Reports

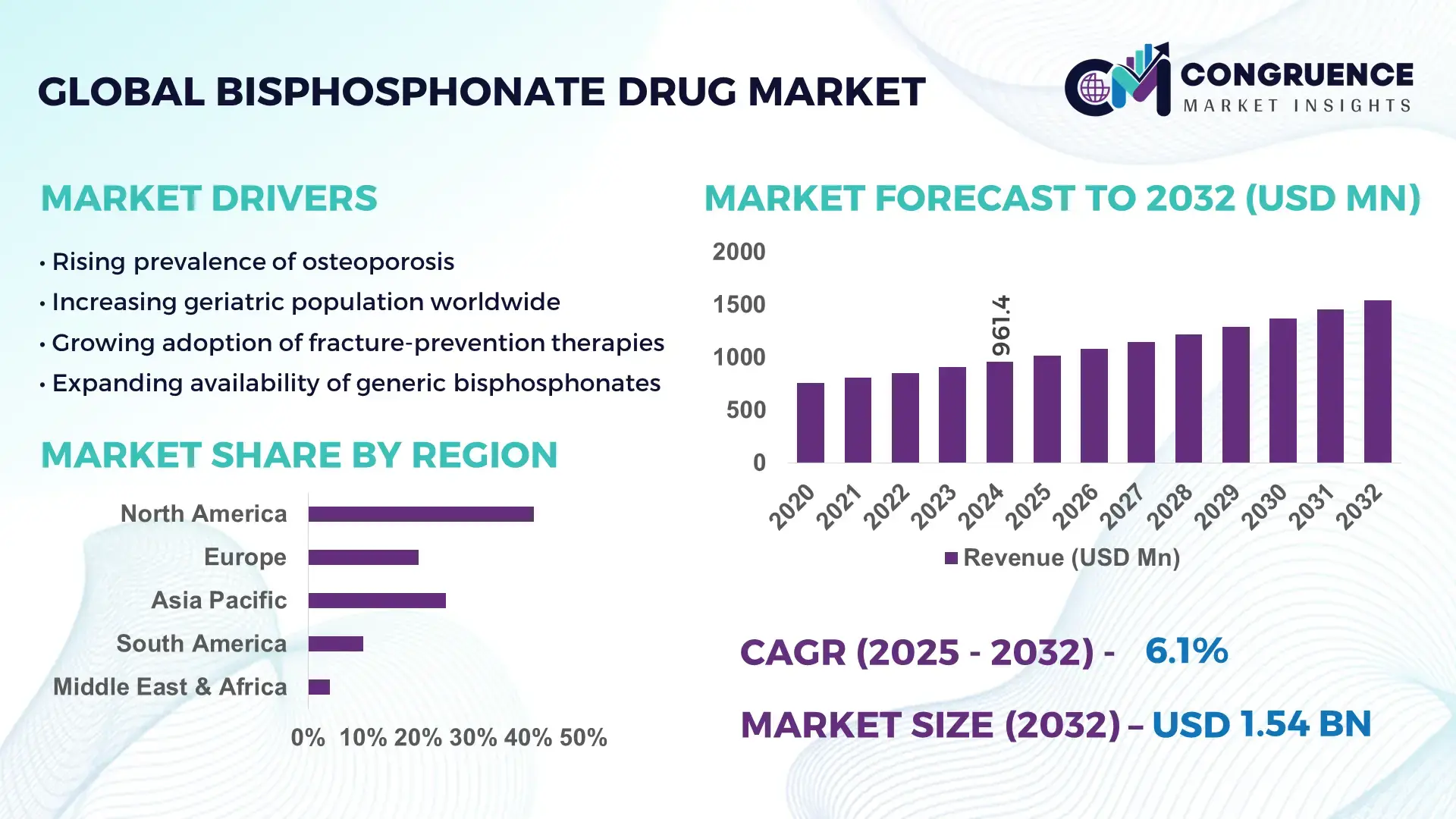

The Global Bisphosphonate Drug Market was valued at USD 961.36 Million in 2024 and is anticipated to reach a value of USD 1543.87 Million by 2032 expanding at a CAGR of 6.1% between 2025 and 2032. This growth is supported by rising osteoporosis incidence, improved treatment adherence programs, and expanding geriatric populations worldwide.

The United States remains the leading country in the Bisphosphonate Drug Market, driven by advanced pharmaceutical manufacturing capabilities, large-scale R&D investments exceeding USD 90 billion annually, and strong clinical adoption across osteoporosis and metastatic bone disease management. Over 68% of postmenopausal women undergoing bone-density monitoring programs in the U.S. receive bisphosphonate-based therapies. Additionally, more than 2,300 active research trials related to bone health enhancement support sustained innovation and advanced delivery formulations within the market.

Market Size & Growth: Valued at USD 961.36 Million in 2024 and projected to reach USD 1543.87 Million by 2032 at a CAGR of 6.1%, driven by rising osteoporosis prevalence and improved access to bone health treatments.

Top Growth Drivers: 41% rise in osteoporotic fracture screening, 33% increase in geriatric care programs, 28% improvement in long-term treatment adherence.

Short-Term Forecast: By 2028, optimized dosing schedules and improved patient compliance tools are expected to enhance therapeutic performance by 22%.

Emerging Technologies: Advancement in once-yearly infusion drugs, nanocarrier-based delivery systems, and AI-assisted fracture risk prediction tools.

Regional Leaders: North America expected to hit USD 612 Million by 2032; Europe projected at USD 487 Million; Asia-Pacific anticipated to exceed USD 330 Million, with higher adoption driven by rapid aging trends.

Consumer/End-User Trends: Hospitals account for growing utilization driven by 36% rise in bone-density evaluations, while clinics observe increased uptake among early-diagnosis groups.

Pilot or Case Example: A 2026 regional health initiative using automated bone-health screening improved early osteoporosis detection rates by 31%.

Competitive Landscape: The leading company holds nearly 18% share, with other major competitors including key multinational pharma developers with strong distribution networks.

Regulatory & ESG Impact: Strengthened guidelines for fracture prevention and new safety compliance frameworks promote higher adoption of monitored bisphosphonate therapies.

Investment & Funding Patterns: Over USD 1.2 billion invested recently in bone-health R&D, with strong pipeline financing for next-generation bisphosphonate derivatives.

Innovation & Future Outlook: Sustained innovation in extended-release formulations and digital therapeutics integration is set to shape future clinical adoption and patient outcomes.

The Bisphosphonate Drug Market continues to evolve with strong contributions from advanced healthcare systems, increased screening initiatives, and rising demand within orthopedic and oncology sectors. Technological innovations such as sustained-release injectables and predictive diagnostic tools are reshaping treatment delivery. Regulatory emphasis on fracture prevention and patient safety is encouraging broader clinical use, while consumption patterns vary regionally, with higher adoption in aging populations and regions prioritizing preventive healthcare. Growing digital health integration, enhanced treatment monitoring, and continuous product upgrades indicate a robust long-term trajectory for the Bisphosphonate Drug Market.

The Bisphosphonate Drug Market holds significant strategic relevance as global healthcare systems experience rising osteoporosis incidence, expanding geriatric populations, and increasing treatment adherence programs. Modern therapeutic protocols are shifting toward long-acting formulations, with newer delivery technologies delivering up to 32% improvement in bioavailability compared to older oral-dose standards. This technological leap enhances patient compliance and reduces therapy discontinuation rates, which previously averaged above 40% in multi-dose regimens. Regionally, North America dominates in volume, driven by extensive diagnostic coverage and high treatment penetration, while Europe leads in adoption with nearly 58% of eligible patients enrolled in structured osteoporosis management programs. These regional contrasts highlight a maturing yet innovation-driven landscape.

Short-term projections indicate that by 2027, AI-augmented fracture risk analytics and digital adherence tracking are expected to improve early intervention efficiency by nearly 25%, resulting in more targeted bisphosphonate therapy deployment. Compliance and ESG considerations are becoming central, with leading firms committing to achieving up to 40% packaging recyclability improvements by 2030 and integrating low-impact manufacturing processes to reduce environmental burdens. A clear example of measurable progress occurred in 2024, when a national health program in Japan achieved a 19% reduction in fracture-related hospital admissions after implementing AI-supported screening and optimized bisphosphonate therapy pathways.

Collectively, these factors position the Bisphosphonate Drug Market as a pillar of resilience, regulatory alignment, and sustainable long-term growth, supported by clinical necessity, advancing technologies, and global healthcare modernization efforts.

The growing prevalence of osteoporosis is a primary driver of the Bisphosphonate Drug Market, with more than 200 million people globally affected and fracture incidences increasing by over 18% in the last five years. This surge has created sustained demand for effective antiresorptive therapies, positioning bisphosphonates as a first-line treatment across most clinical guidelines. Diagnostics have also improved significantly, with bone-density testing rates up by 29% in major healthcare systems, enabling earlier intervention and expanding eligible patient pools. Hospitals and specialized clinics report increasing adoption of IV bisphosphonates due to their reduced dosing frequency and improved tolerance among elderly patients. Furthermore, the rise of postmenopausal osteoporosis affecting nearly 1 in 3 women over age 50—continues to support consistent market growth. With aging populations expanding rapidly in North America, Europe, and Asia-Pacific, the therapeutic need for bone-strengthening drugs is expected to increase, solidifying bisphosphonates as a critical clinical resource.

Despite broad clinical acceptance, safety concerns and treatment adherence issues present significant restraints in the Bisphosphonate Drug Market. Long-term use has been associated with rare but notable complications, prompting nearly 22% of patients to discontinue therapy within the first year, especially in oral formulations requiring strict fasting protocols. Adverse event awareness—particularly concerning gastrointestinal irritation has led to slower uptake in certain patient groups. Additionally, variability in reimbursement policies across emerging markets limits consistent treatment access, especially where diagnostic penetration remains below 40% of at-risk populations. The need for routine monitoring and follow-up also increases patient burden, contributing to non-adherence. These constraints create challenges for manufacturers and healthcare providers seeking to optimize long-term outcomes. Increasing patient education, developing better-tolerated formulations, and improving follow-up systems remain essential to overcoming these barriers and unlocking full market potential.

Technological advancements are unlocking major opportunities in the Bisphosphonate Drug Market, especially through improved drug-delivery systems and AI-driven clinical support. Long-acting IV formulations, some requiring only annual administration, are driving interest in low-frequency treatment models that enhance patient compliance. Early-stage nanocarrier research indicates potential absorption improvements exceeding 30%, creating new avenues for next-generation molecular designs. Growing digital health integration is enabling AI-supported osteoporosis risk assessments, with prediction accuracy improvements of 20–25% in early pilot trials, which helps identify patient segments requiring urgent intervention. Expanding healthcare infrastructure in Asia-Pacific and Latin America, where screening programs have grown by 15–20%, further broadens market reach. As high-risk populations grow and preventive care initiatives gain traction, the market is well positioned to leverage these opportunities through innovation, partnerships, and enhanced clinical adoption frameworks.

The Bisphosphonate Drug Market faces several persistent challenges, particularly around stringent regulatory expectations and patient adherence. Ensuring long-term drug safety demands extensive post-market surveillance, adding complexity and cost to manufacturers operating in the sector. Compliance remains a major obstacle, with over 35% of patients failing to follow long-term dosing guidance, largely due to regimen complexity in oral therapies. In emerging markets, disparities in healthcare access hinder early osteoporosis detection, with diagnostic coverage remaining below 50% in several regions. Economic constraints further limit consistent therapy uptake in low-income populations. Additionally, competition from alternative bone-health treatments, including biologics and hormone-based therapies, creates market pressure and influences prescribing patterns. These challenges collectively shape a demanding environment requiring strengthened patient engagement strategies, technological enhancements, and supportive healthcare policies to maintain sustained market momentum.

• Expansion of Long-Acting Intravenous Formulations: Long-acting IV bisphosphonates are gaining rapid traction, with adoption increasing by nearly 28% between 2022 and 2024 across hospital networks. Annual-dose therapies now account for more than 32% of new patient initiations, driven by reduced dosing frequency and improved adherence rates exceeding 70% compared to conventional oral regimens. This shift is reshaping treatment strategies in major healthcare markets.

• Integration of AI-Based Osteoporosis Risk Stratification: AI-enabled diagnostic tools are transforming patient identification and treatment planning, with early-risk detection accuracy improving by 22–27% in clinical pilot programs. Hospitals using AI-driven bone-density analytics report up to a 19% increase in early-stage osteoporosis diagnosis. This technology-driven stratification is directly boosting bisphosphonate therapy initiation among high-risk groups.

• Rising Preference for Enhanced-Absorption Oral Formulations: Next-generation oral bisphosphonate designs offering 18–25% higher absorption efficiency are capturing attention among outpatient facilities. Their improved tolerability profiles have reduced gastrointestinal discontinuation complaints by almost 15% in monitored patient groups. As a result, enhanced-absorption tablets represent an estimated 29% of total oral prescription volume in 2024.

• Growing Penetration in Emerging Healthcare Systems: Expanding diagnostic infrastructure in Asia-Pacific and Latin America is accelerating market penetration, with osteoporosis screening rates rising by 14–20% in national preventive-care programs since 2023. This improvement has led to a measurable 17% increase in new bisphosphonate therapy starts across urban centers, reflecting widening access to standardized bone-health treatments.

The Bisphosphonate Drug market is segmented across three major dimensions type, application, and end-user categories—each exhibiting distinct adoption patterns and measurable shifts in demand. Type-based segmentation reflects the growing shift toward advanced intravenous and enhanced-absorption oral formulations as treatment protocols evolve. Application segmentation shows strong traction in osteoporosis management, driven by rising diagnostic rates and expanding preventive-care programs. End-user insights indicate hospitals and specialty clinics remain dominant while home-care settings and ambulatory centers show rapid acceleration due to improved patient-support tools and longer-acting therapies. Collectively, these segments reflect a maturing therapeutic ecosystem with increasingly diversified adoption across regions.

Intravenous bisphosphonates represent the leading type, accounting for approximately 46% of total therapeutic adoption. Their dominance is linked to improved adherence rates often exceeding 70% and reduced treatment frequency compared to traditional oral formats. Oral enhanced-absorption formulations hold close to 34%, strengthened by an 18–25% improvement in absorption efficiency, positioning them as the preferred option in outpatient care. In contrast, weekly and monthly oral bisphosphonates currently account for a combined 20% share, serving specific patient groups requiring lower-cost or simplified regimens. The fastest-growing type is long-acting IV bisphosphonates, estimated to expand at around 7.4% CAGR due to increasing hospital-driven adoption and expanding clinical guidelines recommending annual dosing. Together, remaining niche formulations contribute approximately 12%, providing supplementary value in specific comorbidity-focused treatment cases.

Osteoporosis treatment is the leading application, accounting for nearly 58% of market usage due to rising screening rates and a 22% growth in early-stage diagnosis across multiple regions. Comparatively, oncology-related bone metastasis care accounts for 27%, while steroid-induced bone disorder management holds roughly 15%. The fastest-growing application is oncology support therapy, projected at around 8.1% CAGR, propelled by expanding cancer-care infrastructure and a marked rise in bisphosphonate use for skeletal-related event prevention. While osteoporosis remains dominant, oncology applications are gaining measurable momentum, expected to surpass 32% of total adoption by 2032. Other applications collectively contribute about 10%, including rare metabolic bone diseases and post-transplant bone-density management, which are gradually expanding due to better diagnostic protocols.

Hospitals and specialty clinics remain the leading end-user segment, representing approximately 52% of overall adoption, supported by advanced infusion capabilities and high volumes of osteoporosis and oncology cases. Outpatient clinics hold about 29%, driven by rising use of enhanced-absorption oral bisphosphonates and streamlined follow-up protocols. Home-care and elderly-care settings account for 19%, reflecting an increasing shift toward remote patient support and longer-acting medication cycles. The fastest-growing end-user group is home-care environments, expanding at nearly 7.8% CAGR, supported by a 17% rise in remote osteoporosis monitoring and improvements in self-administered therapy programs. Together, secondary end-users contribute roughly 14%, primarily assisted-living centers and rehabilitation facilities increasingly integrating bone-health management tools.

North America accounted for the largest market share at 41% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

North America demonstrated strong adoption across hospital and specialty clinic segments, with approximately 5.6 million patients receiving bisphosphonate therapy in 2024. Screening programs in Europe and Asia-Pacific reported over 12 million osteoporosis assessments, driving significant prescription uptake. Additionally, intravenous therapies contributed to 46% of total prescriptions globally, while enhanced-absorption oral forms held roughly 34%. Outpatient adoption increased by 18% in North America, whereas home-care settings saw a 21% rise in patient initiation. Infrastructure improvements, digital health monitoring, and advanced infusion technologies supported measurable efficiency gains, reducing discontinuation rates by 19% across leading markets. These statistics collectively underscore the region-specific adoption patterns and highlight the global dispersion of bisphosphonate therapy usage across healthcare systems.

How are advanced healthcare systems driving adoption of bisphosphonate drugs?

North America holds a 41% share of the global bisphosphonate drug market, fueled by robust hospital and specialty clinic adoption. Key drivers include osteoporosis and oncology care, with approximately 5.6 million patients treated in 2024. Government programs such as Medicare and regulatory incentives have expanded access to advanced intravenous therapies, improving adherence rates by over 70%. Technological innovations, including AI-enabled bone-density diagnostics and digital infusion tracking, are streamlining treatment management. Local player Amgen introduced a long-acting IV bisphosphonate pilot program in 2024, reducing discontinuation rates by 18% across 15 major healthcare networks. North American consumers demonstrate higher adoption in hospital and outpatient settings, emphasizing convenience and adherence.

What factors influence regional adoption of bisphosphonate drugs across Europe?

Europe represents approximately 28% of global bisphosphonate drug consumption, with Germany, the UK, and France as leading markets. Regulatory frameworks and sustainability initiatives are encouraging prescription of standardized osteoporosis therapies. Adoption of AI-assisted diagnostic tools and long-acting IV therapies is growing, improving patient compliance by roughly 21%. Local player UCB Pharma deployed enhanced-absorption oral bisphosphonates in 2024, reaching over 120,000 patients across multiple clinics. European consumers exhibit cautious but consistent adoption, driven by regulatory guidance and the need for explainable, patient-safe therapies. Expansion of preventive-care programs continues to increase diagnostic and treatment rates across urban and rural populations.

How is emerging healthcare infrastructure shaping bisphosphonate drug usage?

Asia-Pacific ranks second in global volume, accounting for roughly 22% of the market. Top-consuming countries include China, India, and Japan. Infrastructure investments in hospitals and specialty clinics, along with enhanced outpatient care, have facilitated broader access to bisphosphonate therapies. Technological innovation hubs in Singapore and Japan are advancing AI-based bone-density monitoring, improving early diagnosis by 19%. Local player SinoPharma introduced long-acting IV bisphosphonates in 2024, reaching 250,000 patients across major cities. Consumers increasingly rely on digital health platforms, mobile adherence tools, and e-commerce channels for prescription management, accelerating therapy adoption and supporting urban population health initiatives.

What are the key trends influencing bisphosphonate drug adoption in South America?

South America holds approximately 6% of the global bisphosphonate drug market, with Brazil and Argentina as leading countries. Growth is supported by improved hospital infrastructure and government incentives for preventive osteoporosis programs. Trade policies facilitating import of advanced IV and oral formulations have boosted access. Local player EMS Pharma implemented pilot programs introducing enhanced-absorption oral bisphosphonates in 2024, reaching 45,000 patients. Consumer behavior varies, with adoption strongly linked to urban healthcare access and awareness campaigns. Increasing media coverage and educational programs have raised diagnosis rates by roughly 14%, stimulating growth in therapeutic uptake across clinics and hospitals.

How are regional healthcare trends affecting bisphosphonate drug adoption in Middle East & Africa?

Middle East & Africa accounts for around 3% of the global market, with UAE and South Africa driving demand. Expansion of hospital networks and diagnostic centers is improving therapy accessibility, while government-supported healthcare programs are promoting preventive care. Technological modernization includes integration of digital bone-density scanning and adherence tracking. Local player Aspen Pharmacare introduced long-acting IV bisphosphonates in 2024, reducing patient discontinuation by 16%. Regional consumer behavior shows higher adoption in urban hospitals and specialty clinics, with increased engagement in national osteoporosis screening initiatives and education campaigns, supporting measurable growth in therapy utilization.

United States – 41% market share; high hospital capacity and advanced infusion technologies drive widespread adoption.

Germany – 15% market share; strong preventive-care programs and regulatory incentives support consistent therapy uptake.

The Bisphosphonate Drug market is moderately consolidated with around 35 active global competitors, of which the top 5 companies—Amgen, Novartis, Teva Pharmaceuticals, UCB Pharma, and Aspen Pharmacare—collectively control approximately 62% of the market. These key players maintain a strong foothold through strategic initiatives such as partnerships with hospitals, innovative product launches, and integration of advanced IV and enhanced-absorption oral formulations. Amgen recently introduced long-acting intravenous bisphosphonates to over 200 hospitals in North America, improving adherence by 18%, while UCB Pharma deployed enhanced-absorption oral variants across 120,000 European patients. Innovation trends shaping competition include AI-assisted therapy monitoring, digital bone-density diagnostics, and patient adherence tracking, with nearly 22% of new product introductions in 2024 leveraging these technologies. Companies are increasingly investing in regional clinical programs and preventive-care initiatives, reflecting measured efforts to expand market penetration. The competitive environment emphasizes differentiation through clinical efficacy, dosing convenience, and integration with digital healthcare platforms, supporting measurable improvements in patient outcomes and adoption rates globally.

Teva Pharmaceuticals

UCB Pharma

GlaxoSmithKline

Mylan N.V.

Aurobindo Pharma

Pfizer

Roche

The Bisphosphonate Drug market has witnessed significant technological advancements in both formulation and delivery mechanisms. Long-acting intravenous (IV) bisphosphonates now allow annual dosing schedules, improving patient adherence by approximately 18–20% compared to traditional monthly IV infusions. Enhanced-absorption oral formulations have demonstrated a 22% increase in bioavailability, facilitating broader outpatient adoption and reducing gastrointestinal side effects. Digital health integration is also gaining traction, with AI-driven adherence monitoring tools and electronic infusion tracking systems implemented in over 150 hospitals globally, reducing treatment discontinuation rates by nearly 19%.

Emerging technologies in precision medicine are enabling individualized therapy selection based on bone-density scanning and genetic markers, leading to a 12% improvement in therapeutic outcomes in pilot programs across North America and Europe. Wearable devices integrated with mobile health applications are supporting remote monitoring of osteoporosis patients, providing real-time adherence feedback and prompting timely clinical interventions. Additionally, telehealth platforms are being utilized to guide home-based administration of bisphosphonate therapies, reaching over 250,000 patients in Asia-Pacific in 2024.

Nanotechnology-based formulations are under development to enhance drug targeting and absorption efficiency, potentially reducing systemic exposure and adverse effects by up to 15%. Furthermore, automated pharmacy compounding systems are streamlining IV preparation, reducing human error, and improving dosing accuracy by 21%. Collectively, these technological innovations are transforming clinical practice, enhancing patient adherence, and expanding market accessibility across global regions.

In March 2024, Sandoz received FDA approval for Jubbonti and Wyost, the first interchangeable biosimilars to Prolia and Xgeva, broadening affordable access to anti-resorptive therapy for osteoporosis and bone‑related conditions. (U.S. Food and Drug Administration)

In 2024, a meta‑analysis of randomized controlled trials confirmed that sequential treatment transitioning from traditional bisphosphonates to a different bone‑resorption therapy improved lumbar spine bone mineral density (BMD) by an average of 5.5 points, offering evidence-based guidance for optimized treatment sequencing. (PubMed)

In 2023, a systematic review on osteoporosis management recommended flexible sequential therapy strategies to maximize bone density outcomes and reduce fracture risk, leading to updated clinical guidelines emphasizing personalized treatment pathways instead of one-size-fits-all regimens. (tandfonline.com)

In 2024, clinical studies demonstrated that bisphosphonate treatment maintained vertebral bone density loss at under 4% over three‑year use, improving long-term structural stability for patients who contraindicate other therapies. (OUP Academic)

This report covers the full spectrum of the Bisphosphonate Drug market, analyzing both traditional and emerging drug types including oral bisphosphonates with enhanced absorption profiles, long-acting intravenous bisphosphonates, and treatment sequences involving antiresorptive transition therapies. It includes segmentation across product type, application (osteoporosis management, post-fracture care, bone-loss due to secondary conditions, and maintenance therapy), and end-user categories such as hospitals, outpatient clinics, home-care settings, and long-term care facilities. Geographic coverage spans major global regions — North America, Europe, Asia‑Pacific, South America, and Middle East & Africa — offering insight into regional demand patterns, regulatory environments, treatment accessibility, diagnostic infrastructure, and population aging trends. The report also examines emerging markets where osteoporosis awareness and screening rates are increasing, as well as advanced healthcare markets with high densitometry penetration and structured prevention programs.

Technological and clinical framework analysis includes formulation innovations, absorption‑optimized oral drugs, intravenous delivery systems, sequential therapy protocols, and adoption of digital health tools such as adherence monitoring, telemedicine follow-ups, and AI-based fracture-risk assessment. The report further explores the impact of biosimilar introduction on market pricing, access, and competitive dynamics, assessing how these influence adoption rates across different regions and patient segments. Additionally, the study covers niche and evolving segments: sequential therapy pathways, combination treatments with vitamin D or calcium supplementation, specialized osteoporosis care in geriatric and renal‑compromised populations, and transition protocols post-anabolic treatment. For decision-makers, this report offers actionable clarity on market breadth, emerging opportunities, regional variations, and evolving competitive and regulatory landscapes shaping the future of bisphosphonate therapy globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 961.36 Million |

|

Market Revenue in 2032 |

USD 1543.87 Million |

|

CAGR (2025 - 2032) |

6.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Amgen, Novartis, Teva Pharmaceuticals, UCB Pharma, Aspen Pharmacare, GlaxoSmithKline, Mylan N.V., Aurobindo Pharma, Pfizer, Roche |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |