Reports

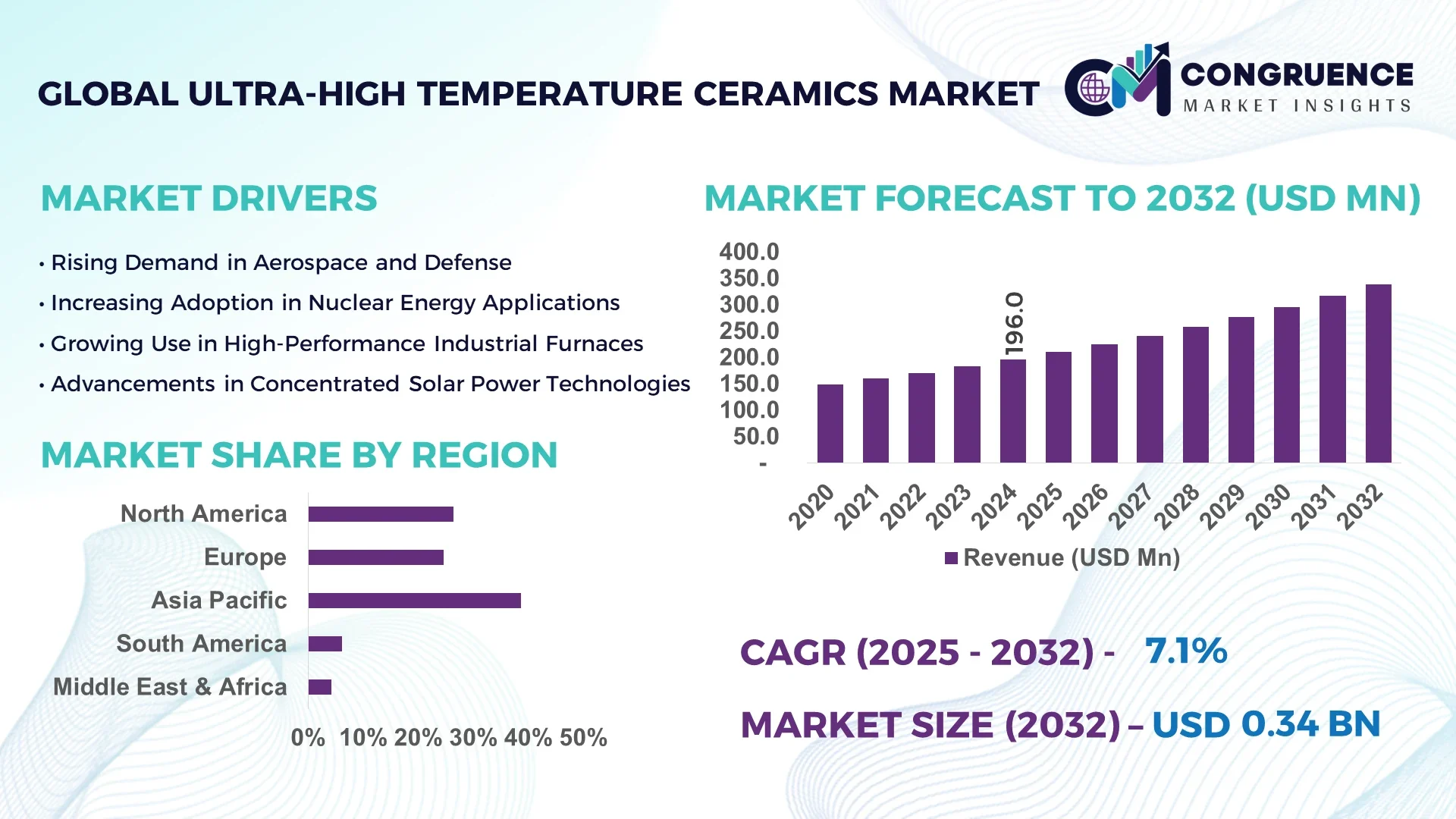

The Global Ultra-High Temperature Ceramics Market was valued at USD 196.0 Million in 2024 and is anticipated to reach a value of USD 339.3 Million by 2032 expanding at a CAGR of 7.1% between 2025 and 2032.

The United States leads global production capacity for ultra-high temperature ceramics (UHTCs), driven by extensive government and private-sector investments into hypersonic vehicle technologies, thermal protection systems, and defense-grade applications. U.S.-based research institutions and manufacturers have accelerated technological developments, particularly in materials engineering and plasma-assisted sintering methods, enabling faster prototyping and scalability of next-generation ceramic composites.

The Ultra-High Temperature Ceramics Market is characterized by rapidly advancing applications across aerospace, defense, nuclear energy, and advanced industrial manufacturing sectors. Aerospace and defense account for the largest segment, driven by the increasing deployment of UHTCs in hypersonic propulsion systems and thermal protection structures. Technological innovations such as spark plasma sintering (SPS), reactive hot pressing, and additive manufacturing are transforming the fabrication of ultra-refractory components. Regulatory frameworks focused on reducing high-temperature emissions and improving thermal efficiency in critical infrastructure have further stimulated market interest. Regional consumption is rising in Asia-Pacific due to expanding space programs and industrial furnace production, while North America remains at the forefront of R&D investments. Emerging trends include the integration of boride-based UHTCs with composite matrices, environmental barrier coatings for turbines, and the development of non-oxide ceramics with ultra-low thermal conductivity. The future outlook is strongly influenced by rising demand for sustainable, thermally stable materials in harsh operational environments.

Artificial Intelligence is revolutionizing the Ultra-High Temperature Ceramics Market by enhancing precision, reducing time-to-market, and significantly improving material performance prediction models. Through AI-enabled materials informatics, manufacturers are now able to simulate and optimize UHTC compositions without extensive laboratory testing. Machine learning algorithms are being used to identify ideal sintering conditions, predict oxidation resistance, and forecast mechanical behaviors under ultra-high thermal stress—tasks that traditionally required years of empirical validation. These innovations are enabling more targeted development of UHTCs for aerospace shielding, jet engine nozzles, and space re-entry modules.

Additionally, AI-driven digital twins are being used in high-temperature testing environments to replicate component behavior under extreme heat flux. This allows engineers to conduct accelerated failure analysis, optimize thermal shock resistance, and adjust design parameters in real-time. In manufacturing operations, AI is improving process control in techniques such as chemical vapor deposition and spark plasma sintering. These optimizations have led to efficiency improvements of over 20% in some facilities, reducing production waste while improving reproducibility. AI is also facilitating integration between CAD design tools and sintering simulation software, creating end-to-end smart manufacturing pipelines. The integration of AI is no longer an auxiliary enhancement but a core component of competitive strategy in the Ultra-High Temperature Ceramics Market.

“In April 2025, a U.S.-based aerospace material research firm implemented a deep learning algorithm to predict failure points in hafnium carbide-based ultra-high temperature ceramics used in hypersonic vehicle nose cones. The AI model, trained on over 5 million data points, achieved a 92% accuracy rate in forecasting material integrity degradation under temperatures exceeding 3500°C, significantly outperforming traditional finite element models.”

The Ultra-High Temperature Ceramics Market is being shaped by a confluence of industrial, technological, and geopolitical factors. Demand from high-performance sectors such as defense, hypersonic aerospace, and thermal energy systems continues to drive innovation and investment. Advances in sintering technologies and nanostructured material development are reducing production constraints and enabling broader applicability. Meanwhile, supply chain concerns related to rare-earth elements and stringent environmental regulations are prompting manufacturers to seek cost-efficient, sustainable production methods. Global competition is intensifying, with countries such as China, the U.S., and Germany accelerating efforts in research, defense-grade manufacturing, and thermal protection system development. These dynamics are creating a highly specialized yet globally competitive market environment.

The proliferation of hypersonic flight initiatives across the U.S., China, and Russia is a significant growth driver for the Ultra-High Temperature Ceramics Market. Hypersonic vehicles experience surface temperatures exceeding 3000°C, necessitating advanced thermal protection systems constructed from UHTCs like zirconium diboride and hafnium carbide. According to 2025 aerospace testing data, ultra-high temperature ceramics have outperformed traditional composites in withstanding ablation and structural degradation during Mach 6+ flight trials. Defense funding in the U.S. alone has earmarked over USD 2.8 billion toward hypersonic R&D programs utilizing ceramic matrix composites, catalyzing demand for thermally stable UHTCs.

The cost and technical complexity involved in processing ultra-high temperature ceramics remain substantial market restraints. High melting points, often above 3000°C, require specialized sintering equipment, such as hot isostatic pressing or spark plasma sintering, which are capital-intensive and energy-demanding. Additionally, maintaining material purity and minimizing porosity during fabrication adds to operational costs. Limited global access to critical raw materials like hafnium compounds and rare borides further increases production difficulty. These factors have constrained scalability, particularly for smaller manufacturers and emerging economies, thereby slowing broader adoption across industries beyond aerospace and defense.

Ultra-High Temperature Ceramics are increasingly being explored for use in next-generation nuclear reactors and concentrated solar power (CSP) systems. Their high thermal conductivity, corrosion resistance, and mechanical strength at extreme temperatures make them ideal candidates for reactor linings, control rods, and heat exchangers. The International Nuclear Energy Research Initiative has begun pilot-scale evaluations of UHTCs in gas-cooled reactor systems, demonstrating improved neutron resistance and heat transfer performance. As nations shift toward carbon-neutral energy solutions, UHTCs offer a viable path for enhancing the efficiency and lifespan of renewable thermal systems, opening new growth avenues beyond traditional markets.

One of the most pressing challenges in the Ultra-High Temperature Ceramics Market is the lack of global standards and insufficient long-term durability data under real-world conditions. While laboratory tests often validate performance under controlled high-heat scenarios, field deployment—particularly in aerospace and nuclear applications—requires reliability over extended operational cycles. Failures under thermal cycling, oxidation, and mechanical load in dynamic environments remain difficult to predict. The absence of internationally accepted testing protocols for evaluating such performance limits mass adoption and increases risk for end-users. This has resulted in hesitancy among stakeholders to integrate UHTCs into large-scale operational systems without further empirical validation.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Ultra-High Temperature Ceramics Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Shift Toward Additive Manufacturing in UHTC Fabrication: Advanced 3D printing methods such as binder jetting and laser sintering are being adopted for complex UHTC geometries, reducing material wastage by over 35%. This trend allows for near-net-shape production of intricate aerospace components and refractory linings with minimal post-processing. Adoption is particularly strong among U.S. defense contractors and research universities.

Increased R&D in Non-Oxide Ceramic Formulations: Recent R&D focus has shifted toward non-oxide UHTCs such as borides and carbides of transition metals, including zirconium and hafnium. These materials offer superior thermal shock resistance and lower emissivity, making them ideal for hypersonic flight. Research consortia in Europe and Asia have launched over 40 new projects in 2025 dedicated to these materials.

Adoption of AI for Real-Time Sintering Control: Manufacturers are leveraging AI to control sintering parameters in real-time, adjusting temperature, pressure, and dwell time to ensure optimal material density. Pilot programs in Germany and Japan have demonstrated improved batch consistency by up to 18%, reducing defect rates and enabling broader commercial-scale production.

The Ultra-High Temperature Ceramics Market is strategically segmented based on type, application, and end-user, each playing a crucial role in shaping market dynamics and innovation. Among the key segments, type-based categorization includes boride ceramics, carbide ceramics, nitride ceramics, and composites, each offering distinct performance profiles. Applications range from aerospace thermal shields to nuclear fuel containment, reflecting the materials’ resistance to extreme heat and environmental degradation. From an end-user perspective, aerospace and defense dominate due to the unique requirements of hypersonic technologies, while energy and industrial sectors are emerging as influential stakeholders. Segmentation enables targeted product development and aligns material characteristics with specific industry needs, supporting both commercial and strategic priorities.

In the Ultra-High Temperature Ceramics Market, boride ceramics—particularly zirconium diboride and hafnium diboride—hold the leading position due to their exceptional thermal conductivity, oxidation resistance, and suitability for aerospace thermal barrier systems. These materials are widely used in leading-edge structures of hypersonic vehicles and spacecraft nose cones. The fastest-growing type is carbide ceramics, notably silicon carbide (SiC) and hafnium carbide, driven by increasing demand in nuclear applications and concentrated solar power systems. These ceramics offer extreme hardness and thermal shock resistance, making them ideal for next-generation reactor components. Nitride ceramics, such as titanium nitride, are used in niche applications requiring high wear resistance and chemical stability. Composite ceramics, though less prevalent, are gaining traction in applications requiring a balance of mechanical toughness and thermal resistance. Overall, type segmentation allows industry players to tailor ceramic properties to end-use scenarios involving extreme operational environments and temperature thresholds exceeding 3000°C.

The aerospace segment is the leading application area in the Ultra-High Temperature Ceramics Market, driven by their critical use in thermal protection systems, propulsion components, and high-speed airframes. UHTCs are employed in structural components exposed to hypersonic airflow and re-entry conditions where material degradation must be minimized. The fastest-growing application is in nuclear energy systems, where UHTCs are being explored for fuel cladding, reactor linings, and high-efficiency heat exchangers. This growth is supported by increasing global interest in fourth-generation reactors that demand long-term stability under high neutron flux and extreme heat. Other notable applications include industrial furnaces, where UHTCs enhance the longevity and thermal reliability of high-temperature processing units. Additionally, concentrated solar power (CSP) systems are incorporating UHTCs into receiver tubes and reflectors to withstand thermal cycling and corrosive environments. This broadening scope of application underscores the versatility of ultra-high temperature ceramics across technologically advanced and energy-intensive domains.

Aerospace and defense remain the dominant end-user segment in the Ultra-High Temperature Ceramics Market, supported by significant investments in hypersonic flight, space exploration, and next-generation missile systems. These industries require UHTCs for critical applications like heat shields, propulsion systems, and high-performance structural components, where traditional materials cannot withstand operational extremes. The fastest-growing end-user is the energy sector, particularly nuclear and renewable thermal power systems, where UHTCs are being incorporated to enhance operational efficiency, safety, and durability under extreme conditions. Emerging reactor designs and thermal energy storage solutions are fueling demand for ceramic materials capable of withstanding prolonged exposure to corrosive, high-temperature environments. Industrial manufacturing also contributes to the market, with UHTCs being used in kiln linings, molds, and chemical processing equipment. These end-users benefit from the ceramics’ resistance to erosion, thermal shock, and corrosive agents. This end-user diversity illustrates the expanding reach of UHTCs beyond traditional aerospace applications into sectors critical to global energy and industrial sustainability.

Asia-Pacific accounted for the largest market share at 38.7% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

The Asia-Pacific region’s dominant position stems from robust industrialization, extensive manufacturing bases in China and India, and government-supported hypersonic and nuclear programs. China leads in UHTC consumption due to its aggressive investments in space and defense sectors, while Japan and South Korea contribute significantly through advanced R&D facilities. Meanwhile, North America’s rapid growth is being propelled by increasing investments in aerospace defense programs, technological advancements in material science, and the presence of leading UHTC manufacturers. Regulatory support for high-performance, heat-resistant materials in defense and clean energy sectors across the U.S. and Canada is further driving innovation. Each region presents unique consumption patterns, infrastructure development trajectories, and technological priorities that influence market positioning and long-term potential.

North America held approximately 26.4% of the global Ultra-High Temperature Ceramics Market in 2024, led primarily by the United States. The region benefits from advanced aerospace and defense sectors, which are major consumers of UHTCs for thermal protection systems and propulsion components. Ongoing initiatives like hypersonic missile development and reusable space launch systems are creating sustained demand. The U.S. government has issued multiple funding packages and defense contracts aimed at bolstering domestic UHTC manufacturing and research. Recent technological advancements include AI-enabled sintering and materials informatics platforms being adopted by key manufacturers. Additionally, regulatory push from U.S. agencies for safer and higher-performing thermal barrier systems in both civilian and military applications supports the region’s upward trajectory. Canada is also gaining traction with growing investment in nuclear energy and ceramic research institutions, supporting regional diversification.

Europe accounted for 19.6% of the global Ultra-High Temperature Ceramics Market in 2024. Germany leads the region, followed by the United Kingdom and France, with strong end-user demand from aerospace, defense, and clean energy sectors. The European Space Agency’s investment in reusable launch systems and hypersonic programs is fostering high-volume procurement of UHTCs. Regulatory bodies such as REACH and the European Commission’s sustainability directives are pushing manufacturers toward eco-efficient, high-performance materials. Technological innovations in Europe include additive manufacturing of UHTC components and hybrid ceramic composites for jet engines. Germany’s Fraunhofer Institutes and France’s national labs are spearheading collaborative research to improve oxidation resistance and scalability of UHTCs. Increasing adoption of these ceramics in industrial furnaces and thermal insulation applications further strengthens regional prospects.

Asia-Pacific holds the highest volume in the Ultra-High Temperature Ceramics Market with a 38.7% share in 2024. China is the largest consumer and producer in the region, driven by its rapidly growing space, defense, and industrial ceramics sectors. Japan follows closely, with a focus on nanostructured ceramic innovation and integration of UHTCs in nuclear and semiconductors. India is emerging as a high-growth country due to expanding thermal energy programs and government-backed defense initiatives. Infrastructure upgrades across industrial processing plants, along with smart manufacturing transitions, are accelerating UHTC demand. Regional tech hubs like Tokyo and Shenzhen are heavily invested in automation, robotics, and high-temperature materials engineering. Asia-Pacific’s dominance stems from cost-effective production, rising internal consumption, and aggressive government funding across strategic industries.

In 2024, South America contributed approximately 6.1% to the global Ultra-High Temperature Ceramics Market, with Brazil and Argentina being the key markets. Brazil leads the region with increased deployment of UHTCs in high-temperature processing units for cement, steel, and energy production. Growing investment in thermoelectric plants and concentrated solar power infrastructure has elevated demand for ceramic linings and heat-resistant components. Trade policies promoting import substitution and government-backed innovation funds are supporting domestic ceramic technology development. Argentina, though smaller in volume, is witnessing growing adoption of UHTCs in chemical processing and laboratory applications. The region benefits from increasing foreign investments and infrastructure modernization programs focused on industrial heat management.

Middle East & Africa accounted for around 4.2% of the global Ultra-High Temperature Ceramics Market in 2024. The UAE and South Africa are the region’s most active markets, driven by demand in oil & gas, metallurgy, and advanced construction applications. UAE’s transition toward high-efficiency refining processes has fueled the use of UHTCs in furnaces and high-pressure reactors. South Africa is investing in mining and materials technology hubs that promote localized production of refractory ceramics. Technological modernization in the form of automated thermal systems and predictive maintenance platforms is underway, primarily in the Gulf countries. Regional trade partnerships and low-tax zones are also incentivizing global ceramic manufacturers to establish distribution and R&D units in the area.

China – 29.4% Market Share

High production capacity, robust industrial demand, and government-backed space and defense programs.

United States – 24.6% Market Share

Strong end-user demand from aerospace and defense sectors, with advanced R&D capabilities and institutional funding.

The Ultra-High Temperature Ceramics Market is characterized by a moderately consolidated competitive landscape with approximately 50 to 60 active global manufacturers, including both established conglomerates and specialized ceramic technology firms. Competition is largely driven by innovation in processing technologies, thermal resistance performance, and integration with advanced manufacturing systems. Companies are actively engaged in strategic alliances, including cross-industry partnerships with aerospace, defense, and nuclear energy players to accelerate product development and application-specific customization.

Several key players have recently launched next-generation ceramic matrix composites optimized for hypersonic propulsion and ultra-high-temperature reactor components. Joint R&D programs, often supported by government or defense agencies, are enabling manufacturers to co-develop tailored ceramic solutions with leading space and defense institutions. Moreover, additive manufacturing and AI-powered process control systems are being adopted as differentiators in production efficiency and design complexity. The landscape is further influenced by regional expansion strategies, with companies entering Asia-Pacific and Middle East markets through local collaborations or new production facilities. Intellectual property, thermal performance benchmarks, and supply chain robustness are becoming decisive factors in sustaining market leadership.

CoorsTek Inc.

Zircar Zirconia Inc.

General Electric (GE)

UltraMet

Rauschert GmbH

ENrG Inc.

Advanced Ceramics Manufacturing

Fraser Advanced Information Systems

Applied Ceramics Inc.

Innovnano – Materials Advance

Technological innovation plays a pivotal role in shaping the growth trajectory of the Ultra-High Temperature Ceramics Market. One of the most significant advancements is spark plasma sintering (SPS), which allows ultra-dense ceramic structures to be fabricated at lower temperatures and in shorter cycles, reducing energy consumption by nearly 40% compared to conventional methods. Reactive hot pressing is also gaining traction, enabling improved bonding and microstructural uniformity in carbides and borides.

Another critical area of development is additive manufacturing (AM), which supports complex geometries and net-shape fabrication. In 2024, over 20% of newly developed UHTC aerospace components incorporated AM processes for reduced lead times and enhanced thermal resistance. Nano-engineered grain boundary modifications are enhancing the oxidation resistance and mechanical properties of UHTCs used in thermal barrier systems and nuclear reactors.

AI-integrated material informatics platforms are revolutionizing the discovery and optimization of ceramic formulations. These platforms simulate thousands of compositional variants under extreme heat and pressure, dramatically shortening development cycles. Moreover, innovations in non-oxide UHTCs such as hafnium carbide and zirconium diboride are enabling use at temperatures exceeding 3500°C, with improved resistance to erosion and ablation. Environmental barrier coatings (EBCs) are also advancing to enhance durability in aerospace and energy systems. These technologies collectively represent a shift toward high-precision, high-performance ceramic manufacturing tailored to mission-critical applications.

• In March 2024, UltraMet announced the successful testing of a hafnium carbide-based UHTC for hypersonic airframes, withstanding over 3600°C without structural degradation during simulated re-entry conditions.

• In August 2023, CoorsTek commissioned a new UHTC production facility in California equipped with automated SPS units, increasing its capacity for aerospace-grade ceramics by 28%.

• In December 2023, Rauschert GmbH launched a 3D-printed boride ceramic series for use in nuclear fuel assembly components, reducing component weight by 15% and improving thermal resistance.

• In February 2024, Applied Ceramics developed a proprietary environmental barrier coating for UHTC components in turbine engines, extending operational life by over 30% under thermal cycling stress.

The Ultra-High Temperature Ceramics Market Report provides a comprehensive analysis of the global market, covering its segmentation by product types, application areas, end-user industries, and regional landscapes. Product-wise, the report includes detailed insights into borides, carbides, nitrides, and advanced ceramic composites, highlighting their thermal, structural, and chemical performance profiles. It also explores application domains such as aerospace, nuclear energy, industrial manufacturing, and renewable energy systems, identifying specific use-cases and material performance requirements.

Geographically, the report examines key markets across Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, noting consumption trends, technology adoption, and regulatory influences. Particular focus is given to China and the United States as dominant players, along with fast-emerging markets in India, UAE, and Germany.

The report also includes technology-specific insights, such as AI-assisted ceramic design, advanced sintering processes, and additive manufacturing trends. Emerging segments such as environmental barrier coatings, UHTC-based composites for hypersonic flight, and reactor-grade ceramics are evaluated for future growth potential. Targeted at industry professionals, analysts, and decision-makers, this report serves as a strategic guide for understanding the present landscape and forecasting the evolution of this mission-critical market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 196.0 Million |

| Market Revenue (2032) | USD 339.3 Million |

| CAGR (2025–2032) | 7.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | CoorsTek Inc., Zircar Zirconia Inc., General Electric (GE), UltraMet, Rauschert GmbH, ENrG Inc., Advanced Ceramics Manufacturing, Fraser Advanced Information Systems, Applied Ceramics Inc., Innovnano – Materials Advance |

| Customization & Pricing | Available on Request (10% Customization is Free) |