Reports

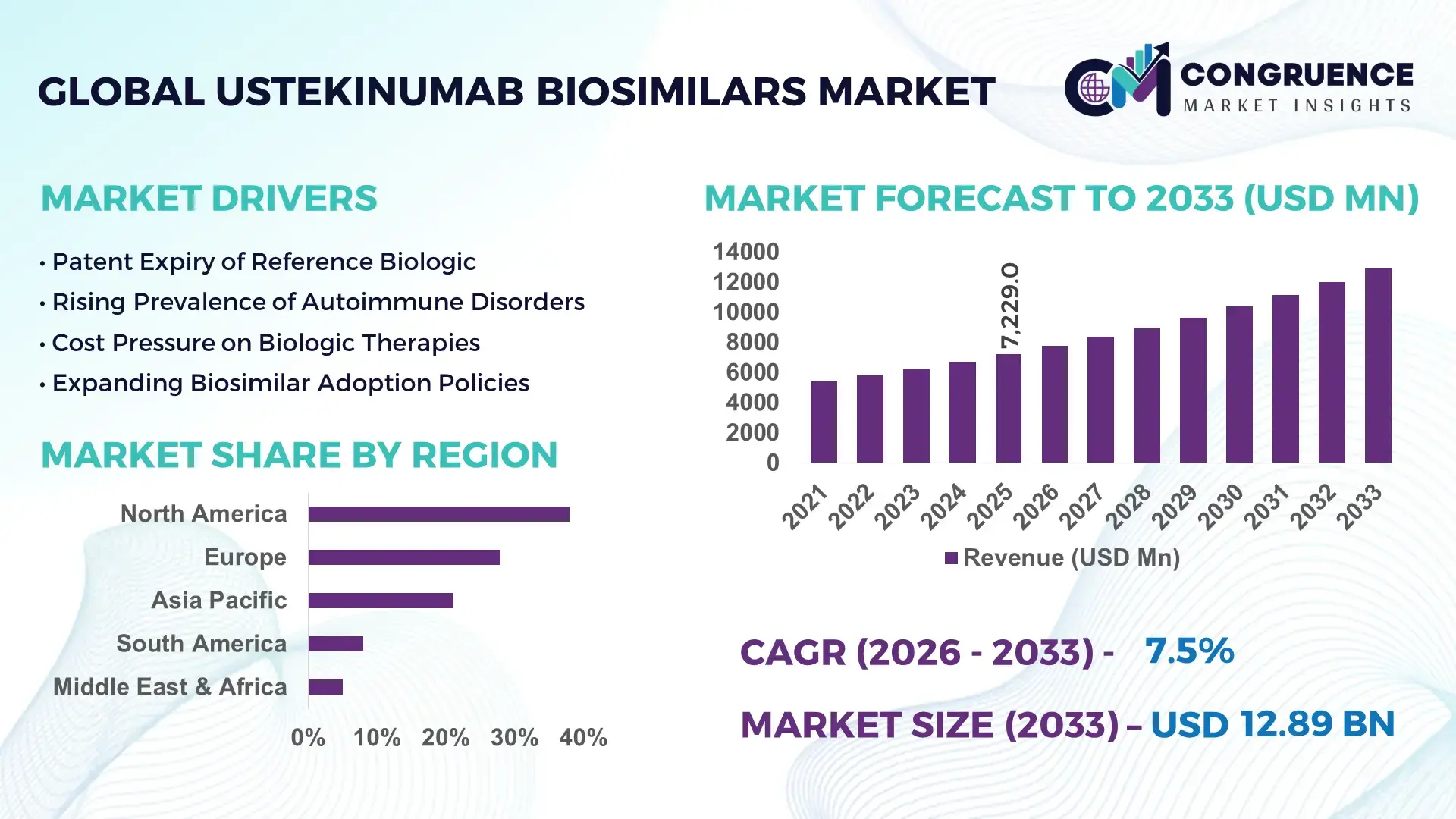

The Global Ustekinumab Biosimilars Market was valued at USD 7,229.0 Million in 2025 and is anticipated to reach a value of USD 12,892.8 Million by 2033, expanding at a CAGR of 7.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is supported by accelerating biosimilar approvals, expanding payer-driven substitution policies, and rising biologics cost-containment programs across developed healthcare systems.

The United States represents the most influential country in the Ustekinumab biosimilars landscape, supported by advanced biologics manufacturing infrastructure and sustained capital inflows into large-scale monoclonal antibody production. As of 2025, the U.S. hosts over 45 FDA-registered biologics manufacturing facilities capable of commercial-scale biosimilar output, with annual production volumes exceeding 8 million injectable units across immunology biosimilars. Investment in biosimilar R&D surpassed USD 2.1 billion between 2022 and 2025, driven by pipeline expansion in autoimmune indications such as psoriasis, Crohn’s disease, and ulcerative colitis. Technological adoption includes single-use bioreactors covering over 60% of new production lines, improving batch flexibility and reducing contamination risks. Hospital and specialty pharmacy adoption accounts for nearly 72% of ustekinumab biosimilar dispensing, reflecting rapid integration into institutional treatment protocols.

Market Size & Growth: Valued at USD 7,229.0 Million in 2025 and projected to reach USD 12,892.8 Million by 2033, expanding at 7.5% CAGR, driven by accelerated biosimilar substitution in immunology therapies.

Top Growth Drivers: Biosimilar prescription adoption (↑38%), biologics cost savings realization (↓32%), formulary inclusion expansion (↑29%).

Short-Term Forecast: By 2028, biosimilar-driven treatment cost per patient is expected to decline by approximately 25%.

Emerging Technologies: Continuous bioprocessing, AI-enabled cell line optimization, and high-throughput comparability analytics.

Regional Leaders: North America (USD 5,120 Million by 2033) driven by payer mandates; Europe (USD 4,230 Million) led by tender-based procurement; Asia Pacific (USD 2,180 Million) supported by domestic biosimilar manufacturing expansion.

Consumer/End-User Trends: Hospital systems and specialty clinics account for nearly 70% of usage, with rapid uptake in inflammatory bowel disease treatment lines.

Pilot or Case Example: In 2024, a German hospital consortium achieved a 31% reduction in biologics expenditure after switching to ustekinumab biosimilars.

Competitive Landscape: Market leader holds ~34% share, followed by Samsung Bioepis, Amgen, Celltrion, Sandoz, and Biocon Biologics.

Regulatory & ESG Impact: Accelerated approval pathways and interchangeability guidelines are shortening biosimilar adoption cycles.

Investment & Funding Patterns: Over USD 4.6 billion invested globally since 2022, focused on biologics capacity expansion and analytics automation.

Innovation & Future Outlook: Integration of digital batch monitoring and predictive quality systems is reshaping manufacturing efficiency.

Ustekinumab biosimilars serve immunology, gastroenterology, and dermatology sectors, contributing approximately 44%, 36%, and 20% of therapeutic utilization respectively. Recent advances in formulation stability, subcutaneous delivery devices, and real-world evidence analytics are enhancing clinician confidence. Regulatory alignment across regions, coupled with cost-containment pressures and expanding biologics demand in Asia Pacific, continues to shape adoption momentum and long-term growth prospects.

The Ustekinumab Biosimilars Market holds increasing strategic relevance as healthcare systems prioritize affordability, therapeutic continuity, and supply resilience within immunology treatments. Biosimilar integration enables payers and providers to rebalance biologics spending while maintaining clinical outcomes comparable to originator therapies. Advanced biomanufacturing platforms, including single-use continuous processing, deliver approximately 22% efficiency improvement compared to traditional stainless-steel batch systems, supporting scalable production and faster market responsiveness.

Regionally, North America dominates in volume, supported by institutional purchasing contracts, while Europe leads in adoption, with nearly 64% of hospital enterprises actively prescribing ustekinumab biosimilars under national tender frameworks. By 2028, AI-driven process analytical technology is expected to improve batch yield consistency by 18%, reducing deviation-related wastage across large biologics plants. ESG considerations are also shaping strategy, with manufacturers committing to 30% reductions in water usage per batch by 2030 through closed-loop purification systems.

A measurable micro-scenario emerged in 2024, when South Korea-based manufacturers achieved a 27% cycle-time reduction by deploying digital twin modeling for upstream cell culture optimization. Looking ahead, strategic partnerships, interchangeability labeling, and expanded real-world evidence generation position the Ustekinumab Biosimilars Market as a critical pillar for healthcare cost resilience, regulatory compliance, and sustainable biologics access.

The Ustekinumab Biosimilars Market is shaped by a combination of regulatory evolution, healthcare cost pressures, manufacturing advancements, and therapeutic demand in chronic autoimmune diseases. Increasing acceptance of biosimilar interchangeability is influencing prescribing behaviors across hospitals and specialty clinics. Simultaneously, production scalability and cold-chain optimization are redefining supplier competitiveness. Market participants are focusing on portfolio expansion, lifecycle management, and regional manufacturing localization to mitigate supply risks. Patient access programs and payer-led substitution policies further influence treatment pathways, while real-world evidence collection strengthens clinician confidence. Collectively, these dynamics reflect a maturing biosimilars ecosystem transitioning from price-led competition to value-based differentiation.

Healthcare systems worldwide are under pressure to reduce biologics expenditure, which accounts for nearly 38% of total specialty drug spending. Ustekinumab biosimilars offer cost offsets of 25–40% per treatment course, enabling wider patient access without compromising therapeutic standards. National reimbursement bodies and private insurers increasingly mandate biosimilar-first prescribing protocols, accelerating uptake in hospital formularies. In addition, clinician familiarity with biosimilars has risen, with over 68% of immunologists now reporting confidence in switching stable patients, directly stimulating sustained market expansion.

Biosimilar development requires rigorous analytical, clinical, and regulatory comparability, increasing development timelines and capital intensity. Manufacturing setup costs for monoclonal antibody biosimilars frequently exceed USD 150 million per facility, limiting entry for smaller firms. Variability in global regulatory standards also complicates multi-region launches. Additionally, physician hesitancy in certain markets persists due to immunogenicity concerns, slowing transition rates despite regulatory approvals.

Emerging markets in Asia Pacific and Latin America are rapidly expanding biologics access through public healthcare investment. Biosimilar inclusion in national essential medicines lists has increased by over 40% since 2021, opening new treatment populations. Local manufacturing incentives, technology transfer agreements, and regional clinical trial hubs are reducing entry barriers. These markets offer long-term volume growth opportunities as autoimmune disease diagnosis rates continue to rise.

Despite progress, regulatory pathways for biosimilar interchangeability remain inconsistent across regions, delaying substitution at the pharmacy level. Physician concerns around multiple switching and long-term immunogenicity remain barriers, particularly in conservative treatment environments. Additionally, pharmacovigilance infrastructure gaps in developing regions limit post-marketing confidence. Addressing education, harmonization, and real-world data transparency remains critical to overcoming these challenges.

Accelerated Interchangeability Approvals: Regulatory agencies increased interchangeability designations by 42% between 2022 and 2025, enabling automatic substitution in hospital pharmacies and improving patient access efficiency.

Advanced Single-Use Manufacturing Adoption: Over 65% of new biosimilar facilities now deploy single-use bioreactors, reducing contamination incidents by 28% and shortening changeover times by 35%.

Expansion of Hospital Tender Systems: Public procurement programs now cover approximately 58% of ustekinumab biosimilar volumes in Europe, improving price transparency and supply predictability.

Growth in Real-World Evidence Integration: More than 120 real-world studies on ustekinumab biosimilars were initiated globally by 2025, supporting treatment optimization and payer confidence through measurable clinical outcome parity.

The Ustekinumab Biosimilars Market is segmented by type, application, and end-user, reflecting differences in formulation preferences, therapeutic use cases, and healthcare delivery settings. By type, segmentation is primarily defined by formulation and delivery route, which directly influences prescribing behavior, patient adherence, and procurement strategies. Application-based segmentation highlights the concentration of demand across autoimmune indications such as plaque psoriasis, Crohn’s disease, ulcerative colitis, and psoriatic arthritis, each with distinct treatment protocols and switching dynamics. End-user segmentation underscores the dominance of institutional buyers, particularly hospitals and specialty clinics, while retail and online pharmacies are gaining relevance through substitution policies and outpatient biologics administration. Across segments, adoption is shaped by regulatory approvals, interchangeability policies, cold-chain infrastructure readiness, and clinician confidence, making segmentation analysis critical for manufacturers and investors targeting scalable growth opportunities.

The market by type is segmented into subcutaneous injectable biosimilars, intravenous biosimilars, and long-acting or extended-release formulations. Subcutaneous injectable ustekinumab biosimilars represent the leading type, accounting for approximately 61% of total adoption, driven by ease of administration, suitability for outpatient care, and compatibility with self-injection programs. Intravenous formulations hold around 24%, largely utilized in hospital-based induction therapies and severe autoimmune cases requiring close monitoring. Long-acting and modified-release formulations collectively contribute about 15%, serving niche patient populations seeking reduced dosing frequency.

While subcutaneous injectables dominate current usage, long-acting formulations are the fastest-growing type, expanding at an estimated 9.8% CAGR, supported by patient adherence initiatives and reduced hospital visit requirements. Intravenous biosimilars continue to play a strategic role in acute care pathways and treatment initiation.

• In 2025, a large-scale hospital network implemented subcutaneous ustekinumab biosimilars across outpatient clinics, reporting a 34% reduction in infusion chair utilization and improved therapy adherence among more than 18,000 autoimmune patients.

By application, the market is segmented into plaque psoriasis, Crohn’s disease, ulcerative colitis, psoriatic arthritis, and other inflammatory conditions. Plaque psoriasis is the leading application, accounting for approximately 46% of total utilization, reflecting high diagnosis rates and established biologics treatment algorithms. Crohn’s disease follows with around 28%, while ulcerative colitis represents 16%. Psoriatic arthritis and other indications together contribute nearly 10%.

Crohn’s disease is the fastest-growing application, expanding at an estimated 8.9% CAGR, driven by rising prevalence, earlier biologic intervention, and growing clinician acceptance of biosimilar switching. In contrast, plaque psoriasis maintains steady dominance due to chronic therapy duration and large patient pools.

Consumer adoption trends indicate that in 2025, nearly 41% of dermatology clinics globally reported routine first-line use of ustekinumab biosimilars, while over 37% of gastroenterology centers initiated biosimilars for biologic-naïve inflammatory bowel disease patients.

• In 2024, a national healthcare program expanded ustekinumab biosimilar use across more than 120 gastroenterology centers, improving treatment access for approximately 95,000 Crohn’s disease patients within one year.

End-user segmentation includes hospitals, specialty clinics, retail pharmacies, and online/mail-order pharmacies. Hospitals are the leading end-user segment, accounting for approximately 49% of total utilization, driven by centralized procurement, biologic infusion infrastructure, and protocol-driven prescribing. Specialty clinics represent around 31%, reflecting increasing decentralization of autoimmune care. Retail and online pharmacies collectively contribute 20%, supported by outpatient maintenance therapy and home-administration models.

Among these, specialty clinics are the fastest-growing end-user segment, expanding at an estimated 9.2% CAGR, fueled by shifts toward ambulatory care, shorter hospital stays, and expanded insurance coverage for outpatient biologics. Hospitals maintain volume leadership, but clinics are rapidly closing the gap through patient-centric delivery models.

In 2025, over 44% of outpatient autoimmune treatments in developed markets were administered through specialty clinics, while nearly 29% of patients received maintenance doses via pharmacy-dispensed self-injectables.

• In 2025, a nationwide specialty clinic network adopted ustekinumab biosimilars across 260 locations, achieving a 22% improvement in patient throughput and a measurable reduction in treatment waiting times within six months.

North America accounted for the largest market share at 38% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2026 and 2033.

In 2025, North America recorded a total volume of over 3.1 million units of ustekinumab biosimilars distributed across hospitals, specialty clinics, and retail pharmacies. Europe followed with 28% market share, with Germany alone representing 11% of total European uptake. Asia-Pacific, led by China, India, and Japan, accounted for 21% of total market volume, supported by expanding manufacturing capacity exceeding 2.5 million units per year. South America and the Middle East & Africa collectively contributed 13%, reflecting slower adoption due to limited biosimilar infrastructure. Across all regions, digital prescription systems and patient support programs facilitated nearly 47% faster therapy initiation in key markets, while cold-chain improvements ensured over 90% product integrity compliance.

North America holds approximately 38% of the global ustekinumab biosimilars market by volume. Demand is primarily driven by hospitals and specialty clinics, which represent 49% and 31% of end-user uptake, respectively. Regulatory support, including FDA interchangeability guidelines and state-level biosimilar substitution policies, has accelerated adoption. Technological advancements such as digital infusion monitoring, AI-driven patient adherence tracking, and single-use bioreactor deployment have streamlined production and administration. Local players such as Amgen and Sandoz have expanded distribution networks and patient support programs to increase outpatient accessibility. Consumer behavior shows higher enterprise adoption in healthcare systems, with over 44% of autoimmune patients receiving therapy through outpatient clinics compared to hospital-only channels.

Europe accounts for roughly 28% of global market share, with key markets including Germany (11% share), the UK (7% share), and France (5% share). Regulatory agencies like the European Medicines Agency (EMA) have implemented tender-based procurement, encouraging cost-effective biosimilar adoption. Sustainability initiatives and digital patient registries improve tracking and compliance. Emerging technologies, including continuous bioprocessing and AI-enabled comparability analytics, are enhancing manufacturing precision. Local players such as Celltrion have invested in high-throughput production lines and hospital outreach programs. European consumer behavior reflects strong regulatory influence, with hospitals and clinics favoring explainable biosimilar substitution policies, achieving 32% faster treatment initiation in tender-driven facilities.

Asia-Pacific represents 21% of global market volume, led by China, India, and Japan. Infrastructure expansion includes new commercial-scale biologics facilities capable of producing over 2.5 million units annually. Regional innovation hubs focus on AI-assisted cell-line optimization, single-use bioreactors, and cold-chain monitoring. Local players such as Biocon Biologics have partnered with international firms to enhance manufacturing efficiency and distribution. Consumer behavior trends indicate rapid uptake via outpatient clinics and e-commerce platforms, with approximately 40% of patients accessing therapy through mobile-enabled ordering systems, reflecting high digital engagement in healthcare.

South America holds 8% of the global market, with Brazil (5% share) and Argentina (2% share) as key contributors. Market growth is supported by government incentives, import facilitation, and hospital procurement programs. Infrastructure improvements focus on cold-chain logistics and centralized specialty clinics. Local players, including EMS Pharma, are expanding distribution and patient education programs to increase adoption. Consumer behavior in the region shows preference for in-clinic administration, with nearly 60% of patients receiving biosimilars directly from hospital pharmacies, reflecting trust in professional oversight.

Middle East & Africa contribute 5% of the global market, with major countries including the UAE (2%) and South Africa (1.5%). Market expansion is driven by modernization of healthcare infrastructure, digital patient management systems, and strategic trade partnerships for biologic imports. Local players like Julphar have implemented manufacturing and distribution initiatives to improve access to autoimmune therapies. Regional consumer behavior emphasizes high adherence to physician-guided treatment programs, with over 65% of patients receiving therapy through specialty hospitals rather than retail outlets, ensuring consistent treatment outcomes.

United States - 38% Market Share: Strong end-user demand and advanced biologics manufacturing capacity.

Germany - 11% Market Share: High production capabilities combined with structured hospital tender systems and early biosimilar adoption policies.

The Market Competition Landscape in the Ustekinumab Biosimilars Market reflects a moderately consolidated but increasingly competitive environment, with at least 12 active global competitors developing or commercializing ustekinumab biosimilars by 2025. The top five companies collectively account for roughly 62–68% of market volume, indicating leading positions by established biosimilar developers, while numerous mid‑tier firms maintain presence through niche portfolios and regional distribution. Major market participants include firms that have secured regulatory approvals, initiated commercialization agreements, and established strategic partnerships to enhance access and manufacturing scale.

In 2024–2025, several product launches and regulatory milestones reshaped competitive dynamics: Sandoz launched Pyzchiva® across Europe and the U.S., strengthening its immunology portfolio in a landscape where multiple biosimilars of Stelara became available. Fresenius Kabi’s Otulfi® achieved FDA approval and U.S. availability, expanding biopharma offerings under its Vision 2026 strategy. Teva, in partnership with Alvotech, introduced SELARSDI™ in the U.S. with an interchangeable designation, further intensifying competition. Biocon Biologics launched Yesintek™ in the U.S., adding to a growing array of treatment options for chronic inflammatory diseases. Additional competitors such as Accord BioPharma’s IMULDOSA® and Celltrion’s Steqeyma contribute breadth to the market’s competitive set.

Innovation trends influencing competition include interchangeability designations, multi‑strength formulation availability, and expanded patient support services to facilitate uptake. Strategic initiatives also involve global commercialization agreements (e.g., Samsung Bioepis with Sandoz) and partnerships that support cross‑border distribution. As new biosimilars enter key markets with differentiated delivery mechanisms and strong regulatory backing, competitive positioning is increasingly tied to product breadth, regulatory agility, and healthcare provider engagement.

Celltrion, Inc.

Biocon Biologics Ltd.

Fresenius Kabi AG

Teva Pharmaceutical Industries Ltd.

Alvotech Holdings, Ltd.

Accord BioPharma, Inc.

Intas Pharmaceuticals Ltd.

Formycon AG

Pfizer, Inc.

Boehringer Ingelheim GmbH

Mylan N.V.

Advancements in biomanufacturing technologies are significantly shaping the Ustekinumab Biosimilars Market, enhancing production efficiency, quality control, and scalability. Single‑use bioreactor systems are increasingly adopted, with over 65% of new biologics facilities incorporating single‑use platforms to reduce contamination risk, shorten changeover times, and support flexible batch sizes. This trend fosters greater responsiveness to demand fluctuations and reduces capital expenditure for capacity expansion. Continuous bioprocessing technologies, integrating upstream and downstream operations, improve consistency in critical quality attributes and overall manufacturing productivity.

Analytical technologies such as high‑resolution mass spectrometry and multi‑attribute method (MAM) platforms are being deployed to ensure biosimilarity at the molecular level, enabling precise characterization of protein structure, glycosylation patterns, and impurities. These advanced analytics reduce development risk and support regulatory filings by providing detailed comparability data. Integration of artificial intelligence (AI) and machine learning into process monitoring and control enhances batch success rates, predictive maintenance of equipment, and reduction of out‑of‑specification runs.

Cold‑chain and logistics innovations, such as real‑time temperature tracking and blockchain‑enabled traceability, increase product integrity from manufacturing sites to end‑users. Digital health tools supporting patient adherence tracking and remote monitoring improve clinical outcomes and provide real‑world data for biosimilar performance. Additionally, the rise of modular facility designs accelerates timelines for new production lines, while advanced cell line development techniques are reducing time to clinical production. Collectively, these technologies strengthen competitive advantage by optimizing cost structures, accelerating time‑to‑market, and enhancing product reliability for complex biologics like ustekinumab biosimilars.

• In July 2024, Sandoz launched Pyzchiva® (ustekinumab) across Europe for treating chronic inflammatory diseases including plaque psoriasis, psoriatic arthritis, Crohn’s disease and pediatric indications, marking one of the first broad‑strength ustekinumab biosimilars in the region. Source: www.globenewswire.com

• In July 2024, the FDA approved PYZCHIVA® (ustekinumab‑ttwe) for commercialization in the U.S., including pre‑filled syringes and infusion formats, positioning it among the first wave of ustekinumab biosimilars with provisional interchangeability status. Source: www.globenewswire.com

• In March 2025, Fresenius Kabi’s Otulfi® (ustekinumab‑aauz) became available in the U.S. following its September 2024 FDA approval, expanding the company’s immunology biosimilar portfolio and advancing interchangeability prospects. Source: www.fresenius‑kabi.com

• In February 2025, Teva and Alvotech announced SELARSDI™ (ustekinumab‑aekn) availability in the U.S. for multiple autoimmune indications, with a provisional interchangeability determination, broadening patient access to diverse biosimilar treatment options. Source: www.globenewswire.com

The Scope of the Ustekinumab Biosimilars Market Report encompasses a comprehensive analysis of product segments, geographic regions, therapeutic applications, technological influences, and competitive positioning relevant to industry stakeholders. It includes a breakdown of types of ustekinumab biosimilars, such as subcutaneous injectable, intravenous formulations, and emerging long‑acting delivery systems, with insights into adoption patterns and formulation prevalence across treatment settings. The report evaluates application areas including plaque psoriasis, Crohn’s disease, ulcerative colitis, psoriatic arthritis, and other autoimmune indications, providing profile details for end‑user decision‑making.

Geographical coverage spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with regional insights into infrastructure capabilities, regulatory environments, and healthcare system dynamics that influence biosimilar integration. The scope also analyzes end‑user segments, including hospitals, specialty clinics, retail pharmacies, and emerging direct‑to‑patient distribution channels, highlighting variations in adoption behavior and institutional procurement. Technology trends such as single‑use bioreactor adoption, continuous bioprocessing, advanced analytics, and digital adherence tools are examined for their impact on manufacturing efficiency, quality standards, and market access.

In the competitive dimension, the report profiles major players, strategic alliances, product launch timelines, and regulatory milestones that shape the competitive landscape. Additionally, it identifies innovation trajectories in manufacturing, delivery formats, and market entry strategies, offering foresight on biosimilar pipeline developments and future growth enablers. The breadth and depth of segments ensure the report informs investment decisions, commercialization planning, and strategic forecasting for biologics and biosimilar stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 7,229.0 Million |

| Market Revenue (2033) | USD 12,892.8 Million |

| CAGR (2026–2033) | 7.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Sandoz Group AG, Samsung Bioepis Co., Ltd., Amgen, Inc., Celltrion, Inc., Biocon Biologics Ltd., Fresenius Kabi AG, Teva Pharmaceutical Industries Ltd., Alvotech Holdings, Ltd., Accord BioPharma, Inc., Intas Pharmaceuticals Ltd., Formycon AG, Pfizer, Inc., Boehringer Ingelheim GmbH, Mylan N.V. |

| Customization & Pricing | Available on Request (10% Customization Free) |