle ecosystems and mandatory road-safety communication frameworks.

The United States represents the most influential country in the Vehicle-To-Vehicle (V2V) Communication market, supported by advanced automotive manufacturing capacity, large-scale pilot deployments, and sustained public–private investments. The country hosts over 40% of global connected vehicle R&D programs, with more than USD 5 billion invested in intelligent transportation systems between 2020 and 2024. Over 20 million vehicles equipped with V2V-ready onboard units are already operational, particularly across highway freight corridors and urban mobility networks. Applications span collision avoidance, cooperative adaptive cruise control, and autonomous driving validation. Technological leadership is reinforced by early adoption of C-V2X standards, 5G integration trials across 15+ smart cities, and active involvement of major OEMs and semiconductor firms in large-volume V2V chipset production.

Market Size & Growth: Valued at USD 28812.22 million in 2024, projected to reach USD 70830.03 million by 2032 at a CAGR of 11.9%, driven by rapid connected vehicle penetration and safety-centric mobility policies.

Top Growth Drivers: Connected vehicle adoption +38%, collision avoidance efficiency improvement +42%, real-time traffic optimization gains +31%.

Short-Term Forecast: By 2028, V2V-enabled fleet operations are expected to reduce accident-related costs by 25% and improve traffic flow efficiency by 18%.

Emerging Technologies: Cellular V2X (C-V2X), 5G-V2X integration, edge-based vehicular AI processing.

Regional Leaders: North America projected at USD 23800 million by 2032 with smart highway deployments; Europe at USD 19200 million driven by safety mandates; Asia-Pacific at USD 22100 million supported by mass connected vehicle adoption.

Consumer/End-User Trends: Commercial fleets and autonomous test vehicles account for over 55% of V2V system usage, with rising uptake in passenger EVs.

Pilot or Case Example: A 2024 multi-state U.S. V2V pilot achieved a 27% reduction in rear-end collisions across equipped freight vehicles.

Competitive Landscape: Qualcomm leads with ~22% share, followed by NXP Semiconductors, Bosch, Continental, and Harman.

Regulatory & ESG Impact: Road safety regulations, emission reduction targets, and smart mobility incentives accelerate V2V deployment.

Investment & Funding Patterns: Over USD 9 billion invested globally since 2022, with strong growth in infrastructure-linked project financing.

Innovation & Future Outlook: Integration of V2V with V2I and V2P systems, AI-driven predictive safety, and nationwide 5G corridors will shape long-term expansion.

The Vehicle-To-Vehicle (V2V) Communication market is primarily driven by automotive OEMs, commercial fleet operators, public transportation authorities, and smart city infrastructure developers, with passenger vehicles contributing approximately 45% of system deployments and commercial fleets around 35%. Recent innovations include low-latency C-V2X chipsets, software-defined vehicular communication platforms, and AI-enabled cooperative driving algorithms. Regulatory mandates for advanced driver assistance systems, environmental goals to reduce congestion-related emissions, and economic investments in digital infrastructure continue to support adoption. Consumption growth is strongest in North America and Asia-Pacific due to large vehicle parc sizes and urban congestion challenges. Emerging trends include autonomous vehicle platooning, cross-border V2V standard harmonization, and integration with mobility-as-a-service ecosystems, positioning the market for sustained long-term expansion.

The strategic relevance of the Vehicle-To-Vehicle (V2V) Communication Market lies in its direct role in transforming road safety, traffic efficiency, and autonomous mobility readiness across global transportation systems. V2V communication enables vehicles to exchange real-time data on speed, position, braking, and hazards, supporting cooperative decision-making at millisecond latency. From a strategic standpoint, Cellular Vehicle-to-Everything (C-V2X) delivers approximately 35% lower latency and 40% higher communication reliability compared to legacy Dedicated Short-Range Communications (DSRC), strengthening its position as the preferred future standard.

Regionally, Asia-Pacific dominates in deployment volume due to high vehicle production density and large-scale smart city rollouts, while North America leads in adoption intensity, with over 48% of connected fleet operators actively using V2V-enabled safety applications. By 2027, AI-driven edge analytics integrated with V2V systems are expected to improve collision prediction accuracy by 30% and reduce traffic congestion-related delays by nearly 18% in urban corridors.

From a compliance and ESG perspective, automotive and mobility firms are committing to sustainability targets such as 25% reduction in congestion-related CO₂ emissions and 20% improvement in road safety metrics by 2030 through intelligent transportation technologies. In 2024, the United States Department of Transportation, through multi-state C-V2X pilots, reported a 26% reduction in intersection-related incidents enabled by real-time V2V alerts and cooperative braking systems. Looking forward, the Vehicle-To-Vehicle (V2V) Communication Market is positioned as a foundational pillar for resilient mobility infrastructure, regulatory alignment, and sustainable long-term growth across passenger, commercial, and autonomous transportation ecosystems.

Rising demand for connected and autonomous vehicles is a primary driver of the Vehicle-To-Vehicle (V2V) Communication Market, as advanced driver assistance systems increasingly rely on real-time external data. Over 70% of newly developed vehicle platforms globally are now designed with built-in connectivity architectures capable of supporting V2V functions. Fleet operators adopting connected vehicle technologies report up to 22% reduction in accident frequency and measurable improvements in route efficiency. Autonomous vehicle testing programs also depend heavily on V2V communication to enable cooperative maneuvers such as platooning, lane merging, and emergency braking coordination. As Level 2+ and Level 3 automation features expand across mid-range vehicles, V2V communication is becoming a functional necessity rather than an optional enhancement, reinforcing sustained demand across both passenger and commercial segments.

Interoperability and infrastructure readiness remain key restraints in the Vehicle-To-Vehicle (V2V) Communication Market. Variations in communication standards, spectrum allocation, and regulatory alignment across regions limit seamless cross-border or cross-manufacturer communication. In several emerging markets, less than 35% of road infrastructure currently supports connected traffic systems, constraining effective V2V deployment. Additionally, legacy vehicle fleets without onboard communication units slow network effects, as V2V performance improves significantly only when penetration exceeds critical thresholds. Cybersecurity concerns and data governance complexities further add to implementation hesitation, particularly among fleet operators managing large-scale deployments. These structural and technical gaps continue to restrain uniform market expansion despite strong underlying demand.

Smart city development and intelligent transportation system investments present significant opportunities for the Vehicle-To-Vehicle (V2V) Communication Market. More than 500 cities globally are actively deploying connected traffic management platforms that integrate vehicle, signal, and infrastructure data. V2V-enabled applications such as intersection movement assistance, emergency vehicle prioritization, and cooperative traffic signal timing can reduce average travel time by up to 20% in dense urban zones. Public–private partnerships supporting digital road corridors and 5G-enabled highways further expand addressable deployment environments. As municipalities increasingly prioritize data-driven mobility planning and congestion mitigation, V2V communication systems are positioned to become core components of next-generation urban transport ecosystems.

Cybersecurity risks and system complexity pose significant challenges to the Vehicle-To-Vehicle (V2V) Communication Market. V2V networks involve continuous exchange of safety-critical data, making them potential targets for signal interference, spoofing, or unauthorized access. Securing low-latency communication without degrading performance requires advanced encryption, authentication, and certificate management systems, increasing implementation complexity. Automotive manufacturers report that integrating secure V2V stacks can extend development timelines by 15–20%. Additionally, ensuring functional safety across heterogeneous hardware, software, and network environments raises validation and compliance burdens. These technical and operational challenges must be addressed to ensure scalable, trustworthy, and resilient V2V deployments.

• Accelerated Shift from DSRC to Cellular V2X (C-V2X) Architectures: The Vehicle-To-Vehicle (V2V) Communication market is witnessing a decisive transition toward Cellular V2X standards due to superior latency and scalability. Over 65% of newly launched connected vehicle platforms in 2024 were designed with native C-V2X compatibility, compared to less than 30% five years earlier. Field deployments show up to 40% improvement in message reliability and nearly 35% reduction in end-to-end latency versus legacy DSRC systems. This shift is particularly pronounced in highway safety applications and autonomous vehicle testing corridors, where deterministic communication performance is critical.

• Integration of V2V with AI-Driven Edge Computing Systems: Automotive manufacturers and fleet operators are increasingly integrating V2V communication with onboard AI and edge analytics. More than 45% of pilot deployments now process V2V data locally within the vehicle rather than relying solely on cloud platforms. This approach has demonstrated up to 28% faster hazard recognition and 22% improvement in cooperative braking response times. Edge-enabled V2V systems are gaining traction in dense urban environments, where real-time decision-making is essential to mitigate congestion and collision risks.

• Expansion of V2V Adoption in Commercial Fleets and Logistics: Commercial vehicle fleets represent one of the fastest-growing adoption segments within the Vehicle-To-Vehicle (V2V) Communication market. Approximately 52% of large logistics fleets operating more than 1,000 vehicles have initiated V2V-enabled safety or platooning programs. Measured outcomes include a 17% reduction in fuel consumption through coordinated driving and a 25% decline in multi-vehicle collision incidents. Adoption is especially strong in long-haul freight routes across North America and Asia-Pacific, where operational efficiency gains are most measurable.

• Convergence of V2V with Smart Infrastructure and Traffic Systems: V2V communication is increasingly deployed as part of integrated intelligent transportation ecosystems. Over 40% of smart city mobility projects launched since 2023 include direct V2V interaction with traffic signals, road sensors, and emergency systems. These deployments have achieved up to 20% reduction in average intersection delays and a 30% improvement in emergency vehicle response coordination. This convergence highlights a shift from standalone vehicle connectivity toward system-level optimization of urban and intercity mobility networks.

The Vehicle-To-Vehicle (V2V) Communication market is segmented based on type, application, and end-user, each reflecting distinct adoption patterns and technological priorities. From a technology perspective, segmentation highlights the coexistence of legacy and next-generation communication protocols, with clear migration toward higher-speed, low-latency solutions. Application-based segmentation underscores the dominance of safety-critical use cases, while efficiency-driven and automation-oriented applications are gaining momentum. End-user segmentation reveals differentiated adoption between passenger vehicles, commercial fleets, and public-sector mobility operators, shaped by regulatory requirements, operational scale, and return-on-investment expectations. Across all segments, penetration levels are closely linked to infrastructure readiness, vehicle production volumes, and digital mobility policies. This segmentation framework provides decision-makers with clarity on where adoption is most mature, where growth is accelerating, and how value creation differs across use cases and user groups.

The Vehicle-To-Vehicle (V2V) Communication market by type is primarily segmented into Dedicated Short-Range Communications (DSRC), Cellular Vehicle-to-Everything (C-V2X), and hybrid or transitional communication systems. C-V2X currently represents the leading type, accounting for approximately 58% of deployed V2V systems, driven by its ability to support longer communication ranges, lower latency, and seamless integration with 4G and 5G networks. DSRC holds close to 27% share, largely concentrated in early deployments and legacy intelligent transportation projects. However, adoption of C-V2X is also the fastest-growing, expanding at an estimated 18% annual rate, supported by telecom-backed infrastructure rollouts and OEM standardization strategies. Hybrid solutions and pilot software-defined communication platforms collectively contribute around 15%, serving niche interoperability and testing requirements.

By application, the Vehicle-To-Vehicle (V2V) Communication market is dominated by road safety and collision avoidance systems, which account for nearly 46% of total implementation. These applications benefit directly from regulatory mandates and measurable reductions in accident severity and frequency. Traffic efficiency and congestion management applications represent about 29%, focusing on cooperative adaptive cruise control, platooning, and dynamic routing. While smaller today, autonomous driving support applications are growing the fastest, with adoption increasing at an estimated 21% annually as higher levels of vehicle automation move closer to commercialization. Other applications, including emergency vehicle coordination and environmental monitoring, collectively contribute around 25%.

From an end-user perspective, passenger vehicle manufacturers represent the largest segment, accounting for approximately 44% of V2V system integration, as connectivity becomes a standard feature in mid- and high-range vehicles. Commercial fleet operators follow closely with about 36% share, driven by quantifiable benefits such as reduced accident downtime, fuel optimization, and insurance cost improvements. Public transportation authorities and government mobility agencies collectively contribute around 20%, primarily through smart city and intelligent corridor projects. Commercial fleets are the fastest-growing end-user group, expanding at an estimated 19% annually due to rapid digitalization of logistics and long-haul transportation.

North America accounted for the largest market share at 38.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2025 and 2032.

North America benefits from early deployment of connected vehicle infrastructure, high penetration of advanced driver-assistance systems, and strong regulatory backing for V2V-enabled road safety. Europe follows closely with 29.4% share, driven by harmonized safety regulations and large-scale intelligent transport programs. Asia-Pacific already contributes over 24.1% of global V2V deployments, supported by high vehicle production volumes exceeding 52 million units annually and aggressive smart city investments. South America and the Middle East & Africa collectively account for 7.9%, but show rising pilot projects, policy alignment, and infrastructure modernization. Across regions, over 65% of new vehicle platforms launched in 2024 were V2V-ready, reflecting broad geographic momentum.

How is early digital mobility adoption accelerating large-scale deployment?

The North America Vehicle-To-Vehicle (V2V) Communication Market holds approximately 38.6% share, supported by mature automotive ecosystems and advanced digital infrastructure. Key demand originates from passenger vehicle OEMs, commercial trucking fleets, and public transportation agencies. Government-backed intelligent transportation programs cover over 120,000 km of connected roadways, while regulatory frameworks support C-V2X deployment at scale. Technological advancements include widespread 5G corridor rollouts and edge-enabled vehicular analytics, with over 48% of fleet operators actively using V2V safety applications. A leading regional semiconductor player has deployed next-generation C-V2X chipsets across more than 8 million vehicles. Consumer behavior shows higher enterprise adoption among logistics, ride-hailing, and municipal fleets, prioritizing safety automation and operational efficiency.

How are safety mandates transforming connected mobility ecosystems?

The Europe Vehicle-To-Vehicle (V2V) Communication Market accounts for around 29.4% of global demand, led by Germany, the United Kingdom, and France. Strong regulatory oversight from transport safety authorities and mandatory vehicle safety frameworks drive adoption. Over 70% of new vehicles sold in Germany in 2024 were equipped with V2V-compatible hardware. Sustainability initiatives promoting congestion reduction and emission control further support deployment. European OEMs are actively integrating V2V with cooperative adaptive cruise control and platooning systems. A major automotive supplier headquartered in Germany expanded V2V testing across 15 smart highway projects. Consumer behavior reflects regulatory-driven demand, with fleet buyers prioritizing certified, explainable, and interoperable V2V solutions.

Why is large-scale manufacturing reshaping adoption momentum?

The Asia-Pacific Vehicle-To-Vehicle (V2V) Communication Market ranks first globally in vehicle production volume, exceeding 52 million vehicles annually, and contributes 24.1% of current V2V deployments. China, Japan, and India dominate consumption due to dense urban traffic and government-led smart mobility programs. Over 90 cities in China have active V2X pilot zones, while Japan integrates V2V into autonomous public transport trials. Regional manufacturing hubs are rapidly embedding V2V modules at the factory level, reducing unit integration costs by nearly 18%. A leading Chinese automaker deployed C-V2X systems across 3 million connected vehicles in one year. Consumer behavior is driven by digital-first mobility, high smartphone integration, and app-based navigation ecosystems.

How are infrastructure upgrades opening new growth corridors?

The South America Vehicle-To-Vehicle (V2V) Communication Market represents approximately 4.6% share, with Brazil and Argentina as key contributors. Infrastructure modernization programs covering over 18,000 km of highways are creating foundational support for V2V adoption. Government incentives targeting road safety and logistics efficiency encourage pilot deployments in freight and public transport. Trade policies supporting automotive electronics imports further enable market entry. A Brazilian mobility technology provider launched V2V-enabled fleet safety trials covering 12,000 commercial vehicles. Consumer adoption remains selective, with demand closely tied to logistics optimization, cross-border freight movement, and localized language-based mobility platforms.

What role does smart infrastructure play in accelerating adoption?

The Middle East & Africa Vehicle-To-Vehicle (V2V) Communication Market accounts for about 3.3% of global demand, driven by infrastructure-intensive economies. The UAE and South Africa lead adoption through smart city initiatives and highway modernization projects. Over 6,500 km of smart roads are under development across the Gulf region. Governments actively promote connected mobility through public–private partnerships and cross-border trade corridors. A UAE-based technology integrator implemented V2V-enabled traffic management systems across 250 intersections. Consumer behavior emphasizes premium vehicle connectivity, safety automation, and integration with smart city services.

United States – 26.8% share

High connected vehicle penetration, large commercial fleet adoption, and strong regulatory support drive dominance in the Vehicle-To-Vehicle (V2V) Communication Market.

China – 18.9% share

Massive vehicle production capacity, extensive smart city pilots, and large-scale C-V2X deployments position China as a key leader in the Vehicle-To-Vehicle (V2V) Communication Market.

The Vehicle-To-Vehicle (V2V) Communication market exhibits a moderately consolidated yet innovation-driven competitive structure, characterized by the presence of approximately 25–30 active global and regional technology providers. Competition is shaped by rapid standardization around Cellular V2X, deep integration with 5G ecosystems, and increasing collaboration between automotive OEMs, semiconductor manufacturers, and telecom operators. The top five companies collectively account for nearly 62% of total deployments, reflecting strong concentration in chipset design, embedded software, and system integration capabilities.

Leading players focus heavily on strategic partnerships with vehicle manufacturers and infrastructure providers to secure long-term deployment contracts. Over 70% of competitive initiatives since 2023 have involved joint development agreements, pilot programs, or interoperability testing alliances. Product innovation remains a core differentiator, with more than 45 new V2V-enabled hardware and software platforms launched globally over the last two years. Companies are also investing aggressively in AI-enabled V2V stacks, cybersecurity frameworks, and software-defined vehicle architectures to enhance latency performance and scalability.

Mergers and technology acquisitions account for roughly 18% of recent competitive moves, primarily aimed at expanding C-V2X intellectual property and regional footprint. Overall, competition is shifting from hardware-centric offerings toward integrated V2V ecosystems, where reliability, compliance readiness, and large-scale deployment capability determine market positioning.

Qualcomm Technologies Inc.

NXP Semiconductors

Robert Bosch GmbH

Continental AG

Harman International

Autotalks

Huawei Technologies Co., Ltd.

Denso Corporation

Infineon Technologies AG

Savari Inc.

The Vehicle-To-Vehicle (V2V) Communication market is being fundamentally shaped by the convergence of advanced wireless communication protocols, edge computing, and AI-enabled vehicle systems. Cellular Vehicle-to-Everything (C-V2X) has emerged as the leading communication standard, deployed in over 58% of new V2V-enabled vehicles in 2024, offering up to 35% lower latency and 40% higher reliability compared to legacy DSRC systems. DSRC still maintains a presence in legacy fleets and regional pilot programs, covering roughly 27% of existing V2V deployments. Hybrid systems combining C-V2X and DSRC are gaining traction, representing about 15% of total market adoption, mainly in transition zones and interoperability testing corridors. Edge computing and AI integration are enhancing real-time decision-making and cooperative safety functions. Approximately 45% of new commercial fleet deployments process V2V data locally to reduce end-to-end latency and improve hazard detection by up to 28%. Software-defined vehicle platforms and over-the-air update capabilities enable rapid deployment of new safety features and protocol upgrades across large vehicle fleets.

Emerging technologies such as 5G-V2X connectivity, AI-driven predictive collision avoidance, and blockchain-based data security frameworks are gaining momentum. Several smart city initiatives now incorporate V2V data into traffic signal optimization, reducing average intersection delays by 20–25%. Advanced sensor fusion, including lidar, radar, and camera integration with V2V networks, is driving improvements in cooperative adaptive cruise control and platooning applications. The market is also witnessing significant investments in cybersecurity and functional safety technologies, with over 60% of deployed systems including encrypted communication and authentication layers. These technological advancements collectively position V2V systems as critical enablers of connected, autonomous, and safe mobility infrastructure, while allowing OEMs and fleet operators to enhance operational efficiency, regulatory compliance, and consumer trust.

• In February 2024, Autotalks collaborated with Rohde & Schwarz and Keysight Technologies to verify its 5G‑V2X system‑on‑a‑chip (SoC), strengthening performance validation for next‑generation V2V communication chips designed for low latency and high reliability across connected vehicle networks. (Auto Talks)

• In June 2025, Qualcomm Technologies completed its acquisition of Autotalks, integrating a leader in direct V2X solutions to enhance C‑V2X deployment, bolster road safety communications, and support advanced automated driving features across global vehicle platforms. (Qualcomm)

• In 2024, Infineon Technologies introduced a new series of automotive‑grade V2X chipsets optimized for advanced driver assistance systems, emergency vehicle notification, and autonomous driving communication, emphasizing low power consumption and compatibility with both DSRC and C‑V2X standards.

• In October 2025, General Motors announced that its Super Cruise hands‑free driving system surpassed 500,000 active users and logged over 700 million hands‑free miles without a single crash attributed to the system, demonstrating high reliability and validating connected vehicle technology performance. (GM News)

The Vehicle‑To‑Vehicle (V2V) Communication Market Report presents a comprehensive examination of the connected vehicle communication ecosystem, encompassing technology types, application domains, and end‑user segments across global regions. It analyzes the technical segmentation between communication protocols such as Dedicated Short‑Range Communication (DSRC), Cellular Vehicle‑to‑Everything (C‑V2X), and hybrid solutions, detailing deployment characteristics, interoperability aspects, and hardware/software platform adoption patterns. The report elaborates on application areas including road safety and collision avoidance, traffic efficiency and congestion management, cooperative autonomous driving support, emergency coordination systems, and fleet communication frameworks.

Geographic coverage extends through North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa, offering insights into regional infrastructure readiness, regulatory frameworks, and localized consumer behavior influencing V2V uptake. Detailed assessments of key markets such as the United States, China, Germany, Japan, and Brazil provide context on production capacity, smart city initiatives, and pilot corridor deployments that shape regional dynamics.

The report also explores technological drivers such as 5G‑V2X integration, edge computing and AI analytics, security and encryption frameworks, and sensor fusion with radar/lidar/camera systems. Included are end‑user analyses across passenger OEMs, commercial fleets, public transport authorities, and aftermarket upgrade opportunities. Additionally, niche segments such as two‑wheeler and micro‑mobility V2V applications, retrofitting solutions, and cloud‑based data services are examined to highlight emerging avenues for market expansion. The scope synthesizes quantitative deployment figures and qualitative industry insights to support strategic decision‑making by stakeholders in automotive, telecommunications, infrastructure, and policy domains.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 28812.22 Million |

Market Revenue in 2032 | USD 70830.03 Million |

CAGR (2025 - 2032) | 11.9% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Qualcomm Technologies Inc. , NXP Semiconductors , Robert Bosch GmbH, Continental AG, Harman International , Autotalks, Huawei Technologies Co., Ltd., Denso Corporation, Infineon Technologies AG, Savari Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |