Reports

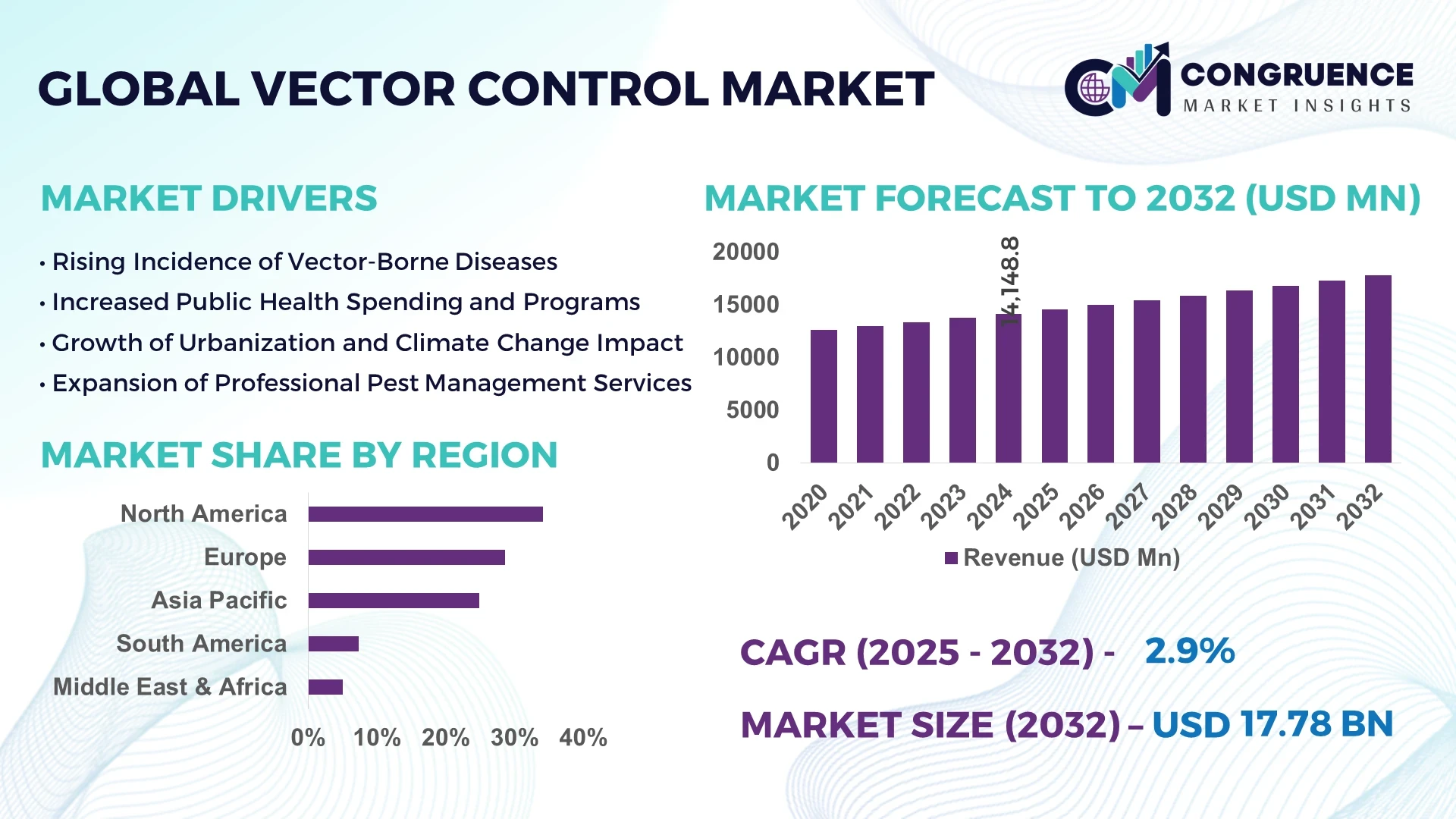

The Global Vector Control Market was valued at USD 14,148.75 Million in 2024 and is anticipated to reach a value of USD 17,784.47 Million by 2032 expanding at a CAGR of 2.9% between 2025 and 2032.

The United States continues to lead the global vector control industry due to its advanced production capacity in biopesticides, strong investment in mosquito-borne disease research, government-backed urban pest eradication programs, and adoption of high-tech monitoring systems in public health and agriculture sectors.

The Vector Control Market is increasingly driven by demand across key sectors such as public health, agriculture, livestock management, and waste management. Innovations in insecticide delivery systems, such as drone-assisted larvicide spraying and spatial repellents, are transforming operational protocols across urban and rural control programs. Environmentally compliant regulations are accelerating the use of biological vector control agents over chemical counterparts, particularly in regions with high ecological sensitivity. Urbanization in Asia-Pacific and Africa is driving consumption, where integrated pest management strategies are becoming essential. Additionally, rising vector-borne diseases, including dengue, Zika, and malaria, are reinforcing long-term government contracts with vector control firms. The market is also seeing an uptick in smart surveillance technology adoption and GIS-based mapping systems for real-time tracking and intervention planning. These trends collectively enhance operational efficiency and forecast a strong future outlook for the global vector control industry.

Artificial Intelligence is revolutionizing the Vector Control Market by enabling predictive modeling, real-time surveillance, and autonomous deployment of control interventions. AI-driven platforms are optimizing pest identification through image recognition and geospatial analysis, allowing faster and more precise responses to outbreaks. These advancements are especially crucial in high-risk zones where vector-borne diseases are escalating due to climate variability and population density.

In the Vector Control Market, AI is streamlining operations for public health agencies and commercial pest control firms. For instance, smart traps integrated with AI sensors can now detect specific species like Aedes aegypti mosquitoes and transmit data to cloud-based dashboards. This real-time vector activity mapping allows field teams to deploy targeted biological or chemical treatments more efficiently, reducing both cost and pesticide usage. Additionally, AI-based forecasting models are helping authorities anticipate disease hotspots before they emerge by analyzing historical outbreak data, humidity levels, rainfall, and temperature fluctuations.

AI-enabled drones are also transforming ground coverage by automating larvicide application across uneven terrains and stagnant water bodies, thereby improving coverage uniformity. Moreover, machine learning algorithms support decision-making in vector resistance management by analyzing genetic and ecological variables. The Vector Control Market is increasingly embracing AI as a core component in sustainable, large-scale pest management frameworks.

“In March 2024, a Florida-based public health department implemented an AI-powered mosquito surveillance system that reduced response time by 40% and improved outbreak prediction accuracy by 36%, using deep learning models trained on historical weather and vector data.”

The Vector Control Market is undergoing significant transformation driven by public health concerns, environmental regulations, and advancements in monitoring technologies. Increasing incidences of mosquito-borne diseases such as malaria, dengue, and chikungunya have led to a surge in demand for integrated pest management solutions across tropical and subtropical regions. Governmental agencies and international health organizations are scaling up investments in proactive and preventative vector management programs. Moreover, a shift toward eco-friendly biological control agents, including bacteria-based larvicides and sterile insect techniques, is reshaping industry strategies. Technological advancements such as AI-driven surveillance systems, autonomous drones, and GIS-integrated mapping tools are improving the speed and precision of interventions. Simultaneously, climate change is altering vector habitats, requiring adaptive and scalable vector control methods. The market’s evolution is marked by a growing emphasis on operational efficiency, targeted solutions, and sustainable practices across urban and rural landscapes.

Expanding public health infrastructure in developing regions is fueling the growth of the Vector Control Market. Governments in Asia-Pacific and Sub-Saharan Africa are increasingly integrating vector control strategies into national health policies to combat rising disease outbreaks. In India, for instance, over 150 million mosquito nets were distributed under public health schemes in 2024 alone, significantly boosting demand for insecticidal-treated materials. African nations such as Nigeria and Kenya have launched widespread larviciding and community-based spraying programs. This increased government spending on public sanitation and pest control not only drives consumption of chemical and biological vector agents but also stimulates innovation in low-cost delivery mechanisms and training programs for field personnel.

The growing resistance of vectors to commonly used insecticides presents a critical restraint for the Vector Control Market. Continuous use of synthetic pyrethroids and organophosphates has led to the development of resistant mosquito strains, particularly in Southeast Asia and Latin America. This resistance undermines the effectiveness of standard interventions and compels authorities to rotate chemical classes or shift to more expensive biological alternatives. For example, a 2024 entomological study found that over 70% of tested Aedes mosquito populations in Brazil exhibited resistance to at least one major insecticide class. As a result, control programs are facing rising costs and logistical complexity in maintaining efficacy, thereby restraining market growth and scalability.

The advent of smart vector surveillance systems offers significant growth potential for the Vector Control Market. AI-powered devices, such as sensor-enabled traps and cloud-connected monitoring platforms, allow authorities to predict vector outbreaks with high precision. These systems utilize real-time data inputs from environmental sensors, citizen reports, and historical patterns to enable targeted interventions, reducing chemical usage and improving response speed. In 2025, several municipal bodies across Europe and North America began deploying AI-based larvicide drones and IoT-enabled mosquito traps that automatically alert control centers when vector activity spikes. This shift toward data-driven pest management represents a lucrative opportunity for technology providers and public health contractors alike.

Stringent regulatory compliance is a key challenge hampering agility in the Vector Control Market. All new biopesticides, chemical formulations, and application devices must undergo rigorous testing and approval across multiple regional and international agencies. For instance, gaining approval from the U.S. Environmental Protection Agency or European Chemicals Agency can take several years and requires extensive environmental impact assessments, toxicity studies, and field trials. Such delays often restrict the timely market introduction of novel solutions. Additionally, variations in regulatory frameworks across countries complicate the global expansion of vector control companies, raising the cost of compliance and creating hurdles for smaller players seeking market entry or partnerships.

• Surge in Biopesticide Adoption Across Urban Regions: There is a measurable shift toward biopesticides in the Vector Control Market, particularly within urban environments concerned with environmental sustainability. Cities across Europe and Latin America are phasing out chemical-based larvicides and instead deploying bacteria-derived biocontrol agents such as Bacillus thuringiensis israelensis (Bti). In 2024, over 25 major metropolitan health departments in Europe transitioned to biopesticide use in public vector management programs. This shift is enabling safer vector mitigation with minimized ecological disruption and lower toxicity to non-target species, while also fulfilling new municipal green procurement mandates.

• Integration of Drone Technology in Larviciding Operations: Drone-enabled larvicide spraying is gaining widespread traction in rural and flood-prone zones, helping to reach stagnant water bodies and swamps that are otherwise inaccessible. In 2024, more than 40% of vector control operations in Southeast Asia incorporated unmanned aerial vehicles (UAVs) for precise chemical and biological agent deployment. This automation is increasing area coverage by over 60% and cutting labor costs by 30% on average, accelerating adoption among government-led disease prevention programs.

• GIS-Based Vector Surveillance Expansion: Geographic Information System (GIS) integration into vector control frameworks has surged, particularly in Africa and Southeast Asia. Governments are now employing satellite data and geospatial analytics to map vector density, migration patterns, and high-risk transmission corridors. In 2025, over 18 national vector control agencies reported the implementation of GIS-enhanced dashboards to monitor Aedes and Anopheles populations. These tools enable predictive decision-making, route optimization for spray vehicles, and strategic resource allocation, contributing to increased operational efficiency.

• Regulatory Push for Insecticide Rotation Strategies: With rising insecticide resistance, international regulatory bodies are enforcing more stringent insecticide rotation protocols. In 2024, over 70 countries updated their national guidelines to mandate alternation among at least three different classes of insecticides. This trend is prompting manufacturers to diversify product portfolios and introduce novel chemical compounds. It’s also encouraging investment in resistance surveillance tools and diagnostic kits, which are increasingly becoming standard requirements in government procurement contracts.

The Vector Control Market is segmented by type, application, and end-user, each demonstrating unique consumption behavior and adoption trends. By type, the market includes chemical, biological, and mechanical vector control products, with chemical-based solutions currently dominating but biological agents showing rapid growth. Application segmentation comprises areas such as public health, agriculture, commercial buildings, industrial zones, and residential premises. Among these, public health applications are most prominent, driven by vector-borne disease mitigation programs globally. End-user segmentation includes government agencies, private pest control firms, agriculture bodies, and non-governmental organizations, with government institutions accounting for a large portion of demand due to their extensive urban and rural intervention projects. Each segment reflects distinct operational needs and budget structures, making this segmentation critical for manufacturers and service providers tailoring their offerings to specific market niches.

Chemical-based vector control agents continue to dominate the market due to their broad-spectrum efficacy, rapid action, and availability in various formulations such as aerosols, sprays, and foggers. These agents are especially prevalent in emergency interventions during outbreaks of diseases like malaria and dengue. However, biological vector control agents are emerging as the fastest-growing segment, driven by rising environmental regulations and public demand for non-toxic, sustainable solutions. Biopesticides and larvicidal bacteria such as Bacillus thuringiensis are increasingly deployed in urban green zones and eco-sensitive areas. Mechanical control methods, including mosquito traps and netting systems, occupy a niche yet growing segment, especially in household and commercial settings. Innovations in smart trap technology and wearable repellent devices are also contributing to this segment’s evolution. Manufacturers are now offering hybrid product lines combining chemical and biological components to meet complex regulatory and environmental requirements across different regions.

Public health remains the leading application segment within the Vector Control Market due to the persistent threat of vector-borne diseases, particularly in densely populated countries in Asia and Africa. National malaria and dengue control programs, often backed by international aid, are fueling bulk procurement of insecticides, larvicides, and surveillance technologies. The fastest-growing application segment is commercial real estate and hospitality, where maintaining pest-free environments has become a top priority for compliance and customer experience. Hotels, resorts, and shopping complexes are increasingly investing in proactive vector control measures, including automated repellent systems and integrated pest management (IPM) frameworks. Agricultural applications also hold a significant position, particularly in tropical regions where crop damage due to vectors impacts food security. Moreover, industrial and residential sectors continue to adopt modern vector control solutions, although on a relatively smaller scale compared to government-led interventions.

Government health departments and public institutions are the leading end-users in the Vector Control Market. These bodies are responsible for executing large-scale eradication programs, epidemic response actions, and community health campaigns. In 2024, over 60% of total procurement in the sector was attributed to government agencies, reflecting their dominant operational footprint. The fastest-growing end-user category is private pest control companies, which are increasingly contracted by municipalities and commercial establishments for outsourced services. These firms are benefiting from the adoption of AI-driven equipment and remote surveillance systems, enabling scalable operations with reduced human resource dependencies. Non-governmental organizations and international development bodies also play a vital role, particularly in regions affected by humanitarian crises and poor public health infrastructure. Additionally, end-users from the agriculture sector are increasingly implementing integrated vector management strategies to minimize crop loss, especially in export-oriented economies facing phytosanitary regulations.

North America accounted for the largest market share at 34.1% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 3.6% between 2025 and 2032.

North America’s dominance is fueled by well-established public health infrastructure, widespread adoption of vector surveillance systems, and consistent governmental investment in disease prevention. Meanwhile, the Asia-Pacific region is undergoing rapid transformation driven by increasing urbanization, frequent vector-borne outbreaks, and rising governmental funding for pest control technologies.

The global Vector Control Market shows strong regional fragmentation, with differing levels of industrialization, climate exposure, and regulatory maturity shaping demand patterns. In North America, vector control is a mature market with large-scale implementations in residential and commercial sectors. Europe follows closely, shaped by environmental compliance mandates and urban sustainability goals. Asia-Pacific is seeing an uptick in vector-borne disease prevalence, fueling demand for scalable larvicide deployment and AI-based monitoring platforms. In South America, Brazil leads efforts with state-led programs targeting mosquito-borne disease mitigation. Meanwhile, the Middle East & Africa region is expanding vector control initiatives in alignment with infrastructure projects and health modernization programs. Regional disparities in technology access, insecticide resistance, and ecological conditions make tailored product offerings essential to success across these global segments.

Innovative Surveillance and Targeted Vector Elimination Programs Fuel Growth

North America held a significant 34.1% share of the global Vector Control Market in 2024, driven primarily by the United States and Canada. The public health sector remains the primary end-user, with increased investments in mosquito and rodent control strategies across both urban and rural communities. Advanced technologies such as AI-integrated mosquito traps and drone-assisted pesticide deployment are widely adopted across several U.S. states. Regulatory actions, such as EPA mandates for insecticide rotations and sustainability evaluations, are influencing market offerings. Additionally, emergency response funding from federal bodies is accelerating the rollout of scalable larvicide campaigns. Public-private partnerships have further enhanced innovation, leading to more effective surveillance programs supported by GIS and cloud-based systems.

Eco-Conscious Policy Shifts and Biopesticide Innovation Drive Market Expansion

Europe captured 28.6% of the Vector Control Market in 2024, led by Germany, the UK, and France. This region is witnessing rapid growth in biopesticide utilization due to its stringent environmental directives. The European Chemicals Agency (ECHA) has enforced limitations on certain synthetic compounds, prompting a shift toward bacteria-based larvicides and botanical repellents. Sustainability-driven regulations are encouraging adoption of non-toxic vector control methods in municipalities and agricultural sectors. Leading pest control companies are innovating with biodegradable product lines and IoT-connected traps. Additionally, local governments are funding digital transformation programs to replace manual pest surveillance with automated vector tracking and reporting systems.

Explosive Urbanization and Disease Control Efforts Stimulate Advanced Control Mechanisms

The Asia-Pacific region ranked second in terms of volume consumption in 2024 and is projected to become the fastest-expanding Vector Control Market. China, India, and Japan are the key countries contributing to this surge, driven by large populations, rapid urban sprawl, and tropical climates conducive to vector proliferation. India's government-led Smart Cities initiative has integrated vector management into urban planning, increasing procurement of drones and GIS-based pest control platforms. China continues to invest in large-scale biopesticide manufacturing and thermal fogging technologies to combat dengue outbreaks. Japan focuses on AI and robotics-based control tools for maintaining high public sanitation standards. These trends reflect a tech-forward, high-demand environment for next-gen vector control solutions.

Government Interventions and Urban Disease Mitigation Programs Bolster Growth

Brazil and Argentina are the top contributors in this region, which accounted for approximately 7.4% of the Vector Control Market in 2024. Government-funded initiatives in Brazil have expanded vector control coverage through nationwide spraying programs and public education campaigns. In Argentina, increasing dengue cases have triggered multi-city deployments of advanced fogging systems and community mosquito reduction efforts. The market is also supported by demand from energy and construction projects requiring pest control compliance in remote operational areas. Trade-friendly policies and health-focused infrastructure improvements are fostering cross-border collaborations for vector control product distribution and technology transfer.

Infrastructure Development and Health Reforms Propel Vector Control Demand

In 2024, this region represented 6.3% of the global Vector Control Market, led by countries such as the UAE, South Africa, and Kenya. Demand is largely driven by urban infrastructure projects and efforts to modernize public health protocols. The oil & gas and construction sectors are required to implement vector mitigation measures to comply with environmental health regulations. Governments are introducing national disease eradication programs and adopting modern larvicide equipment, AI-based mapping tools, and community vector surveillance initiatives. Regulatory harmonization across the Gulf Cooperation Council (GCC) nations is also improving product approval timelines and supporting private sector expansion into underserved areas.

United States – 31.4% market share

High production capacity, strong government health mandates, and advanced surveillance infrastructure support its dominance in the Vector Control Market.

China – 17.2% market share

Strong end-user demand and large-scale implementation of vector control in urban and peri-urban areas drive its leadership position globally.

The Vector Control Market exhibits a moderately fragmented competitive landscape with over 60 globally active players offering diverse vector management solutions across chemical, biological, and mechanical categories. Industry competition is fueled by ongoing innovation, regulatory adaptation, and region-specific service capabilities. Leading players maintain strong presence in high-demand regions through robust distribution networks and long-term contracts with government and public health agencies. Mid-sized and emerging firms are increasingly penetrating niche markets by offering eco-friendly alternatives and smart technology-enabled solutions.

Strategic partnerships and public-private collaborations are reshaping the competitive dynamics, especially in disease-prone geographies. For instance, several firms are partnering with municipal governments to roll out AI-based vector surveillance systems and drone-assisted larviciding programs. Mergers and acquisitions are also playing a significant role, as companies aim to consolidate regional market shares and expand technology portfolios. Notable innovation trends include automated fogging systems, biodegradable repellents, and IoT-enabled mosquito traps. The ability to align with evolving regulatory frameworks and provide scalable, tech-driven solutions is emerging as a key differentiator among top-tier competitors.

Bayer AG

BASF SE

Rentokil Initial PLC

UPL Limited

Sumitomo Chemical Co., Ltd.

Thermacell Repellents, Inc.

Vestergaard Frandsen SA

MGK (McLaughlin Gormley King Company)

PelGar International Ltd

Bell Laboratories Inc.

The Vector Control Market is witnessing rapid technological evolution, particularly in the areas of automation, bioengineering, and smart surveillance. One of the most notable advances is the integration of AI and machine learning into vector identification and activity forecasting. AI-powered traps equipped with image recognition sensors now detect mosquito species in real-time, enabling immediate and targeted intervention. These systems are increasingly deployed in urban environments, significantly reducing manual labor and enhancing the precision of chemical application.

Drones have also revolutionized larvicide deployment, especially in flood-prone or densely vegetated areas. Equipped with GPS and sensor-based navigation, these UAVs can distribute larvicides across wide areas within a fraction of the time required by ground teams. In 2024, drone deployment efficiency was reported to improve field coverage by 50% in remote vector hotspots. Additionally, the use of GIS-based platforms allows authorities to visualize disease outbreak zones and optimize spray routes accordingly, boosting intervention impact and resource efficiency.

On the chemical front, the shift toward biologically derived insecticides, including bacteria-based larvicides and pheromone disruptors, is gaining momentum. These formulations reduce toxicity while maintaining effectiveness. Also emerging are wearable vector repellents and biodegradable control products designed for eco-sensitive environments. The combined advancement in digital tools, eco-conscious formulations, and automation is reshaping the operational and strategic approach to modern vector control.

• In February 2023, Rentokil Initial partnered with Bayer to pilot AI-powered mosquito surveillance traps in select U.S. cities, resulting in a 45% reduction in response time for outbreak control teams using real-time species identification data.

• In August 2023, India’s Ministry of Health deployed over 300 drone units for larvicide spraying across flood-affected districts, achieving 60% faster coverage compared to traditional methods and extending reach to previously inaccessible areas.

• In April 2024, Thermacell Repellents launched a new biodegradable mosquito repellent device targeting eco-tourism markets, offering 12-hour protection using a botanical formula and reducing plastic waste by over 70% compared to earlier models.

• In January 2024, South Africa’s National Department of Health rolled out GIS-integrated vector surveillance software across five provinces, enhancing disease prediction accuracy by 38% through geospatial analysis and historical outbreak data modeling.

The Vector Control Market Report offers a comprehensive analysis of technologies, market segments, and regional dynamics influencing the global industry. It provides detailed coverage across product types including chemical agents, biological control solutions, and mechanical devices such as traps and barriers. The report segments the market based on application areas such as public health, agriculture, commercial properties, industrial zones, and residential settings. End-users profiled include government agencies, private pest control firms, NGOs, and agricultural bodies, each with distinct procurement patterns and operational needs.

Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting consumption behavior, regulatory trends, and infrastructure developments across each region. It also includes insights into emerging countries such as India, Brazil, and South Africa, where rising urbanization and disease outbreaks are intensifying demand.

The technological landscape section covers advancements in AI-powered surveillance systems, UAV-based larvicide delivery, GIS-integrated intervention platforms, and biodegradable repellent technologies. Additionally, the report identifies niche markets such as wearable repellents and smart traps tailored to the hospitality and eco-tourism sectors. It serves as a strategic tool for stakeholders seeking to understand the operational, regulatory, and technological intricacies shaping the Vector Control Market globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 14148.75 Million |

|

Market Revenue in 2032 |

USD 17784.47 Million |

|

CAGR (2025 - 2032) |

2.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bayer AG, BASF SE, Rentokil Initial PLC, UPL Limited, Sumitomo Chemical Co., Ltd., Thermacell Repellents, Inc., Vestergaard Frandsen SA, MGK (McLaughlin Gormley King Company), PelGar International Ltd, Bell Laboratories Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |