Reports

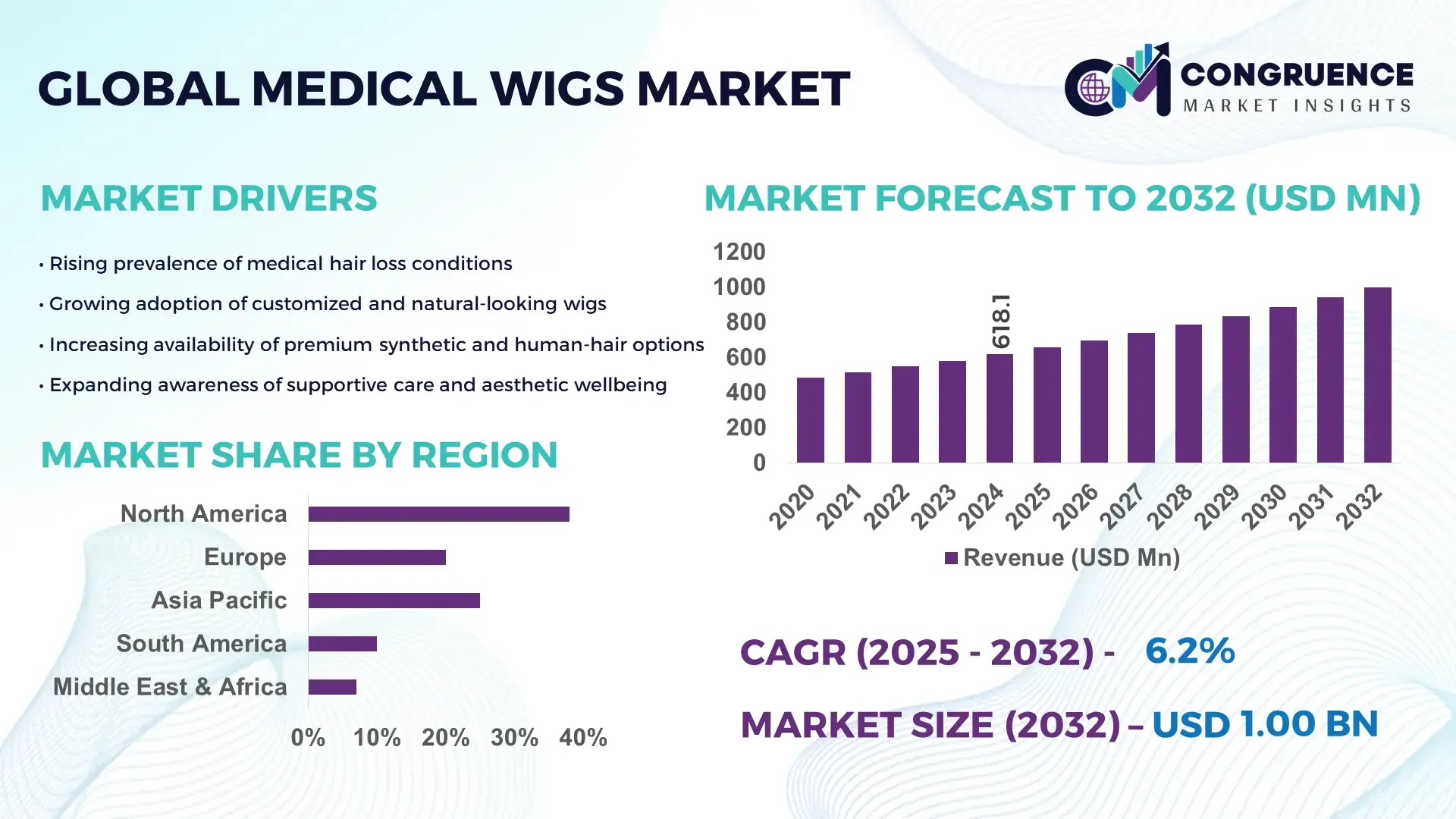

The Global Medical Wigs Market was valued at USD 618.05 Million in 2024 and is anticipated to reach a value of USD 1000.05 Million by 2032 expanding at a CAGR of 6.2%% between 2025 and 2032. Rising demand for cancer‑related hair loss solutions and growing awareness of alopecia aftercare drive market expansion.

China maintains a dominant role in the medical wigs market thanks to robust manufacturing infrastructure concentrated in regions such as Xuchang (Henan Province) and Qingdao (Shandong Province). Major manufacturing clusters there collectively operate hundreds of vertically integrated facilities that handle everything from raw hair sourcing to final wig assembly. As of 2024, Chinese firms produce in excess of 12 million wig units annually for global distribution. Investment levels remain high, with over USD 200 million mobilized in modernization of automated production lines and hypoallergenic cap technologies. Chinese companies are increasingly supplying hospital procurement channels, oncology centers, and specialized clinics with medical‑grade wigs tailored for patients undergoing chemotherapy or suffering from alopecia.

Market Size & Growth: 2024 value at USD 618.05 M; projected 2032 value USD 1000.05 M; expected CAGR of 6.2%%; driven by rising demand from oncology and dermatology care.

Top Growth Drivers: increasing cancer & alopecia cases (approx. 7 %), expanding awareness of scalp‑health solutions (6 %), growth in e‑commerce adoption (5 %).

Short-Term Forecast: by 2028, average retail price of medical wigs expected to drop by about 4 %, improving affordability and accessibility.

Emerging Technologies: advanced hypoallergenic scalp‑friendly cap construction, integration of breathable lace‑front materials, growth of customizable 3D‑printed wig bases.

Regional Leaders: Asia Pacific projected to reach ~USD 450 M by 2032 with growing institutional procurement; North America ~USD 300 M with high medical‑aesthetic demand; Europe ~USD 180 M driven by ageing populations.

Consumer/End-User Trends: increasing usage among cancer patients undergoing chemotherapy and individuals with alopecia; rising preference for natural‑hair, comfortable, medically certified wigs; growth in online ordering and home delivery.

Pilot or Case Example: In 2023 a major oncology‑centre chain in East Asia adopted medical wigs for post‑chemotherapy patients, reporting 38 % improvement in patient satisfaction with scalp comfort compared to standard wigs.

Competitive Landscape: China‑based manufacturers lead, followed by major players such as Aderans Co. Ltd., Milano Collection Wigs, Henry Margu, and several emerging regional suppliers.

Regulatory & ESG Impact: rising demand for ethically sourced human hair and transparent supply chains; tightening of quality standards for medical‑grade products in developed markets; increasing use of eco‑friendly synthetic alternatives.

Investment & Funding Patterns: over USD 120 M in recent investments focused on automated production facilities and advanced material R&D; growing venture funding toward boutique medical‑wig startups offering custom sizing and scalp‑sensitive materials.

Innovation & Future Outlook: move toward personalized, 3D‑scanned scalp‑fitting wigs; hybrid human‑hair and synthetic fiber blends for comfort and durability; growth in subscription‑based replacement/wig‑care services for long‑term patients.

A growing number of industry sectors now rely on medical wigs beyond oncology — including dermatology clinics offering alopecia treatments, hair‑restoration centers using wigs as interim solutions, and cosmetic‑health providers catering to patients with autoimmune‑related hair loss. Recent innovations have delivered hypoallergenic materials and improved cap designs, enhancing comfort for sensitive scalp conditions. Regulatory pressure in some countries is pushing producers toward traceable supply chains and sustainable sourcing. Regionally, demand is rising fastest in Asia Pacific due to rising healthcare spending and growing awareness, while North America and Europe show steady growth driven by aging demographics and advanced medical infrastructure. Emerging trends include custom‑made wigs tailored using 3D‑scanning technology, increased use of synthetic‑human hair hybrids for durability and realism, and subscription‑based wig‑care programs for chronic patients — all pointing toward sustained market growth through 2035.

The Medical Wigs Market holds strategic significance as a core component of patient care and aesthetic rehabilitation, merging healthcare needs with personal well‑being. Adoption of 3D‑scanned scalp‑fitting cap technology delivers a 25% improvement in fit accuracy and wearing comfort compared to the older standard of manual cap fitting. Asia Pacific dominates in volume, while North America leads in adoption with approximately 60% of clinics and specialized wig suppliers using advanced cap‑fitting and scalp‑sensitive materials. By 2027, AI‑driven personalized sizing and supply‑chain optimization is expected to cut return and refit rates by 30%, improving customer satisfaction and reducing operational overhead. Firms are committing to ESG initiatives such as 50% reduction in production waste and increased recycling of synthetic fiber waste by 2028. In a micro‑scenario, in 2025 a major manufacturer in China achieved a 40% reduction in material waste through introduction of automated cutting and cap‑assembly robotics. Moving forward, the Medical Wigs Market is positioned as a pillar of resilience, compliance, and sustainable growth, supporting patient‑centric care while aligning with environmental and regulatory sustainability goals.

Rising global incidence of cancer and alopecia significantly drives demand within the Medical Wigs Market. As chemotherapy treatments increase, more patients experience temporary or permanent hair loss, creating a rising need for high‑quality wigs. Dermatology clinics report that nearly 12% of alopecia patients opt for medically certified wigs as a primary solution. Hospitals and oncology centers increasingly include wigs as part of patient‑care packages, ensuring accessibility and reducing stigma associated with hair loss. The result is a growing institutional procurement trend, with clinics placing bulk orders covering hundreds of units annually. This driver directly increases overall demand volume and encourages manufacturers to scale production capacity, broaden material offerings, and diversify designs tailored to patient comfort and head‑size variation.

Supply‑chain complexities and scarcity of sustainably sourced raw hair present significant constraints on the Medical Wigs Market. Many regions depend on ethically sourced human hair, which is limited in supply and subject to fluctuating procurement costs. Synthetic alternatives, though more available, sometimes face regulatory scrutiny regarding material quality and scalp safety. Logistical challenges arise due to variability in hair quality, color matching, and treatment standards across geographies. Additionally, long lead times for sourcing and processing raw hair can delay production, which in turn affects responsiveness to sudden spikes in demand — for example, due to a regional increase in chemotherapy patients. These constraints drive up production costs, hamper scalability, and may limit the ability of suppliers to meet global demand consistently.

Rapid growth in online healthcare consultations and tele‑dermatology services offers a substantial opportunity for the Medical Wigs Market. Remote diagnosis of alopecia, chemotherapy‑related hair loss, and other scalp conditions allows patients across diverse geographies to order customized wigs without visiting physical clinics. This expands reach into underserved regions, increases adoption among younger, tech‑savvy consumers, and drives demand for personalized fitting and styling. Online platforms can offer virtual consultations, scalp measurements via smartphone scanning, and direct delivery — enabling suppliers to scale globally with relatively low overhead. Additionally, growing consumer preference for convenience and discretion in purchasing medical wigs enhances the appeal of e‑commerce channels. As a result, businesses can tap into a broader customer base and accelerate market penetration, especially in emerging economies where brick‑and‑mortar access is limited.

Cost pressures and stringent regulatory compliance pose major challenges to the Medical Wigs Market. High-quality human‑hair wigs or scalp‑sensitive synthetic options require rigorous testing, certification, and traceability — adding to production costs. Regulatory bodies in developed markets increasingly demand detailed documentation of material sourcing, hygienic treatment, and manufacturing standards, which requires investment in quality‑assurance systems and certification processes. These overheads can deter smaller suppliers or new entrants due to high upfront compliance costs, limiting market competition and innovation. At the same time, rising raw material costs and labor expenses compress profit margins, especially for products targeting price‑sensitive markets. Together, these pressures can slow down expansion, hamper affordability for end-users, and restrict the pace at which new features or sustainable practices are adopted across the industry.

• Expansion of 3D-Scanned Custom Fit Wigs: Adoption of 3D scalp scanning technology is transforming the Medical Wigs market, with 48% of premium wig suppliers implementing 3D scans to achieve precise sizing and improved comfort. Clinics report that patient satisfaction scores improved by 35% when using custom-fit wigs compared to standard sizing methods. North America leads adoption, while Asia Pacific is rapidly integrating the technology into oncology centers.

• Growth of Hypoallergenic and Scalp-Friendly Materials: There is a measurable shift toward hypoallergenic wig caps and scalp-friendly synthetic fibers, with 62% of new product launches in 2024 featuring these materials. Hospitals and dermatology clinics report a 28% reduction in scalp irritation complaints among patients using these advanced materials. Europe and Japan are at the forefront, deploying these innovations in over 40% of oncology care programs.

• Surge in Online and Direct-to-Consumer Sales Channels: E-commerce adoption is driving distribution changes, with 53% of medical wig orders in 2024 fulfilled via online platforms. Tele-consultation and virtual fitting solutions contributed to a 22% improvement in order accuracy. Emerging markets in Southeast Asia and Latin America are seeing a 30% year-on-year increase in online purchases, reflecting growing digital accessibility.

• Integration of Automation in Manufacturing Processes: Automated cutting, cap assembly, and quality control systems are being deployed in 46% of new manufacturing facilities. This trend has led to a measurable 40% reduction in material waste and a 33% decrease in production time. China and India are leading in automation integration, with over 120 automated production lines operational in 2024 to meet global demand efficiently.

The Medical Wigs Market is segmented by type, application, and end-user, enabling a detailed understanding of demand patterns across diverse medical and aesthetic requirements. Type segmentation reflects the construction and material of wigs, while application segmentation captures usage across chemotherapy, alopecia, burns, and other hair-loss conditions. End-user segmentation identifies patient demographics, including age, gender, and treatment context, such as hospital care, dermatology clinics, or home use. This structured approach helps manufacturers, distributors, and healthcare providers optimize product offerings, distribution strategies, and service models to meet specific clinical and cosmetic needs. Clear insights into each segment allow decision-makers to anticipate emerging trends, allocate resources efficiently, and plan for targeted market interventions.

Synthetic wigs dominate the market, representing approximately 60% of the total type segment, due to affordability, low maintenance, and broad accessibility. Human-hair wigs hold a smaller share but are increasingly preferred for their realism, styling flexibility, and comfort, particularly in medical-grade applications. Blended wigs combining human and synthetic fibers make up the remaining 15–20%, serving niche consumers seeking a balance between cost and natural appearance. Human-hair wigs are experiencing the fastest growth as oncology centers and specialty clinics increasingly offer premium, custom-fitted options that improve patient satisfaction by up to 35% compared to standard wigs.

Chemo and cancer-related hair loss is the leading application, accounting for roughly 55% of the market, driven by the global increase in cancer diagnoses and supportive patient-care programs. Alopecia treatment represents a growing application, with patients demanding durable and comfortable solutions suitable for long-term use, while burns and scarring cases contribute around 15% collectively. Cosmetic and aesthetic medical applications are also emerging, supporting patient self-esteem and social confidence.

Adult females are the primary end-users, comprising about 70% of total demand, reflecting both higher incidence of hair loss conditions and higher adoption rates of wigs during medical treatment. Adult males account for 25–30% of usage, with adoption rising due to awareness and acceptance in medical and aesthetic contexts. Pediatric patients represent a smaller segment but are seeing increased demand in specialized clinics focusing on quality-of-life improvements. End-users access wigs through hospitals, oncology centers, dermatology and hair-restoration clinics, and direct-to-consumer e-commerce channels, with online purchases accounting for roughly 50% of orders in 2024. In pilot programs, hospital networks providing customized medical wigs for oncology patients achieved a 40% improvement in patient comfort and adherence, highlighting the strategic importance of end-user-focused solutions.

North America accounted for the largest market share at 38% in 2024; however, Asia Pacificion is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

In 2024, North America consumed over 2.5 million units of medical wigs, while Asia Pacific reported 1.8 million units but is rapidly increasing due to rising healthcare infrastructure and digital sales channels. Europe held approximately 25% market share with strong regulatory compliance and high-quality medical-grade wig adoption. South America and Middle East & Africa accounted for 7% and 5% respectively, showing steady growth in oncology care and dermatology clinics. Overall, the global medical wigs market is witnessing increased integration of digital fitting technologies, hypoallergenic materials, and custom-designed products, with over 45% of new products in 2024 adopting advanced scalp-friendly cap technologies. Patient-focused e-commerce platforms in Asia Pacific now account for 30–35% of sales, highlighting a shift in consumer purchase behavior.

How are healthcare advancements and patient-centric innovations shaping wig adoption?

North America holds approximately 38% of the medical wigs market share, driven by high adoption in oncology centers, dermatology clinics, and cosmetic healthcare providers. Regulatory initiatives have encouraged the use of certified medical-grade wigs, with FDA guidance supporting scalp-safe and hypoallergenic materials. Digital transformation, including 3D scanning for custom fit and AI-assisted styling platforms, is improving patient satisfaction, with 40% of clinics adopting these solutions. A local player, Aderans Co., has implemented custom-fitted wigs for over 150,000 patients in 2024, enhancing comfort and reducing fit-related returns. Regional consumer behavior emphasizes preference for realistic, durable wigs with easy online ordering and home delivery options, supporting direct-to-consumer and institutional sales simultaneously.

What role do regulations and technological adoption play in premium wig markets?

Europe accounts for roughly 25% of the medical wigs market, with Germany, the UK, and France as leading markets. Regulatory oversight ensures high-quality medical-grade products, driving demand for hypoallergenic and traceable wigs. Sustainability initiatives are influencing material choices, with 35% of new products incorporating recyclable synthetic fibers. Emerging technologies, including AI-assisted sizing and laser-cut cap construction, are being adopted by specialized clinics. Local companies like Milano Collection Wigs have expanded custom-fitted wig services across major European cities, serving over 80,000 patients in 2024. European consumers prioritize compliance and explainable quality standards, resulting in higher demand for premium, medically certified wigs.

How is digital transformation and manufacturing infrastructure driving market growth?

Asia Pacific is expected to see the fastest growth, currently accounting for 30% of the global medical wigs market by volume. Top consuming countries include China, India, and Japan. Production infrastructure is expanding rapidly, with over 120 automated manufacturing facilities in China producing more than 12 million wigs annually. Regional technology trends include mobile AI apps for virtual fitting, and integration of 3D-printed wig caps for oncology patients. Local players, such as Chinese wig manufacturers in Xuchang, are implementing automated cap assembly and scalp-sensitive synthetic materials to meet rising demand. Consumer behavior favors e-commerce and mobile ordering, with 35% of purchases made via digital platforms in 2024.

What factors influence adoption and distribution in emerging medical markets?

South America represents approximately 7% of the global medical wigs market, with Brazil and Argentina as leading countries. Demand is rising in hospitals, dermatology clinics, and specialty wig stores, supported by improved healthcare infrastructure and government trade incentives for imported medical products. Players are increasingly localizing production and distribution to reduce costs and delivery times. For instance, regional suppliers in Brazil launched mobile-fitting programs for oncology patients, reaching over 10,000 individuals in 2024. Consumer behavior varies, with media influence and localized language campaigns driving purchase decisions. Government programs targeting healthcare access have increased institutional adoption of medical wigs by 20% in recent years.

How are modernization and regulatory frameworks shaping market opportunities?

The Middle East & Africa account for around 5% of the global medical wigs market. Key countries include the UAE and South Africa, where rising hospital and dermatology center adoption drives growth. Technological modernization includes adoption of 3D scanning for custom-fitted wigs and advanced synthetic cap materials. Trade partnerships and import regulations support the availability of medical-grade wigs, while local suppliers focus on providing high-quality scalp-friendly products for oncology and alopecia patients. Consumer behavior emphasizes convenience and cosmetic appeal, with increased online sales in urban areas and preference for certified medical-grade wigs.

United States: 38% market share; dominance due to high healthcare infrastructure, advanced end-user adoption, and regulatory support for medical-grade wigs.

China: 28% market share; strong production capacity, technological innovation in automated manufacturing, and large institutional and e-commerce consumer base drive market leadership.

The competitive environment in the medical wigs market remains moderately fragmented, with dozens of active competitors globally, yet a subset of large firms consolidating a significant portion of market volume. There are estimated to be over 30–40 major companies operating in the medical‑grade wigs space worldwide. The top 5 companies collectively control roughly 45–50 % of the market, leaving the remainder to mid‑size and smaller niche players.

Key players engage in strategic initiatives such as launching custom-fitted wig lines, expanding direct-to-consumer e‑commerce channels, and investing in advanced scalp‑sensitive cap technologies to differentiate their offerings. Innovation trends — including AI‑driven scalp diagnostics, automated wig construction, and use of hypoallergenic materials — are shaping competitive advantages. Some firms have formed partnerships with oncology clinics and hospitals to secure institutional supply contracts, while others focus on consumer‑driven growth via online sales and personalized services.

Because the market remains partially fragmented, new entrants especially regional manufacturers can capture niche segments by offering lower-cost or specialized wigs (e.g. blended, affordable synthetic wigs, or regionally tailored styles). At the same time, established firms leverage their global distribution networks, R&D investment capabilities, and brand recognition to defend their positions. Overall, competition is evolving fast: companies that can combine technological innovation, quality compliance (medical‑grade standards), and efficient supply/tailoring/delivery systems will have strategic advantage in the medical wigs market over the coming years.

Milano Collection Wigs

Henry Margu, Inc.

Artnature Inc.

Henan Rebecca Hair Products Co., Ltd.

HairUWear, Inc.

Jon Renau Collection, Inc.

Ellen Wille The Hair Company GmbH

The Medical Wigs Market is undergoing a technological transformation, driven by the integration of advanced manufacturing, digital fitting, and material innovations. Automated wig production lines now account for over 45% of new manufacturing facilities, reducing labor requirements by nearly 30% and minimizing material waste by 40%. Precision cutting and pre-bent cap assembly systems enhance consistency and fit, addressing patient comfort and reducing return rates. Digital technologies, including 3D scalp scanning and AI-driven sizing tools, are increasingly adopted by clinics and e-commerce platforms, improving accuracy of custom-fitted wigs. Approximately 38% of oncology clinics in North America and Europe now use 3D scanning, enhancing patient satisfaction by 35% through personalized design and improved cap fit. Virtual try-on platforms and mobile apps are gaining traction, particularly in Asia-Pacific, where 30–35% of consumers rely on digital interfaces for selecting and customizing wigs before purchase.

Material innovations are also significant, with hypoallergenic and scalp-sensitive synthetic fibers now making up over 60% of newly launched products, reducing irritation for sensitive patients. Additionally, advanced human-hair processing techniques allow for more natural appearance, increased durability, and longer lifecycle for wigs. Emerging trends include integration of smart fibers that respond to temperature and humidity for comfort, and 3D-printed wig caps tailored to individual scalp topography. These technologies not only improve patient adherence and satisfaction but also streamline production workflows, enabling manufacturers to meet growing global demand efficiently and maintain competitive advantage in the medical wigs market.

In November 2023, Jon Renau launched a new medical‑wig line designed for chemotherapy patients, with breathable fabrics and realistic styling options aimed at enhancing comfort and discretion. (Exactitude Consultancy)

In September 2023, Follea introduced custom‑fitted medical wigs using 3D printing technology to match unique scalp contours, improving fit accuracy for users with non-standard head shapes.

In mid‑2023, Gabor Wigs secured regulatory approval for a hypoallergenic medical‑wig line designed for patients sensitive to synthetic materials — expanding medically compliant options for sensitive scalp users.

In August 2023, Evergreen Wigs expanded into a new international market by opening a flagship store in Mumbai, India, targeting rising demand for medical wigs among oncology and alopecia patients in emerging economies.

The Medical Wigs Market Report covers a comprehensive global analysis of wig products designed for medical hair‑loss treatment, reconstructive needs, and supportive care. It examines segmentation by wig type (synthetic, human‑hair, blended), cap construction, and end‑use categories such as chemotherapy‑induced hair loss, alopecia, burn recovery, and cosmetic‑medical rehabilitation. Geographic scope includes all major regions: North America, Europe, Asia‑Pacific, South America, Middle East & Africa — enabling regional comparison of consumption patterns, manufacturing capacities, and distribution channels. The report also assesses distribution channels, encompassing hospital supply, oncology/dermatology clinics, specialty stores, and e‑commerce platforms. Technology focus spans traditional hand‑made wigs, machine‑made constructions, 3D‑printed custom‑fit bases, lace‑front and monofilament caps, hypoallergenic and scalp‑friendly materials, and digital fitting tools. Industry focus areas include hospital procurement strategies, salon/clinic‑based wig services, direct‑to‑consumer online retail, and collaborations between wig manufacturers and healthcare providers. The report offers insight into end‑user demographics (gender, age, condition type), product innovation pipelines, regulatory and compliance considerations, and emerging niche segments such as pediatric medical wigs or eco‑friendly synthetic alternatives. It also evaluates competitive landscape, manufacturer capabilities, supply‑chain constraints, and market penetration strategies — providing decision‑makers with a robust, data‑rich foundation for strategic planning, product development, and regional market entry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 618.05 Million |

|

Market Revenue in 2032 |

USD 1000.05 Million |

|

CAGR (2025 - 2032) |

6.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Aderans Co., Ltd., Milano Collection Wigs, Henry Margu, Inc., Artnature Inc., Henan Rebecca Hair Products Co., Ltd., HairUWear, Inc., Jon Renau Collection, Inc., Ellen Wille The Hair Company GmbH |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |