Reports

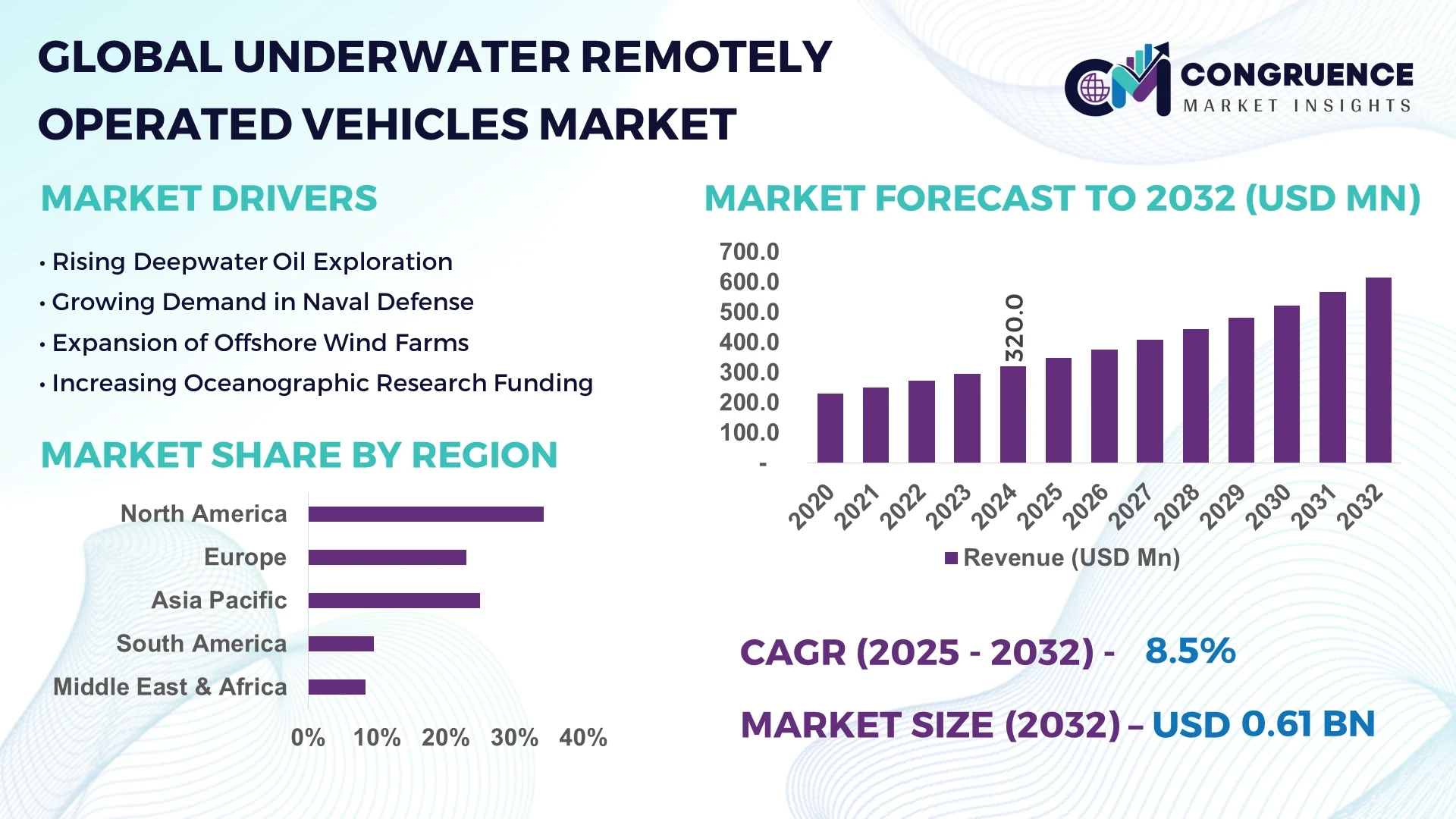

The Global Underwater Remotely Operated Vehicles Market was valued at USD 320 Million in 2024 and is anticipated to reach a value of USD 614.6 Million by 2032 expanding at a CAGR of 8.5% between 2025 and 2032.

China leads in production capacity, operating multiple large-scale ROV assembly lines that output thousands of units annually. Government-backed investment programs exceed USD 500 million per annum to upgrade offshore and defense fleets. Key applications include deep-ocean pipeline inspection, salvage operations, naval mine countermeasures, and aquaculture monitoring. China is pioneering lightweight composite materials and integrated lithium-ion power systems to improve endurance and payload versatility.

The market is segmented across core sectors—namely oil & gas, defense and security, marine science, and commercial offshore engineering—each contributing substantial revenue. Oil & gas remains the largest consumer, leveraging ROVs for inspection, maintenance, and deep-sea drilling support. Defense and security entities deploy ROVs for surveillance and mine detection, while marine science applications include oceanographic research and environmental monitoring. Recent technological innovations include modular battery-swappable designs, high-definition 4K and hyperspectral imaging systems, and AI-assisted tether management platforms, enhancing operational flexibility and data quality. Regulatory drivers such as maritime safety mandates and strict environmental impact protocols are accelerating ROV adoption under frameworks like SOLAS and national coastal protection laws. Economically, rising offshore renewable energy investments—particularly wind and tidal—are driving demand in Europe and APAC, where regional consumption is bolstered by deepwater infrastructure projects. Emerging trends include remote dockyard maintenance, subsea robotics as-a-service models, and aftermarket sensor upgrades. The future outlook points to increased integration of hybrid AUV/ROV platforms, deeper mission capability, and on-demand service delivery via cloud-based operation centers.

AI is reshaping the Underwater Remotely Operated Vehicles Market by significantly enhancing operational performance and efficiency through intelligent automation, predictive analytics, and adaptive control systems. In 2024, several commercial ROVs integrated onboard AI edge processors that continuously analyze sonar and video feeds in real time. These systems automatically identify pipeline anomalies, corrosion patches, and marine debris with up to 95% classification accuracy—reducing manual inspection time by approximately 40%.

Furthermore, AI-based tether management systems optimize cable tension and length dynamically, enabling smoother maneuverability and reducing wear-related downtime by roughly 30%. Advanced path-planning algorithms allow ROVs to autonomously execute pre-programmed survey missions, optimizing energy use and reducing power consumption by 20% compared to legacy systems. Machine learning models trained on historical mission data now forecast operational failures—such as thruster clogging—with predictive certainty levels of about 88%, allowing maintenance teams to schedule proactive interventions and avoid unscheduled mobilization costs.

In data communications, AI-driven compression algorithms halve bandwidth requirements for live high-resolution video streaming, facilitating longer mission durations and enabling remote operations from onshore command centers. Autonomous decision-making frameworks embedded in certain work-class ROVs enable real-time tool selection—such as switching from cutting torch to manipulator grip—in response to environmental sensors, reducing human operator input by up to 60%.

Such AI-infused developments are redefining the Underwater Remotely Operated Vehicles Market, enabling operators to execute complex marine missions more reliably, with lower risk profiles, and at reduced cost per operational hour. As industry players adopt these smart systems, the market is shifting toward more autonomous, intelligent, and connected subsea platforms capable of delivering higher value across sectors.

“In 2024, a leading ROV platform integrated an AI‑based sonar anomaly detector that identified structural defects with 92% accuracy during offshore wind farm inspections, reducing survey time by 35% while maintaining full mission autonomy.”

The global expansion of offshore wind farms and subsea pipelines has elevated demand for high-capacity inspection and maintenance ROVs. Between 2022 and 2024, over 50 offshore wind projects utilized ROV-assisted installation techniques capable of operating at depths of 100–150 m. ROVs equipped with dual manipulators performed bolt-tightening and conduit inspections, enabling turnaround times up to 25% faster than divers. This trend is propelling investment in mid‑depth work‑class ROV platforms with enhanced thrust—some units deliver over 500 kgf thrust—and automated torque control tools.

Maintaining and deploying complex work‑class ROVs remains costly. Annual maintenance budgets for these systems average USD 200–300k per unit, with thruster overhauls and tether replacements accounting for up to 40% of that. Planned docking and refurbishment cycles typically remove units from service for 4–6 weeks annually. Additionally, ship time and specialist crew for launch and recovery can cost up to USD 50k per day, meaning that clients often seek rental solutions over outright purchase to mitigate fixed cost burdens.

Several service providers are offering as-a-service contracts that deliver ROV capabilities without upfront capital outlay. By 2024, four major subsea firms deployed on-demand ROV fleets that generate over USD 10 million annually through time-and-material and outcome-based contracts. This asset-light model allows clients to access high-spec ROVs, advanced sensors, and remote diagnostics on short-term engagements—helping small operators perform complex interventions without large CAPEX.

ROV operations must comply with diverse international regulations—such as IMO’s MARPOL noise reduction standards, US Navy mine-countermeasure protocols, and EU seabed contaminant mapping requirements. Different jurisdictions require certification and field trials that can delay deployment by 6–12 months. For example, adoption in the North Sea requires ROV acoustic signature tests below 120 dB, while US operations require compliance with Navy’s acoustic and electromagnetic interference limits. These varying standards complicate global fleet deployment and increase certification costs by up to USD 150k annually per fleet.

Advanced Battery-Swapping Platforms: Several new ROV models now support hot-swappable modular batteries allowing continuous mission flow. Operators report mission uptime increases of 15–20% as vehicles need not return to surface for recharge, enabling extended offshore operations.

Lightweight Composite Frames: Manufacturers are shifting to carbon-fiber-reinforced polymers, reducing vehicle weight by 30–40%. This improves launch-and-recovery efficiency and allows smaller support vessels to carry larger payload capacities.

Integrated 4K/3D Imaging Systems: Recent platforms combine high-resolution 4K video with dual-stereo vision and real-time point-cloud generation. This system permits millimeter-precision in structural surveys and manipulation tasks, cutting post-processing times by half.

Cloud-Enabled Operational Analytics: ROV providers now offer dashboards delivering live telemetry, maintenance logs, and AI-generated insights. These platforms support predictive maintenance and fleet optimization, enabling asset managers to schedule deployments based on real-world performance data.

The Underwater Remotely Operated Vehicles Market is segmented into three primary categories: by type, by application, and by end-user. This segmentation enables industry stakeholders to align development, procurement, and deployment strategies with specific operational needs. In terms of types, the market features observation-class, work-class, and hybrid vehicles tailored to mission complexity and water depth. Application-wise, ROVs serve diverse operations including inspection, construction support, and environmental monitoring. End-users span oil & gas companies, defense institutions, scientific research organizations, and renewable energy developers. Segmentation analysis helps businesses navigate demand trends, operational suitability, and procurement preferences across regional and sectoral lines, allowing for more targeted product development and service offerings. Understanding these segmented insights is essential for OEMs, service providers, and investors to align with evolving end-market dynamics, regulatory expectations, and operational specifications.

The Underwater Remotely Operated Vehicles Market includes observation-class, work-class, and hybrid ROVs. Work-class ROVs represent the dominant type due to their multifunctional capabilities in deepwater construction, pipeline inspection, and heavy-duty maintenance. These vehicles typically offer higher thrust capacities, multiple manipulators, and are equipped to operate at depths exceeding 3,000 meters—making them indispensable in offshore oil & gas and subsea cable deployment.

Hybrid ROVs, integrating features of both ROVs and autonomous underwater vehicles (AUVs), are the fastest-growing segment. Their ability to perform semi-autonomous missions while retaining tethered safety and control makes them ideal for complex tasks like subsea archaeology and sensitive defense missions. This flexibility reduces human intervention while enhancing safety and efficiency.

Observation-class ROVs, though less complex, play a vital role in scientific research, shallow inspection tasks, and aquaculture monitoring. These systems are compact, cost-effective, and often used by smaller operators or research agencies for routine tasks, giving them a niche relevance within the market.

The Underwater Remotely Operated Vehicles Market is utilized across various application domains, with inspection, maintenance, and repair (IMR) emerging as the leading application segment. These tasks are critical to subsea pipeline integrity, offshore drilling platforms, and undersea power cable networks. IMR operations account for a majority of ROV deployments globally, due to the necessity for routine inspection cycles and emergency intervention in deepwater settings.

The fastest-growing application is in offshore renewable energy support, particularly within offshore wind farms. ROVs are being increasingly deployed for subsea cable laying, foundation inspections, and post-installation verification, driven by the rapid expansion of renewable infrastructure globally.

Other important applications include underwater construction, search and recovery missions, and marine scientific research. These areas leverage ROVs for their precision in object manipulation, data capture, and ability to access hazardous or inaccessible underwater environments, supporting both commercial and governmental objectives.

In terms of end-user segmentation, the oil & gas sector remains the most prominent user of ROV systems, leveraging their capabilities for deep-sea drilling, infrastructure inspection, and emergency response tasks. The extensive subsea infrastructure and requirement for high operational uptime necessitate regular ROV operations, especially in deepwater fields where diver deployment is not feasible.

The fastest-growing end-user segment is the offshore renewable energy sector, primarily driven by the global push toward decarbonization and large-scale offshore wind projects. This segment increasingly demands high-precision, compact ROVs for cost-effective cable inspections, turbine base surveys, and ongoing maintenance of submerged components.

Other key end-users include naval defense forces, oceanographic institutes, and aquaculture operations. Defense institutions utilize ROVs for mine countermeasure missions and hull inspections. Research institutions use ROVs for biodiversity assessments, underwater mapping, and sediment analysis. Aquaculture firms deploy compact ROVs for cage inspections and fish health monitoring, contributing to operational safety and sustainability in marine farming.

North America accounted for the largest market share at 34.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2025 and 2032.

The dominance of North America is largely attributed to its mature offshore oil & gas sector, advanced naval infrastructure, and early adoption of cutting-edge ROV technologies. Meanwhile, Asia-Pacific’s growth is being driven by rapid offshore energy development in China and India, increasing defense modernization budgets, and government investments in deep-sea exploration. Regional differences in regulations, availability of skilled operators, and infrastructure maturity significantly influence ROV adoption. Europe maintains a strong foothold due to its aggressive offshore renewable energy expansion, particularly in the North Sea, while the Middle East & Africa benefits from continued investments in subsea oilfield development. Each region presents distinct challenges and opportunities, shaping tailored strategies for OEMs and service providers in the global Underwater Remotely Operated Vehicles Market.

The North America Underwater Remotely Operated Vehicles Market held approximately 34.2% of the global share in 2024, driven predominantly by the United States and Canada. Offshore oil & gas exploration in the Gulf of Mexico continues to be a primary demand driver, along with increasing investments by the U.S. Navy in mine detection and underwater surveillance ROVs. The region benefits from strong regulatory frameworks such as the Outer Continental Shelf Lands Act, which mandates regular subsea inspections. Notably, technological transformation is reshaping operations—digital twin platforms, AI-enabled sensor systems, and remote piloting capabilities are now standard among leading operators. Moreover, the U.S. Department of Energy and NOAA support several R&D grants aimed at deep-sea robotics, bolstering innovation across academia and the private sector. These combined factors make North America a technologically advanced and economically robust region in the Underwater Remotely Operated Vehicles Market.

Europe accounted for around 28.7% of the global Underwater Remotely Operated Vehicles Market in 2024. The UK, Germany, and Norway are among the leading markets, largely due to their extensive offshore wind infrastructure and marine research capabilities. Regulatory bodies such as the European Maritime Safety Agency (EMSA) and environmental sustainability initiatives under the EU Green Deal are pushing for increased automation and environmentally friendly subsea systems. Europe is also at the forefront of adopting eco-design principles, with ROVs now being developed using biodegradable lubricants and low-noise propulsion systems. Technological trends include widespread deployment of cloud-connected ROV fleets, high-resolution sonar imaging, and the use of AI-powered navigation algorithms. Europe’s push for renewable integration and marine biodiversity monitoring ensures that ROV adoption will remain a central part of its blue economy strategy in the years to come.

Asia-Pacific ranked as the fastest-growing region in the Underwater Remotely Operated Vehicles Market by volume in 2024, with China, Japan, and India representing the top three consuming countries. The expansion of subsea pipeline infrastructure and offshore wind energy installations across Southeast Asia and East Asia has catalyzed demand for inspection and maintenance ROVs. China's dominance in domestic ROV manufacturing and India’s focus on building deep-sea mining capabilities are reshaping the regional supply chain. Infrastructure investments under maritime development programs in countries like South Korea and Vietnam further boost market traction. Technological innovation is centered around AI-based control systems, lightweight chassis design, and domestic sensor module production. Additionally, new innovation hubs in Shenzhen and Tokyo are fueling startups focused on hybrid ROV-AUV platforms, reinforcing Asia-Pacific's role as a fast-growing innovation hub for marine robotics.

In 2024, Brazil and Argentina dominated the South America Underwater Remotely Operated Vehicles Market, which accounted for nearly 6.5% of the global share. Brazil’s robust offshore oil fields in the pre-salt basin continue to attract deep-sea ROV applications, with Petrobras and other regional operators deploying heavy-duty work-class vehicles for infrastructure inspection. Argentina has also shown rising demand for compact ROVs in marine conservation and fisheries monitoring. Infrastructure expansion in regional ports and growing investments in undersea cable projects are further contributing to market growth. On the policy front, Brazil’s Ministry of Mines and Energy has launched several fiscal incentives to modernize subsea exploration capabilities. Additionally, trade partnerships with European ROV suppliers are bringing in high-end technologies, particularly in navigation and subsea mapping systems.

The Middle East & Africa Underwater Remotely Operated Vehicles Market exhibited strong demand in 2024, particularly across the UAE, Saudi Arabia, and South Africa. The region’s focus on expanding offshore oil fields and subsea construction projects is a primary driver for ROV usage. Countries like the UAE are modernizing their fleets with AI-enabled ROVs and incorporating digital diagnostics into standard operating procedures. South Africa is using ROVs for coastal conservation and shipwreck analysis, broadening market appeal beyond oil & gas. Technological modernization is evident with the integration of remotely managed systems, fiber-optic telemetry, and modular tooling payloads. Regulations promoting local partnerships and knowledge transfer—such as those under Saudi Vision 2030—are encouraging regional innovation while simultaneously increasing foreign investment in subsea robotics infrastructure. MEA is positioned as an emerging frontier for the Underwater Remotely Operated Vehicles Market.

United States – 34.2% market share

The United States leads the Underwater Remotely Operated Vehicles Market due to its advanced naval operations, large offshore oil infrastructure, and significant investment in subsea robotics R&D.

China – 17.5% market share

China holds the second-highest market share in the Underwater Remotely Operated Vehicles Market, fueled by high domestic production capacity, government-backed offshore energy expansion, and rapid adoption of hybrid marine robotics.

The Underwater Remotely Operated Vehicles (ROVs) Market is characterized by a moderately consolidated competitive landscape with over 40 active global and regional players. Key companies compete based on product innovation, operational reliability, and mission versatility. Market leaders focus on expanding their technological portfolios through advanced sensor integration, AI-assisted navigation, and enhanced subsea mobility platforms. A significant share of competition revolves around securing contracts from defense agencies, oil & gas operators, and offshore wind developers.

Strategic initiatives such as joint ventures, fleet modernization programs, and cross-sector partnerships have gained momentum. For instance, several ROV manufacturers are collaborating with AI software providers to develop autonomous functions that reduce human piloting requirements. New product launches featuring modular architecture, real-time telemetry, and adaptive propulsion systems have also intensified market competition.

Furthermore, companies are investing in global service and maintenance networks to support rapid deployment and reduce downtime. Regional players are increasingly offering customizable solutions to address localized marine and environmental conditions. The market is also witnessing a growing focus on sustainability, with innovations aimed at reducing energy consumption and ecological footprint, particularly for operations in sensitive marine zones.

Oceaneering International, Inc.

Saab AB

Subsea 7 S.A.

TechnipFMC plc

Fugro N.V.

DOF Subsea AS

Deep Ocean Group

Kongsberg Gruppen ASA

Soil Machine Dynamics Ltd (SMD)

Blue Robotics Inc.

ECA Group

International Submarine Engineering Ltd (ISE)

Technological advancement in the Underwater Remotely Operated Vehicles (ROVs) Market is being driven by the convergence of marine engineering, robotics, AI, and data analytics. Modern ROVs are equipped with ultra-high-definition (UHD) cameras, real-time video streaming, and advanced sonar systems that allow operators to visualize and analyze subsea environments with unprecedented clarity. Propulsion systems have evolved from traditional thruster-based setups to vectored and dynamic positioning systems, improving maneuverability in high-current environments.

Tether management systems now support longer, deeper, and more stable operations, with some commercial work-class ROVs capable of operating at depths exceeding 6,000 meters. Power efficiency has also improved, with newer ROVs incorporating onboard energy-saving modules and adaptive power distribution systems to extend mission duration.

Emerging trends include the integration of AI for predictive maintenance, route optimization, and automated object recognition. Hybrid ROV-AUV (Autonomous Underwater Vehicle) platforms are gaining traction, offering users the safety of tethered operation with partial autonomy for complex tasks. Sensor miniaturization has allowed for compact ROVs with capabilities comparable to larger units, making them ideal for scientific research and offshore wind applications.

Additionally, edge computing is being embedded into control units, enabling onboard data processing and reducing latency in decision-making. These innovations are shaping a new generation of intelligent, resilient, and cost-effective ROV systems for industrial, defense, and environmental applications.

In January 2024, Oceaneering International deployed its next-generation Magnum Plus ROV for deep-sea pipeline inspection in the Gulf of Mexico. The system achieved operational depth of 3,700 meters with real-time AI fault detection and 4K visual feedback, setting a new benchmark for offshore inspection reliability.

In November 2023, Saab Seaeye launched the Leopard XTi ROV, featuring an enhanced modular design, advanced fiber-optic communication, and 250 kg payload capacity. The system supports both industrial and defense applications, enabling rapid mission reconfiguration.

In April 2024, Deep Ocean Group opened a new R&D facility in Stavanger, Norway, focused on developing AI-based control algorithms for autonomous subsea navigation. The center will also work on integrating edge computing into control systems to boost mission autonomy and energy efficiency.

In August 2023, Kongsberg Maritime unveiled its next-gen ROV control system, SmartNav™ 2.0, designed for high-current environments. The system utilizes sensor fusion and machine learning to stabilize ROV position and improve responsiveness during complex underwater operations.

The Underwater Remotely Opered Vehicles Market Report provides a comprehensive analysis of the global landscape, encompassing a wide range of market segments, regional dynamics, and technological advancements. The report covers three core segmentation categories: type (observation-class, work-class, hybrid), application (inspection, construction, environmental monitoring), and end-user (oil & gas, defense, research, renewable energy). Each of these segments is analyzed in terms of demand trends, operational requirements, and technological alignment.

Geographically, the report provides deep insights into key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with granular analysis for major contributing countries such as the United States, China, Brazil, Germany, and the UAE. The report also highlights leading innovation hubs and emerging demand centers across the offshore energy, naval defense, and environmental sectors.

Technological domains addressed include AI-enhanced navigation systems, modular chassis design, advanced sonar and telemetry, energy-efficient propulsion, and real-time edge computing for data processing. The report also identifies niche segments gaining traction, such as ROVs for aquaculture, underwater archaeology, and subsea cable inspection in remote geographies.

This detailed scope ensures that industry professionals, investors, and policymakers receive an all-encompassing perspective to guide strategy, investment, and operational planning in the evolving Underwater Remotely Operated Vehicles Market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Underwater Remotely Operated Vehicles Market |

| Market Revenue (2024) | USD 320 Million |

| Market Revenue (2032) | USD 614.6 Million |

| CAGR (2025–2032) | 8.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Technological Insights, Market Dynamics, Segment Analysis, Regional and Country-Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Oceaneering International, Inc., Saab AB, Subsea 7 S.A., TechnipFMC plc, Fugro N.V., DOF Subsea AS, Deep Ocean Group, Kongsberg Gruppen ASA, Soil Machine Dynamics Ltd (SMD), Blue Robotics Inc., ECA Group, International Submarine Engineering Ltd (ISE) |

| Customization & Pricing | Available on Request (10% Customization is Free) |