Reports

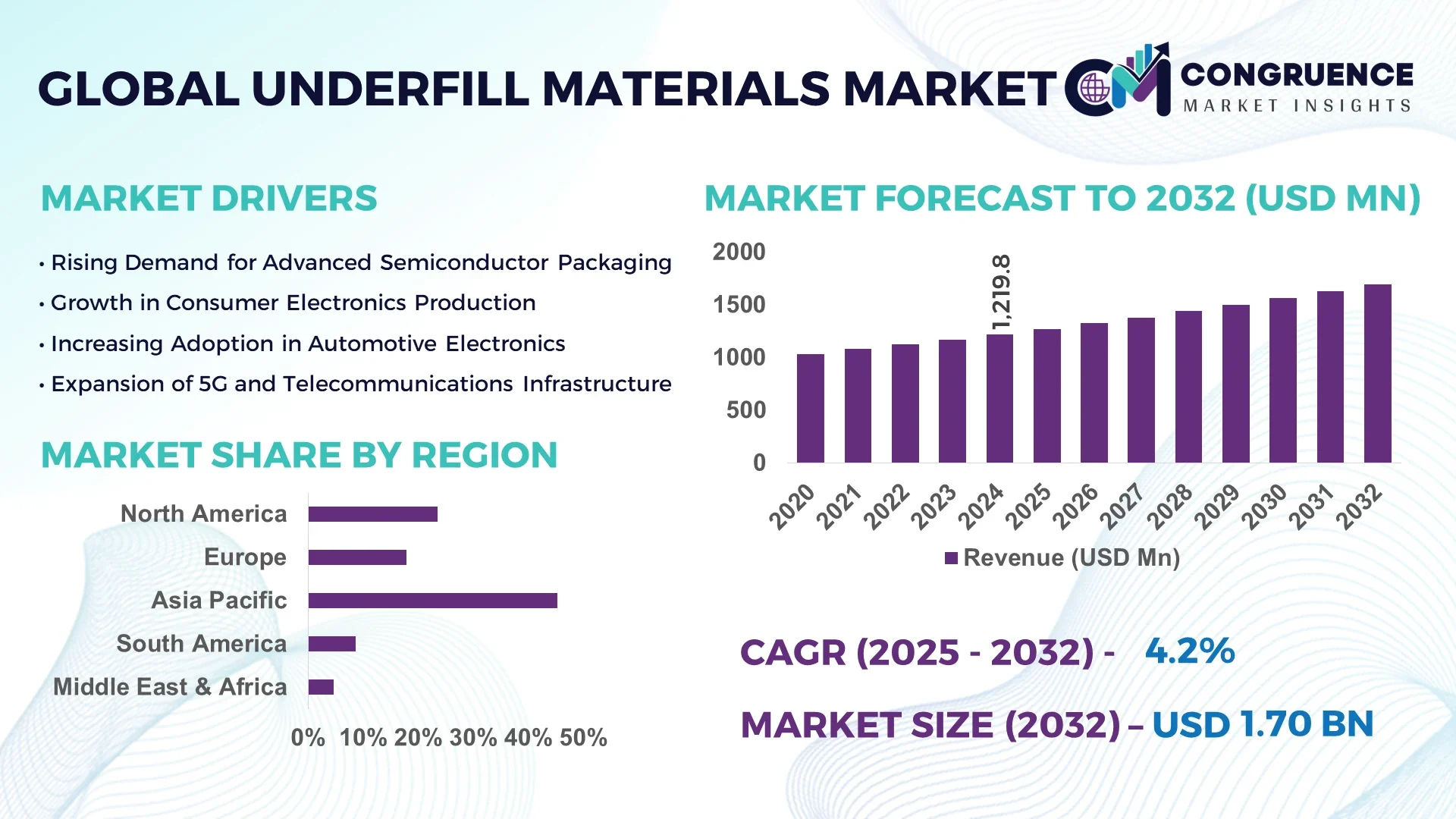

The Global Underfill Materials Market was valued at USD 1219.76 Million in 2024 and is anticipated to reach a value of USD 1695.18 Million by 2032 expanding at a CAGR of 4.2% between 2025 and 2032.

China stands as the most active participant in the underfill materials landscape, with extensive investments in semiconductor packaging infrastructure, cutting-edge R&D hubs for microelectronic applications, and production capacities integrated with advanced polymer chemistry to support the country’s robust electronics manufacturing ecosystem.

The Underfill Materials Market is undergoing structural shifts due to the convergence of semiconductor packaging demands and evolving electronics miniaturization. High-reliability sectors such as automotive electronics, telecommunications, and consumer electronics are driving usage of capillary underfill, no-flow underfill, and molded underfill solutions. The automotive segment, particularly electric vehicles (EVs), is fostering innovation in thermally conductive underfills, while telecommunications infrastructure upgrades are expanding adoption of high-performance die-attach materials. Emerging innovations in nano-engineered fillers and low-temperature curing chemistries are reshaping product portfolios. Meanwhile, environmental regulations and the transition to halogen-free and lead-free materials are influencing global compliance strategies. Regional growth trends are especially evident in East Asia and Southeast Asia due to favorable trade conditions and rapid electronics production scaling. Long-term outlook remains positive, with 3D integration and system-in-package (SiP) configurations fueling demand for advanced underfill systems.

Artificial Intelligence is ushering in transformative efficiencies in the Underfill Materials Market by revolutionizing how manufacturers design, formulate, and deploy underfill products across electronics assembly lines. AI-powered predictive analytics are being integrated into materials science labs to simulate molecular behaviors, enabling faster development of next-gen underfill formulations with improved adhesion, thermal resistance, and curing profiles. Machine learning algorithms help optimize resin viscosity and filler distribution during development, enhancing compatibility with increasingly complex substrates used in microelectronics.

Moreover, AI-enhanced process control systems are streamlining production lines, reducing defects during high-speed dispensing and curing operations. Automated optical inspection (AOI) tools backed by AI are being deployed in real-time quality control of underfill dispensing, identifying air voids, misalignments, and inadequate fills with precision unmatched by traditional methods. Smart sensors, integrated into AI frameworks, are monitoring temperature and pressure conditions during cure cycles to maintain process consistency and reduce wastage.

In packaging facilities, AI-driven robotics are improving the application accuracy of underfill materials in 3D-stacked dies and wafer-level packaging scenarios. This not only elevates manufacturing throughput but also ensures mechanical reliability under thermal cycling stress. AI is also contributing to digital twin simulations of underfill behavior under various field conditions, supporting proactive design validation and reliability assessments. As the Underfill Materials Market continues evolving with more compact and high-performance electronic devices, AI is proving indispensable in enhancing material innovation, production scalability, and operational excellence.

“In April 2024, a leading semiconductor packaging company integrated an AI-based formulation platform that reduced underfill development cycle times by 40%, enabling the launch of a low-void, high-flow capillary underfill optimized for sub-10 nm chip architectures used in 5G modules.”

The Underfill Materials Market is shaped by ongoing advancements in electronics miniaturization, rising reliability standards in semiconductor packaging, and the growing complexity of integrated circuits. As industries transition toward advanced packaging technologies such as flip-chip, fan-out wafer-level packaging (FOWLP), and 2.5D/3D ICs, demand for reliable underfill solutions has intensified. These materials play a critical role in enhancing the mechanical strength, thermal performance, and shock resistance of chip assemblies. The push toward smaller form factors and higher power densities in applications such as smartphones, wearables, automotive ECUs, and IoT devices is pushing manufacturers to develop highly tailored underfill chemistries. Market dynamics are further influenced by regional shifts in electronics manufacturing, particularly the relocation of production facilities to Southeast Asia for cost efficiency. Environmental regulations and a growing emphasis on green packaging solutions are also reshaping material formulation and compliance practices across the value chain.

The rising adoption of flip-chip and wafer-level packaging (WLP) technologies is a primary growth driver in the Underfill Materials Market. These advanced packaging methods require precise application of underfill materials to ensure component stability and mitigate thermal stress. With flip-chip shipments expected to exceed 70 billion units annually by 2026, driven by consumer electronics and high-performance computing, demand for high-performance capillary and no-flow underfills has surged. WLP applications in mobile processors, RF modules, and MEMS sensors require fine-tuned formulations with low shrinkage, fast flow rates, and excellent thermal cycling endurance. This transition toward advanced packaging is fostering innovation in thermally conductive and low-k dielectric compatible underfill systems, creating significant demand across Asia-Pacific and North American assembly lines.

A major restraint within the Underfill Materials Market is the challenge of ensuring compatibility between underfill formulations and diverse material interfaces in heterogeneous integration. As multi-chip modules and system-in-package (SiP) architectures gain traction, underfills must function reliably across varying coefficients of thermal expansion (CTEs), substrate types, and metallization layers. Inadequate bonding, delamination risks, or outgassing during cure cycles can lead to device failures, particularly under thermal cycling or high-vibration environments. These technical constraints necessitate extended validation cycles and custom formulations, limiting rapid scalability. Furthermore, the increased use of low-k dielectrics and organic interposers complicates the selection of suitable underfill systems, often requiring trade-offs between mechanical strength, flow behavior, and curing profile.

The accelerating demand for high-performance electronic components in electric vehicles (EVs) presents a lucrative opportunity for the Underfill Materials Market. Automotive electronics, including inverters, ADAS units, and battery management systems, demand robust encapsulation and underfill materials capable of withstanding extreme thermal and mechanical stresses. Underfills used in EV applications must perform reliably at elevated temperatures (above 150°C) and under continuous power cycling conditions. The global EV boom, with EV unit sales surpassing 13 million in 2024 alone, is fueling the development of automotive-grade, high-Tg underfill materials with enhanced dielectric properties. Tier-1 suppliers and OEMs are increasing investments in automotive semiconductors, prompting material manufacturers to introduce tailored formulations that ensure reliability in harsh vehicular environments.

One of the persistent challenges in the Underfill Materials Market is the need to meet increasingly stringent environmental and safety regulations while maintaining high-performance characteristics. Global directives such as RoHS, REACH, and regional green manufacturing mandates are pressuring manufacturers to eliminate hazardous substances like halogens and certain curing agents. Reformulating underfills to meet these standards without compromising mechanical strength, adhesion, or reworkability remains a complex task. The cost of regulatory compliance, coupled with the need for extensive testing and certification, increases product development timelines and expenditures. Additionally, some eco-friendly alternatives may not yet meet the thermal and mechanical benchmarks required by advanced semiconductor packages, thereby slowing their adoption in high-reliability sectors.

Growth in System-in-Package (SiP) and 3D IC Integration: The increased complexity of integrated circuit designs is accelerating the adoption of SiP and 3D integrated circuits, significantly boosting the need for advanced underfill materials. These packaging configurations require high-performance capillary underfills that provide mechanical reinforcement and thermal stress resistance. In 2024, global SiP module shipments for smartphones and wearable devices increased by over 18%, directly raising demand for underfill materials capable of maintaining reliability during thermal cycling, shock exposure, and miniaturization-related stresses.

Development of Fast-Curing Underfill Formulations: To improve production efficiency, manufacturers are introducing fast-curing underfill materials that reduce total process time without compromising structural performance. UV-curable and snap-cure underfill systems have recently gained traction, allowing curing durations to drop by over 30% compared to traditional thermally cured epoxies. These innovations are especially favored in high-throughput electronics packaging lines, where even marginal time savings can result in major cost advantages and operational throughput gains.

Surge in Demand for Low-CTE and Halogen-Free Materials: As environmental compliance and material compatibility become critical, there is growing preference for halogen-free underfill materials with low coefficients of thermal expansion (CTE). These formulations are ideal for low-k dielectric substrates and minimize reliability risks such as delamination or warping. In 2024, over 65% of underfill introductions for advanced chipsets and RF modules were halogen-free, highlighting a global transition toward sustainable, regulation-compliant formulations.

AI-Driven Quality Control in Underfill Application: AI-powered process monitoring and inspection tools are transforming how underfill materials are applied and validated in real time. Smart optical inspection systems, integrated with AI algorithms, are improving defect detection accuracy by up to 45% on production lines for microelectronics. These systems detect voids, misalignments, and flow inconsistencies earlier in the process, resulting in improved product quality and reduced material waste, especially in high-density packaging facilities.

The Underfill Materials Market is segmented by type, application, and end-user, each contributing uniquely to overall market performance. By type, the market includes capillary, no-flow, and molded underfill variants. Capillary underfill remains the most widely used due to its compatibility with flip-chip packaging. Applications include consumer electronics, automotive, telecommunications, industrial electronics, and medical devices. Consumer electronics leads the application segment, with automotive electronics rapidly growing. End-user segmentation covers OEMs, contract manufacturers, and semiconductor foundries. OEMs dominate due to direct design involvement, while contract manufacturers are expanding in emerging economies. These segments collectively shape the innovation, procurement, and scalability trends of the Underfill Materials Market.

Capillary underfill dominates the Underfill Materials Market, widely utilized in flip-chip assemblies for its strong capillary action and low void rate. Its ability to enhance mechanical reliability and thermal cycling endurance makes it indispensable in smartphones, tablets, and wearables. The fastest-growing segment is molded underfill, driven by its compatibility with system-in-package (SiP) and wafer-level packaging (WLP) technologies. Molded underfills offer better encapsulation for multi-chip modules and are gaining acceptance in high-reliability sectors like automotive electronics. No-flow underfills, although niche, are preferred in reflow soldering applications due to their ease of processing and time efficiency. Each type caters to distinct needs within microelectronic packaging, balancing performance requirements, application methods, and curing conditions to match the end-use scenario.

Consumer electronics remain the leading application area in the Underfill Materials Market, supported by consistent demand for thinner, lighter, and high-performance devices. Underfills ensure mechanical reinforcement in densely packed circuits of mobile phones, laptops, and wearables. The fastest-growing application is automotive electronics, where electric vehicles and ADAS systems demand thermally resistant, high-reliability underfill formulations for control units and power devices. Telecommunications infrastructure, particularly in 5G deployments, also requires advanced underfills to support high-frequency signal integrity and thermal management. Medical electronics and industrial equipment, though smaller segments, are increasingly adopting underfill materials for mission-critical systems where reliability is essential. The broadening range of applications is pushing manufacturers to diversify formulations for multiple thermal and mechanical stress scenarios.

Original Equipment Manufacturers (OEMs) represent the largest end-user segment in the Underfill Materials Market, as they oversee product design, quality control, and performance validation across semiconductor packaging lines. OEMs prefer premium-grade underfill materials that meet stringent performance specifications across diverse product categories. The fastest-growing end-user category is contract manufacturers, benefiting from increased outsourcing of electronics assembly by global brands seeking cost and time efficiencies. Their adoption of automated underfill dispensing and real-time quality control systems is accelerating. Semiconductor foundries and assembly houses also contribute significantly, particularly in Asia-Pacific, by offering turnkey solutions for chip packaging and die-attach processes. The evolving end-user mix is influencing procurement models, formulation customization, and product qualification cycles within the global underfill materials supply chain.

China accounted for the largest market share at 39.2% in 2024; however, India is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

China's dominant position in the Underfill Materials Market stems from its robust semiconductor packaging infrastructure, high-density electronics manufacturing clusters, and significant government-backed R&D in materials innovation. Meanwhile, India's rapid advancement in electronics manufacturing services (EMS), supported by favorable policy incentives and domestic demand for consumer electronics, is propelling market expansion. The Underfill Materials Market is witnessing geographically varied growth, with East Asia leading in production and Western economies increasing imports of specialized materials. Regional diversification in packaging formats—ranging from flip-chip to 2.5D and 3D ICs—is reshaping demand dynamics. Additionally, local regulatory frameworks focused on green compliance and material safety are influencing procurement and formulation strategies, especially in Europe and North America. Growth in infrastructure, EV production, and industrial electronics is further fueling regional consumption trends.

Advanced semiconductor assembly driving material innovation

The North America segment held a 23.5% market share in 2024, with the United States being the primary contributor. Demand is fueled by high adoption of advanced packaging in consumer electronics, aerospace systems, and electric vehicles. Automotive manufacturers and chip fabrication facilities are integrating next-generation underfill formulations to improve thermal resilience and mechanical integrity. Regulatory changes, including government initiatives supporting domestic semiconductor production through funding and tax benefits, are catalyzing market expansion. Ongoing digital transformation and IoT integration are also increasing the need for compact, high-performance electronics, subsequently boosting demand for low-void, high-flow underfill materials.

Eco-conscious innovation fueling packaging materials evolution

Europe captured 17.8% of the Underfill Materials Market in 2024, with Germany, France, and the UK driving regional consumption. Market demand is influenced by strict sustainability mandates under REACH and RoHS regulations, compelling manufacturers to shift toward halogen-free and lead-free underfill formulations. Germany’s automotive and electronics sectors are major end-users, particularly for SiP and EV powertrain applications. The European Union’s investments in semiconductor self-reliance and green electronics packaging are further accelerating demand. Rapid adoption of 5G infrastructure and AI-enabled industrial automation is also increasing usage of advanced underfill materials compatible with high-frequency devices and complex circuit assemblies.

High-volume electronics manufacturing fueling market scale-up

Asia-Pacific leads in terms of volume and scale, accounting for 45.3% of the global Underfill Materials Market in 2024. China, Japan, South Korea, and India dominate due to their strong semiconductor and consumer electronics industries. China’s capacity expansion in chip fabrication and India’s government-backed EMS policies are fueling increased consumption of underfill materials. Regional manufacturing trends are focused on ultra-high-density interconnects, 3D ICs, and compact module packaging. Innovation hubs in Shenzhen, Tokyo, and Seoul are actively integrating AI-driven quality control into electronics production, further increasing demand for precision underfill systems tailored for reliability under thermal and mechanical stress.

Regional growth driven by electronic component production and energy investments

South America accounted for 8.7% of the Underfill Materials Market in 2024, with Brazil and Argentina leading the demand. Brazil’s emerging electronics manufacturing base, supported by strategic trade agreements and incentives for industrial investment, is boosting regional usage of underfill materials. Growth in renewable energy infrastructure and automotive electronics—particularly in EV pilot projects—is increasing demand for thermally stable and durable underfills. The region is also witnessing a modest rise in outsourced packaging services, attracting international players to establish local assembly operations that depend on cost-effective, high-reliability underfill systems.

Strategic industrial transformation boosting specialty materials adoption

The Middle East & Africa region held a 4.7% share of the Underfill Materials Market in 2024. UAE, Saudi Arabia, and South Africa are showing rising consumption due to diversification in industrial electronics, oil & gas monitoring systems, and construction automation. Government-led industrial modernization initiatives and increased participation in global electronics supply chains are driving demand for robust encapsulation and underfill solutions. Local regulations are being aligned with global safety and material sustainability standards, pushing manufacturers to introduce compliant formulations. The growth of smart city infrastructure and connected industrial systems is further supporting the rise in underfill application across sectors.

China – 39.2% market share

High production capacity and strong vertical integration in semiconductor packaging infrastructure.

United States – 23.5% market share

Robust end-user demand driven by domestic electronics, defense systems, and EV markets.

The Underfill Materials Market is characterized by a moderately consolidated competitive landscape, with approximately 40 to 50 globally active players competing across various subsegments such as capillary, no-flow, and molded underfills. Leading players maintain strong market positioning by leveraging their vertically integrated manufacturing capabilities, advanced R&D facilities, and strategic global distribution networks. Intense competition centers around formulation innovation, especially in thermally conductive, halogen-free, and fast-curing underfill systems. Manufacturers are increasingly investing in nanomaterial-based fillers and hybrid epoxy systems to differentiate their offerings.

In 2024 and early 2025, the market witnessed multiple strategic moves including collaborative R&D partnerships between materials companies and semiconductor OEMs aimed at co-developing next-generation solutions for high-density and 3D packaging. Several players have launched new product lines tailored for AI processors and EV applications, reflecting a shift toward performance-specific material customization. Mergers and acquisitions have also occurred, with companies consolidating regional manufacturing capabilities to optimize supply chains and reduce delivery lead times. Competitive advantage is often driven by the ability to offer high-reliability products with low defect rates and compatibility with advanced dispensing technologies. Players focusing on digital transformation and automation in production processes are gaining a technological edge, enabling faster time-to-market and improved quality control.

Henkel AG & Co. KGaA

Namics Corporation

Shin-Etsu Chemical Co., Ltd.

H.B. Fuller Company

Zymet Inc.

Panacol-Elosol GmbH

Master Bond Inc.

AIM Solder

Kyocera Corporation

Dexter Corporation

The Underfill Materials Market is experiencing rapid technological transformation driven by the evolution of semiconductor packaging and the push for more efficient, compact, and thermally stable electronics. Advanced packaging technologies such as fan-out wafer-level packaging (FOWLP), 2.5D, and 3D IC integration are requiring underfill materials with enhanced flow properties, superior thermal conductivity, and higher mechanical reliability. These innovations are leading to the development of low-viscosity, snap-cure, and UV-curable underfill systems that reduce process time while improving adhesion and reducing void formation.

Nanotechnology integration is becoming increasingly prominent, with manufacturers introducing nano-silica and other nanoparticle-based fillers to improve the mechanical strength and thermal dissipation of underfill formulations. Such materials enhance the reliability of microelectronic assemblies under thermal cycling and stress loading, particularly in automotive and aerospace applications. Furthermore, AI-powered simulation tools are being utilized during the formulation phase to predict material behavior under real-world conditions, accelerating the development of tailored chemistries for complex substrate interfaces.

In addition, automated dispensing systems featuring precision robotics and real-time defect detection sensors are optimizing underfill application accuracy. These systems are now capable of achieving micron-level precision to match high-density interconnects in system-in-package modules. Environmental trends are also pushing technological innovation, with a surge in the development of halogen-free, lead-free, and bio-based underfill materials that meet global safety and compliance mandates without sacrificing performance.

In March 2024, Henkel launched a new high-flow, halogen-free underfill solution designed for automotive control units, offering improved thermal performance and adhesion, especially in EV applications with operating temperatures exceeding 150°C.

In December 2023, Namics introduced a snap-curable underfill optimized for flip-chip packaging in AI processors, reducing total curing time by 35% while maintaining structural integrity under thermal stress.

In August 2024, Master Bond unveiled a nano-filled epoxy underfill featuring enhanced vibration resistance and thermal shock endurance, specifically formulated for aerospace-grade electronic assemblies and MEMS devices.

In May 2023, Zymet developed a reworkable underfill material with a glass transition temperature over 140°C and low ionic contamination, targeted at telecom and 5G modules requiring high-frequency signal stability.

The Underfill Materials Market Report provides a comprehensive analysis of the global landscape, covering a wide range of underfill types including capillary, no-flow, and molded variants. It explores their application across critical sectors such as consumer electronics, automotive electronics, telecommunications, medical devices, and industrial systems. The report examines end-user categories like OEMs, contract manufacturers, and semiconductor foundries, highlighting demand patterns, innovation drivers, and material requirements specific to each.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with segmented insights into regional performance, industrial trends, and regulatory frameworks influencing underfill adoption. The study includes quantitative insights into volume distribution and market share across major countries such as China, the United States, Germany, Japan, and India.

Technology trends analyzed include advancements in nano-engineered fillers, halogen-free chemistries, fast-curing systems, and AI-integrated production and quality control mechanisms. Special emphasis is given to the role of underfills in advanced semiconductor packaging formats such as 2.5D/3D ICs, SiP, and fan-out wafer-level packages. The report also explores emerging niche markets such as underfills for flexible electronics and EV powertrain systems. It serves as a strategic tool for stakeholders seeking a detailed, data-backed understanding of the market’s present and future trajectory.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1219.76 Million |

|

Market Revenue in 2032 |

USD 1695.18 Million |

|

CAGR (2025 - 2032) |

4.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Henkel AG & Co. KGaA, Namics Corporation, Shin-Etsu Chemical Co., Ltd., H.B. Fuller Company, Zymet Inc., Panacol-Elosol GmbH, Master Bond Inc., AIM Solder, Kyocera Corporation, Dexter Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |