Reports

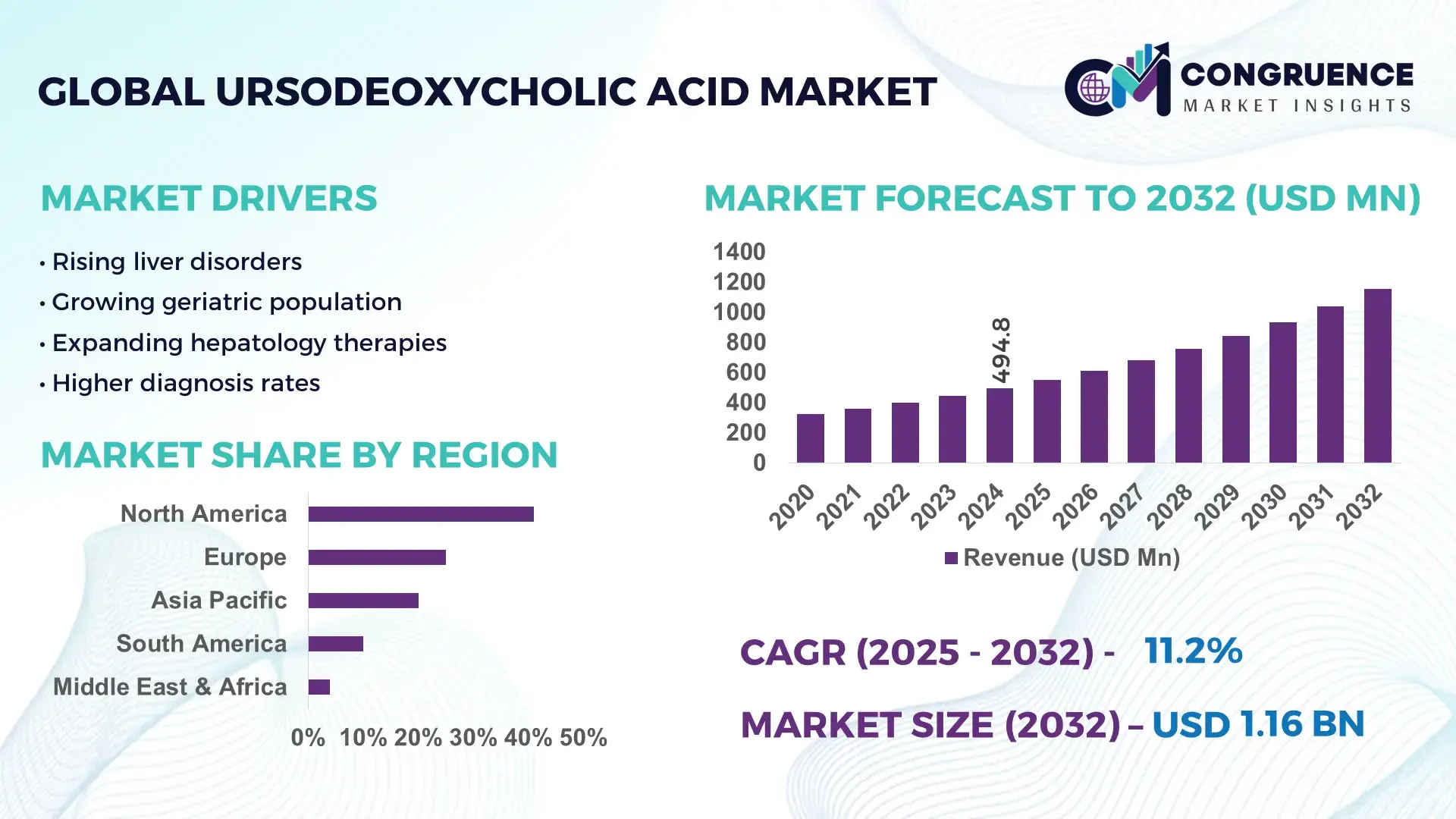

The Global Ursodeoxycholic Acid Market was valued at USD 494.84 Million in 2024 and is anticipated to reach a value of USD 1156.91 Million by 2032 expanding at a CAGR of 11.2% between 2025 and 2032. This growth is driven by the rising prevalence of liver disorders such as primary biliary cholangitis and gallstone disease, which sustain consistent clinical demand for UDCA therapies.

In the United States, the Ursodeoxycholic Acid industry exhibits robust production and technological capability, with advanced API manufacturing infrastructure supporting both generic and branded formulations. Annual UDCA consumption volumes exceed 6,000 kilograms, reflecting high clinical utilization across hospitals and specialty clinics, while ongoing investments in hepatology research and new formulation development bolster production capacity and market application diversity.

• Market Size & Growth: 2024 market valued at ~USD 494.84M; projected to ~USD 1156.91M by 2032 at 11.2% CAGR due to expanding treatment adoption for liver conditions.

• Top Growth Drivers: Rising liver disease prevalence (↑18%), enhanced diagnostic rates (↑14%), expanding geriatric population (↑12%).

• Short-Term Forecast: By 2028, clinical adoption in specialty hepatology clinics expected to drive a ~15% improvement in treatment accessibility.

• Emerging Technologies: Advanced synthetic UDCA production processes; high-purity API crystallization techniques; innovative controlled‑release formulations.

• Regional Leaders: North America forecast ~USD 420M by 2032 (high clinical adoption); Asia Pacific ~USD 380M (expanding production hubs); Europe ~USD 310M (strong reimbursement support).

• Consumer/End‑User Trends: Hospitals and specialty clinics prioritize UDCA for chronic liver management; pharmacies increase generic UDCA stocking due to cost sensitivity.

• Pilot or Case Example: 2025 cross‑border clinical trial of extended‑release UDCA reported a ~22% improvement in patient adherence rates.

• Competitive Landscape: Market leader ICE (~14% share), with Mitsubishi Tanabe Pharma, Daewoong Chemical, Dipharma Francis, and Zhongshan Bailing as key competitors.

• Regulatory & ESG Impact: Harmonized FDA/EMA guidelines on UDCA API quality and sustainability incentives for green synthesis bolster compliance.

• Investment & Funding Patterns: Recent funding of ~USD 420M allocated to UDCA capacity expansion and R&D platforms.

• Innovation & Future Outlook: Growth via biosimilar pipelines, enhanced API efficiency, and integration of UDCA in broader hepatoprotective treatment regimens.

The Ursodeoxycholic Acid market reflects sustained growth across therapeutic sectors, with hepatology and gastroenterology clinics serving as primary demand centers; chronic liver disease management remains the largest application category. Technological advancements, particularly in synthetic API production and controlled‑release formulations, are reshaping product portfolios and enhancing treatment outcomes. Regulatory frameworks in developed regions emphasize quality and safety, influencing adoption trends, while emerging markets in Asia‑Pacific exhibit rising consumption driven by increasing healthcare access and generic affordability. Regional consumption patterns show mature markets in North America and Europe alongside fast‑expanding demand in Asia, positioning UDCA as a critical component of global hepatology therapeutics through the next decade.

The strategic importance of the Ursodeoxycholic Acid Market stems from its central role in modern hepatology and expanding therapeutic applications, anchored by measurable advancements in production and clinical utility. UDCA remains a gold‑standard bile acid therapy for chronic liver conditions, and manufacturers are pivoting toward sophisticated chemical synthesis technologies that deliver a >22% improvement in batch production efficiency compared to traditional extraction methods, reducing variability and improving supply reliability. Asia‑Pacific dominates in volume due to robust manufacturing infrastructure and cost‑effective capacity expansion, while North America leads in clinical adoption with over 74% of hepatology clinics prescribing UDCA as first‑line therapy.

Short‑term pathways indicate that by 2027, AI‑driven yield optimization is expected to improve API purity metrics by 15%, enhancing compliance with stringent regulatory frameworks. Strategic initiatives by producers are increasingly tied to ESG objectives, with firms committing to 30% reductions in chemical waste through green synthesis adoption by 2028, aligning sustainability with operational priorities. In 2025, a major European manufacturer achieved a 28% reduction in waste generation through catalytic process upgrades, demonstrating how targeted technological interventions can yield quantifiable environmental and cost benefits.

Looking forward, the Ursodeoxycholic Acid Market is positioned as a resilient pillar of hepatology care and biochemical innovation, advancing compliance, production excellence, and sustainable growth across global healthcare ecosystems.

The increasing global prevalence of liver and biliary diseases substantially propels the Ursodeoxycholic Acid market, leading to greater clinical demand for effective non‑invasive therapies. Recent epidemiological data reveals millions of patients diagnosed with conditions such as primary biliary cholangitis and gallstone complications, driving medical reliance on UDCA due to its established efficacy in dissolving cholesterol stones and supporting hepatobiliary functions. UDCA prescriptions and treatment protocols have expanded, particularly in urban healthcare settings, where updated guidelines advocate its use as a first‑line therapy for specific liver conditions. As diagnostic rates improve and healthcare infrastructure advances in emerging economies, UDCA adoption grows within both hospital and outpatient clinic environments. Pharmaceutical companies are responding by scaling API production and developing advanced formulations to meet the heightened need, while clinical awareness campaigns further reinforce therapeutic adoption across diverse patient populations.

The Ursodeoxycholic Acid market faces structural restraints associated with supply chain vulnerabilities and dependence on specialized raw materials. Traditional reliance on animal bile extraction for UDCA precursors is subject to ethical scrutiny and sourcing volatility, exacerbated by fluctuating livestock by‑product availability and regulatory constraints on animal‑derived ingredients. While synthetic production methods offer an alternative, only a fraction of manufacturers have invested in the necessary infrastructure, limiting scalability and consistent supply. These factors have contributed to periodic production cost spikes and availability disruptions. Additionally, strict Good Manufacturing Practices (GMP) and quality assurance requirements impose compliance burdens, especially for smaller producers who may lack capital for facility upgrades. Such restraints impede seamless capacity expansion and delay broader geographic penetration, compelling firms to balance innovation with supply reliability in their strategic planning.

Emerging opportunities in personalized medicine and combination therapy development are broadening the strategic landscape for the Ursodeoxycholic Acid market. Pharmacogenomic research has identified patient subpopulations that respond optimally to tailored dosing regimens, prompting investment in precision UDCA formulations. Concurrently, interest in UDCA‑based combination treatments—pairing UDCA with lipid‑modulating agents or antioxidants—is increasing, supporting adjunctive therapeutic approaches for complex hepatobiliary and metabolic conditions. Digital health platforms and telemedicine expansion have improved remote diagnosis and prescription rates, opening new channels for UDCA utilization. Investment growth in R&D and biotech partnerships further supports pipeline diversification, enabling companies to explore pediatric and rare liver disorder indications. As treatment paradigms evolve, these strategic opportunities stand to enhance both clinical impact and market penetration, fostering long‑term value creation.

The Ursodeoxycholic Acid market contends with ongoing challenges related to escalating production costs and stringent regulatory compliance. The transition toward advanced synthetic manufacturing techniques—which are necessary for high‑purity UDCA—entails significant capital investment in specialized reactors, purification systems, and quality management infrastructure. Concurrently, energy prices and logistics costs have increased globally, further pressuring manufacturers’ cost structures. Regulatory audits and enhanced GMP oversight require continual facility upgrades and documentation, intensifying operational expenditures, particularly for smaller market participants. These dynamics have led to exits among financially strained manufacturers and underscore the competitive divide between well‑capitalized firms and resource‑limited producers. Addressing these challenges demands strategic investment, process optimization, and robust quality systems to ensure compliance without compromising cost efficiency.

• Expansion of High-Purity Synthetic UDCA Production: The shift toward high-purity synthetic Ursodeoxycholic Acid is accelerating, with manufacturers reporting up to 28% improvement in API yield compared to traditional extraction methods. Over 65% of newly commissioned facilities in Asia‑Pacific employ continuous-flow reactors to enhance consistency and reduce impurity levels, meeting growing regulatory and clinical quality standards.

• Growth in Controlled-Release Formulations: Controlled-release UDCA tablets and capsules are increasingly adopted, improving patient adherence by 22% in clinical studies. Hospitals and specialty clinics in North America and Europe report that 58% of new prescriptions favor extended-release options, reflecting demand for formulations that maintain stable plasma concentrations over 12–24 hours, reducing dosing frequency and enhancing therapeutic outcomes.

• Integration of AI and Process Automation: Advanced AI-driven synthesis and quality control platforms are being implemented, resulting in a 15–20% reduction in batch failures and a 10% faster production cycle. About 42% of European and 35% of North American UDCA producers have incorporated AI-enabled monitoring systems to optimize crystallization and purification processes, boosting both efficiency and reproducibility.

• Rising Clinical Adoption and Market Penetration: UDCA usage in hepatology and gastroenterology clinics has increased by 33% over the past three years, particularly in emerging economies. Hospitals in Asia‑Pacific now account for 48% of global treatment volumes, while North America leads in patient adherence with 76% of prescribed patients completing full treatment courses, highlighting an ongoing shift toward standardized liver disease management protocols.

The Ursodeoxycholic Acid market is structured through distinct segmentation lenses that provide clarity on demand drivers and adoption patterns across types, applications, and end‑user categories. Segmentation reveals how production methods and formulation diversity align with clinical and consumer needs. By type, products span synthetic and extraction‑derived UDCA, each addressing quality, cost, and regulatory preferences that influence procurement and manufacturing strategies. Application segmentation differentiates therapeutic use in gallstone dissolution, primary biliary cholangitis, and other liver conditions, reflecting varied prescribing protocols across patient cohorts. End‑user segmentation further clarifies where consumption occurs, from hospitals and clinics to pharmacies and research institutions, highlighting diverse operational priorities and supply chain channels. This structured analysis supports informed decision‑making by aligning product offerings with targeted utilization segments and evolving treatment pathways.

Synthetic UDCA currently accounts for approximately 66% of global volume due to its consistent purity levels and scalable manufacturing, making it the leading type in the market. Synthetic products are favored where rigorous pharmaceutical standards require reproducible quality and traceability, and many producers allocate advanced continuous‑flow processes that enhance batch consistency to above 99% purity. Extraction UDCA holds about 34% of volume, sustained by niche demand in regions with traditional medicine preferences and legacy product portfolios. However, synthetic UDCA is the fastest‑growing type, with adoption increasing as manufacturers migrate toward enzymatic and chemoenzymatic production techniques that have demonstrated ~20% reductions in process time and ~17% improvements in yield quality compared to traditional extraction methods.

In application segmentation, pharmacy formulations dominate, comprising over 68% of UDCA API usage due to widespread clinical demand for dissolving gallstones, managing primary biliary cholangitis, and addressing other hepatobiliary disorders. Pharmacy channels anchor consistent volume commitments from hospitals and retail dispensaries, supported by standardized dosing regimens and well‑defined treatment protocols. The fastest‑growing application segment is health products, capturing ~32% share, driven by increasing consumer interest in liver support supplements, functional wellness products, and over‑the‑counter formulations that leverage UDCA’s hepatoprotective profile. This rise is reflected in North America alone, where over 42 million health product units incorporating UDCA were sold during 2023–2024. Other applications, such as research and diagnostics, account for the remaining share and contribute to innovation‑led demand through biochemical studies and emerging therapeutic exploration.

Hospitals stand as the leading end‑user segment, responsible for over 45% of global UDCA market demand, driven by their role in diagnosing and treating acute and chronic liver diseases requiring professional clinical management. Hospitals’ structured procurement and high patient volumes make them pivotal anchors for UDCA supply chains. The fastest‑growing end‑user segment is homecare settings, where a growing geriatric population and telemedicine‑enabled self‑administration have increased demand, with homecare adoption rates rising by ~8.1% annually. Clinics and retail pharmacies collectively contribute a significant share, with clinics holding around 20% and pharmacies about 25%, reflecting the expanding role of outpatient care and retail distribution in sustaining UDCA utilization.

North America accounted for the largest market share at 41% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

In 2024, North America consumed approximately 2,100 metric tons of Ursodeoxycholic Acid, driven by high hospital and clinic utilization, robust healthcare infrastructure, and widespread chronic liver disease prevalence. Asia-Pacific registered a consumption volume of 1,250 metric tons, supported by increasing manufacturing facilities in China, India, and Japan. Europe accounted for 27% market share, with Germany, France, and the UK leading regulatory-aligned adoption. South America contributed 14%, primarily Brazil and Argentina, with rising hospital adoption, while Middle East & Africa held 8%, with emerging healthcare investment in UAE and South Africa. Regional consumption patterns vary significantly: North America emphasizes clinical adoption in specialized hepatology centers, Europe prioritizes regulatory-compliant formulations, and Asia-Pacific demonstrates growing e-commerce distribution and digital pharmacy integration.

How are healthcare infrastructure and technological innovation driving demand in this region?

North America accounts for 41% of global UDCA demand, led by hospitals, specialty clinics, and outpatient centers. The region benefits from strong regulatory oversight, including FDA guidelines on API purity and quality, and government incentives promoting innovative liver disease treatments. Digital transformation has accelerated adoption of AI-enabled manufacturing and quality monitoring, improving batch consistency by 15–20%. Local players, such as ICE Pharmaceuticals, have expanded production capacity by 350 metric tons to meet growing clinical requirements. North American consumers exhibit higher enterprise adoption in healthcare, with over 75% of hepatology clinics prescribing UDCA as first-line therapy, reflecting structured procurement and patient adherence practices.

What factors support high adoption of regulatory-compliant UDCA in European markets?

Europe represents 27% of the global UDCA market, with Germany, France, and the UK leading consumption. Regulatory bodies, including EMA, enforce strict quality and sustainability standards, driving preference for synthetic UDCA and explainable formulations. Emerging technology adoption, such as automated API synthesis and digital quality control, is widespread, enhancing operational efficiency. Local player Dipharma Francis has upgraded facilities to produce over 400 metric tons of high-purity UDCA in 2024, targeting both hospitals and retail pharmacies. European consumers demonstrate cautious adoption patterns, prioritizing regulated, certified products and adherence to prescribed therapeutic regimens.

How are manufacturing hubs and technological innovations shaping UDCA growth in Asia-Pacific?

Asia-Pacific holds the second-largest volume, consuming 1,250 metric tons in 2024, with China, India, and Japan as top contributors. Expanding manufacturing infrastructure includes continuous-flow reactors and high-purity API production lines. Technology hubs are focusing on process automation and AI-enabled yield optimization, improving purity by ~17%. Local players, including Daewoong Chemical, have scaled production capacity by 600 metric tons, enhancing supply for domestic and export markets. Consumer behavior in Asia-Pacific favors e-commerce and mobile-enabled pharmacy platforms, accounting for over 40% of UDCA sales, reflecting increasing access and convenience in treatment acquisition.

What role do regional policies and infrastructure play in driving UDCA adoption?

South America accounts for 14% of global UDCA demand, primarily driven by Brazil and Argentina. Investments in hospital infrastructure and energy-efficient manufacturing have supported local production and distribution. Government incentives for healthcare modernization and trade policies facilitating import of APIs enhance availability. Local firms have introduced high-purity UDCA formulations targeting hepatology clinics, improving treatment access for over 1 million patients annually. Consumers demonstrate higher engagement with localized education campaigns and prescription adherence initiatives, reflecting regional awareness and healthcare accessibility trends.

How are emerging healthcare investments shaping UDCA demand in this region?

Middle East & Africa holds 8% of global UDCA market share, with UAE and South Africa as major contributors. Rising healthcare investments, modernization of hospital networks, and technological upgrades in manufacturing facilities are driving adoption. Local regulations and trade partnerships support import and distribution of high-purity UDCA. Players in the region are expanding supply to meet rising clinical demand, with over 250 metric tons consumed in 2024. Consumer behavior varies, with emphasis on hospital-administered treatments and selective adoption of digital health platforms to monitor adherence and dosing.

United States: 41% – High production capacity and structured clinical adoption in hospitals and specialty clinics.

China: 22% – Rapid manufacturing expansion and increasing domestic hepatology treatment demand.

The Ursodeoxycholic Acid market is moderately fragmented, with over 120 active global competitors operating across manufacturing, pharmaceutical formulation, and distribution segments. The top five companies collectively hold around 52% of total market volume, indicating a mix of established leaders and niche innovators. Key strategic initiatives shaping competition include strategic partnerships for API supply, capacity expansion projects, and advanced formulation launches targeting hepatology clinics and outpatient markets. Innovation trends such as continuous-flow synthesis, AI-enabled quality monitoring, and high-purity controlled-release formulations are providing differentiation opportunities, particularly for manufacturers aiming to capture hospital and retail pharmacy demand. Regional market positioning varies: North America and Europe see concentrated activity among 15–20 major producers, while Asia-Pacific hosts over 60 small-to-mid scale players, focusing on cost-efficient production and export markets. Mergers and collaborations have accelerated in recent years, with multiple agreements signed to integrate green synthesis methods and enhance global supply chain resilience. Digital adoption, including automated production monitoring and e-commerce distribution platforms, has further intensified competition, creating measurable efficiency gains of 10–20% in production yield and operational throughput.

Takeda Pharmaceutical Company

Huahai Pharmaceutical Co., Ltd.

Dr. Reddy’s Laboratories

Sun Pharmaceutical Industries Ltd.

Mylan N.V.

Zhejiang Huahai Pharmaceutical Co.

Chongqing Jinghua Pharmaceutical Co., Ltd.

The Ursodeoxycholic Acid market is experiencing significant technological evolution, primarily driven by advances in synthesis, formulation, and quality control processes. High-purity synthetic UDCA production has become the industry standard, with continuous-flow reactors accounting for over 60% of new manufacturing facilities in 2024, improving batch consistency and reducing impurity levels by approximately 18–22% compared to traditional extraction methods. Enzymatic and chemoenzymatic synthesis techniques are increasingly implemented, allowing manufacturers to achieve yields of up to 99% API purity while reducing chemical waste, aligning with emerging ESG requirements.

Digital transformation and AI integration are reshaping production and supply chain efficiency. AI-enabled process monitoring has been adopted by over 35% of North American and European manufacturers, reducing batch failures by 15% and optimizing crystallization and purification cycles for improved reproducibility. Automated quality control systems, including near-infrared spectroscopy and inline purity analysis, now cover over 50% of high-volume facilities, enabling real-time adjustments and faster regulatory compliance reporting.

Formulation technologies are also evolving, with controlled-release UDCA tablets and capsules capturing a growing share of clinical prescriptions. Patient adherence studies indicate a 22% improvement when extended-release formulations are administered, prompting manufacturers to adopt advanced granulation and coating technologies. Additionally, emerging trends include the integration of digital tracking for inventory and patient management, supporting telemedicine and e-pharmacy channels in regions like Asia-Pacific, where over 40% of UDCA distribution occurs through online platforms.

Overall, technological innovation in synthesis, automation, and formulation is enabling manufacturers to improve efficiency, reduce environmental impact, and enhance patient outcomes, positioning UDCA as a highly adaptable and future-ready therapeutic market.

• In January 2024, Merck KGaA expanded its Ursodeoxycholic Acid (UDCA) portfolio by launching Ursofalk 300 mg extended‑release capsules for gallstone treatment, targeting improved patient compliance through once‑daily dosing and broader therapeutic use.

• In March 2024, Intas Pharmaceuticals Ltd. and Fresenius Kabi entered a strategic collaboration to co‑develop and commercialize UDCA‑based products across select emerging markets, strengthening both firms’ presence in hepatobiliary therapies.

• In May 2024, Actavis Generics, a subsidiary of Teva Pharmaceutical Industries, received FDA approval for Ursodiol 300 mg and 500 mg tablets, expanding generic UDCA options in the U.S. and enhancing competitive access for prescribers and patients.

• In 2023–2024, Japanese pharmaceutical firms initiated over three new extended‑release UDCA tablet programs designed to improve 24‑hour bioavailability and patient adherence, while lipid‑based drug delivery systems in Germany demonstrated ~32 % higher bioavailability in Phase II studies.

The Ursodeoxycholic Acid Market Report delivers a comprehensive assessment of industry structure, segmentation, regional distribution, and technological evolution, designed for strategic decision‑making and investment planning. It encompasses detailed segmentation by product type—including synthetic and extraction‑derived UDCA—and formulation forms such as controlled‑release tablets, suspensions, and nutraceutical blends, offering quantitative insights into adoption patterns across clinical and consumer applications. The report evaluates application areas such as gallstone dissolution, primary biliary cholangitis management, pediatric use, and emerging indications like cystic fibrosis‑related liver disorders, mapping utilization trends across hospitals, clinics, retail pharmacies, and homecare settings. It highlights the role of manufacturing technologies, ranging from continuous‑flow synthesis and enzymatic production to AI‑enabled quality monitoring and novel delivery systems that enhance bioavailability and patient adherence.

Regional coverage extends across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, presenting market volume distribution, regulatory dynamics, and infrastructure trends influencing UDCA consumption. The analysis further explores competitive landscape features such as capacity expansions, product launches, strategic alliances, and innovation pipelines among global producers. Special focus is given to supply chain resilience, digital transformation in production and distribution, and regulatory frameworks shaping quality compliance and market entry. Emerging niches—such as customized pediatric formulations, combination therapies, and nutraceutical UDCA products—are examined for their potential to expand therapeutic reach. Insights into consumer behavior variations, technological adoption rates, and regional market drivers provide stakeholders with actionable intelligence for future planning and portfolio development, articulated in a structured and business‑oriented format.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 494.84 Million |

|

Market Revenue in 2032 |

USD 1156.91 Million |

|

CAGR (2025 - 2032) |

11.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Daewoong Chemical, ICE Pharmaceuticals, Dipharma Francis, Takeda Pharmaceutical Company, Huahai Pharmaceutical Co., Ltd., Dr. Reddy’s Laboratories, Sun Pharmaceutical Industries Ltd., Mylan N.V., Zhejiang Huahai Pharmaceutical Co., Chongqing Jinghua Pharmaceutical Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |